主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (6): 1-13.doi: 10.16381/j.cnki.issn1003-207x.2022.1247

Longbing Xu1,2,3( ), Wenbin Wu1

), Wenbin Wu1

Received:2022-06-07

Revised:2023-04-17

Online:2025-06-25

Published:2025-07-04

Contact:

Longbing Xu

E-mail:xlb@mail.shufe.edu.cn

CLC Number:

Longbing Xu, Wenbin Wu. Over-reaction, Jump Return and A-share Momentum Strategy[J]. Chinese Journal of Management Science, 2025, 33(6): 1-13.

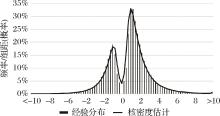

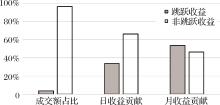

"

| 变量 | 样本数 | 均值 | 中位数 | 标准差 | 25%分位数 | 75%分位数 |

|---|---|---|---|---|---|---|

| 日收益(%) | 4568903 | 0.029 | 0 | 2.941 | -1.363 | 1.383 |

| 跳跃收益(%) | 4568903 | 0.308 | 0 | 1.434 | 0 | 0.266 |

| 非跳跃收益(%) | 4568903 | -0.280 | -0.173 | 2.450 | -1.406 | 0.866 |

| 日内羊群效应 | 28140344 | 0.169 | 0.146 | 0.129 | 0.063 | 0.252 |

| 未预期盈余 | 74695 | 0.048 | 0.048 | 2.393 | -1.074 | 1.187 |

| 换手率 | 225216 | 3.008 | 2.347 | 2.208 | 1.414 | 3.948 |

| 短期反转 | 225216 | 3.181 | 2.483 | 2.410 | 1.498 | 4.123 |

| 特质波动率 | 225216 | 0.005 | -0.703 | 12.624 | -7.279 | 6.638 |

| 最大收益 | 225216 | -0.036 | -0.019 | 0.295 | -0.198 | 0.143 |

| 收益偏度 | 225216 | 3.345 | 2.942 | 1.815 | 2.016 | 4.253 |

| 异常换手率 | 225216 | 0.104 | -0.022 | 1.014 | -0.365 | 0.383 |

| 市值 | 225216 | 1.005 | 0.846 | 0.628 | 0.564 | 1.276 |

| 盈利市值比 | 225216 | 13.703 | 13.525 | 0.976 | 13.010 | 14.188 |

| 波动率 | 225216 | 0.037 | 0.028 | 0.031 | 0.016 | 0.048 |

| 流动性 | 225216 | 2.807 | 2.639 | 1.001 | 2.102 | 3.325 |

"

"

"

"

"

| 变量 | 是否发生跳跃 (发生跳跃=1,未发生跳跃=0) |

|---|---|

| 日内羊群效应 | 2.27*** (82.42) |

| 早市开盘半小时 | 2.17*** (64.53) |

| 个体效应 | 控制 |

| 周度效应 | 控制 |

| 其他日内时段 | 控制 |

| 样本数 | 6578266 |

| LR chi2 | 60683.8*** |

"

| 跳跃方向 | 样本 总数 | 卖出羊群行为(%) | 买入羊群行为(%) | ||||

|---|---|---|---|---|---|---|---|

| 强 | 中 | 弱 | 弱 | 中 | 强 | ||

| 正向 | 228038 | 1.39 | 4.11 | 7.00 | 13.72 | 35.38 | 38.39 |

| 负向 | 139796 | 19.66 | 37.88 | 21.96 | 11.62 | 6.93 | 1.94 |

"

"

