主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2024, Vol. 32 ›› Issue (4): 1-13.doi: 10.16381/j.cnki.issn1003-207x.2021.0382

Zhongfei Li1,Qi Zhou2( )

)

Received:2021-02-26

Revised:2021-04-20

Online:2024-04-25

Published:2024-04-25

Contact:

Qi Zhou

E-mail:zhouqi@scut.edu.cn

CLC Number:

Zhongfei Li,Qi Zhou. An Industry Allocation Model Based on BL Model and Complex Network[J]. Chinese Journal of Management Science, 2024, 32(4): 1-13.

"

| 变量 | 含义 | 矩阵维度 | 变量 | 含义 | 矩阵维度 |

|---|---|---|---|---|---|

| 期望收益率向量 | 主观观点的信心误差矩阵 | ||||

| 调整系数 | 市场均衡收益率 | ||||

| 资产的市值权重 | 主观观点收益矩阵 | ||||

| 投资者主观观点矩阵 | 历史收益率的协方差矩阵 |

"

"

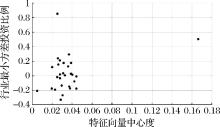

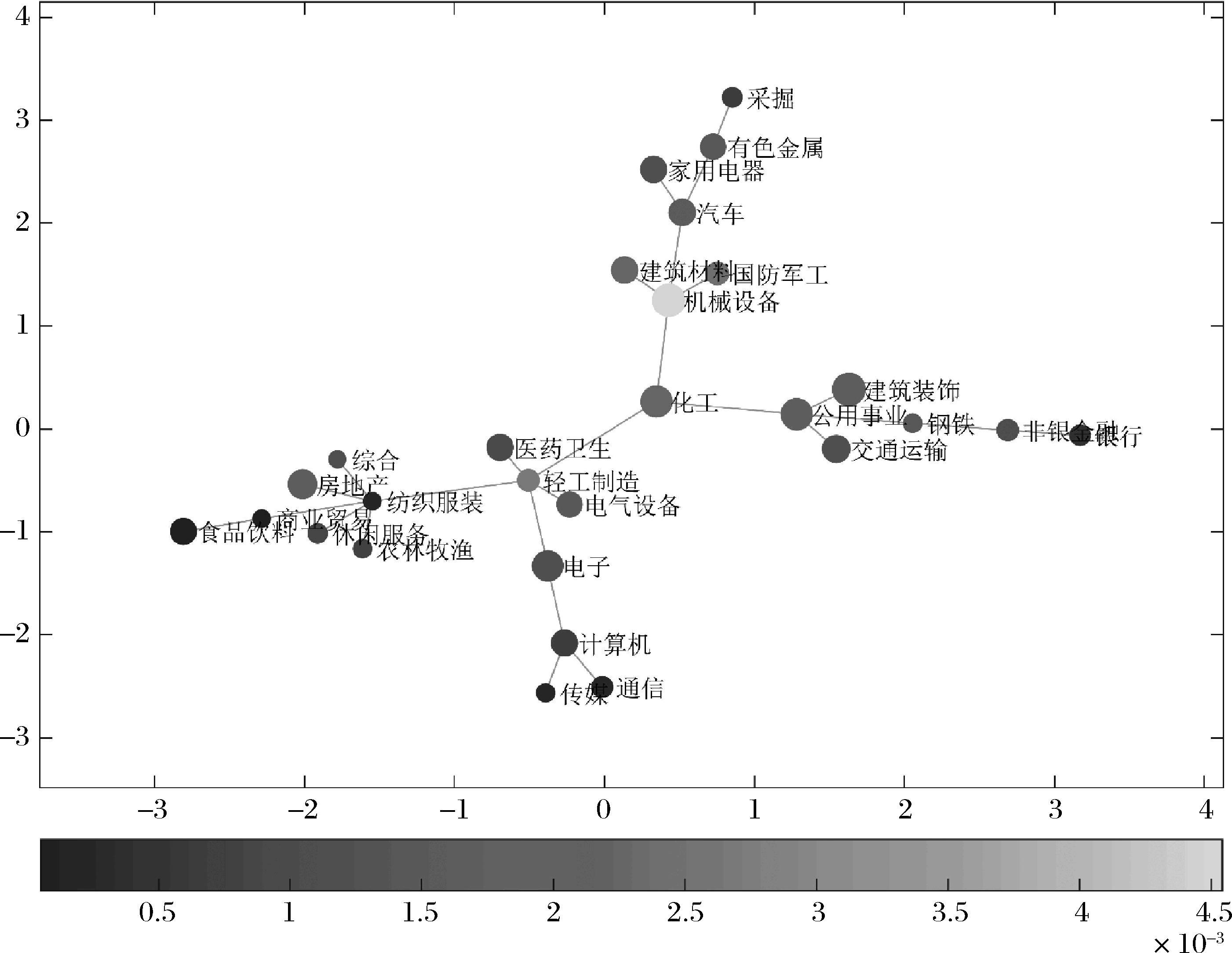

| 中间中心度行业 | 中心度极值行业 | 中心度稳定的行业 | 中心度波动较大的行业 | 中间中心度稳定的行业 |

|---|---|---|---|---|

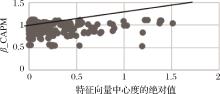

| 传媒,农林牧渔,汽车,食品饮料,通信,医药生物,综合 | 化工,银行,建筑,材料,有色金属,机械设备,非银金融 | 传媒,电气设备,食品饮料,交通运输,通信,医药生物,综合 | 房地产,纺织服装,非银金融,机械设备,建筑材料,银行,有色金属 | 传媒,食品饮料,通信,医药卫生,综合 |

"

"

"

| 变量 | |||

|---|---|---|---|

-0.0152 (-2.41)** | -0.0143 (-3.85)*** | -0.0152 (-2.96)*** | |

0.4728 (3.29)*** | 0.3679 (4.25)*** | 0.3622 (3.47)*** | |

| N | 336 | 336 | 336 |

| 0.169 | 0.226 | 0.184 |

"

"

