主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (3): 1-12.doi: 10.16381/j.cnki.issn1003-207x.2022.0567

Haixiang Yao1,2, Qiuyu Liu1, Xiaoguang Yang3,4( )

)

Received:2022-03-22

Revised:2022-10-22

Online:2025-03-25

Published:2025-04-07

Contact:

Xiaoguang Yang

E-mail:xgyang@iss.ac.cn

CLC Number:

Haixiang Yao, Qiuyu Liu, Xiaoguang Yang. Strengthening or Weakening: Systemic Risk Spillovers between Diversified Financial in Dustries and Traditional Financial Industries[J]. Chinese Journal of Management Science, 2025, 33(3): 1-12.

"

| 状态变量 | 计算方法 |

|---|---|

| 股票市场收益率(m1) | 沪深300指数收益率 |

| 股票市场波动(m2) | 沪深300指数波动率 |

| 期限利差变动(m3) | 10年期国债即期收益率与一年期国债即期收益率之差 |

| 流动性价差(m4) | 6个月Shibor与6个月固定利率国债到期收益率之差 |

| 房地产超额收益(m5) | 沪深300房地产指数收益率与上证综指收益率之差 |

"

| 行业 | 均值 | 标准差(%) | 偏度 | 峰度 |

|---|---|---|---|---|

| 银行业 | 0 | 1.8038 | 0.0227 | 8.5673 |

| 证券业 | 0.0001 | 2.6150 | 0.0788 | 5.9657 |

| 保险业 | -0.0001 | 2.2472 | 0.0293 | 6.0799 |

| 新型金融 | 0.0003 | 2.3323 | 0.5573 | 6.3353 |

"

| 指标 | 银行业 | 证券业 | 保险业 | 新型金融 |

|---|---|---|---|---|

| ADF值 | -55.62*** | -53.63*** | -55.42*** | -52.79*** |

| 概率值P | 0.0001 | 0.0001 | 0.0001 | 0.0001 |

| 平稳性 | 平稳 | 平稳 | 平稳 | 平稳 |

"

| 变量 | ||||

|---|---|---|---|---|

j i | 银行业 | 证券业 | 保险业 | 新型金融 |

| 银行业 | 2.90 | 3.02 | -2.11 | |

| 证券业 | 2.18 | 2.60 | -2.78 | |

| 保险业 | 2.47 | 3.24 | -2.50 | |

| 新型金融 | -1.78 | -3.45 | -2.52 | |

"

"

"

"

"

"

