主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (6): 14-26.doi: 10.16381/j.cnki.issn1003-207x.2022.1453

Previous Articles Next Articles

Zisheng Ouyang1, Xuewei Zhou2,3( )

)

Received:2022-07-04

Revised:2023-02-04

Online:2025-06-25

Published:2025-07-04

Contact:

Xuewei Zhou

E-mail:zhouxuewei@mail.shufe.edu.cn

CLC Number:

Zisheng Ouyang, Xuewei Zhou. Systemic Risk Backtesting and Connectedness of Chinese Financial Institutions: Evidence from MES and ΔCoVaR[J]. Chinese Journal of Management Science, 2025, 33(6): 14-26.

"

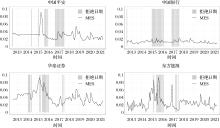

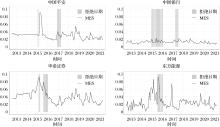

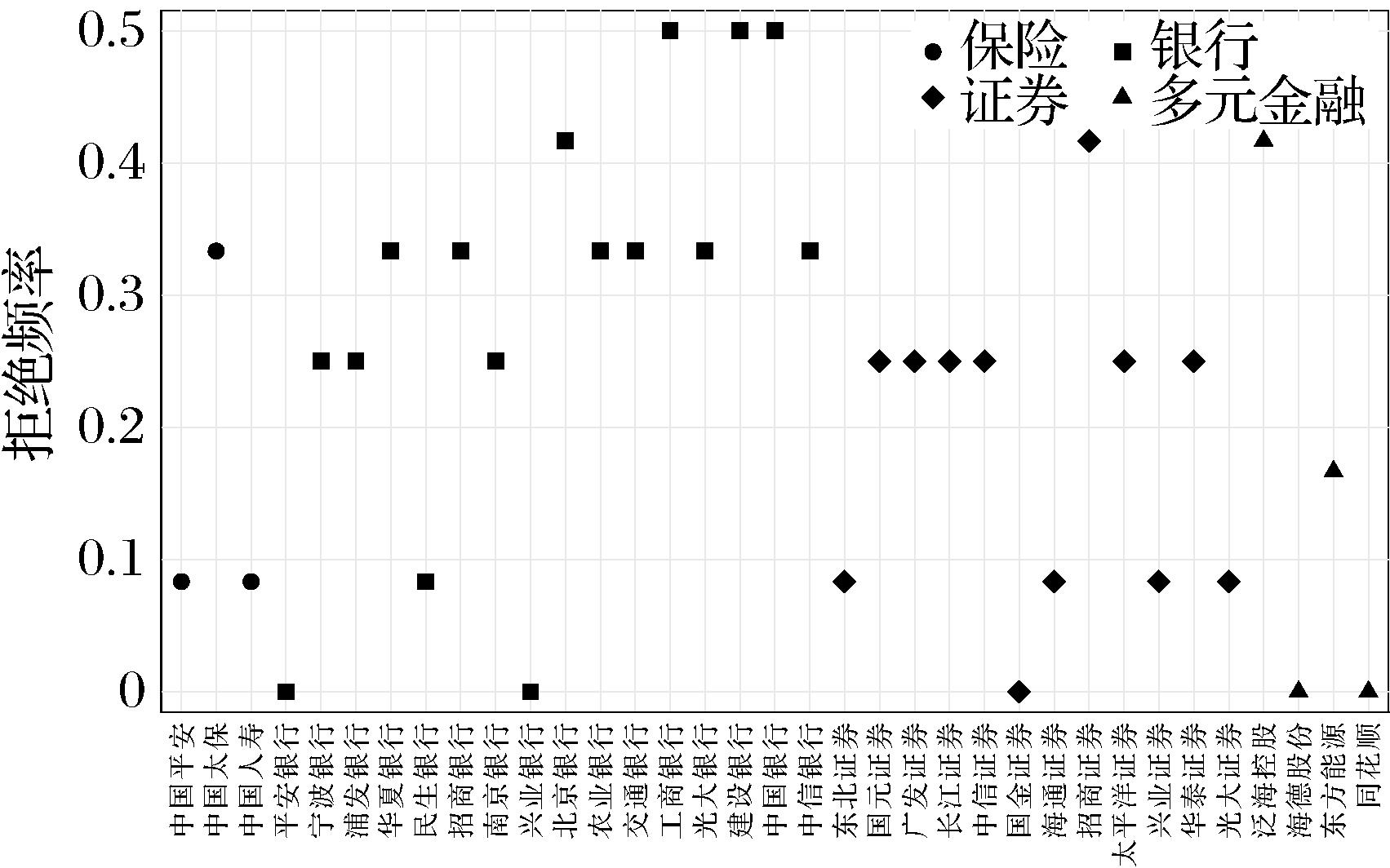

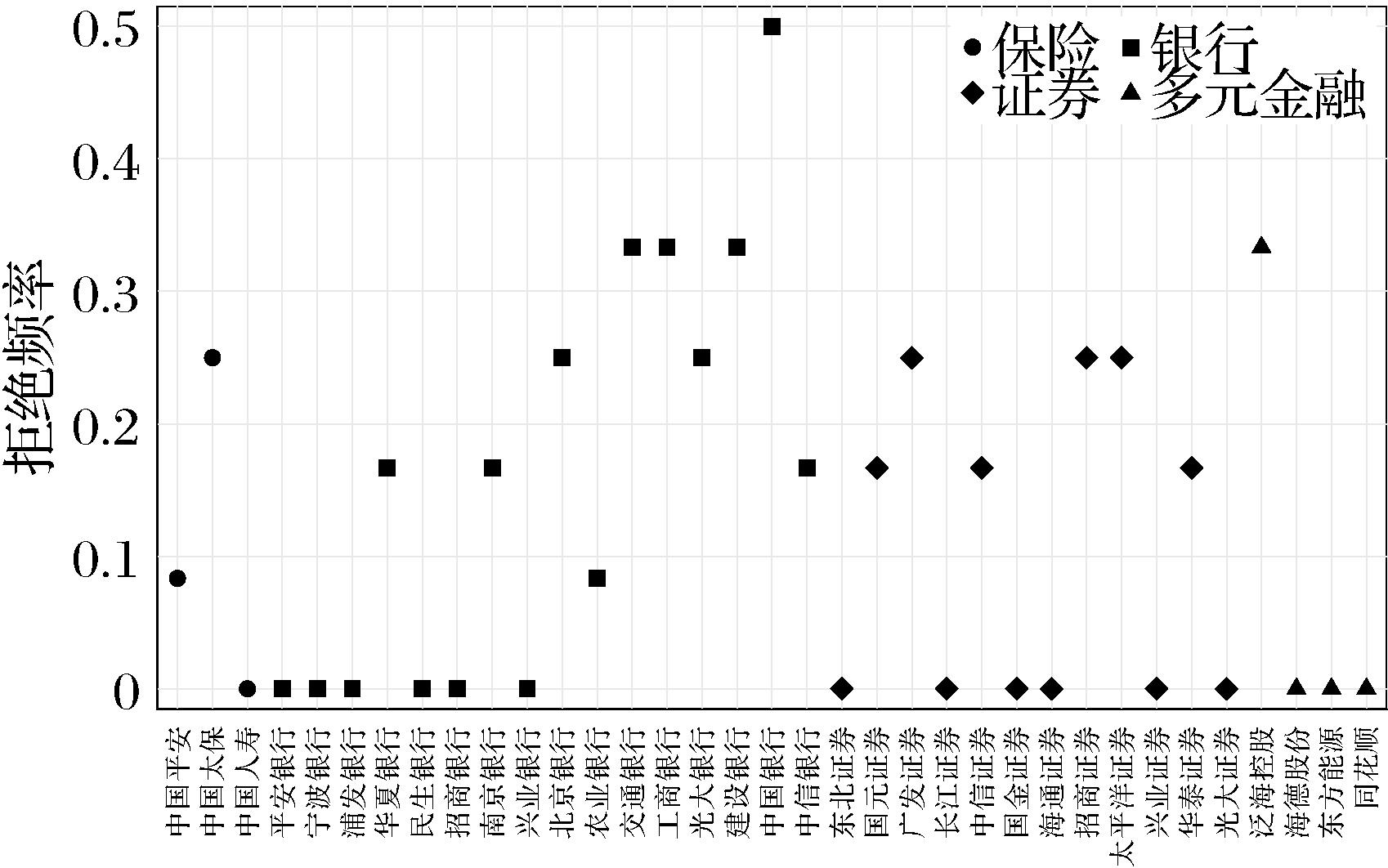

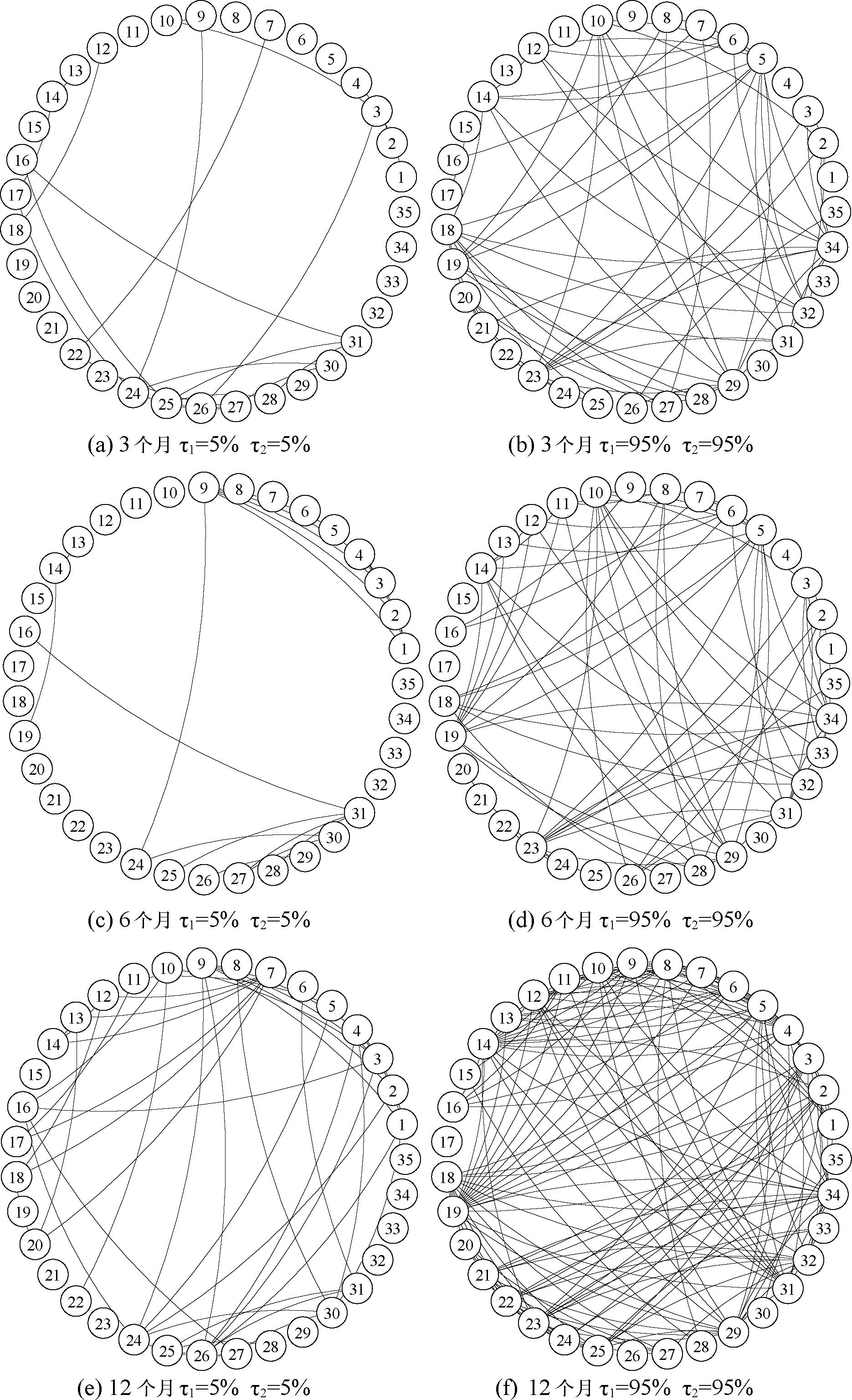

| 序号 | 机构 | 行业 | 序号 | 机构 | 行业 |

|---|---|---|---|---|---|

