主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (2): 28-37.doi: 10.16381/j.cnki.issn1003-207x.2024.1777

Previous Articles Next Articles

Yang Lu1,2, Baofeng Shi1,2( )

)

Received:2024-09-30

Revised:2024-10-24

Online:2025-02-25

Published:2025-03-06

Contact:

Baofeng Shi

E-mail:shibaofeng@nwsuaf.edu.cn

CLC Number:

Yang Lu, Baofeng Shi. Min-max Algorithm for Matching Credit Ratings with Loss Given Default[J]. Chinese Journal of Management Science, 2025, 33(2): 28-37.

"

贷款人 编号 | 应收本息和Ri | 应收未收 本息Li | 银行A的 排名 | 银行B的 排名 |

|---|---|---|---|---|

| Loan 1 | 1 | 0 | 1 | 10 |

| Loan 2 | 1 | 0.1 | 2 | 9 |

| Loan 3 | 1 | 0.2 | 3 | 8 |

| Loan 4 | 1 | 0.3 | 4 | 7 |

| Loan 5 | 1 | 0.4 | 5 | 6 |

| Loan 6 | 1 | 0.5 | 6 | 5 |

| Loan 7 | 1 | 0.6 | 7 | 4 |

| Loan 8 | 1 | 0.7 | 8 | 3 |

| Loan 9 | 1 | 0.8 | 9 | 2 |

| Loan 10 | 1 | 0.9 | 10 | 1 |

"

| 借款人编号 | 应收本息和(元) | 应收未收本息和(元) | 信用得分 |

|---|---|---|---|

| Loan 1 | 103910 | 0 | 99.99 |

| Loan 2 | 103915 | 0 | 99.97 |

| … | … | … | … |

| Loan 1226 | 104263 | 316.5536 | 89.17 |

| Loan 1227 | 103871.5 | 0 | 89.17 |

| … | … | … | … |

| Loan 2156 | 103995 | 132.4311 | 46.61 |

| Loan 2157 | 10387.15 | 0 | 44.53 |

"

