主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2024, Vol. 32 ›› Issue (1): 260-267.doi: 10.16381/j.cnki.issn1003-207x.2020.0816

Yuting Yan,Wenjie Bi( )

)

Received:2020-05-08

Revised:2020-10-20

Online:2024-01-25

Published:2024-02-08

Contact:

Wenjie Bi

E-mail:beenjoy@126.com

CLC Number:

Yuting Yan,Wenjie Bi. A Data-driven Single-Period Newsvendor Problem Based on XGBoost Algorithm[J]. Chinese Journal of Management Science, 2024, 32(1): 260-267.

"

"

| 数据类别 | 特征 |

|---|---|

| 产品 | 产品id、重量、件数、品牌, 品牌名 |

| 商店 | 商店id、商店名, 商店类型 |

| 地理位置 | 商店id、州、 城镇 |

| 交易数据 | 周数、商店id、产品id、销量、销售渠道、销售路线、销量滞后值、销量均值滞后值(按商店、产品和品牌不同指标分类) |

| 时间 | 周数、产品上次销售时间, 产品首次销售时间 (按时间和产品分类) |

"

| 方法 | RMSE | MAE | 中位数绝对误差 | R2 |

|---|---|---|---|---|

| XGBoost点预测 | ||||

| 线性回归点预测 | 53.19 | 35.30 | 24.18 | 0.74 |

| Lasso点预测 | 52.79 | 34.77 | 24.28 | 0.75 |

| 岭回归点预测 | 53.16 | 35.27 | 24.18 | 0.75 |

"

| 方法 | cost | ?cost | SL | 参数 |

|---|---|---|---|---|

| XO- | 47814.28 | 59.82% | 0.61 | 5 |

| XO- | 0.6 | 5 | ||

| XGBoost点预测 | 51887.34 | 56.39% | 0.58 | — |

| 线性回归点预测 | 66671.92 | 43.97% | 0.49 | — |

| Lasso点预测 | 65668.30 | 44.81% | 0.52 | 0.1 |

| 岭回归点预测 | 66619.21 | 44.01% | 0.49 | 1 |

| SAA | 118988.57 | — | 0.43 | — |

"