| 1 | 中国平安 | 保险 | 19 | 中信银行 | 银行 |

| 2 | 中国太保 | 保险 | 20 | 东北证券 | 证券 |

| 3 | 中国人寿 | 保险 | 21 | 国元证券 | 证券 |

| 4 | 平安银行 | 银行 | 22 | 广发证券 | 证券 |

| 5 | 宁波银行 | 银行 | 23 | 长江证券 | 证券 |

| 6 | 浦发银行 | 银行 | 24 | 中信证券 | 证券 |

| 7 | 华夏银行 | 银行 | 25 | 国金证券 | 证券 |

| 8 | 民生银行 | 银行 | 26 | 海通证券 | 证券 |

| 9 | 招商银行 | 银行 | 27 | 招商证券 | 证券 |

| 10 | 南京银行 | 银行 | 28 | 太平洋证券 | 证券 |

| 11 | 兴业银行 | 银行 | 29 | 兴业证券 | 证券 |

| 12 | 北京银行 | 银行 | 30 | 华泰证券 | 证券 |

| 13 | 农业银行 | 银行 | 31 | 光大证券 | 证券 |

| 14 | 交通银行 | 银行 | 32 | 泛海控股 | 多元金融 |

| 15 | 工商银行 | 银行 | 33 | 海德股份 | 多元金融 |

| 16 | 光大银行 | 银行 | 34 | 东方能源 | 多元金融 |

| 17 | 建设银行 | 银行 | 35 | 同花顺 | 多元金融 |

| 18 | 中国银行 | 银行 |

"

"

"

"

"

"

"

"

"

"

"

"

"

| LOO_3 | LOO_6 | LOO_12 | |||

|---|---|---|---|---|---|

| 金融机构 | 关联重要性(%) | 金融机构 | 关联重要性(%) | 金融机构 | 关联重要性(%) |