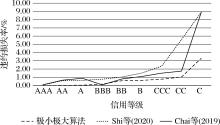

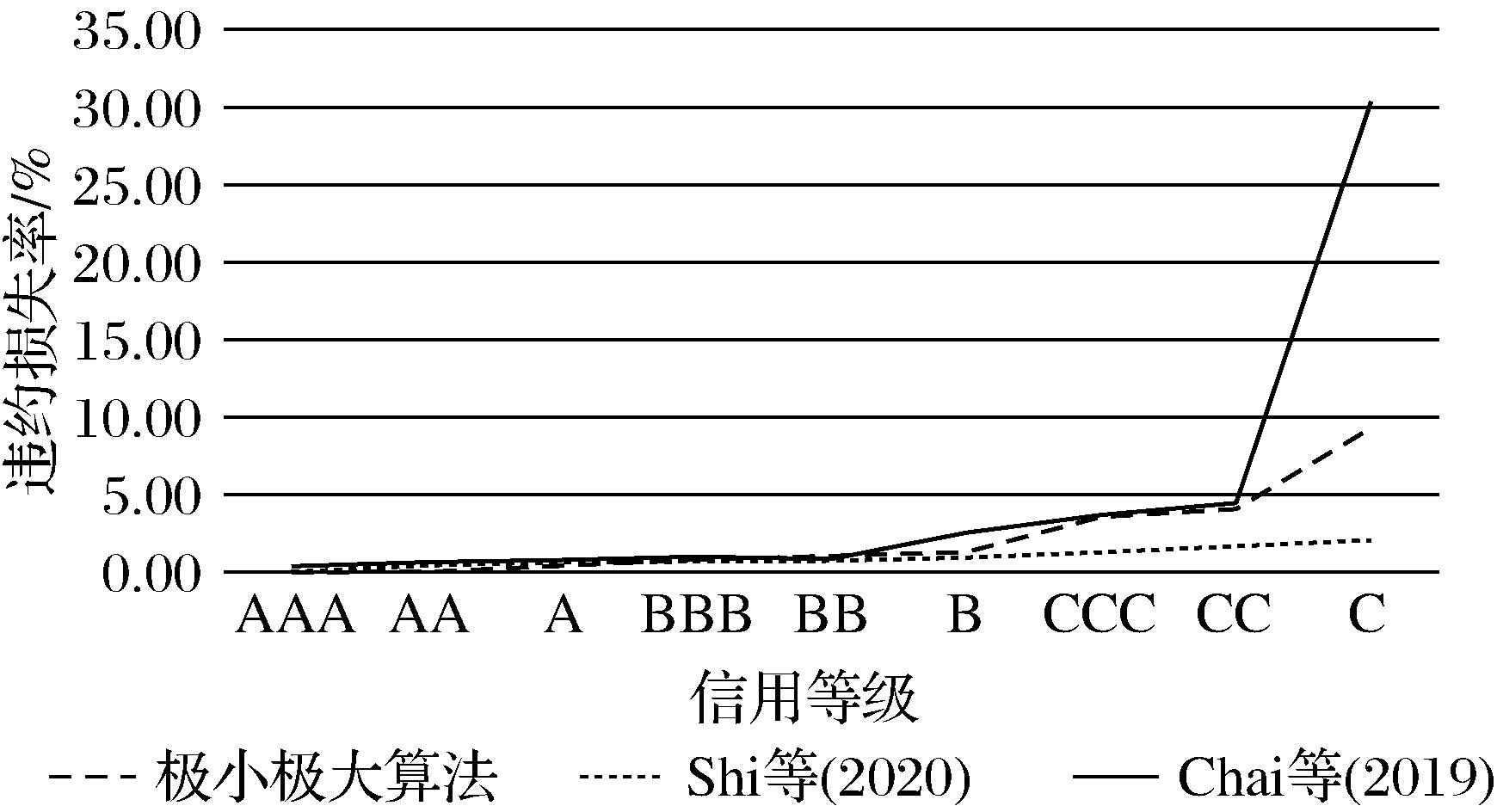

| 1 | 2 | 极小极大算法 | Shi 等(2020) | Chai 等 (2019) | |||

|---|---|---|---|---|---|---|---|

| 3 | 4 | 5 | 6 | 7 | 8 | ||

| 等级 | 等级 | 样本量 | LGDk | 样本量 | LGDk | 样本量 | LGDk |

| 1 | AAA | 11 | 0.00% | 127 | 0.07% | 102 | 0.09% |

| 2 | AA | 67 | 0.02% | 518 | 0.60% | 478 | 0.65% |

| 3 | A | 1 | 0.04% | 756 | 0.63% | 493 | 0.88% |

| 4 | BBB | 48 | 0.17% | 312 | 0.77% | 283 | 0.08% |

| 5 | BB | 523 | 0.59% | 256 | 1.03% | 298 | 0.80% |

| 6 | B | 751 | 0.63% | 81 | 1.52% | 227 | 1.10% |

| 7 | CCC | 312 | 0.77% | 56 | 2.36% | 174 | 1.50% |

| 8 | CC | 256 | 1.03% | 22 | 5.58% | 73 | 1.75% |

| 9 | C | 188 | 3.32% | 29 | 8.92% | 29 | 8.92% |

| 计算复杂度 | |||||||

"

"

"

| 借款人编号 | 应收本息和(元) | 应收未收本息和(元) | 信用得分 |

|---|---|---|---|

| Loan 1 | 52613.75 | 0 | 96.54 |

| Loan 2 | 84294.4 | 0 | 96.32 |

| … | … | … | … |

| Loan 1218 | 54620 | 52894.48 | 88.69 |

| Loan 1219 | 31557.6 | 0 | 88.69 |

| … | … | … | … |

| Loan 2043 | 16345.125 | 6943.66 | 60.57 |

| Loan 2044 | 55505 | 55330.36 | 59.90 |

"

"

"