"

| 变量 | 非跳跃收益占比低 | 非跳跃收益占比高 | 全样本 |

|---|---|---|---|

| SUE | 0.34*** | 0.61*** | 0.35*** |

| (12.37) | (18.75) | (12.94) | |

| SUE | 0.24*** | ||

| (5.80) | |||

| 股票特征 | 控制 | 控制 | 控制 |

| 所属行业 | 控制 | 控制 | 控制 |

| 报告期 | 控制 | 控制 | 控制 |

| 样本数 | 31316 | 32038 | 63354 |

| Adj. R2 | 0.091 | 0.087 | 0.386 |

组间系数 差异检验 | -0.27*** | ||

"

| 变量 | 跳跃次数 | ||

|---|---|---|---|

| 合计 | 正向 | 负向 | |

| CICSI | 0.006*** | 0.003** | 0.005*** |

| (3.79) | (2.17) | (5.00) | |

| 截距项和滞后项 | 控制 | 控制 | 控制 |

| 样本数 | 143 | 143 | 143 |

| DW-stat | 2.20 | 2.11 | 2.16 |

| Adj. R2 | 0.474 | 0.190 | 0.290 |

"

| 变量 | 被解释变量 | ||

|---|---|---|---|

| 月度收益 | 月度跳跃收益 | 月度非跳跃收益 | |

| Turn | -0.20*** | 0.12*** | -0.27*** |

| (-8.98) | (6.10) | (-13.35) | |

| 股票特征 | 控制 | 控制 | 控制 |

| 个体效应 | 控制 | 控制 | 控制 |

| 所属行业 | 控制 | 控制 | 控制 |

| 月度效应 | 控制 | 控制 | 控制 |

| 样本数 | 194991 | 194991 | 194991 |

| Adj. R2 | 0.439 | 0.153 | 0.418 |

"

| 变量 | 月均收益 | CH-3模型 | FF-5模型 | CH-3模型+JumpRet | FF-5模型+JumpRet | |

|---|---|---|---|---|---|---|

| 面板A 跳跃收益因子对过度反应因子的解释能力(过度反应因子的alpha) | ||||||

| JumpRet | 1.06*** | 0.85*** | 1.09*** | |||

| (3.36) | (3.02) | (5.34) | ||||

| Rev | 1.11*** | 0.83** | 1.09*** | -0.15 | -0.17 | |

| (2.82) | (2.44) | (3.48) | (-0.53) | (-0.59) | ||

| IVol | 0.29 | 0.43* | 0.24 | 0.33 | 0.18 | |

| (1.31) | (1.68) | (1.00) | (1.22) | (0.74) | ||

| Max | 0.73** | 0.31 | 0.76*** | -0.47*** | -0.27 | |

| (2.43) | (0.94) | (3.21) | (-2.71) | (-1.56) | ||

| Skew | 0.81*** | 0.33 | 0.67*** | -0.16 | 0.02 | |

| (2.62) | (1.24) | (2.61) | (-0.62) | (0.09) | ||

| AbnTurn | 0.74*** | 0.74** | 0.77*** | 0.27 | 0.14 | |

| (2.69) | (2.40) | (3.23) | (1.04) | (0.56) | ||

| 面板B 过度反应因子对跳跃收益因子的解释能力(跳跃收益因子的alpha) | ||||||

| 因子模型 | Rev | IVol | Max | Skew | AbnTurn | |

| CH-3模型+对应过度反应因子 | 0.52*** | 0.83*** | 0.70*** | 0.75*** | 0.64*** | |

| (2.59) | (2.99) | (3.77) | (3.11) | (2.51) | ||

| FF-5模型+对应过度反应因子 | 0.67*** | 1.11*** | 0.71*** | 0.88*** | 0.87*** | |

| (4.05) | (5.36) | (4.73) | (4.35) | (4.27) | ||

"

| 变量 | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | (12) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| JumpRet | -0.05 | -0.04 | -0.05 | -0.04 | -0.05 | -0.04 | -0.03 | |||||