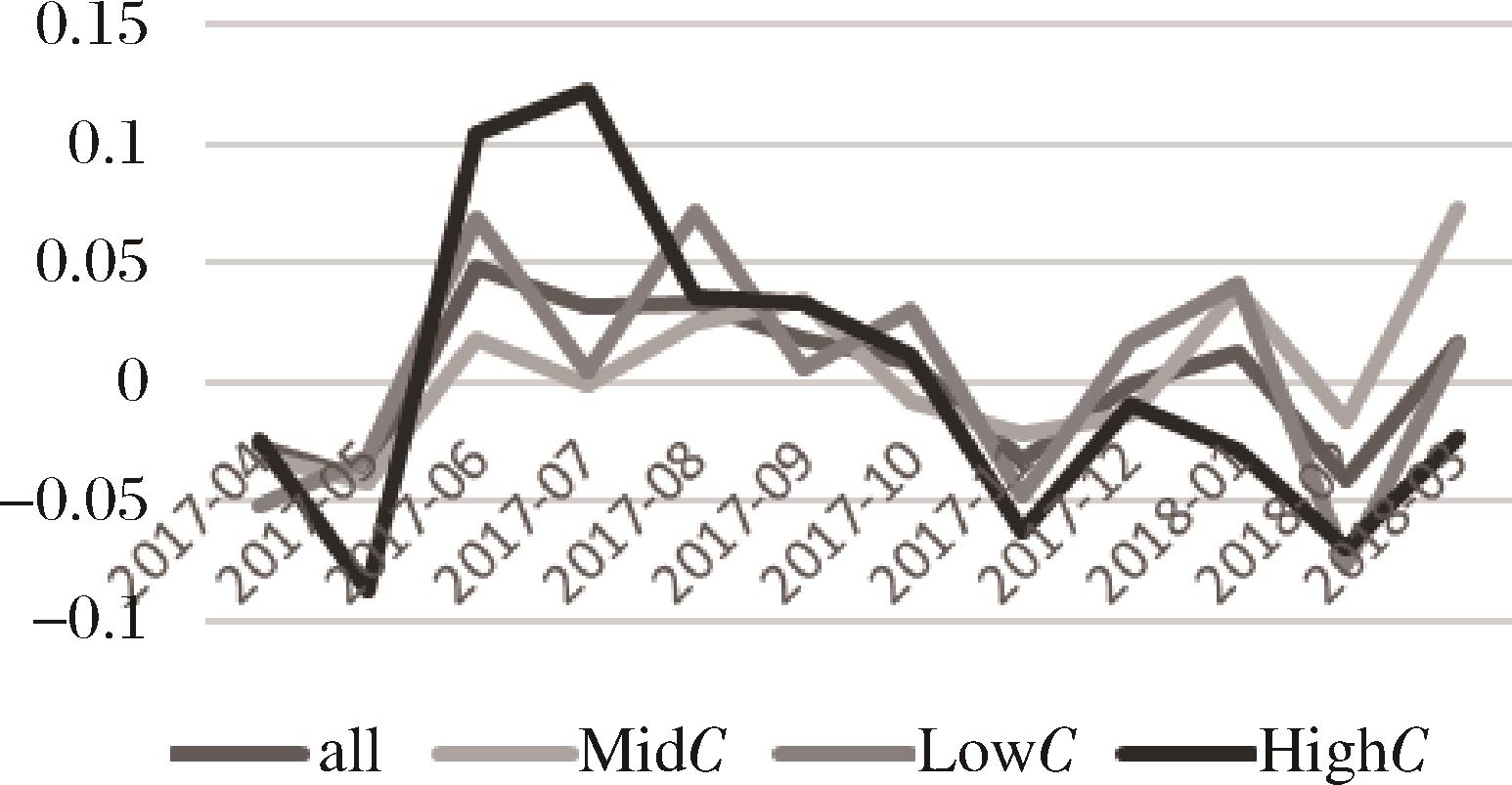

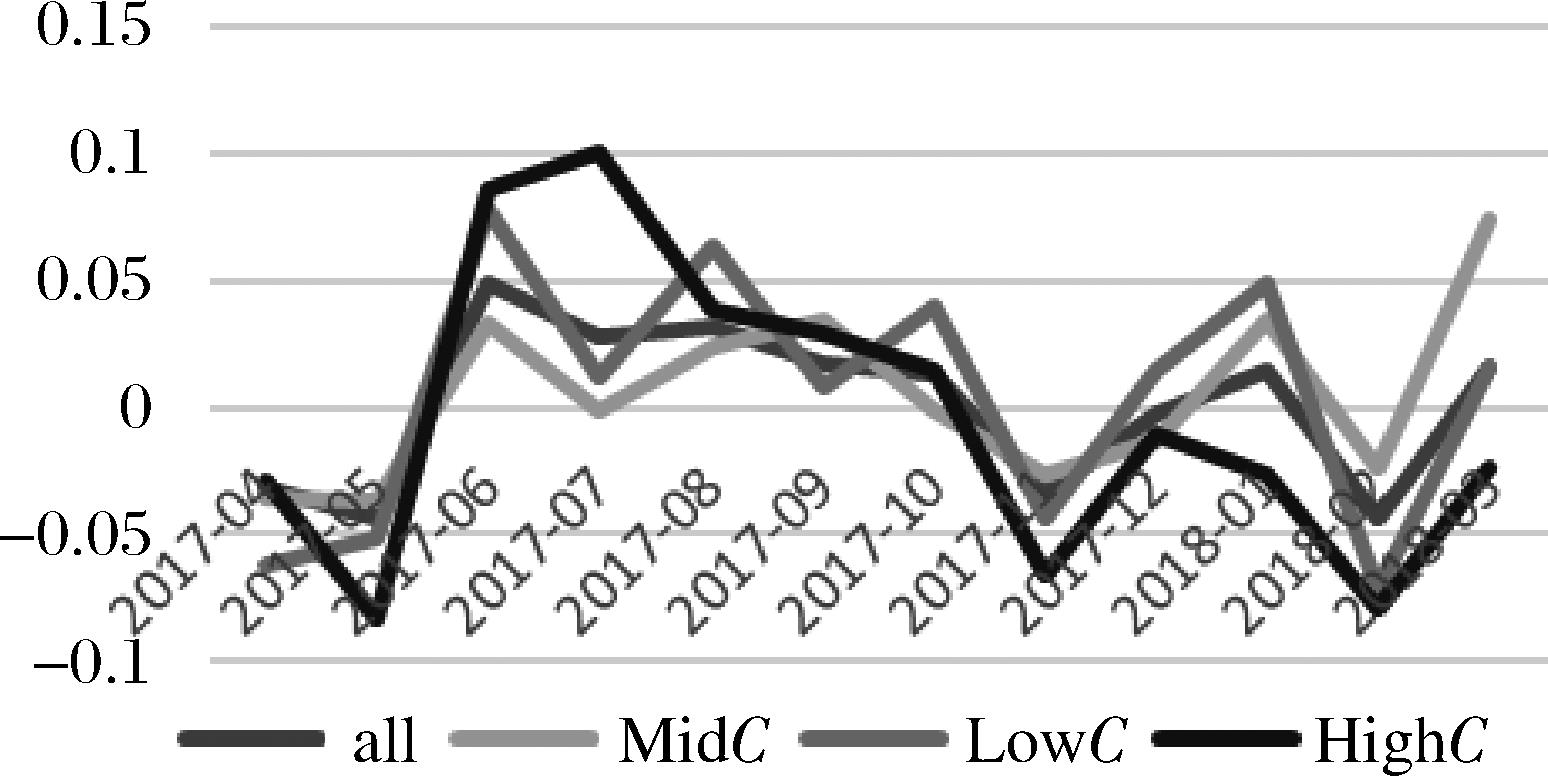

| 时间 | 1/N模型 | MV模型 | Min-V模型 | BL(GARCH)模型 | BL(MA)模型 | BL(SVM)模型 |

|---|---|---|---|---|---|---|

| 2017-04 | -0.0351 | -0.09004 | -0.05681 | -0.0316 | -0.02336 | -0.02674 |

| 2017-05 | -0.0469 | -0.0509 | 0.068128 | -0.0428 | -0.01639 | -0.04011 |

| 2017-06 | 0.0432 | 0.050526 | 0.217576 | 0.0490 | 0.039031 | 0.047659 |

| 2017-07 | 0.0113 | 0.155548 | 0.076737 | 0.0276 | 0.028705 | 0.031279 |

| 2017-08 | 0.029 | 0.004552 | -0.04298 | 0.0313 | 0.038751 | 0.03283 |

| 2017-09 | 0.0142 | -0.1745 | 0.012375 | 0.0176 | 0.015803 | 0.01811 |

| 2017-10 | 0.004 | 0.083156 | 0.074148 | 0.0134 | 0.009781 | 0.008235 |

| 2017-11 | -0.0355 | -0.47025 | 0.083917 | -0.0340 | -0.03495 | -0.03299 |

| 2017-12 | -0.005 | -0.03433 | -0.04684 | -0.0023 | 0.000196 | -0.00133 |

| 2018-01 | 0.0105 | 0.100866 | 0.150276 | 0.0144 | 0.012852 | 0.012724 |

| 2018-02 | -0.0431 | -0.04685 | -0.04539 | -0.0436 | -0.0155 | -0.04014 |

| 2018-03 | -0.0307 | 0.04185 | -0.46597 | 0.0165 | 0.020901 | 0.0161 |

| 平均收益率 | -0.0070 | -0.03586 | 0.002098 | 0.0013 | 0.0063 | 0.0021 |

| 夏普比率 | -0.2314 | -0.2187 | 0.0123 | 0.0408 | 0.2581 | 0.0704 |

| 方差 | 0.000917 | 0.026894 | 0.02905 | 0.000998 | 0.000599 | 0.00092 |

"