| 宁波银行 | 8.87 | 宁波银行 | 7.97 | 宁波银行 | 5.81 |

| 东方能源 | 8.87 | 中信银行 | 6.52 | 交通银行 | 5.48 |

| 兴业证券 | 8.06 | 长江证券 | 6.52 | 中信银行 | 4.84 |

| 中国银行 | 7.26 | 兴业证券 | 6.52 | 兴业证券 | 4.84 |

| 南京银行 | 5.65 | 东方能源 | 6.52 | 东方能源 | 4.84 |

| 长江证券 | 5.65 | 南京银行 | 5.80 | 平安银行 | 4.52 |

| 光大证券 | 5.65 | 光大证券 | 5.80 | 民生银行 | 4.52 |

| 交通银行 | 4.84 | 交通银行 | 5.07 | 北京银行 | 4.52 |

| 泛海控股 | 4.84 | 中国人寿 | 4.35 | 长江证券 | 4.52 |

| 中国太保 | 4.03 | 海德股份 | 4.35 | 招商银行 | 3.87 |

| 1 | Adrian T, Brunnermeier M K. CoVaR[J]. American Economic Review, 2016, 106(7): 1705-1741. |

| 2 | 赵林海, 陈名智. 金融机构系统性风险溢出和系统性风险贡献—基于滚动窗口动态Copula模型双时变相依视角[J]. 中国管理科学, 2021, 29(7): 71-83. |

| Zhao L H, Chen M Z. Systemic risk spillovers and systemic risk contributions of financial institutions in China: A perspective of dual time-varying dependence of rolling window dynamic copula model[J]. Chinese Journal of Management Science, 2021, 29(7): 71-83. | |

| 3 | 张伟平, 庄新田, 王健. 中国股市跨行业系统性风险空间溢出关联及风险预测分析——基于尾部风险网络模型[J]. 中国管理科学, 2021, 29(12): 15-28. |

| Zhang W P, Zhuang X T, Wang J. Systemic risk spatial spillover correlation and risk prediction analysis of cross-industry in China’s stock market:Based on the tail risk network model[J]. Chinese Journal of Management Science, 2021, 29(12): 15-28. | |

| 4 | 欧阳资生, 周学伟. 系统性金融风险对宏观经济的溢出效应研究——基于分位数对分位数方法[J]. 统计研究, 2022, 39(10): 68-83. |

| Ouyang Z S, Zhou X W. The spillover effect of systemic financial risks on macro economy: Based on quantile on quantile approach[J]. Statistics Research, 2022, 39(10): 68-83. | |

| 5 | Acharya V V, Pedersen L H, Philippon T, et al. Measuring systemic risk[J]. Review of Financial Studies, 2017, 30(1): 2-47. |