| (-5.2) | (-4.3) | (-5.1) | (-4.4) | (-5.1) | (-4.8) | (-4.0) | ||||||

| Rev | -4.30 | -3.00 | -2.01 | |||||||||

| (-4.5) | (-3.4) | (-2.1) | ||||||||||

| IVol | -0.03 | 0.07 | 0.24 | |||||||||

| (-0.1) | (0.25) | (0.87) | ||||||||||

| Max | -0.35 | -0.25 | -0.02 | |||||||||

| (-4.9) | (-4.0) | (-0.4) | ||||||||||

| Skew | -3.36 | -2.69 | -1.05 | |||||||||

| (-1.6) | (-1.3) | (-1.3) | ||||||||||

| AbnTurn | -0.68 | -0.53 | -0.39 | |||||||||

| (-4.3) | (-3.6) | (-2.6) | ||||||||||

| CH-3 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 |

| 股票特征 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 |

| 所属行业 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 |

| Avg. R2 | 0.181 | 0.184 | 0.186 | 0.180 | 0.183 | 0.183 | 0.185 | 0.182 | 0.184 | 0.183 | 0.185 | 0.196 |

"

| 变量 | 跳跃收益 | 非跳跃收益 | ||||

|---|---|---|---|---|---|---|

| 月均收益 | CH-3模型 | FF-5模型 | 月均收益 | CH-3模型 | FF-5模型 | |

| IVol | 0.30* | 0.33* | 0.35** | 0.36 | 0.32 | 0.31 |

| (1.83) | (1.90) | (2.49) | (1.38) | (1.11) | (1.16) | |

| Max | 0.84*** | 0.51** | 0.86*** | 0.28 | -0.07 | 0.31 |

| (2.77) | (2.12) | (4.36) | (1.11) | (-0.24) | (1.44) | |

| Skew | 0.85*** | 0.45** | 0.74*** | 0.09 | -0.27 | 0.05 |

| (3.16) | (2.23) | (4.48) | (0.38) | (-1.40) | (0.23) | |

"

| 组合 | 按跳跃收益排序 | 按非跳跃收益排序 | ||||

|---|---|---|---|---|---|---|

| 1 | 10 | 10-1 | 1 | 10 | 10-1 | |

跳跃 收益 | 4.35 | 8.97 | 4.62 | 8.08 | 5.35 | -2.73 |

| (5.0) | (5.2) | (5.1) | (5.2) | (4.8) | (-4.6) | |

非跳跃 收益 | -3.43 | -8.63 | -5.20 | -7.04 | -5.18 | 1.86 |

| (-3.8) | (-4.9) | (-4.9) | (-4.8) | (-4.1) | (2.6) | |

"

"

"

| J/K | 市值加权 | 等权 | ||||||

|---|---|---|---|---|---|---|---|---|

| 1 | 3 | 6 | 9 | 1 | 3 | 6 | 9 | |

| 面板A 基于累计跳跃收益的市值中性多空组合 | ||||||||

| 1 | -0.35 | -0.56** | -0.59** | -0.46* | -0.76*** | -0.61*** | -0.51*** | -0.45*** |

| (-1.00) | (-2.18) | (-2.36) | (-1.91) | (-3.07) | (-3.07) | (-3.05) | (-2.77) | |

| 3 | -0.96* | -0.99** | -0.76** | -0.63* | -0.94*** | -0.78*** | -0.68*** | -0.61*** |

| (-1.94) | (-2.29) | (-2.07) | (-1.74) | (-3.42) | (-3.04) | (-2.84) | (-2.56) | |

| 6 | -1.28** | -1.08** | -0.90** | -0.88** | -1.11*** | -0.95*** | -0.84*** | -0.81*** |

| (-2.35) | (-2.22) | (-2.12) | (-2.01) | (-3.55) | (-3.10) | (-2.82) | (-2.61) | |

| 9 | -0.98* | -0.94* | -0.78* | -0.75 | -1.10*** | -0.99*** | -0.89*** | -0.81** |

| (-1.87) | (-1.91) | (-1.74) | (-1.60) | (-3.53) | (-3.09) | (-2.79) | (-2.43) | |

| 12 | -1.00* | -0.91* | -0.80* | -0.71 | -1.13*** | -1.01*** | -0.85*** | -0.77** |

| (-1.81) | (-1.83) | (-1.74) | (-1.48) | (-3.25) | (-3.02) | (-2.65) | (-2.26) | |