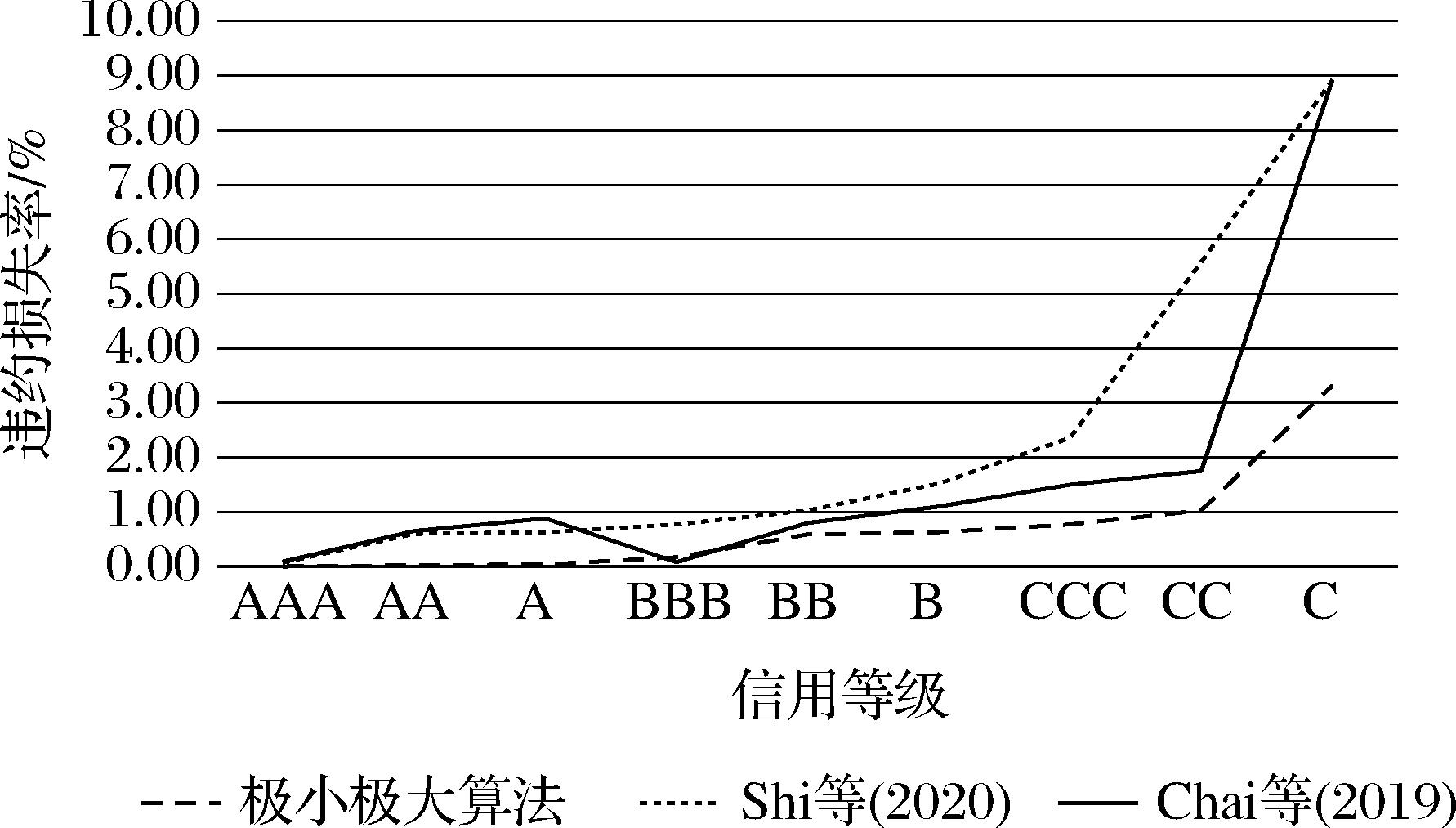

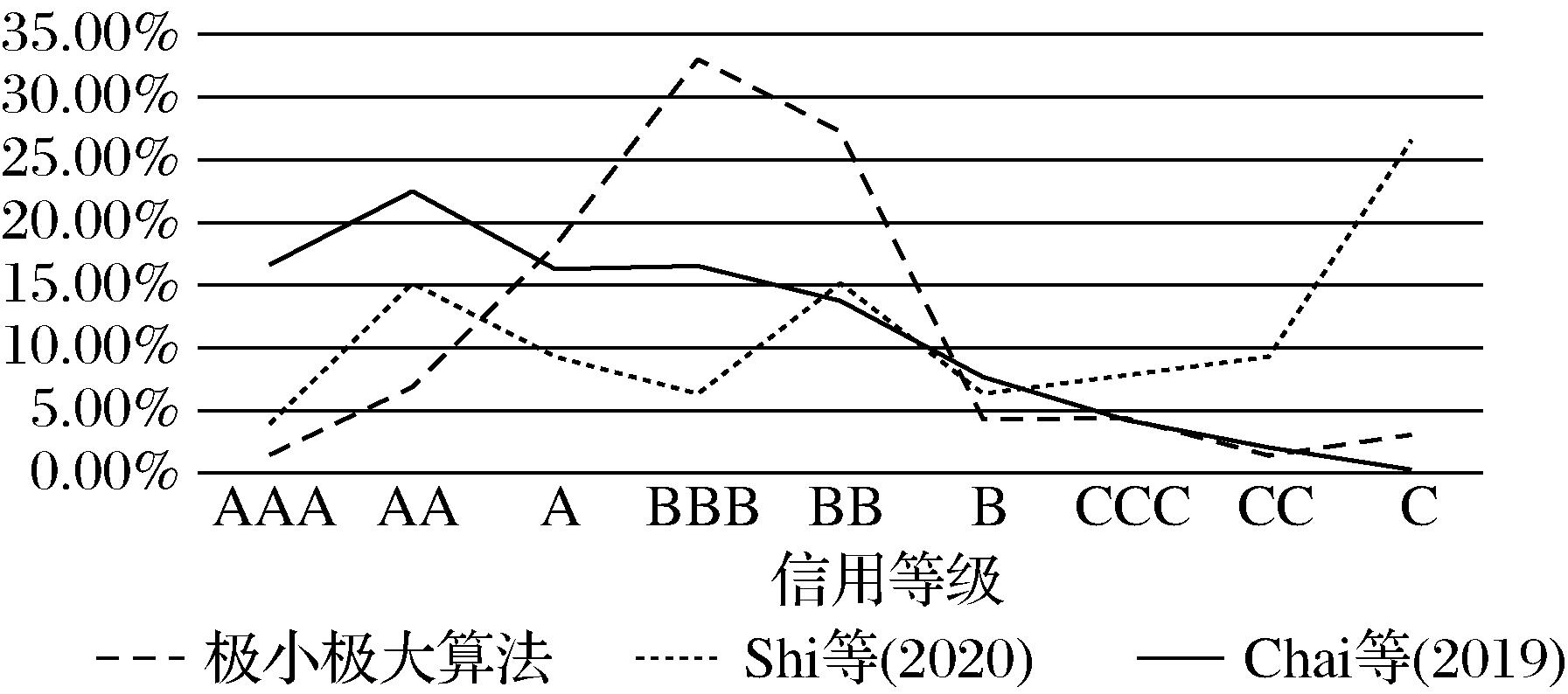

| 1 | 2 | 极小极大算法 | Shi 等(2020) | Chai 等 (2019) | |||

|---|---|---|---|---|---|---|---|

| 3 | 4 | 5 | 6 | 7 | 8 | ||

| 等级 | 等级 | 样本量 | LGDk | 样本量 | LGDk | 样本量 | LGDk |

| 1 | AAA | 30 | 0.00% | 81 | 0.01% | 340 | 0.37% |

| 2 | AA | 141 | 0.01% | 310 | 0.42% | 460 | 0.63% |

| 3 | A | 371 | 0.40% | 190 | 0.63% | 333 | 0.78% |

| 4 | BBB | 675 | 0.80% | 130 | 0.67% | 338 | 0.99% |

| 5 | BB | 557 | 1.04% | 310 | 0.72% | 281 | 0.84% |

| 6 | B | 88 | 1.28% | 130 | 0.93% | 157 | 2.54% |

| 7 | CCC | 90 | 3.55% | 160 | 1.27% | 87 | 3.68% |

| 8 | CC | 29 | 4.07% | 190 | 1.66% | 42 | 4.45% |

| 9 | C | 63 | 9.29% | 543 | 2.05% | 6 | 30.35% |

| 计算复杂度 | |||||||

| 1 | Bolton P, Freixas X, Shapiro J. The credit ratings game[J]. Journal of Finance, 2012, 67(1): 85-111. |

| 2 | Goldstein I, Huang C. Credit rating inflation and firms’ investments[J]. Journal of Finance, 2020, 75(6):2929-2972. |

| 3 | Piccolo A, Shapiro J. Credit ratings and market information[J]. Review of Financial Studies, 2022, 35(10):4425-4473. |

| 4 | Li Y R, Wang H J, Gao H K, et al. Credit rating, repayment willingness and farmer credit default[J]. International Review of Financial Analysis, 2024, 93:103117. |

| 5 | Elliott R J, Siu T K, Fung E S. A double HMM approach to altman z-scores and credit ratings[J]. Expert Systems With Applications, 2014, 41(4): 1553-1560. |

| 6 | Basel Committee on Banking Supervision. International convergence of capital measurement and capital standards: A revised framework[R]. Discussion Paper, Bank for International Settlements, Basel, 2005. |

| 7 | Shi B F, Zhao X, Wu B. Credit rating and microfinance lending decisions based on loss given default (LGD)[J]. Finance Research Letters, 2019, 30: 124-129. |