| 6 | Berger A N, Cai J, Roman R A, et al. Supervisory enforcement actions against banks and systemic risk[J]. Journal of Banking & Finance, 2022: 106222. |

| 7 | Brownlees C, Engle R F. SRISK: A conditional capital shortfall measure of systemic risk[J]. The Review of Financial Studies, 2017, 30(1): 48-79. |

| 8 | Huang X, Zhou H, Zhu H. Assessing the systemic risk of a heterogeneous portfolio of banks during the recent financial crisis[J]. Journal of Financial Stability, 2012, 8(3): 193-205. |

| 9 | Oh D H, Patton A J. Time-varying systemic risk: Evidence from a dynamic copula model of CDS spreads[J]. Journal of Business & Economic Statistics, 2018, 36(2): 181-195. |

| 10 | 叶五一, 谭轲祺, 缪柏其. 基于动态因子Copula模型的行业间系统性风险分析[J]. 中国管理科学, 2018, 26(3): 1-12. |

| Ye W Y, Tan K Q, Miao B Q. Analysis of systemic risk among industries via dynamic factor Copulas[J]. Chinese Journal of Management Science, 2018, 26(3): 1-12. | |

| 11 | 李敏波, 梁爽. 监测系统性金融风险——中国金融市场压力指数构建和状态识别[J]. 金融研究, 2021(6): 21-38. |

| Li M B, Liang S. Monitoring systemic financial risks: Construction and state identification of China’s financial market stress index[J]. Journal of Financial Research, 2021(6): 21-38. | |

| 12 | 欧阳资生, 李虹宣, 刘凤根. 中国系统性金融风险对宏观经济的影响研究[J]. 统计研究, 2019, 36(8): 19-31. |

| Ouyang Z S, Li H X, Liu F G. Research on the impact of China’s systemic financial risks on the macroeconomy[J]. Statistical Research, 2019, 36(8): 19-31. | |

| 13 | Zedda S, Cannas G. Analysis of banks’ systemic risk contribution and contagion determinants through the leave-one-out approach[J]. Journal of Banking & Finance, 2020, 112: 105160. |

| 14 | 黄乃静, 于明哲. 系统性金融风险指标的比较分析—基于实体经济风险预测的视角[J]. 系统工程理论与实践, 2020, 40(10): 2475-2491. |

| Huang N J, Yu M Z. Comparison analysis of systemic risk measures: A study based on real economic risk forecasting[J]. Systems Engineering-Theory & Practice, 2020, 40(10): 2475-2491. | |

| 15 | Ouyang Z S, Yang X T, Lai Y. Systemic financial risk early warning of financial market in China using Attention-LSTM model[J]. The North American Journal of Economics and Finance, 2021, 56: 101383. |

| 16 | Billio M, Getmansky M, Lo A W, et al. Econometric measures of connectedness and systemic risk in the finance and insurance sectors[J]. Journal of Financial Economics, 2012, 104(3): 535-559. |

| 17 | Diebold F X, Yilmaz K. On the network topology of variance decompositions: Measuring the connectedness of financial firms[J]. Journal of Econometrics, 2014, 182(1): 119-134. |

| 18 | 杨子晖, 陈雨恬, 谢锐楷. 我国金融机构系统性金融风险度量与跨部门风险溢出效应研究[J]. 金融研究, 2018(10): 19-37. |

| Yang Z H, Chen Y T, Xie R K. Research on systemic risk measures and cross-sector risk spillover effect of financial institutions in China[J]. Journal of Financial Research, 2018(10): 19-37. | |

| 19 | 宫晓莉, 熊熊. 波动溢出网络视角的金融风险传染研究[J]. 金融研究, 2020(5): 39-58. |

| Gong X L, Xiong X. A study of financial risk contagion from the volatility spillover network perspective[J]. Journal of Financial Research, 2020(5): 39-58. | |

| 20 | 陈少凌, 谭黎明, 杨海生, 等. 我国金融行业的系统重要性研究——基于HD-TVP-VAR模型的复杂网络分析[J]. 系统工程理论与实践, 2021, 41(8): 1911-1925. |

| Chen S L, Tan L M, Yang H S, et al. A study on the systemic importance of financial industries: A complex network analysis based on HD-TVP-VAR model[J]. Systems Engineering-Theory & Practice, 2021, 41(8): 1911-1925. | |

