主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2024, Vol. 32 ›› Issue (2): 199-209.doi: 10.16381/j.cnki.issn1003-207x.2021.2369

Jiliang Sheng1( ),Yi Huang1,2,Juchao Li1

),Yi Huang1,2,Juchao Li1

Received:2021-11-15

Revised:2022-03-08

Online:2024-02-25

Published:2024-03-06

Contact:

Jiliang Sheng

E-mail:shengjiliang@163.com

CLC Number:

Jiliang Sheng,Yi Huang,Juchao Li. Research on the Correlation Between Industry Risk and Industry Network Structure in China[J]. Chinese Journal of Management Science, 2024, 32(2): 199-209.

"

| 网络 | Y | X | X?Y | Y?X | 结论 | ||

|---|---|---|---|---|---|---|---|

| 临界值 | 检验值 | 临界值 | 检验值 | ||||

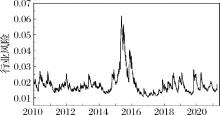

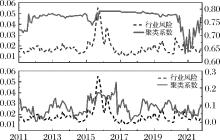

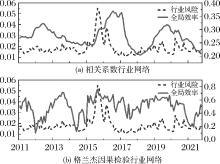

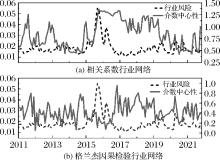

| 行业无向网络 | 行 业 风 险 | 聚类系数 | 3.93 | 0.15 | 3.92 | 0.07 | X?Y |

| 全局效率 | 3.92 | 1.34 | 3.92 | 3.83 | X?Y | ||

| 介数中心性 | 3.92 | 4.26 | 2.68 | 1.83 | X?Y | ||

| 行业有向网络 | 聚类系数 | 1.95 | 3.74 | 1.91 | 3.29 | X?Y | |

| 全局效率 | 3.93 | 1.14 | 2.01 | 2.48 | X?Y | ||

| 介数中心性 | 3.92 | 10.97 | 3.92 | 0.06 | X?Y | ||

"

"

"

"

"

"

| 无向网络 | 有向网络 | |||||

|---|---|---|---|---|---|---|

| 分位点(%) | 聚类系数(%) | 全局效率(%) | 介数中心(%) | 聚类系数(%) | 全局效率(%) | 介数中心(%) |

| 0.1 | 5.88* | 0.69 | 2.55 | 4.27 | 2.20* | 9.97* |

| 0.2 | 2.35* | 0.05 | 0.92 | 1.70 | 0.35 | 6.55* |

| 0.5 | 0.12 | 0.74 | 0.44 | 3.83 | 2.38* | 4.80* |

| 0.8 | 0.99 | 3.77* | 3.91 | 11.53 | 7.58* | 8.27* |

| 0.9 | 1.66 | 5.41* | 16.25* | 23.01* | 11.62* | 10.86* |

| 0.95 | 7.34* | 11.17 | 29.31* | 37.63* | 23.10* | 16.03 |

| 0.99 | 0.12 | 13.58* | 40.72* | 48.32* | 34.10* | 22.74* |

"

"