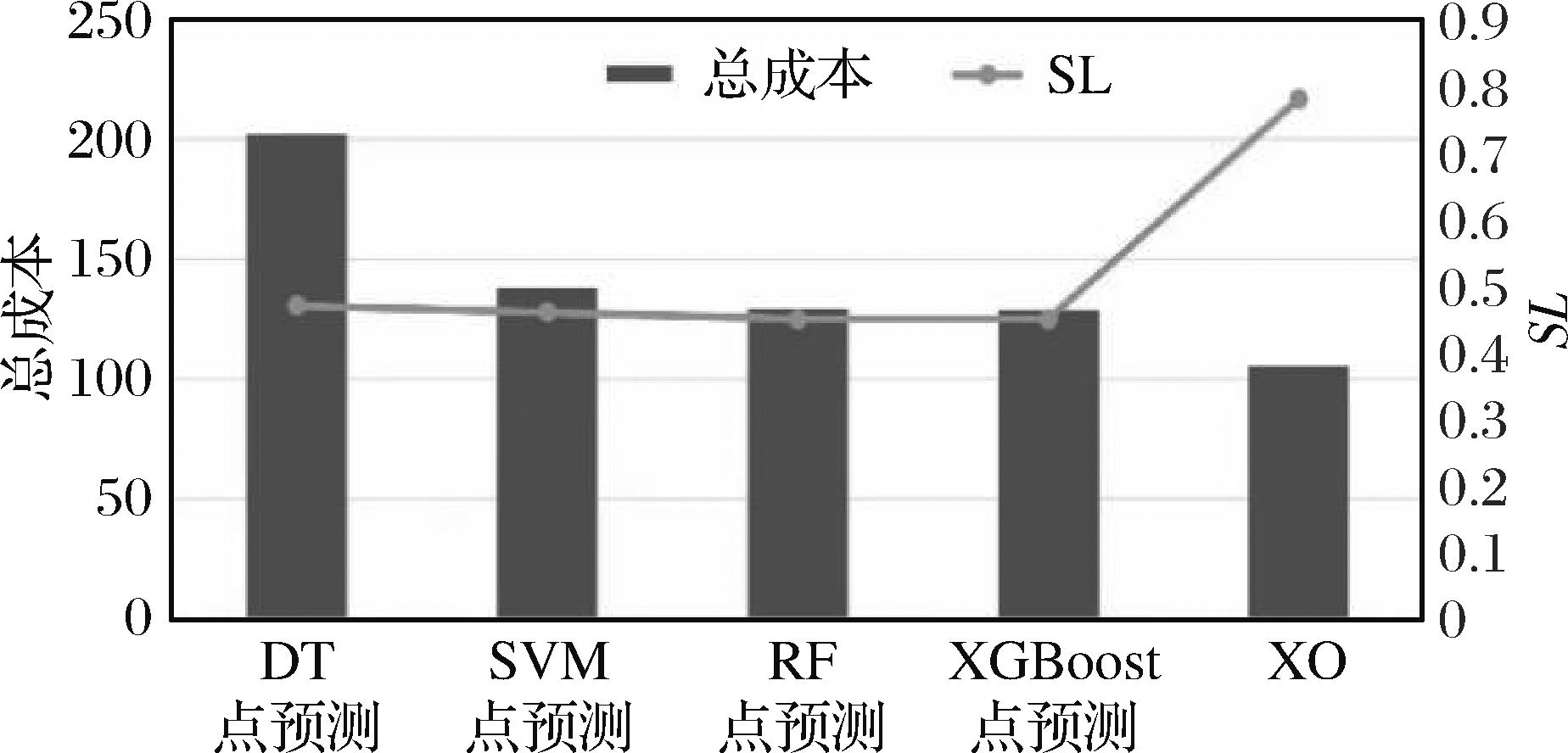

| 方法 | TSL=0.6 | TSL=0.7 | TSL=0.8 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| cost | ?cost(%) | SL | cost | ?cost(%) | SL | cost | ?cost(%) | SL | |

| XO-- | 0.59 | 47814.28 | 59.82 | 0.61 | 0.8 | ||||

| XO-- | 57486.67 | 58.59 | 0.49 | 0.6 | 43802.5 | 57.93 | 0.78 | ||

| XGBoost点预测 | 63106.33 | 54.54 | 0.51 | 51887.34 | 56.39 | 0.58 | 46942.5 | 54.91 | 0.62 |

| 线性回归点预测 | 77783.91 | 43.97 | 0.43 | 66671.92 | 43.97 | 0.49 | 58337.93 | 43.97 | 0.49 |

| Lasso点预测 | 76613.02 | 44.81 | 0.49 | 65668.30 | 44.81 | 0.52 | 57459.76 | 44.81 | 0.52 |

| 岭回归点预测 | 77722.42 | 44.01 | 0.52 | 66619.21 | 44.01 | 0.49 | 58291.81 | 44.01 | 0.49 |

| SAA | 138820.0 | — | 0.49 | 118988.57 | — | 0.43 | 104115.0 | — | 0.43 |

"

| 方法 | S= 0.2 | S= 0.4 | S= 0.6 | S= 0.8 | S= 1.0 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| cost | ?cost(%) | SL | cost | ?cost(%) | SL | cost | ?cost(%) | SL | cost | ?cost(%) | SL | cost | ?cost(%) | SL | |