| 面板B 基于累计非跳跃收益的市值中性多空组合 | ||||||||

| 1 | 3 | 6 | 9 | 1 | 3 | 6 | 9 | |

| 1 | 0.00 | 0.60** | 0.46** | 0.35 | 0.25 | 0.54** | 0.44** | 0.35* |

| (-0.01) | (2.50) | (1.87) | (1.41) | (0.86) | (2.44) | (2.16) | (1.84) | |

| 3 | 0.92** | 0.86** | 0.67** | 0.53 | 0.76** | 0.83*** | 0.74** | 0.58** |

| (2.19) | (2.21) | (1.73) | (1.38) | (2.00) | (2.61) | (2.45) | (1.97) | |

| 6 | 0.52 | 0.67 | 0.67 | 0.52 | 0.92** | 0.91** | 0.73** | 0.57* |

| (1.05) | (1.30) | (1.30) | (1.08) | (2.41) | (2.43) | (1.97) | (1.59) | |

| 9 | 0.37 | 0.51 | 0.35 | 0.24 | 0.83** | 0.76** | 0.56 | 0.36 |

| (0.69) | (0.93) | (0.62) | (0.43) | (2.05) | (1.92) | (1.41) | (0.93) | |

| 12 | 0.71 | 0.58 | 0.50 | 0.44 | 0.96** | 0.78** | 0.56 | 0.42 |

| (1.41) | (1.21) | (1.09) | (0.98) | (2.47) | (2.11) | (1.53) | (1.19) | |

"

| 加权方式 | jump(3,1,1) | jump(6,1,1) | non-jump(3,1,1) | non-jump(6,1,1) | ||||

|---|---|---|---|---|---|---|---|---|

| 市值 | 等权 | 市值 | 等权 | 市值 | 等权 | 市值 | 等权 | |

| Intercept | -0.37 | -0.59*** | -0.62* | -0.66** | 1.27** | 1.08*** | 1.05** | 1.29*** |

| (-1.10) | (-2.62) | (-1.68) | (-2.32) | (2.44) | (2.64) | (2.14) | (2.85) | |

| CH-3 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 | 控制 |

| 样本数 | 140 | 140 | 137 | 137 | 140 | 140 | 137 | 137 |

| Adj. R2 | 0.365 | 0.354 | 0.510 | 0.375 | 0.102 | 0.085 | 0.382 | 0.199 |

| 1 | Jegadeesh N, Titman S. Returns to buying winners and selling losers: Implications for stock market efficiency[J]. The Journal of Finance,1993,48(1):65-91. |

| 2 | Fama E F, French K R. Size,value,and momentum in international stock returns[J]. Journal of Financial Economics,2012,105(3):457-472. |

| 3 | Asness C S, Moskowitz T J, Pedersen L H. Value and momentum everywhere[J]. The Journal of Finance,2013,68(3):929-985. |

| 4 | 潘莉,徐建国. A股个股回报率的惯性与反转[J]. 金融研究,2011(1):149-166. |

| Pan L, Xu J G. Price continuation and reversal in China’s A-share stock market:A comprehensive examination[J]. Journal of Financial Research,2011(1):149-166. | |

| 5 | 田利辉,王冠英,谭德凯. 反转效应与资产定价:历史收益率如何影响现在[J]. 金融研究,2014(10):177-192. |

| Tian L H, Wang G Y, Tan D K. Reversal effects and asset pricing in China: How do historical returns influence stock performance[J].Journal of Financial Research,2014(10):177-192. | |

| 6 | Liu J N, Stambaugh R F, Yuan Y. Size and value in China[J]. Journal of Financial Economics,2019,134(1):48-69. |

| 7 | Jegadeesh N. Evidence of predictable behavior of security returns[J]. The Journal of Finance,1990,45(3):881-898. |

| 8 | 白颢睿,吴辉航,柯岩. 中国股票市场月频动量效应消失之谜——基于T+1制度下隔夜折价现象的研究[J]. 财经研究,2020,46(4):140-154. |