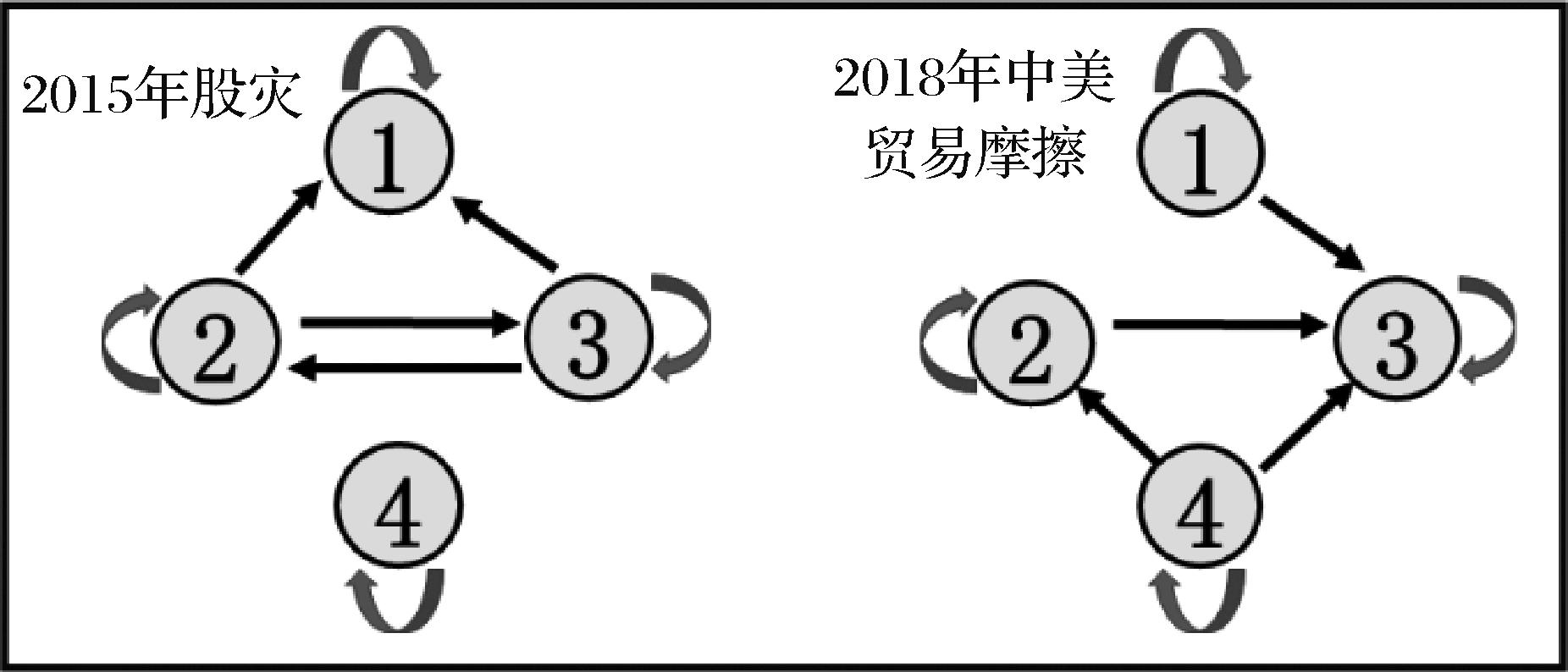

| 模块 | 连边关系 | 节点个数 | 内部期望连边 比率(%) | 实际内部连边 比率(%) | 从外部 接边数 | 向外发送 边数 | 模块角色 | |||

|---|---|---|---|---|---|---|---|---|---|---|

| M1 | M2 | M3 | M4 | |||||||

| M1 | 5 | 6 | 9 | 1 | 3 | 8.7 | 23.81 | 26 | 16 | 向内溢出 |

| M2 | 8 | 19 | 25 | 4 | 6 | 21.74 | 33.93 | 41 | 37 | 双向溢出 |

| M3 | 14 | 27 | 45 | 5 | 11 | 43.48 | 49.45 | 47 | 46 | 双向溢出 |

| M4 | 4 | 8 | 13 | 8 | 4 | 13.04 | 24.24 | 10 | 25 | 向外溢出 |

"

| 行业风险 | |||

|---|---|---|---|

| 模型(1) | 模型(2) | 模型(3) | |

| 聚类系数 | 0.121*** | ||

| (0.001) | |||

| 全局效率 | 0.227*** | ||

| (0.000) | |||

介数 中心性 | -0.189*** | ||

| (0.000) | |||

| 制造业PMI | -2.304 | -2.275 | -1.217 |

| (0.113) | (0.113) | (0.405) | |

非制造业PMI 商务活动 | 0.49 | 0.468 | -0.445 |

| (0.568) | (0.581) | (0.61) | |

国房 景气指数 | -3.508*** | -3.912*** | -2.903*** |

| (0.000) | (0.000) | (0.000) | |

| 常数项 | 19.463*** | 21.152*** | 15.659*** |

| (0.000) | (0.000) | (0.000) | |

| F | 14.36 | 15.46 | 16.06 |

| N | 129 | 129 | 129 |

| adj.R2 | 0.2945 | 0.2446 | 0.243 |

"

| 1 | 马永强,张志远.资本市场开放与过度负债企业去杠杆:来自“沪深港通”的经验证据[J].世界经济研究,2021(10):55-68+135. |

| Ma Y Q, Zhang Z Y. Capital market liberalization and deleveraging of over-indebted enterprises: evidence from “shang hai /shen zhen-hong kong stock connect”[J]. World Economy Studies,2021(10):55-68+135. | |