| 8 | Lappas P Z, Yannacopoulos A N. A machine learning approach combining expert knowledge with genetic algorithms in feature selection for credit risk assessment[J]. Applied Soft Computing, 2021, 107:107391. |

| 9 | Tezerjan M Y, Samghabadi A S, Memariani A. ARF: A hybrid model for credit scoring in complex systems[J]. Expert Systems with Applications, 2021, 185:115634. |

| 10 | Roy P K, Shaw K. Ishizaka A. Developing an integrated fuzzy credit rating system for SMEs using fuzzy-BWM and fuzzy-TOPSIS-Sort-C[J]. Annals Of Operations Research, 2023, 325(2):1197-1229. |

| 11 | Chen R D, Chen X H, Jin C L, et al. Credit rating of online lending borrowers using recovery rates[J]. International Review of Economics & Finance, 2020, 68:204-216. |

| 12 | Le R, Ku H, Jun D. Sequence-based clustering applied to long-term credit risk assessment[J]. Expert Systems with Applications, 2021, 165: 72-85. |

| 13 | Gaganis C, Papadimitri P, Tasiou M. A multicriteria decision support tool for modelling bank credit ratings[J]. Annals of Operations Research, 2021, 306(1-2):27-56. |

| 14 | Chen Y J, Chen Y M. Forecasting corporate credit ratings using big data from social media[J]. Expert Systems with Applications, 2022, 207:118042. |

| 15 | Sha Y Z. Rating manipulation and creditworthiness for platform economy: Evidence from peer-to-peer lending[J]. International Review of Financial Analysis, 2022, 84:102393. |

| 16 | Zhang Y J, Chi G T. A credit rating model based on a customer number bell-shaped distribution[J]. Management Decision, 2018, 56(5): 987-1007. |

| 17 | 迟国泰,于善丽.基于违约鉴别能力最大的信用等级划分方法[J].管理科学学报, 2019, 22(11): 106-126. |

| Chi G T, Yu S L. Credit rating division method with maximum default identification capability[J]. Journal of Management Sciences in China, 2019, 22(11): 106-126. | |

| 18 | Shi B F, Chi G T, Li W P. Exploring the mismatch between credit ratings and loss-given-default: A credit risk approach[J]. Economic Modelling, 2020, 85: 420-428. |

| 19 | 周颖,张志鹏.基于违约企业分布约束的上市公司信用等级划分模型[J].管理评论, 2023, 35(5): 3-18. |

| Zhou Y, Zhang Z P. Listed company credit rating division model based on defaulting customer distribution constraint[J]. Management Review, 2023, 35(5):3-18. | |

| 20 | BCBS, Basel Committee on Banking Supervision. Basel III: Finalizing post-crisis reforms [R]. Discussion Paper, Bank for International Settlements, Basel, 2017. |

| 21 | Calabrese R. Downturn loss given default: Mixture distribution estimation[J]. European Journal of Operational Research, 2014, 237(1): 271-277. |

| 22 | Nazemi A, Pour F F, Heidenreich K, et al. Fuzzy decision fusion approach for loss-given-default modeling[J]. European Journal of Operational Research, 2017, 262(2): 780-791. |

| 23 | Yao X, Crook J, Andreeva G. Support vector regression for loss given default modelling[J]. European Journal of Operational Research, 2015, 240(2): 528-538. |

| 24 | Chai N N, Shi B F, Hua Y T. Loss given default or default status: Which is better to determine farmers? credit ratings?[J]. Finance Research Letters, 2023, 53:103674. |

| 25 | 袁先智,何华,张启珑,等.在大数据框架下建立与国际接轨并适合中国金融市场国情的主体信用评级体系[C]//第十七届中国管理学年会, 南京,中国, 8月19-21日,中国学术期刊电子出版社, 2022: 869-885. |

| Yuan X Z, He H, Zhang Q L, et al. The framework of the credit rating system in the line with international standards for financial market in China by applting bigdata method [C]// Proceedings of the 17th Chinese Academy of Management Annual Conference, Nanjing,China, August 19-21 , China Academic Journal Electronic Publishing House, 2022:869-885. | |

| 26 | Wong K P. Regret theory and the banking firm: The optimal bank interest margin[J]. Economic Modelling, 2011, 28(6): 2483-2487. |