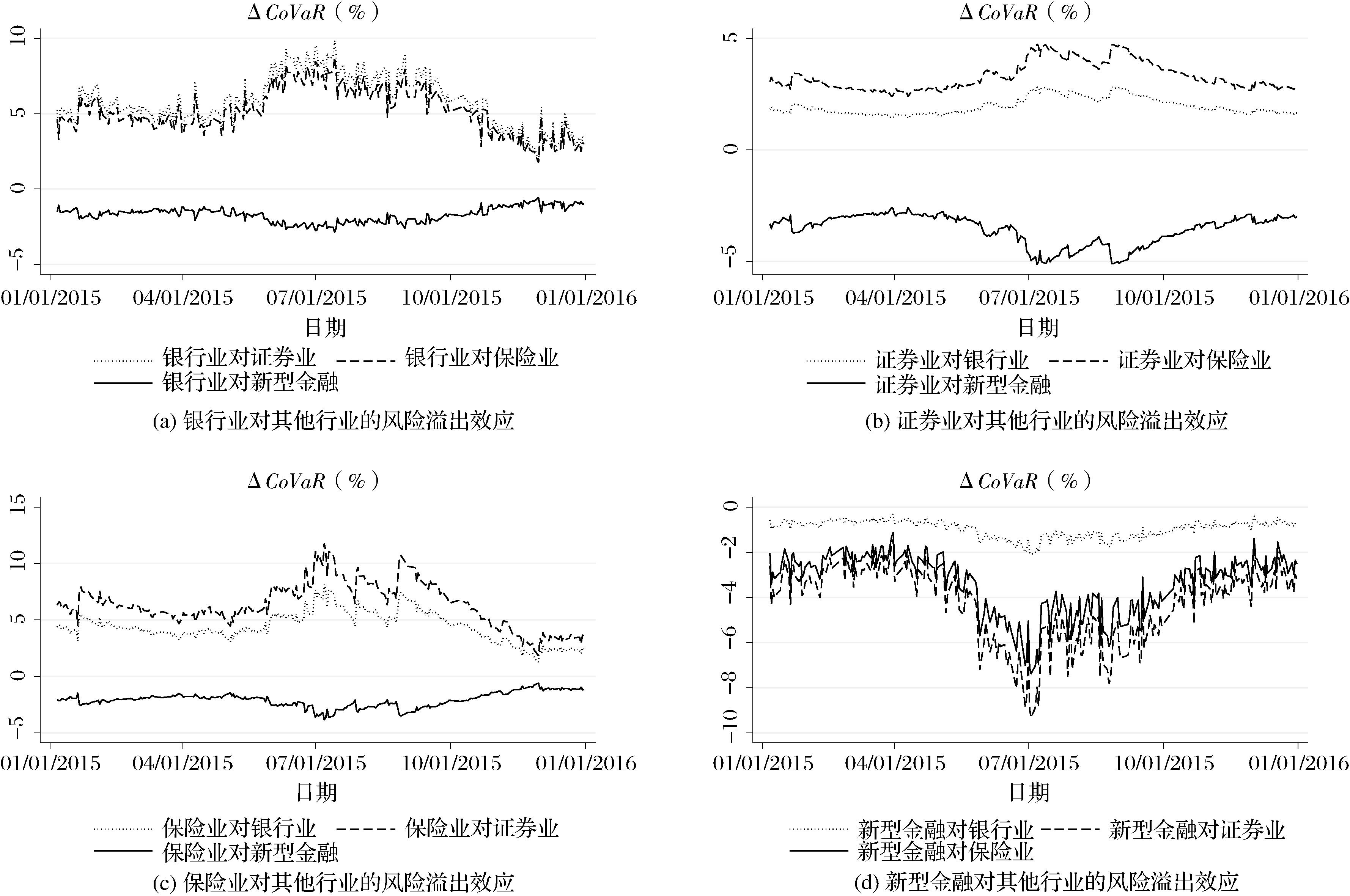

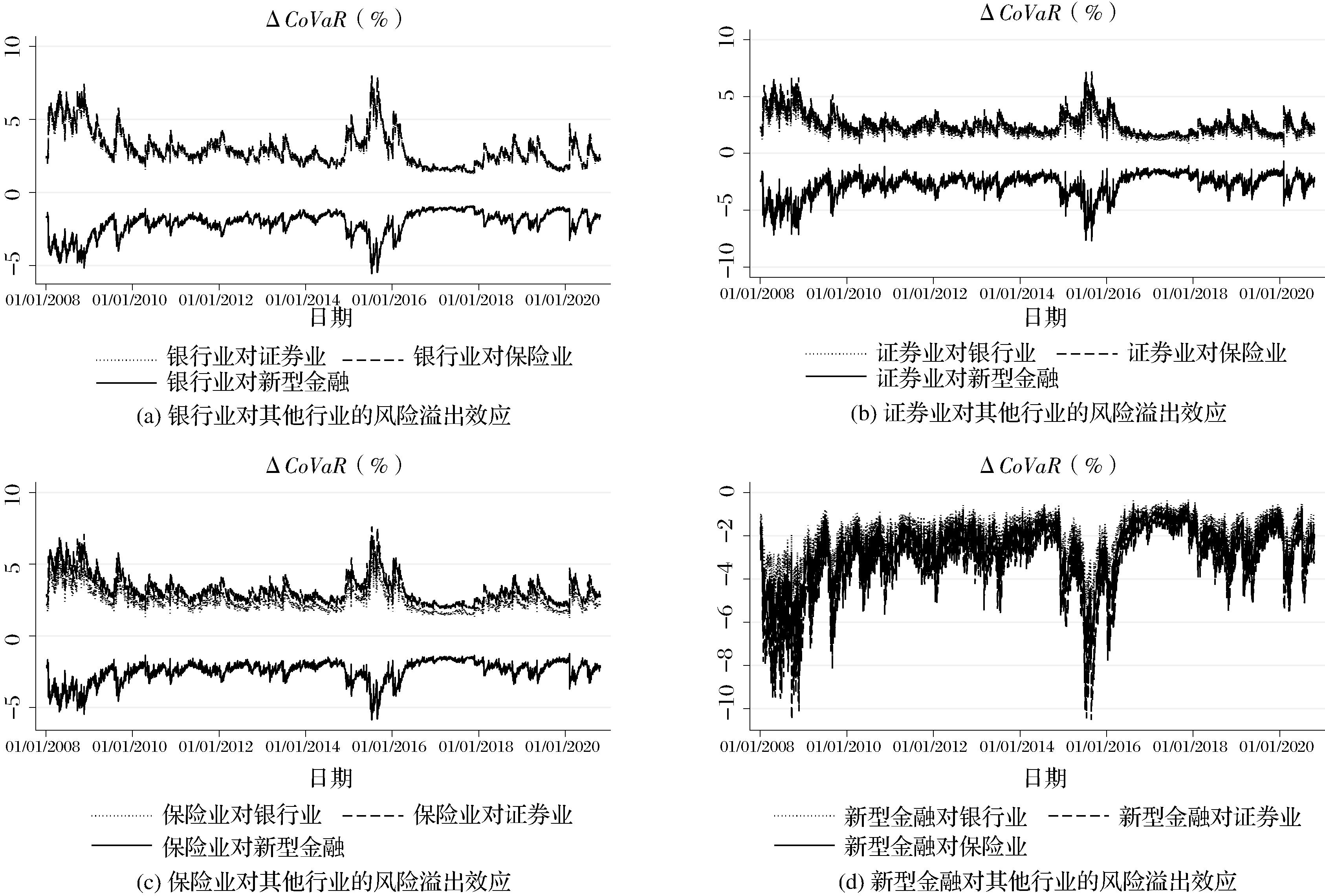

| 数量 | 2008年 | 2015年 | ||||||

|---|---|---|---|---|---|---|---|---|

j i | 银行业 | 证券业 | 保险业 | 新型金融 | 银行业 | 证券业 | 保险业 | 新型金融 |

| 银行业 | 0.736 | 0.911 | -1.028 | 1.343 | 1.193 | -0.390 | ||

| 证券业 | 0.616 | 0.644 | -0.781 | 0.326 | 0.549 | -0.594 | ||

| 保险业 | 0.689 | 0.623 | -0.750 | 0.861 | 1.245 | -0.408 | ||

| 新型金融 | -0.646 | -0.823 | -0.675 | -0.185 | -0.822 | -0.651 | ||

| 2020年 | 2017年 | |||||||

| 银行业 | 1.397 | 1.329 | -0.923 | 0.708 | 1.500 | 0.025 | ||

| 证券业 | 0.506 | 0.693 | -0.799 | 0.523 | 0.216 | -0.416 | ||

| 保险业 | 0.722 | 1.264 | -0.823 | 0.383 | 0.366 | -0.096 | ||

| 新型金融 | -0.344 | -1.218 | -0.831 | -0.157 | -0.830 | -0.216 | ||

| 1 | 国际货币基金组织. 2011年4月期全球金融稳定报告[M]. 北京:中国金融出版社, 2011. |

| International Monetary Fund. April 2011 global financial stability report [M]. Beijing: China Financial Publishing House, 2011. | |

| 2 | European Central Bank. Annual report 2010[EB/OL].(2011-02-25)[2011-02-25]. . |