| 2 | Heiberger R H. Stock network stability in times of crisis ScienceDirect[J]. Physica A Statistical Mechanics &Its Applications, 2014, 393:376-381. |

| 3 | Tarasov V E. Fractional econophysics: market price dynamics with memory effects[J]. Physica A: Statistical Mechanics &Its Applications, 2020, 557:124865 |

| 4 | 李政,涂晓枫,卜林.金融机构系统性风险:重要性与脆弱性[J].财经研究,2019,45(2):100-112+152. |

| Li Z, Tu X F, Bu L.Systemic risks of financial institutions:importance and vulnerability[J].Journal of Finance and Economics,2019,45(2):100-112+152. | |

| 5 | 王博,齐炎龙.宏观金融风险测度:方法、争论与前沿进展[J].经济学动态,2015(4):149-158. |

| Wang B, Qi Y L.Macro financial risk measurement: methods, debates, and advances[J]. Economic Perspectives,2015(4):149-158. | |

| 6 | Huang X, Zhou H, Zhu H B. A framework for assessing the systemic risk of major financial institutions[J]. Journal of Banking and Finance,2009,33(11):2036-2049. |

| 7 | Acharya V V, Pedersen L H, Philippon T,et al. Measuring systemic risk[J]. The Review of Financial Studies,2017,30(1):2-47. |

| 8 | Brownlees C, Engle R F. SRISK:a conditional capital shortfall measure of systemic risk[J]. The Review of Financial Studies,2017,30(1): 48-79. |

| 9 | Adrian T, Brunnermeier M K. CoVaR[J]. American Economic Review, 2016, 106(7):1705-1741. |

| 10 | Feng S, Huang S, Qi Y, et al. Network features of sector indexes spillover effects in china: a multi-scale view[J]. Physica A: Statistical Mechanics & Its Applications, 2018, 496: 461-473 |

| 11 | Wu F, Zhang D, Zhang Z. Connectedness and risk spillovers in China’s stock market: a sectoral analysis[J]. Economic Systems, 2019, 43(3-4): 100718. |

| 12 | Li Y, Zhuang X, Wang J, et al. Analysis of the impact of Sino-US trade friction on China’s stock market based on complex networks[J]. The North American Journal of Economics and Finance, 2020, 52: 101185. |

| 13 | 刘超,钱存,罗春燕.基于复杂网络的行业动态演化与证券市场风险相关性研究——来自2007—2019年28个行业数据的证据[J].管理评论,2021,33(3):29-40. |

| Liu C, Qian C, Luo C Y. Research on the correlation between industry dynamic evolution and securities market risk based on complex network[J].Management Review,2021,33(3):29-40. | |

| 14 | Morgan J P .Risk metrics:technical document [M].Chichester:John Wiley & Son,1994:1-13. |

| 15 | Mantegna R N. Hierarchical structure in financial markets[J]. The European Physical Journal B-Condensed Matter and Complex Systems, 1999, 11(1):193-197. |

| 16 | Tumminello M, Aste T, Matteo T D, et al. A tool for filtering information in complex systems[J]. Proceedings of the National Academy of Sciences of the United States of America, 2005, 102(30):10421-10426. |

| 17 | Ge T, Cui Y, Lin W, et al. Characterizing time series: when granger causality triggers complex networks[J]. New Journal of Physics, 2012, 14:083028. |

| 18 | Seth A K. Granger causality[J]. Scholarpedia, 2007, 2(7):1667. |

| 19 | 刘海飞,柏巍,李冬昕,等.沪港通交易制度能提升中国股票市场稳定性吗?—基于复杂网络的视角[J].管理科学学报,2018,21(1):97-110. |

| Liu H F, Bo W, Li D X, et al.Does Shanghai-Hong Kong stock connect trading mechanism improve the stability of chinesestockmarket?a complex network perspective[J]. Jounal of Management Sciences in China, 2018,21(1), 97-110. | |

| 20 | White H C, Boorman S A, Breiger R L. Social structure from multiple networks. I. blockmodels of roles and positions[J]. American Journal of Sociology, 1976, 81(4):730-780. |

| 21 | Zhang W, Zhuang X, Wu D. Spatial connectedness of volatility spillovers in G20 stock markets: based on block models analysis[J]. Finance Research Letters,2020, 34:101274. |