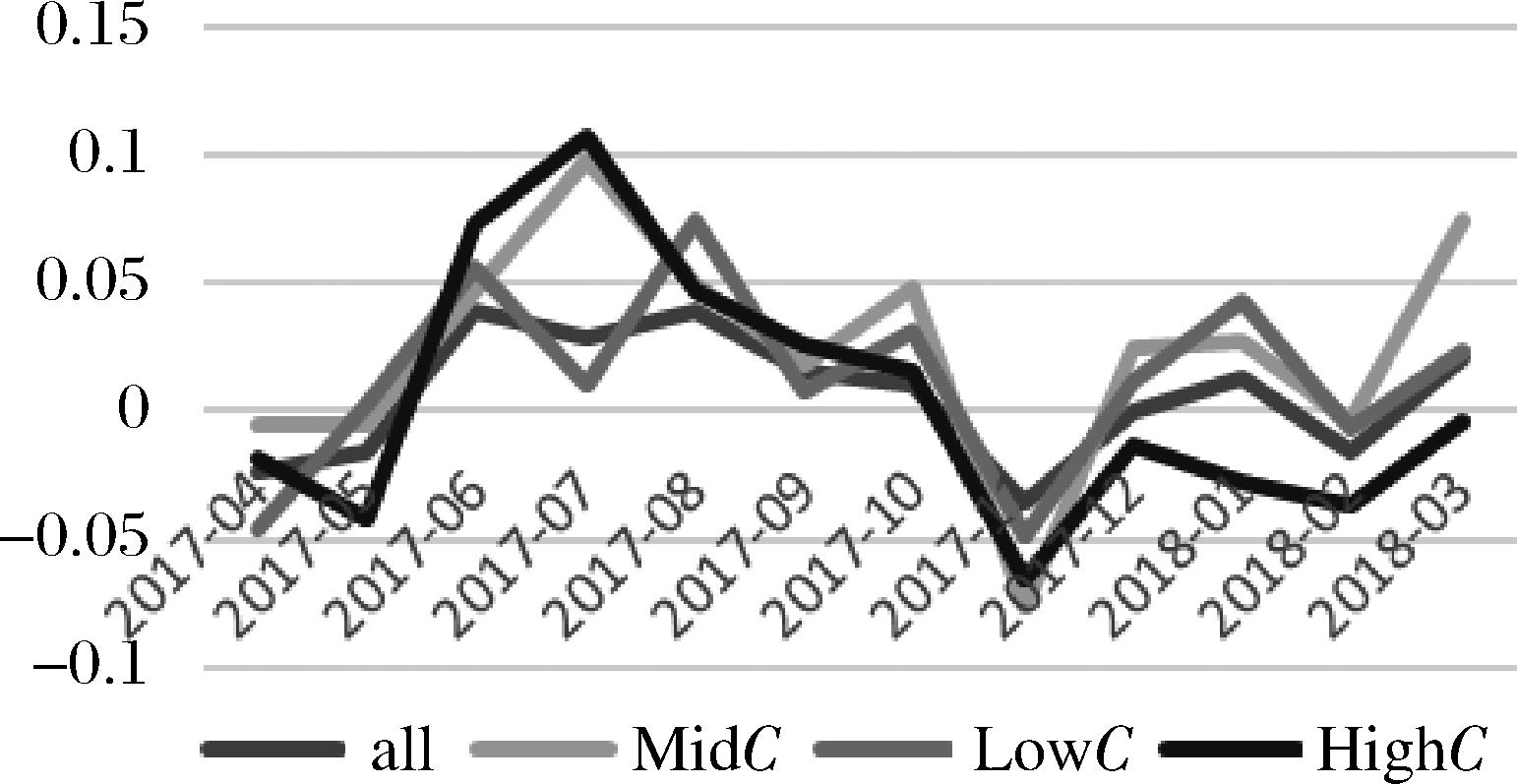

| Strategy | Average Returns | Sharpe Ratio | Omega | Variance |

|---|---|---|---|---|

| Tradition | ||||

| 1/N | -0.00701 | -0.2314 | 0.5716 | 0.000917 |

| BL(GARCH) | 0.001289629 | 0.0408 | 0.5239 | 0.000997594 |

| BL(MA) | 0.006319 | 0.2581 | 1.8407 | 0.000599 |

| BL(SVM) | 0.0021342 | 0.0704 | 0.5415 | 0.000919635 |

| 1/N+Network | ||||

| 1/N- MidC | 0.001721157 | 0.0564 | 1.1388 | 0.000930666 |

| 1/N- LowC | -0.008525509 | -0.3277 | 0.4288 | 0.000676746 |

| 1/N- HighC | -0.003056117 | -0.098 | 0.7768 | 0.000972405 |

| 1/N-HSR | -0.004946272 | -0.1792 | 0.5874 | 0.000802374 |

| BL+Network | ||||

| BL(GARCH )-MidC | 0.00518347 | 0.15 | 0.5925 | 0.001193866 |

| BL(GARCH)- LowC | 0.004308787 | 0.0856 | 0.551 | 0.002531251 |

| BL(GARCH) -HighC | -0.004333741 | -0.0723 | 0.4557 | 0.003595042 |

| BL(GARCH)-HSR | 0.001305736 | 0.03056 | 0.4938 | 0.003078329 |

| BL(MA)-MidC | 0.024765016 | 0.5466 | 4.2366 | 0.002052442 |

| BL(MA)-LowC | 0.013375332 | 0.3654 | 0.7218 | 0.001340048 |

| BL(MA)-HighC | 0.004961713 | 0.0978 | 0.5625 | 0.002572639 |

| BL(MA)-HSR | 0.00812953 | 0.1972 | 0.6146 | 0.001973671 |

| BL(SVM) -MidC | 0.004373806 | 0.1311 | 0.5818 | 0.001113676 |

| BL(SVM)-LowC | 0.004095918 | 0.0871 | 0.5535 | 0.002212517 |

| BL(SVM)-HighC | 6.70765E-05 | 0.001 | 0.5007 | 0.004228955 |

| BL(SVM)-HSR | 0.001539855 | 0.0274 | 0.0516 | 0.002965301 |

"

"