| XO- | 56.13 | 0.65 | 60.23 | 0.62 | 50630.98 | 57.45 | 0.59 | 59.30 | 0.62 | 47814.28 | 59.82 | 0.61 | |||

| XO- | 54591.42 | 54.12 | 0.7 | 48054.28 | 59.61 | 0.71 | 58.41 | 0.59 | 49151.42 | 58.69 | 0.55 | 60.85 | 0.6 | ||

| XGBoost点预测 | 57887.34 | 51.35 | 0.56 | 54329.75 | 54.34 | 0.55 | 52265.71 | 56.08 | 0.56 | 52416.32 | 55.95 | 0.56 | 51887.34 | 56.39 | 0.58 |

| 线性回归点预测 | 72756.51 | 38.85 | 0.48 | 69844.55 | 41.30 | 0.47 | 66535.08 | 44.08 | 0.48 | 66538.08 | 44.08 | 0.48 | 66671.92 | 43.97 | 0.49 |

| Lasso点预测 | 71071.79 | 40.27 | 0.54 | 65607.61 | 44.86 | 0.5 | 63785.62 | 46.39 | 0.57 | 64751.26 | 45.58 | 0.5 | 65668.30 | 44.81 | 0.52 |

| 岭回归点预测 | 72252.52 | 39.28 | 0.48 | 68930.05 | 42.07 | 0.47 | 66381.74 | 44.21 | 0.49 | 66417.88 | 44.18 | 0.48 | 66619.21 | 44.01 | 0.49 |

| SAA | 118988.6 | — | 0.43 | 118989 | — | 0.43 | 118988.7 | — | 0.43 | 118988.57 | — | 0.43 | 118988.57 | — | 0.43 |

"

| 参数 | 含义 | 样本量 | ||||

|---|---|---|---|---|---|---|

| 0.2 | 0.4 | 0.6 | 0.8 | 1 | ||

| learning_rate | 每步迭代步长 | 0.01 | 0.01 | 0.13 | 0.11 | 0.1 |

| n_estimators | 控制弱学习器数目,即最大迭代次数 | 500 | 500 | 500 | 500 | 500 |

| max_depth | 树的最大深度,用来控制过拟合 | 7 | 9 | 7 | 6 | 9 |

| min_child_weight | 子集的所有观察值的最小权重和,控制过拟合 | 9 | 9 | 5 | 3 | 9 |

| subsample | 构建每棵树样本采样率,用于训练模型子样本占整个样本集合的比例 | 0.8 | 0.7 | 0.8 | 0.8 | 0.8 |

| colsample_bytree | 列采样率,即特征采样率 | 0.8 | 0.8 | 0.8 | 0.8 | 0.8 |

| gamma | 分裂节点时损失函数减小值只有大于gamma节点才分裂,值越大算法越不容易过拟合 | 0.3 | 0 | 0 | 0 | 0.3 |

| 权重 | 1 | 10 | 5 | 10 | 5 | |

| 权重 | 0 | 5 | 10 | 20 | 5 | |

| 1 | Silver E A, Pyke D F, Thomas D J. Inventory and production management in supply chains[M]. Florida: CRC Press, 2016. |

| 2 | Kleywegt A J, Shapiro A, Homem-de-Mello T. The sample average approximation method for stochastic discrete optimization[J]. SIAM Journal on Optimization, 2002, 12(2): 479-502. |

| 3 | Shapiro A. Monte Carlo sampling methods[J]. Handbooks in operations research and management science, 2003(10): 353-425. |

| 4 | Levi R, Roundy R O, Shmoys D B. Provably near-optimal sampling-based policies for stochastic inventory control models[J]. Mathematics of Operations Research, 2007, 32(4): 821-839. |

| 5 | Levi R, Perakis G, Uichanco J. The data-driven newsvendor problem: new bounds and insights[J]. Operations Research, 2015, 63(6): 1294-1306. |

| 6 | Liyanage L H, Shanthikumar J G. A practical inventory control policy using operational statistics[J]. Operations Research Letters, 2005, 33(4): 341-348. |

| 7 | See C T, Sim M. Robust approximation to multiperiod inventory management[J]. Operations research, 2010, 58(3): 583-594. |