| 27 | 石宝峰,王静,迟国泰.普惠金融、银行信贷与商户小额贷款融资——基于风险等级匹配视角[J].中国管理科学, 2017, 25(9): 28-36. |

| Shi B F, Wang J, Chi G T. The inclusive finance, bank loans and financing of small private business microfinance loan: Based on matching credit risk and credit rating[J]. Chinese Journal of Management Science, 2017, 25(9):28-36. |

| [1] | Yi-yun CHEN, Man-lian CHEN. Qualitative Textual Information and Credit Rating: A Study Based on Risk Information in the Annual Report Text Content [J]. Chinese Journal of Management Science, 2023, 31(9): 94-104. |

| [2] | CHEN Ting-qiang, WANG Jie-peng, YANG Xiao-guang. Bilayer-Coupled Network Evolution Model of Counterparty Credit Risk Contagion in the CRT Market [J]. Chinese Journal of Management Science, 2023, 31(4): 260-274. |

| [3] | LI Cheng-gang, JIA Hong-ye, ZHAO Guang-hui, FU Hong. Credit Risk Warning of Listed Companies Based on Information Disclosure Text:Empirical Evidence from Management Discussion and Analysis of the Chinese Annual Report [J]. Chinese Journal of Management Science, 2023, 31(2): 18-29. |

| [4] | Jing GU,Ya-ting HU. The Transmission Effect of SMEs' Financial Distress on the Credit Risk of Suppliers [J]. Chinese Journal of Management Science, 2023, 31(12): 23-33. |

| [5] | GUO Wei-dong, ZHOU Zach Zhi-zhong, QIAN Chun-tao. Application of Mobile App List in Evaluating Borrowers’ Credit Risk——An Empirical Analysis of an Online Lending Platform [J]. Chinese Journal of Management Science, 2022, 30(12): 96-107. |

| [6] | YUAN George Xianzhi, , , , , , ZHAO Min, LIU Hai-yang, ZHOU Yun-peng, YAN Cheng-xing, SHI Bao-feng, CHAI Na-na, LIN Jian-wu, HE Cheng-ying, MA Sheng, ZHANG Qian-you, DING Xiao-wei. The Framework for Characteristic Factors of Poverty Statusby Using AI Algorithms:Related to the Path Choice of Rural Revitalization in China [J]. Chinese Journal of Management Science, 2022, 30(12): 234-244. |

| [7] | YAN Yan, LI Bo. Research on Influence Mechanism of Credit Ratings between Different Payers [J]. Chinese Journal of Management Science, 2022, 30(1): 1-11. |

| [8] | XIE Xiao-feng, YANG Yang, ZHANG Feng-ying, HU Xiu-ying, ZHOU Zong-fang. Contagion Effects of Associated Credit Risk in Supply Chain under Multiple Associated Relationships [J]. Chinese Journal of Management Science, 2021, 29(9): 77-89. |

| [9] | WANG Xiao-yan, ZHANG Zhong-yan, MA Shuang-ge. A Loan Credit Risk Model Incorporating Text Prior Information [J]. Chinese Journal of Management Science, 2021, 29(5): 34-44. |

| [10] | LI Zhe, CHI Guo-tai. Research on the Listed Companies' Credit Risk Based on Maximum Discrimination and Optimal Relative Membership Degree [J]. Chinese Journal of Management Science, 2021, 29(4): 1-15. |

| [11] | XU Kai, ZHOU Zong-fang, QIAN Qian. Study on the Contagion Mechanism of Associated Credit Risk with Double Propagation Path [J]. Chinese Journal of Management Science, 2021, 29(3): 49-58. |

| [12] | DONG Lu-an, YE Xin. Interpretable Credit Risk Assessment Modeling Based on Improved Pedagogical Method [J]. Chinese Journal of Management Science, 2020, 28(9): 45-53. |

| [13] | ZHU Xiao-qian, LI Jian-ping. A Review of Bank Risk Aggregation [J]. Chinese Journal of Management Science, 2020, 28(8): 1-14. |

| [14] | CHEN Ting-qiang, ZHOU Wen-jing, TONG Mao-di, LIU Hai-fei. Research on the Model of Inter-bank Credit Risk Contagion by Fusing CDS Networks [J]. Chinese Journal of Management Science, 2020, 28(6): 24-37. |

| [15] | YU Shan-li, CHI Guo-tai, JIANG Xin. Small Enterprise Facility Rating Based on the Maximum Discrimination of Indicator System [J]. Chinese Journal of Management Science, 2020, 28(6): 38-50. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||