"

"

"

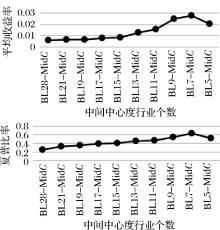

| Strategy | Average Returns | Sharpe Ratio | Omega | Variance |

|---|---|---|---|---|

| Strategy of 1/N in Network | ||||

| 1/N-MidC-9 | 0.001721 | 0.0564 | 1.13884 | 0.000930666 |

| 1/N-MidC-7 | 0.005087 | 0.148 | 1.417339 | 0.001180472 |

| 1/N-MidC-5 | 0.00835 | 0.2065 | 1.656672 | 0.00163459 |

| Strategy of BL in Network | ||||

| BL(MA)-MidC-9 | 0.024765 | 0.5466 | 4.236592 | 0.002052442 |

| BL(MA)-MidC-7 | 0.027959 | 0.64 | 6.103315 | 0.001908212 |

| BL(MA)-MidC-5 | 0.020599 | 0.5177 | 4.726464 | 0.001584634 |

"

| 1 | Li D, Ng W L. Optimal dynamic portfolio selection: multi-period mean‐variance formulation[J]. Mathematical Finance, 2000, 10(3): 387–406. |

| 2 | Zhou X Y, Li D. Continuous-time mean-variance portfolio selection: a stochastic LQ framework[J]. Applied Mathematics & Optimization, 2000, 42(1): 19-33. |

| 3 | Yao H, Li Z, Li D. Multi-period mean-variance portfolio selection with stochastic interest rate and uncontrollable liability[J]. European Journal of Operational Research, 2016, 252(3): 837-851. |

| 4 |

黄金波, 吴莉莉, 尤亦玲. 非对称Laplace分布下的均值-VaR模型[J].中国管理科学, 2020, DOI:10.16381/j.cnki.issn1003-207x.2019.1681 .

doi: 10.16381/j.cnki.issn1003-207x.2019.1681 |

|

Huang J B, Wu L L, You Y L. Mean-VaR model based on the asymmetric Laplace distribution[J]. Chinese Journal of Management Science, 2020, DOI:10.16381/j.cnki.issn1003-207x.2019.1681 .