| 8 | Bertsimas D, Kallus N. From predictive to prescriptive analytics[J]. Management Science, 2020, 66(3): 1025-1044. |

| 9 | Huber J, Müller S, Fleischmann M, et al. A data-driven newsvendor problem: from data to decision[J]. European Journal of Operational Research, 2019, 278(3): 904-915. |

| 10 | 文平, 庞庆华. 基于预期的报童问题研究[J]. 中国管理科学, 2018, 26(3): 109-116. |

| Wen P, Pang Q H. The research of newsvendor problem based on expectation[J]. Chinese Journal of Management Science, 2018, 26(3): 109-116. | |

| 11 | 文平. 损失厌恶的报童-预期理论下的报童问题新解[J]. 中国管理科学, 2005(6): 64-68. |

| Wen P. The loss averse newsboy-the solution of newsboy problem under prospect theory [J]. Chinese Journal of Management Science, 2005(6): 64-68. | |

| 12 | 曹兵兵, 樊治平, 尤天慧,等. 考虑损失规避的温度敏感型产品定价与订货联合决策[J]. 中国管理科学, 2017, 25(4): 60-69. |

| Cao B B, Fan Z P, You T H, et al. Joint pricing and ordering decisions for the temperature sensitive product considering the loss aversion[J]. Chinese Journal of Management Science, 2017, 25(4): 60-69. | |

| 13 | 刘咏梅, 彭民, 李立. 基于前景理论的订货问题[J]. 系统管理学报, 2010, 19(5): 481-490. |

| Liu Y M, Peng M, Li L. Ordering problems based on prospect theory[J]. Journal of Systems & Management, 2010, 19(5): 481-490. | |

| 14 | 周艳菊, 应仁仁, 陈晓红,等. 基于前景理论的两产品报童的订货模型[J].管理科学学报, 2013, 16(11): 17-29. |

| Zhou Y J, Ying R R, Chen X H, et al. Two-product newsboy problem based on prospect theory[J]. Journal of Management Sciences in China, 2013, 16(11): 17-29. | |

| 15 | Scarf H E, Arrow K J, Karlin S. A min-max solution of an inventory problem[M]. Santa Monica: Rand Corporation, 1957. |

| 16 | Beutel A L, Minner S. Safety stock planning under causal demand forecasting[J]. International Journal of Production Economics, 2012, 140(2): 637-645. |

| 17 | Ban G Y, Rudin C. The big data newsvendor: practical insights from machine learning[J].Operations Research, 2019, 67(1): 90-108. |

| 18 | Oroojlooyjadid A, Snyder L V, Takáč M. Applying deep learning to the newsvendor problem[J].IISE Transactions, 2020, 52(4): 444-463. |

| 19 | Chen T Q, Guestrin C. Xgboost: a scalable tree boosting system[C]//Proceedings of the 22nd acm sigkdd international conference on knowledge discovery and data mining, San Francisco, USA, August 13-17, 2016: 785-794. |

| 20 | 周志华. 机器学习[M]. 北京:清华大学出版社, 2016. |

| Zhou Z H. Machine learning[M]. Beijing:Tsinghua Press, 2016. | |

| 21 | Ferreira K J, Lee B H A, Simchi-Levi D. Analytics for an online retailer: demand forecasting and price optimization[J]. Manufacturing & Service Operations Management, 2016, 18(1): 69-88. |

| 22 | Breiman L, Friedman J H, Olshen R A, et al. Classification and regression trees[M]. New York: Routledge, 2017. |

| 23 | Hearst M A, Dumais S T, Osuna E, et al. Support vector machines[J]. IEEE Intelligent Systems and their applications, 1998, 13(4): 18-28. |

| 24 | Breiman L. Random forests[J]. Machine Learning, 2001, 45(1): 5-32. |

| 25 | Zhang Y, Yang X Y. Online ordering policies for a two-product, multi-period stationary newsvendor problem[J]. Computers & Operations Research, 2016, 74: 143-151. |