| 21 | Demirer M, Diebold F X, Liu L, et al. Estimating global bank network connectedness[J]. Journal of Applied Econometrics, 2018, 33(1): 1-15. |

| 22 | 周开国, 季苏楠, 杨海生. 系统性金融风险跨市场传染机制研究——基于金融协调监管视角[J]. 管理科学学报, 2021, 24(7): 1-20. |

| Zhou K G, Ji S N, Yang H S. Cross-market contagion mechanism of systemic risk from the perspective of coordinated supervision[J]. Journal of Management Sciences in China, 2021, 24(7): 1-20. | |

| 23 | 钟婉玲, 李海奇. 国际油价、宏观经济变量与中国股市的尾部风险溢出效应研究[J]. 中国管理科学, 2022, 30(2): 27-37. |

| Zhong W L, Li H Q. Tail risk spillover effects among crude oil price, macroeconomic variables and China’s stock market[J]. Chinese Journal of Management Science, 2022, 30(2): 27-37. | |

| 24 | 欧阳资生, 杨希特, 黄颖. 嵌入网络舆情指数的中国金融机构系统性风险传染效应研究[J]. 中国管理科学, 2022, 30(4): 1-12. |

| Ouyang Z S, Yang X T, Huang Y. Research on systemic risk contagion effect of Chinese financial institutions considering network public opinion index[J]. Chinese Journal of Management Science, 2022, 30(4): 1-12. | |

| 25 | Benoit S, Colliard J E, Hurlin C, et al. Where the risks lie: A survey on systemic risk[J]. Review of Finance, 2017, 21(1): 109-152. |

| 26 | Baruník J, Křehlík T. Measuring the frequency dynamics of financial connectedness and systemic risk[J]. Journal of Financial Econometrics, 2018,16(2): 271-296. |

| 27 | 欧阳资生, 周学伟, 谢楠. 中国金融机构时变关联性测度研究—来自频域视角的新证据[J]. 系统工程理论与实践, 2022, 42(8): 2087-2101. |

| Ouyang Z S, Zhou X W, Xie N. Time-varying connectedness measurement of Chinese financial institutions: New evidence from the frequency domain perspective[J]. Systems Engineering-Theory & Practice, 2022, 42(8): 2087-2101. | |