| Bai H R, Wu H H, Ke Y. On the reason for “weak monthly momentum effect” in the Chinese stock market: Evidence from t+1 overnight discount[J]. Journal of Finance and Economics,2020,46(4):140-154. | |

| 9 | Barberis N, Shleifer A, Vishny R. A model of investor sentiment[J]. Journal of Financial Economics,1998,49(3):307-343. |

| 10 | Daniel K, Hirshleifer D, Subrahmanyam A. Investor psychology and security market under- and overreactions[J].The Journal of Finance,1998,53(6):1839-1885. |

| 11 | 高秋明,胡聪慧,燕翔. 中国A股市场动量效应的特征和形成机理研究[J]. 财经研究,2014,40(2):97-107. |

| Gao Q M, Hu C H, Yan X. On characteristics and formation mechanisms of momentum effect in China’s A-share market[J]. Journal of Finance and Economics,2014,40(2):97-107. | |

| 12 | 陆蓉,陈实,李金龙. 彩票型股票与动量效应[J]. 经济学动态,2021(7):34-50. |

| Lu R, Chen S, Li J L. Lottery stocks and momentum effects[J]. Economic Perspectives,2021(7):34-50. | |

| 13 | Ang A, Hodrick R J, Xing Y H,et al. The cross-section of volatility and expected returns[J].The Journal of Finance,2006,61(1):259-299. |

| 14 | Asness C S, Frazzini A, Gormsen N J,et al. Betting against correlation: Testing theories of the low-risk effect[J]. Journal of Financial Economics,2020,135(3):629-652. |

| 15 | Lou D, Polk C, Skouras S. A tug of war: Overnight versus intraday expected returns[J]. Journal of Financial Economics,2019,134(1):192-213. |

| 16 | Andersen T G, Bollerslev T, Diebold F X,et al. The distribution of realized stock return volatility[J]. Journal of Financial Economics,2001,61(1):43-76. |

| 17 | 欧丽莎,袁琛,李汉东. 中国股票价格跳跃实证研究[J]. 管理科学学报,2011,14(9):60-66. |

| Ou L S, Yuan C, Li H D. Empirical research on jumps in stock price in Chinese stock markets[J]. Journal of Management Sciences in China,2011,14(9):60-66. | |

| 18 | Kapadia N, Zekhnini M. Do idiosyncratic jumps matter?[J]. Journal of Financial Economics,2019,131(3):666-692. |

| 19 | 刘志东,杨竞一. 基于非参数日内跳跃检验和高频数据的公司信息披露对股市价格波动影响研究[J]. 中国管理科学,2016,24(10):22-34. |

| Liu Z D, Yang J Y. A study of firm specific information disclosure on the price variation with nonparametric intraday jumps detection in high frequency data[J]. Chinese Journal of Management Science,2016,24(10):22-34. | |

| 20 | 龚旭,林伯强. 跳跃风险、结构突变与原油期货价格波动预测[J]. 中国管理科学,2018,26(11):11-21. |

| Gong X, Lin B Q. Jump risk, structural breaks and forecasting crude oil futures volatility[J]. Chinese Journal of Management Science,2018,26(11):11-21. | |

| 21 | Jiang G J, Yao T. Stock price jumps and cross-sectional return predictability[J]. Journal of Financial and Quantitative Analysis,2013,48(5):1519-1544. |

| 22 | 陆蓉,李金龙,陈实. 中国投资者的股票出售行为画像——处置效应研究新进展[J]. 管理世界,2022,38(3):59-78. |

| Lu R, Li J L, Chen S. Portraits of investors’ selling behavior in China's stock market: Advances in disposition effect[J]. Journal of Management World,2022,38(3):59-78. | |

| 23 | 朱菲菲,李惠璇,徐建国,等. 短期羊群行为的影响因素与价格效应——基于高频数据的实证检验[J]. 金融研究,2019(7):191-206. |

| Zhu F F, Li H X, Xu J G,et al. Determinants and pricing effects of short-term herd behavior: An empirical test based on high-frequency data[J]. Journal of Financial Research,2019(7):191-206. | |