doi: 10.16381/j.cnki.issn1003-207x.2019.1681 |

|

| 5 | Merton R C. On estimating the expected return on the market: an exploratory investigation[J]. Journal of Financial Economics, 1980, 8(4): 323-361. |

| 6 | De Miguel V, Garlappi L, Uppal R. Optimal versus naive diversification: how inefficient is the 1/N portfolio strategy?[J]. Review of Financial Studies, 2009, 22(5): 1915-1953. |

| 7 | Mandere E O. Financial networks and their applications to the stock market[D]. Bowling Green State University, 2009. |

| 8 | Peralta G, Zareei A. A network approach to portfolio selection[J]. Journal of Empirical Finance, 2016, 38: 157-180. |

| 9 | 黄乃静, 张冰洁, 郭冬梅, 等. 中国股票市场行业间金融传染检验和风险防范[J]. 管理科学学报, 2017(12): 19-28. |

| Huang N J, Zhang B J, Guo D M, et al. Industry-level financial contagion of the Chinese stock market and risk control[J]. Journal of Management Science in China, 2017(12): 19-28. | |

| 10 | 肖琴. 复杂网络在股票市场相关分析中的应用[J]. 中国管理科学, 2016, 24(S1): 470-474. |

| Xiao Q. Application of the complex network in stock market board analysis[J]. Chinese Journal of Management Science, 2016, 24(S1): 470-474. | |

| 11 | 李政, 梁琪, 涂晓枫.我国上市金融机构关联性研究——基于网络分析法[J]. 金融研究, 2016(8): 95-110. |

| Li Z, Liang Q, Tu X F. The connectedness of chinese listed financial institutions:a study based on network analysis[J]. Journal of Financial Research, 2016(8): 95-110. | |

| 12 | 胡振华, 覃子龙, 杨燕. 基于互信息的深证股票复杂网络拓扑性质分析[J]. 统计与决策, 2016(20): 160-163. |

| Hu Z H, Qin Z L, Yang Y. Topological property analysis of Shenzhen stock with complex network based on mutual information[J]. Statistics & Decision, 2016(20): 160-163. | |

| 13 | 鲍勤, 孙艳霞. 网络视角下的金融结构与金融风险传染[J]. 系统工程理论与实践, 2014, 34(9): 2202-2211. |

| Bao Q, Sun Y X. Financial structure and financial contagion from the network perspective[J]. System Engineering Theory and Practice, 2014, 34(9): 2202-2211. | |

| 14 | 杨海军, 胡敏文. 基于核心-边缘网络的中国银行风险传染[J]. 管理科学学报, 2017(10): 49-61. |

| Yang H J, Hu M W. Risk contagion of Chinese interbank markets based on core-periphery network[J]. Journal of Management Science in China, 2017(10): 49-61. | |

| 15 | 张来军, 杨治辉, 路飞飞. 基于复杂网络理论的股票指标关联性实证分析[J]. 中国管理科学, 2014, 22(12): 85-92. |

| Zhang L J, Yang Z H, Lu F F. Empirical analysis of relevance of stock indicators based on complex network theory[J]. Chinese Journal of Management Science, 2014, 22(12): 85-92. | |

| 16 | 隋聪, 王宗尧. 银行间网络的无标度特征[J]. 管理科学学报, 2015, 18(12): 18-26. |

| Sui C, Wang Z Y. Interbank network scale-free characteristics[J]. Journal of Management Science in China, 2015, 18(12): 18-26. | |

| 17 | 钟韬, 彭勤科. 基于社会网络分析的投资组合优选方法[J]. 系统工程理论与实践, 2015, 35(12): 3017-3024. |

| Zhong T, Peng Q K. Portfolio selection method based on social network analysis[J]. System Engineering-Theory & Practice, 2015, 35(12): 3017-3024. | |

| 18 | 庄新田, 黄小原. 金融网络下投资组合风险及最优规模研究[J]. 管理科学学报, 2004(3): 54-58. |

| Zhuang X T, Huang X Y. Research on investment portfolio risk and optimization scale under financial networks[J]. Journal of Management Science in China, 2004(3): 54-58. | |

| 19 | Diebold F X, Yilmaz K. On the network topology of variance decompositions: measuring the connectedness of financial firms [J]. Journal of Econometrics, 2011, 182(1): 119-134. |

| 20 | Barigozzi M, Brownlees C. Nets: network estimation for time series[J]. Journal of Applied Econometrics, 2019, 34(3): 347-364. |

| 21 | Peralta G. Network-Based measures as leading indicators of market instability: the case of the spanish stock market[J]. Social Science Electronic Publishing, 2015. |