| [1] | Hongmei Guo,Menglin Qin,Xianyu Wang,Meng Wu. Does Fixed-Rate Loans Help Small and Mirco Retailers with Insufficient Operational Capitals? [J]. Chinese Journal of Management Science, 2024, 32(1): 177-186. |

| [2] | Ruo-zhen QIU,Xiao-jing CHU,Yue SUN. Dual-channel Supply Chain Decision Model Based on Robust Optimizationunder Price and Delivery-time Dependent Demand [J]. Chinese Journal of Management Science, 2023, 31(9): 114-126. |

| [3] | Yue-wu TANG,Yang SONG,Ti-jun FAN. Retailer Pricing when Facing Strategic Consumers with Different Waiting Costs [J]. Chinese Journal of Management Science, 2023, 31(9): 177-185. |

| [4] | Li-ping XIAO,Jia-lian LI,Xue-yan SHAO,Hong CHI. Medical Alliance System Optimization Based on Queuing Network under Hierarchical Diagnosis and Treatment [J]. Chinese Journal of Management Science, 2023, 31(9): 186-195. |

| [5] |

Hai-yu WANG.

Economic-statistical Optimization Design of Dynamic |

| [6] | Jiang-tao WANG,Ya CAI,Cheng-li ZHENG. An Adaptive Algorithm for Prediction of Risk and Its Application [J]. Chinese Journal of Management Science, 2023, 31(8): 1-8. |

| [7] | ZHOU Ying, YI Ping-tao, WANG Lu, DONG Qian-kun. Objective Optimization Method and Verification Analysis of Group Evaluation Data from the Perspective of Psychological Threshold Coordination [J]. Chinese Journal of Management Science, 2023, 31(7): 237-245. |

| [8] | HU Hai-qing, Pandu R Tadikamalla. Twostage Inventory Model Considering Forecast Accuracy of Online Fast Fashion Products [J]. Chinese Journal of Management Science, 2023, 31(7): 256-265. |

| [9] | ZHANG Li-li, YANG Wen-wen, LUO Guan-cong. Inverse Optimal Value Method of “Task-personnel” Matching with Time Inferring: Taking Petrochemical Equipment Emergency Repair as an Example [J]. Chinese Journal of Management Science, 2023, 31(6): 276-286. |

| [10] | XIANG Yin. Hydrogenation Infrastructure Network Optimization Considering Industrial Layout and Customer Satisfaction [J]. Chinese Journal of Management Science, 2023, 31(5): 164-175. |

| [11] | LI De-chang, YANG Hua-long, SONG Wei, ZHENG Jian-feng. Freight Revenue Robust Optimization for Container Liner Shipping Considering Vessel Sailing Speed Deviation [J]. Chinese Journal of Management Science, 2023, 31(4): 151-160. |

| [12] | CHEN Hao-ran, ZHAO Xiao-li. Research on Electric Vehicle Charging Optimization Considering Distributed Photovoltaic Power Generation [J]. Chinese Journal of Management Science, 2023, 31(4): 161-170. |

| [13] | OUYANG Lin-han, TAO Bao-ping, MA Yan. Research on Quality Prediction Based on Gaussian Process Model with Selective Ensemble Kernel [J]. Chinese Journal of Management Science, 2023, 31(3): 69-80. |

| [14] | HE Xue-ting, ZHEN Lu. Optimization of Route Rescheduling Considering Realtime Orders in Demandresponsive Transit [J]. Chinese Journal of Management Science, 2023, 31(3): 113-123. |

| [15] | SONG Jin-bo, ZHOU Yu-shan, HE Qiu-ying. The Impact of Emotional Load on Service Quality and Operational Efficiency of Online Political Inquiry Platform—Evidence from Textual Data [J]. Chinese Journal of Management Science, 2023, 31(3): 133-142. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||