| 3 | 谢志刚 .系统性风险与系统重要性:共识和方向[J].保险研究,2016(7):25-34. |

| Xie Z G .Systemic risks and systemic importance: Consensus and future directions[J].Insurance Studies,2016(7):25-34. | |

| 4 | 杨子晖,陈里璇,陈雨恬 .经济政策不确定性与系统性金融风险的跨市场传染——基于非线性网络关联的研究[J].经济研究,2020, 55(1):65-81. |

| Yang Z H, Chen L X, Chen Y T .Cross-market contagion of economic policy uncertainty and systemic financial risk: A nonlinear network connectedness analysis[J].Economic Research Journal,2020, 55(1):65-81. | |

| 5 | 陆静,胡晓红 .基于条件在险价值法的商业银行系统性风险研究[J].中国软科学, 2014(4):25-42. |

| Lu J, Hu X H .Study on systemic risk of commercial banks based on conditional value at risk[J].China Soft Science, 2014(4):25-42. | |

| 6 | 白雪梅,石大龙 .中国金融体系的系统性风险度量[J].国际金融研究,2014(6):75-85. |

| Bai X M, Shi D L .Measurement of the systemic risk of China’s financial system[J].Studies of International Finance,2014(6):75-85. | |

| 7 | White H, Kim T H, Manganelli S. VAR for VaR: Measuring tail dependence using multivariate regression quantiles[J]. Journal of Econometrics, 2015,187(1): 169-188 |