| 22 | Billio M, Getmansky M, Lo A W, et al. Econometric measures of connectedness and systemic risk in the finance and insurance sectors[J]. Journal of Financial Economics, 2012, 104(3): 535-559. |

| 23 | Dees B S, Stanković L, Constantinides A G, et al. Portfolio cuts: a graph-theoretic framework to diversification[C]//ICASSP 2020-2020 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP). IEEE, 2020: 8454-8458. |

| 24 | Cerqueti R, Lupi C. Risk Measures on networks and expected utility[J]. Reliability Engineering & System Safety, 2016, 155: 1-8. |

| 25 | Huang S, Chow N S C, Xu R, et al. Analyzing the Hong Kong stock market structure: a complex network approach[R]. Working Paper, SSRN 2633433, 2015. |

| 26 | Li H, An H, Fang W, et al. Global energy investment structure from the energy stock market perspective based on a Heterogeneous Complex Network Model[J]. Applied Energy, 2017, 194: 648-657. |

| 27 | Pozzi F, Di M T, Aste T. Spread of risk across financial markets: better to invest in the peripheries [J]. Scientific Reports, 2013, 3(3): 1665. |

| 28 | Puerto J, Rodríguez-Madrena M, Scozzari A. Clustering and portfolio selection problems: a unified framework[J]. Computers & Operations Research, 2020, 117: 104891. |

| 29 | Alvin C M L, Ashish A, Prabhudev K, et al. Network analysis of search dynamics: the case of stock habitats[J]. Management Science, 2017, 63(8): 2667-2687. |

| 30 | Zareei A. Network origins of portfolio risk[J]. Journal of Banking & Finance, 2019, 109: 105663. |

| 31 | 张维, 武自强, 张永杰, 等. 基于复杂金融系统视角的计算实验金融: 进展与展望[J]. 管理科学学报, 2013, 16(6): 85-94. |

| Zhang W, Wu Z Q, Zhang Y J, et al. Agent-based computational finance on complex financial system perspective: progress and prospects[J]. Journal of Management Science in China, 2013, 16(6): 85-94. | |

| 32 | Glasserman P, Young H P. How likely is contagion in financial networks?[J]. Journal of Banking & Finance, 2015, 50: 383-399. |

| 33 | Newman M E J. The mathematics of networks[J]. The New Palgrave Encyclopedia of Economics, 2008, 2(2008): 1-12. |

| 34 | Black F, Litterman R. Global portfolio optimization[J]. Financial Analysts Journal, 1992: 28-43. |

| 35 | Fama E F, Macbeth J D. Risk, return, and equilibrium: some empirical tests[J]. Journal of Political Economy, 1973, 81(3): 607-636. |

| 36 | Mantegna R N. Hierarchical structure in financial markets[J]. The European Physical Journal B, 1999, 11(1): 193-196. |

| 37 | 尹群耀, 何建敏, 卞曰瑭. 基于STSA的中国股市的聚集效应研究——以上证50指数为例[J]. 系统工程, 2013(1): 10-17. |

| Yin Q Y, He J M, Bian R T. Aggregation effect of the china stock market based on STSA method:take SSE 50 Index as an example[J]. Systems Engineering, 2013(1): 10-17. | |

| 38 | 欧阳红兵, 刘晓东. 中国金融机构的系统重要性及系统性风险传染机制分析——基于复杂网络的视角[J]. 中国管理科学, 2015, 23(10): 30-37. |

| Ouyang H B, Liu X D. An analysis of the systemic importance and systemic risk contagion mechanism of China’s financial institutions based on network analysis[J]. Chinese Journal of Management Science, 2015, 23(10): 30-37. | |

| 39 | Keating C, Shadwick W F. A universal performance measure[J]. Journal of Performance Measurement, 2002, 6(3): 59-84. |

| 40 | Idzorek T. A step-by-step guide to the black-litterman model: incorporating user-specified confidence levels[J]. Forecasting Expected Returns in the Financial Markets, 2007: 17-38. |

| 41 | Jones C M, Lamont O A. Short-sale constraints and stock returns[J]. Journal of Financial Economics, 2002, 66(2-3): 207-239. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||