| 22 | Kritzman M, Li Y. Skulls, financial turbulence, and risk management[J]. Financial Analysts Journal, 2010,66(5):30-41. |

| 23 | 沈丽,刘媛,李文君.中国地方金融风险空间关联网络及区域传染效应:2009-2016[J].管理评论,2019,31(8):35-48. |

| Shen L, Liu Y, Li W J. China’s regional financial risk spatial correlation network and regional contagion effect:2009-2016[J].Managementreview,2019,31(8):35-48. |

| [1] | FAN Hong, CHEN Nai-xi. Multi-stage Risk Contagion Mechanism and Empirical Study Based on Spillover Effect [J]. Chinese Journal of Management Science, 2023, 31(6): 39-48. |

| [2] | LI Bing-qing, ZHANG Xiao-yuan. Study on the Internal Risk Contagion Mechanism of Enterprise Groups Based on Network Structure [J]. Chinese Journal of Management Science, 2023, 31(5): 20-28. |

| [3] | WANG Lei, , LI Shou-wei, HE Jian-min, HOU De-fei. The Behavior Spread of “Buying the Winners” of Real Estate Investors under the Disturbance of Internet Public Opinion [J]. Chinese Journal of Management Science, 2023, 31(1): 56-69. |

| [4] | WANG Mei-qiang, HUANG Yang. A Neutral Two-stage Cross-efficiency Evaluation Approach [J]. Chinese Journal of Management Science, 2022, 30(11): 229-238. |

| [5] | WANG Wei-ming, XU Hai-yan, ZHU Jian-jun. Interactive Large-scale Group Evaluation Method Based on Complex Network and Linguistic Information [J]. Chinese Journal of Management Science, 2022, 30(11): 260-271. |

| [6] | LIU Chao, GUO Ya-dong. Systemic Financial Risk Spillover and Its Topology Analysis of Sector Indexes in China under a Multi-Scale View [J]. Chinese Journal of Management Science, 2022, 30(10): 46-59. |

| [7] | MO Dong-xu, ZHENG Tian-dan. Research on Portfolio Optimization Based on Complex Network [J]. Chinese Journal of Management Science, 2021, 29(5): 25-33. |

| [8] | MA Qian-ting, YANG Wen-ke, HE Jian-min. Investigating Bank-Firm Systemic Risk within a Multilayer Network [J]. Chinese Journal of Management Science, 2021, 29(12): 1-14. |

| [9] | XIE Chi, HU Xue-jing, WANG Gang-jin. Dynamic Evolution and Market Robustness of Chinese Stock Market in the Past 10 Years of the Financial Crisis: An Empirical Research Based on Complex Network Perspective [J]. Chinese Journal of Management Science, 2020, 28(6): 1-12. |

| [10] | CHEN Ting-qiang, ZHOU Wen-jing, TONG Mao-di, LIU Hai-fei. Research on the Model of Inter-bank Credit Risk Contagion by Fusing CDS Networks [J]. Chinese Journal of Management Science, 2020, 28(6): 24-37. |

| [11] | LI Shou-wei, WEN Shi-hang, WANG Lei, HE Jian-min, GONG Chen. Evolution Characteristics of Financial Institutions' Interrelationships from the Perspective of Multilayer Network [J]. Chinese Journal of Management Science, 2020, 28(12): 35-43. |

| [12] | ZHANG Qi, LI Yan, WANG Ge, ZHU Li-jing, HU Ying, WANG Le. Credit Risk Modeling and Analysis for Crowdfunding Market of Electric Vehicle Charging Pile based on Complex Network [J]. Chinese Journal of Management Science, 2019, 27(8): 66-74. |

| [13] | YANG Xiang-hao, DUAN Zhe-zhe, WANG Xiao-li. Enterprise Tacit Knowledge Propagation SIR Model with Consideration of Forgetting Mechanisms [J]. Chinese Journal of Management Science, 2019, 27(7): 195-202. |

| [14] | ZOU Xing-qi, YANG Qing. R&D Project Portfolio Selection Based on Domination and Diffusion Relationship in the Project Network [J]. Chinese Journal of Management Science, 2019, 27(4): 198-209. |

| [15] | PANG Xiao-bo, WANG Ke-da. The Identification of Potential Infectious Source of International Financial Crisis and the Analysis of Their Contagiousness [J]. Chinese Journal of Management Science, 2018, 26(3): 43-50. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||