| 8 | Hartmann P, Straetmans S, Vries C D. Asset market linkages in crisis periods[J]. Review of Economics and Statistics, 2004, 86(1): 3113-3126. |

| 9 | 裴茜,朱书尚.中国股票市场金融传染及渠道——基于行业数据的实证研究[J]. 管理科学学报,2019,22(3):90-112. |

| Pei X, Zhu S S.Financial contagion in China’s stock market: A study based on industry-level data[J]. Journal of Management Sciences in China,2019,22(3):90-112. | |

| 10 | 杨子晖,陈雨恬,张平淼 .重大突发公共事件下的宏观经济冲击、金融风险传导与治理应对[J].管理世界,2020,36(5):13-35+7. |

| Yang Z H, Chen Y T, Zhang P M .Macroeconomic shock, financial risk transmission and governance response to major public emergencies[J].Journal of Management World,2020,36(5):13-35+7. | |

| 11 | 陈建青, 王擎, 许韶辉. 金融行业间的系统性金融风险溢出效应研究[J]. 数量经济技术经济研究, 2015, 32(9): 89-100. |

| Chen J Q, Wang Q, Xu S H. A CoVaR research on spillover effect of systemic financial risk between financial sub-sectors[J]. The Journal of Quantitative & Technical Economics, 2015, 32(9): 89-100. | |

| 12 | 苏明政, 张庆君. 关联性视阈下我国金融行业间系统性风险传染效应研究[J]. 会计与经济研究, 2015, 29(6): 111-124. |

| Su M Z, Zhang Q J. A Study on the contagion effect of systemic risk in Chinese financial sectors: A correlation perspective[J]. Journal of Accounting and Economics, 2015, 29(6): 111-124. | |

| 13 | 梁琪,常姝雅.我国金融混业经营与系统性金融风险——基于高维风险关联网络的研究[J].财贸经济,2020,41(11):67-82. |

| Liang Q, Chang S Y. China’s universal financial operation and financial systemic Risk:A study on high-dimensional risk interconnected network[J].Finance & Trade Economics,2020,41(11):67-82. | |

| 14 | 彭建刚,邹克,蒋达.混业经营对金融业系统性风险的影响与我国银行业经营模式改革[J].中国管理科学,2014,22(S1):272-280. |

| Peng J G, Zou K, Jiang D. Effect of mixed operation on financial systemic risk and reform of business model of China banking[J].Chinese Journal of Management Science,2014,22(S1):272-280. | |

| 15 | Wagner W. Diversification at financial institutions and systemic crises[J]. Journal of Financial Intermediation,2009,19(3): 373-386 |

| 16 | Allen F, Gale D. Optimal currency crises[J]. Carnegie-Rochester Conference Series on Public Policy, 2000, 53(1): 177-230. |

| 17 | 李政,梁琪,涂晓枫 .我国上市金融机构关联性研究——基于网络分析法[J].金融研究,2016(8):95-110. |

| Li Z, Liang Q, Tu X F .The connectedness of Chinese listed financial institutions: A study based on network analysis[J].Journal of Financial Research,2016(8):95-110. | |

| 18 | 欧阳红兵,刘晓东 .中国金融机构的系统重要性及系统性风险传染机制分析——基于复杂网络的视角[J].中国管理科学,2015,23(10):30-37. |

| Ouyang H B, Liu X D .An analysis of the systemic importance and systemic risk contagion mechanism of China’s financial institutions based on network analysis[J].Chinese Journal of Management Science,2015,23(10):30-37. | |

| 19 | Adrian T, Brunnermeier M K. CoVaR[J]. American Economic Review,2016,106(7):1705-1741. |

| 20 | Girardi G, Erguen A T. Systemic risk measurement: Multivariate GARCH estimation of CoVaR[J]. Journal of Banking & Finance, 2013, 37(8): 3169-3180. |

| 21 | 李政,涂晓枫,卜林 .金融机构系统性风险:重要性与脆弱性[J].财经研究,2019,45(2):100-112+152. |

| Li Z, Tu X F, Bu L .Systemic risks of financial institutions: Importance and vulnerability[J].Journal of Finance and Economics,2019,45(2):100-112+152. | |