| 24 | Jiang G J, Zhu K X. Information shocks and short-term market underreaction[J]. Journal of Financial Economics,2017,124(1):43-64. |

| 25 | Fama E F, French K R. Comparing cross-section and time-series factor models[J]. The Review of Financial Studies,2020,33(5):1891-1926. |

| 26 | Hua J, Peng L, Schwartz R A,et al. Resiliency and stock returns[J]. The Review of Financial Studies,2020,33(2):747-782. |

| 27 | 孔东民,柯瑞豪. 谁驱动了中国股市的PEAD?[J]. 金融研究,2007(10):82-99. |

| Kong D M, Ke R H. Who drives the PEAD in China[J]. Journal of Financial Research,2007(10):82-99. | |

| 28 | 游家兴. 谁反应过度,谁反应不足——投资者异质性与收益时间可预测性分析[J]. 金融研究,2008(4):161-173. |

| You J X. Who overreacts and who underreacts? analysis on the relationship between the investor’s heterogeneity and return time-series predictability[J]. Journal of Financial Research,2008(4):161-173. | |

| 29 | Baker M, Stein J C. Market liquidity as a sentiment indicator[J]. Journal of Financial Markets,2004,7(3):271-299. |

| 30 | Bandi F M, Russell J R. Separating microstructure noise from volatility[J]. Journal of Financial Economics,2006,79(3):655-692. |

| 31 | 胡志军,凌爱凡,杨超. 我国A股市场的模糊性溢价——基于日内高频数据的分析[J]. 中国管理科学,2022,30(1):42-53. |

| Hu Z J, Ling A F, Yang C. The ambiguity premium in china’s a-shares market:The analysis from intra-day high frequency data[J]. Chinese Journal of Management Science,2022,30(1):42-53. | |

| 32 | Wermers R. Mutual fund herding and the impact on stock prices[J]. The Journal of Finance,1999,54(2):581-622. |

| 33 | Lakonishok J, Shleifer A, Vishny R W. The impact of institutional trading on stock prices[J]. Journal of Financial Economics,1992,32(1):23-43. |

| 34 | 姚禄仕,吴宁宁. 基于LSV模型的机构与个人羊群行为研究[J]. 中国管理科学,2018,26(7):55-62. |

| Yao L S, Wu N N. A study on herding behavior of institution and individual investors based on LSV model[J]. Chinese Journal of Management Science,2018,26(7):55-62. | |

| 35 | 陆静,张银盈. “特质波动率之谜”与估计模型有关吗?[J]. 中国管理科学,2022,30(9):36-48. |

| Lu J, Zhang Y Y. Idiosyncratic volatility puzzle and its estimation model[J]. Chinese Journal of Management Science,2022,30(9):36-48. | |

| 36 | Ali U, Hirshleifer D. Shared analyst coverage: Unifying momentum spillover effects[J]. Journal of Financial Economics,2020,136(3):649-675. |

| 37 | Fama E F, French K R. A five-factor asset pricing model[J]. Journal of Financial Economics,2015,116(1):1-22. |

| 38 | Fama E F, MacBeth J D. Risk, return, and equilibrium empirical tests[J]. The Journal of Political Economy,1973,81(3):607-636. |

| 39 | Jegadeesh N, Noh J, Pukthuanthong K,et al. Empirical tests of asset pricing models with individual assets: Resolving the errors-in-variables bias in risk premium estimation[J]. Journal of Financial Economics,2019,133(2):273-298. |

| 40 | 蒋崇辉,刘林. 惯性因子跟踪策略的有效性:来自中国股票市场的证据[J]. 中国管理科学,2022,30(5):86-97. |

| Jiang C H, Liu L. The effectiveness of momentum factor tracking strategy: Evidence from china stock market[J]. Chinese Journal of Management Science,2022,30(5):86-97. | |

| 41 | Akbas F, Boehmer E, Jiang C,et al. Overnight returns, daytime reversals, and future stock returns[J]. Journal of Financial Economics,2022,145(3):850-875. |