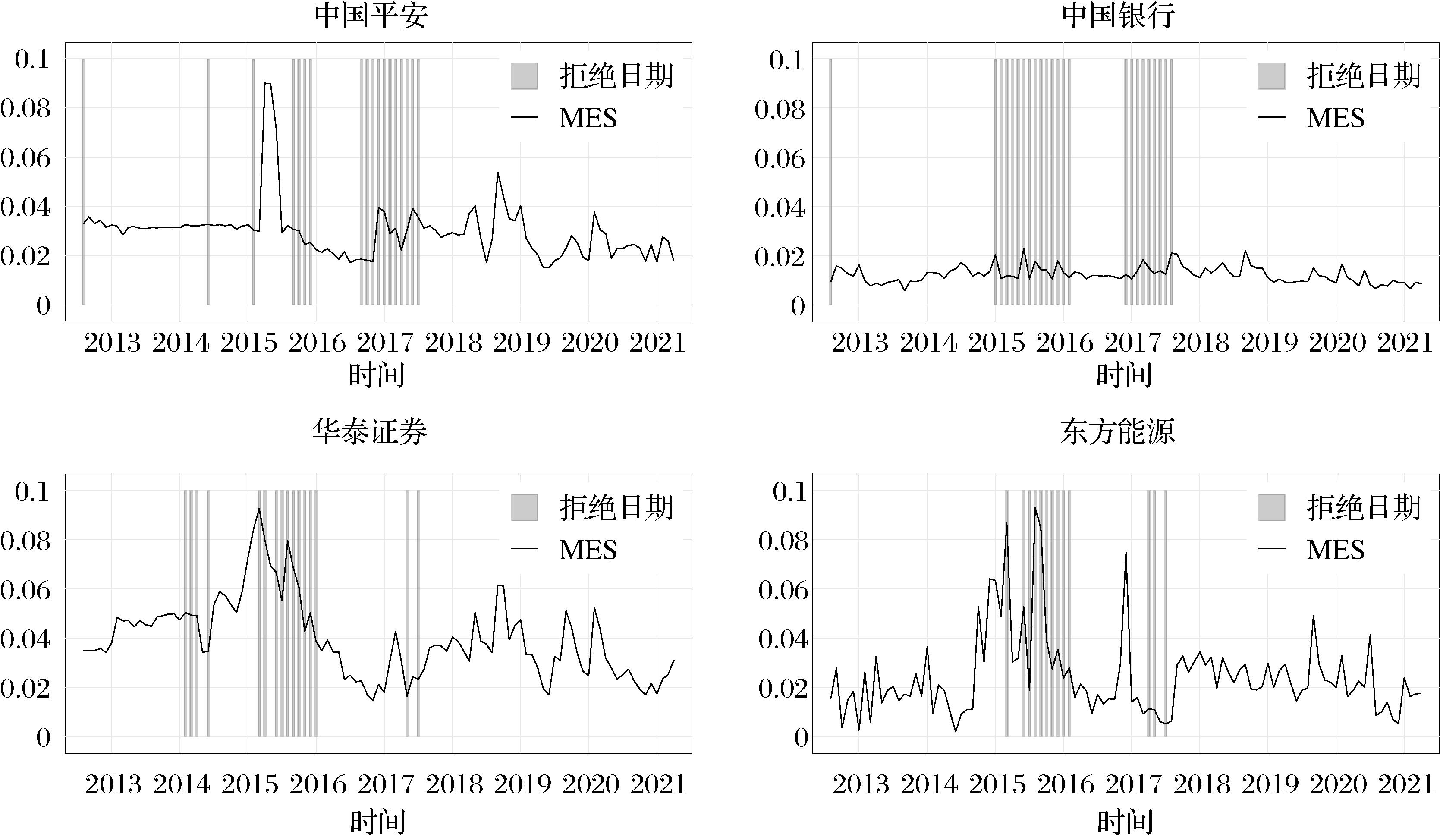

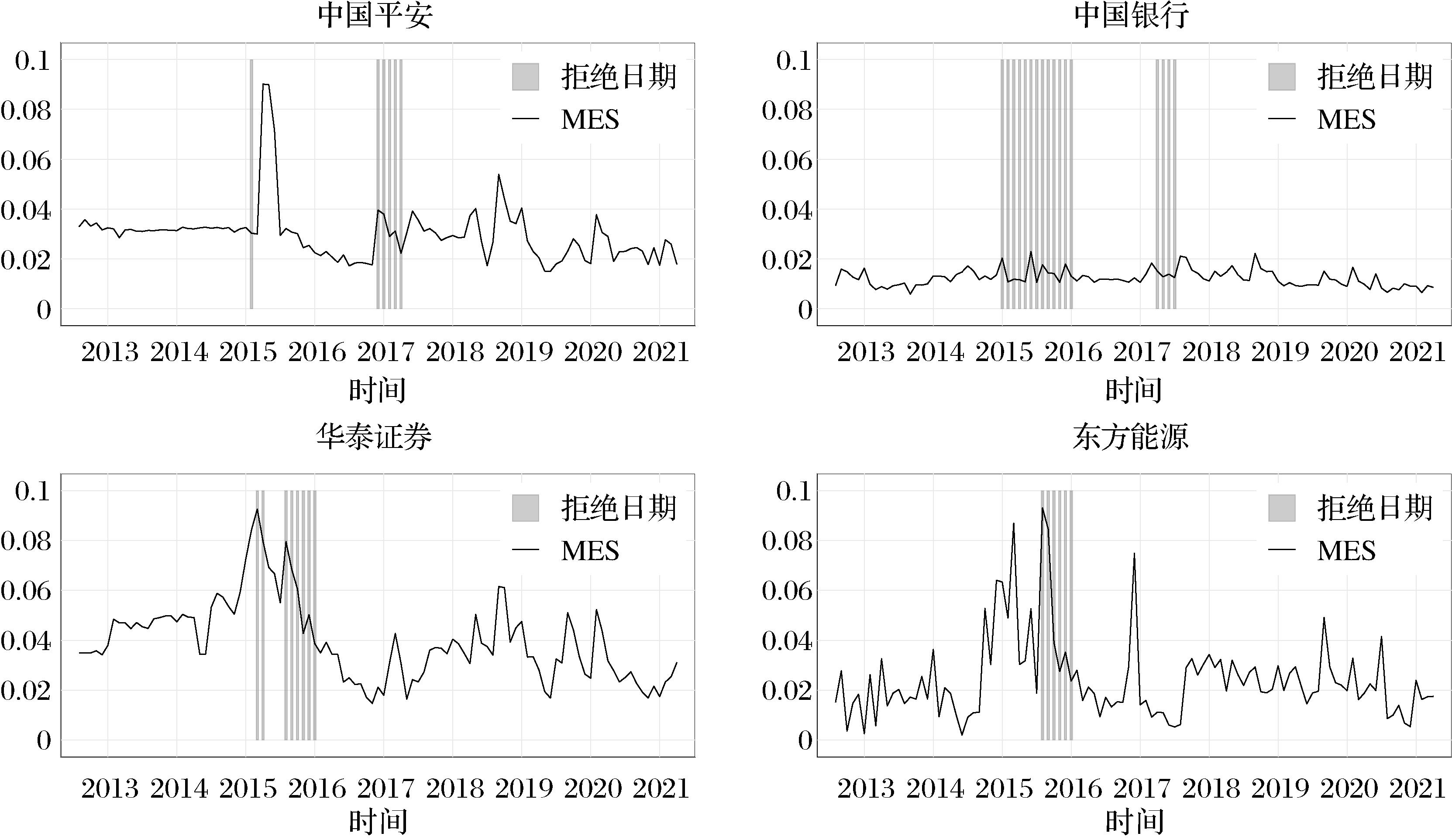

| 28 | Banulescu-Radu D, Hurlin C, Leymarie J, et al. Backtesting marginal expected shortfall and related systemic risk measures[J]. Management Science, 2020, 67(9): 5730-5754. |

| 29 | Baruník J, Kley T. Quantile coherency: A general measure for dependence between cyclical economic variables[J].The Econometrics Journal,2019,22(2): 131-152. |

| 30 | Hué S, Lucotte Y, Tokpavi S. Measuring network systemic risk contributions: A leave-one-out approach[J]. Journal of Economic Dynamics and Control, 2019, 100: 86-114. |

| 31 | 欧阳资生, 莫廷程. 基于广义CoVaR模型的系统重要性银行的风险溢出效应研究[J]. 统计研究, 2017, 34(9): 36-43. |

| Ouyang Z S, Mo T C. Research on the risk spillover effect of the systemically importance bank based on a generalized CoVaR model[J]. Statistical Research, 2017, 34(9): 36-43. | |

| 32 | Meuleman E, Vander Vennet R. Macroprudential policy and bank systemic risk[J]. Journal of Financial Stability, 2020, 47: 100724. |

| 33 | Girardi G, Tolga Ergün A. Systemic risk measurement: Multivariate GARCH estimation of CoVaR[J]. Journal of Banking & Finance, 2013, 37(8): 3169-3180. |