| 22 | 韩浩,王向楠,刘璐 .保险业系统性风险及对相关行业的溢出效应研究[J].保险研究,2020(7):31-48. |

| Han H, Wang X N, Liu L .Insurance industry’s systemic risk and its spillover effect on related sectors[J].Insurance Studies,2020(7):31-48. | |

| 23 | 姚登宝, 施腾, 刘治戎. 金融周期视角下中国系统性金融风险的状态转换效应研究[J].金融经济学研究, 2021, 36(2): 3-17. |

| Yao D B, Shi T, Liu Z R. State transition effect of China’s systemic financial risks from the financial cycle perspective[J].Financial Economics Research, 2021, 36(2): 3-17. | |

| 24 | 张冰洁,汪寿阳,魏云捷,赵雪婷. 基于CoES模型的我国金融系统性风险度量[J]. 系统工程理论与实践,2018,38(3):565-575. |

| Zhang B J, Wang S Y, Wei Y J,et al. Measuring the systemic risk contribution of financial institutes in China based on coesmodel[J]. Systems Engineering-Theory & Practice,2018,38(3):565-575. | |

| 25 | 李政,梁琪,方意. 中国金融部门间系统性风险溢出的监测预警研究——基于下行和上行ΔCoES指标的实现与优化[J]. 金融研究,2019(2):40-58. |

| Li Z, Liang Q, Fang Y. Monitoring and forewarning of systemic risk spillover in China’s financial sector based on modified coes indicators[J]. Journal of Financial Research,2019(2):40-58. | |

| 26 | Acharya V V, Pedersen L H, Philippon T, et al. Measuring systemic risk[J]. The Review of Financial Studies, 2017, 30(1): 2-47. |

| 27 | 卜林,李政 .我国上市金融机构系统性风险溢出研究——基于CoVaR和MES的比较分析[J].当代财经,2015(6):55-65. |

| Bu L, Li Z .A study of systematic risk spillover of China’s listed financial institutions: A comparative analysis based on covar and MES[J].Contemporary Finance & Economics,2015(6):55-65. | |

| 28 | Brownlees C, Engle R F. SRISK: A conditional capital shortfall measure of systemic risk[J]. The Review of Financial, 2017, 30(1):48-79 |

| 29 | 陈湘鹏,周皓,金涛,等. 微观层面系统性金融风险指标的比较与适用性分析——基于中国金融系统的研究[J]. 金融研究,2019(5):17-36. |

| Chen X P, Zhou H, Jin T, et al. Comparison and applicability analysis of micro-level systemic risk measures: A study based on China’s financial system[J]. Journal of Financial Research,2019(5):17-36. | |

| 30 | 赵林海, 陈名智. 金融机构系统性风险溢出和系统性风险贡献——基于滚动窗口动态Copula模型双时变相依视角[J]. 中国管理科学, 2021, 29(7): 71-83. |

| Zhao L H, Chen M Z. Systemic risk spillovers and systemic risk contributions of financial institutions in China: A perspective of dual time:Varing dependence of rolling window dynamic copula model[J]. Chinese Journal of Management Science, 2021, 29(7): 71-83. | |

| 31 | Koenker R, Bassett Jr G. Regression quantiles[J]. Econometrica, 1978(46): 33-50. |

| 32 | 胡吉祥. 互联网金融对证券业的影响[J]. 中国金融, 2013(16): 73-74. |

| Hu J X. TheIinfluence of internet finance on securities industry[J]. China Finance, 2013(16): 73-74. | |

| 33 | 朱晓谦,李靖宇,李建平,等.基于危机条件概率的系统性风险度量研究[J].中国管理科学,2018,26(6):1-7. |

| Zhu X Q, Li J Y, Li J P, et al.An indicator of conditional probability of crisis for systemic risk measurement[J].Chinese Journal of Management Science,2018,26(6):1-7. | |

| 34 | 陈守东,王妍. 我国金融机构的系统性金融风险评估——基于极端分位数回归技术的风险度量[J]. 中国管理科学,2014,22(7):10-17. |

| Chen S D,WangY. Measuring systemic financial risk of China’s financial institutions:Applying extremal quantile regression technology and covarmodel[J]. Chinese Journal of Management Science,2014,22(7):10-17. | |

| 35 | 李绍芳, 刘晓星. 中国金融机构关联网络与系统性金融风险[J]. 金融经济学研究, 2018, 33(5): 34-48. |

| Li S F, Liu X X. The interconnected network and systemic risk of China’s financial Institutions[J]. Financial Economics Research, 2018, 33(5): 34-48. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||