| 42 | Pástor Ľ, Stambaugh R F. Liquidity risk and expected stock returns[J]. Journal of Political Economy,2003,111(3):642-685. |

| [1] | Weiqi Liu, Jianying Li, Jie Zhou, Dongliang Yuan. Digital Transformation and Firm Value: Theory and Empirical Evidence [J]. Chinese Journal of Management Science, 2025, 33(5): 138-149. |

| [2] | Xia Liu, Yunyue Zhang, Mengqi Li, Yejun Xu. Quantum Supervised Game Model and Simulation Analysis for Manipulative Behavior in Trading Stock Market [J]. Chinese Journal of Management Science, 2025, 33(3): 24-33. |

| [3] | Jiaxian Shen, Haozhi Chen, Weiguo Zhang. Research on Systemic Risk Measurement of China’ s Foreign Exchange Market Based on Knowledge Graph Network Characteristics [J]. Chinese Journal of Management Science, 2025, 33(3): 45-61. |

| [4] | Baohuan Zhou, Xiaoli Hu, Pingfan Wang, Guangwei Deng, liang Liang. The Way of Bridging Salary Disparity and Cooperative Tendency: Through Employee Fairness Perception and Team Competition Atmosphere [J]. Chinese Journal of Management Science, 2024, 32(12): 49-59. |

| [5] | Jiayu Zheng, Yi Hu. Can Green Credit Drive the “Greening” of the Financial System and Enterprise Emission Reduction?Based on Evolutionary Game Analysis [J]. Chinese Journal of Management Science, 2024, 32(12): 288-299. |

| [6] | Hong Shen, Chenyao Zhang, Xiaoxing Liu. Analysis of Risk Spillover Characteristics and Mechanism among Industries: Evidence from Multilayer Network [J]. Chinese Journal of Management Science, 2024, 32(12): 173-182. |

| [7] | Kun Zhou,Xiaohui Gao,Lianshui Li. Integrated Carbon Emission Trading Price Prediction Based on EMD-XGB-ELM and FSGM from the Perspective of Dual Processing [J]. Chinese Journal of Management Science, 2024, 32(10): 325-334. |

| [8] | Xinnan Lei,Lefan Lin,Binqing Xiao,Honghai Yu. Re-exploration of Small and Micro Enterprises' Default Characteristics Based on Machine Learning Models with SHAP [J]. Chinese Journal of Management Science, 2024, 32(5): 1-12. |

| [9] | Lanbiao Liu,Liang Guo. Downside Risk in the Chinese A-Share Market: Based on the Perspective of Generalized Disappointment Aversion [J]. Chinese Journal of Management Science, 2024, 32(5): 61-72. |

| [10] | De-hua SHEN,Yue LI. Do Commodity Futures Improve the Performances of Traditional Portfolios? Evidence from the Chinese Market [J]. Chinese Journal of Management Science, 2023, 31(12): 34-45. |

| [11] | Yong-ji ZHANG,Tian-xiong LI,Zhi SU,Qiong HUANG. Fund Size, Investor Attention and Fund Performance Persistence [J]. Chinese Journal of Management Science, 2023, 31(12): 57-68. |

| [12] | Dan LI,Yong-mei LIU,Xiao-hong CHEN. Pricing and Coupon Strategies in an Online Platform-based Supply Chain [J]. Chinese Journal of Management Science, 2023, 31(11): 165-173. |

| [13] | Dan-yang WANG,Lu-shi YAO. Mutual Funds' Dynamic Liquidity Risk Management [J]. Chinese Journal of Management Science, 2023, 31(10): 40-48. |

| [14] | Jiang-tao WANG,Ya CAI,Cheng-li ZHENG. An Adaptive Algorithm for Prediction of Risk and Its Application [J]. Chinese Journal of Management Science, 2023, 31(8): 1-8. |

| [15] | Song-liang LI,Peng-fei CHENG. Research on Dynamic Evolution Game of Collaborative Innovation in University Science and Technology City [J]. Chinese Journal of Management Science, 2023, 31(8): 204-213. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||