| 34 | Han H, Linton O, Oka T, et al. The cross-quantilogram: Measuring quantile dependence and testing directional predictability between time series[J]. Journal of Econometrics, 2016, 193(1): 251-270. |

| 35 | 贾妍妍, 方意, 荆中博. 中国金融体系放大了实体经济风险吗[J]. 财贸经济, 2020(10): 111-128. |

| Jia Y Y, Fang Y, Jing Z B. Does China’s financial system amplify risks in the real economy?[J]. Finance & Trade Economics, 2020(10): 111-128. | |

| 36 | Härdle W K, Wang W, Yu L. TENET: Tail-Event driven NETwork risk[J]. Journal of Econometrics, 2016, 192(2): 499-513. |

| 37 | 陈昆亭, 周炎. 防范化解系统性金融风险——西方金融经济周期理论货币政策规则分析[J]. 中国社会科学, 2020(11): 192-203. |

| Chen K T, Zhou Y. Preventing resolving systemic financial risks: An analysis of the monetary policy rules of western financial and economic cycle theory [J]. Social Sciences in China, 2020(11): 192-203. | |

| 38 | 杨子晖, 周颖刚. 全球系统性金融风险溢出与外部冲击[J]. 中国社会科学, 2018(12): 69-90+200-201. |

| Yang Z H, Zhou Y G. Global systemic financial risk spillovers and their external impact[J]. Social Sciences in China, 2018(12): 69-90+200+201. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||