主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (8): 1-13.doi: 10.16381/j.cnki.issn1003-207x.2024.1601

Yinhong Yao, Xiaoxu Wang, Wei Chen, Zhensong Chen( )

)

Received:2024-09-13

Revised:2024-10-22

Online:2025-08-25

Published:2025-09-10

Contact:

Zhensong Chen

E-mail:chenzhensong@cueb.edu.cn

CLC Number:

Yinhong Yao, Xiaoxu Wang, Wei Chen, Zhensong Chen. Extreme Risk Spillover among Global Stock Markets Based on Transformer-LSTM Quantile Regression[J]. Chinese Journal of Management Science, 2025, 33(8): 1-13.

"

"

| 股市 | 均值 | 最大值 | 最小值 | 标准差 | 偏度 | 峰度 | JB检验 | ARCH检验 | ADF检验 |

|---|---|---|---|---|---|---|---|---|---|

| 中国 | 0.049 | 13.945 | -14.898 | 3.191 | -0.202 | 2.618 | 324.379*** | 311.587*** | -17.426*** |

| 奥地利 | 0.136 | 11.424 | -29.933 | 2.545 | -1.775 | 20.324 | 19752.867*** | 83.373*** | -20.962*** |

| 澳大利亚 | 0.119 | 15.817 | -36.255 | 3.116 | -1.674 | 18.243 | 15963.294*** | 41.224*** | -35.064*** |

| 巴西 | 0.053 | 12.432 | -27.055 | 2.984 | -1.299 | 9.847 | 4811.127*** | 128.240*** | -35.855*** |

| 比利时 | 0.101 | 17.226 | -40.380 | 3.430 | -2.309 | 22.669 | 24837.609*** | 85.667*** | -7.963*** |

| 德国 | 0.080 | 8.101 | -22.522 | 2.166 | -1.812 | 13.866 | 9531.783*** | 97.814*** | -19.838*** |

| 法国 | 0.203 | 16.843 | -35.495 | 3.698 | -0.995 | 9.874 | 4705.988*** | 144.685*** | -22.514*** |

| 马来西亚 | 0.033 | 10.005 | -28.161 | 2.829 | -1.773 | 14.324 | 10103.901*** | 80.551*** | -6.035*** |

| 新加坡 | 0.115 | 14.942 | -28.841 | 3.141 | -1.189 | 10.255 | 5140.368*** | 164.950*** | -20.343*** |

| 英国 | 0.079 | 6.653 | -9.793 | 1.685 | -0.398 | 3.531 | 606.560*** | 103.884*** | -30.914*** |

| 韩国 | 0.070 | 15.321 | -21.326 | 2.419 | -0.544 | 9.862 | 4564.891*** | 259.028*** | -32.323*** |

| 荷兰 | 0.037 | 12.584 | -25.781 | 2.439 | -1.589 | 16.287 | 12777.293*** | 131.888*** | -12.173*** |

| 加拿大 | 0.129 | 17.032 | -22.929 | 2.989 | -0.762 | 6.781 | 2239.672*** | 343.442*** | -8.899*** |

| 美国 | 0.051 | 12.475 | -31.778 | 3.004 | -1.657 | 14.393 | 10121.758*** | 92.526*** | -20.291*** |

| 墨西哥 | 0.097 | 12.817 | -29.091 | 2.344 | -2.487 | 27.266 | 35650.515*** | 136.850*** | -35.587*** |

| 日本 | 0.202 | 18.579 | -25.136 | 2.709 | -0.747 | 11.102 | 5819.659*** | 276.199*** | -19.777*** |

| 瑞士 | 0.056 | 13.165 | -24.263 | 2.456 | -1.499 | 13.711 | 9139.129*** | 176.794*** | -13.808*** |

| 意大利 | 0.007 | 10.472 | -29.046 | 3.274 | -1.575 | 10.610 | 5683.438*** | 79.679*** | -6.165*** |

| 印度 | 0.276 | 13.171 | -21.876 | 2.878 | -0.710 | 5.437 | 1463.906*** | 285.278*** | -21.370*** |

"

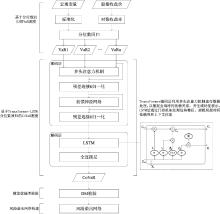

| 参数 | 值 | 解释 |

|---|---|---|

| Transformer注意力头大小 | 8 | 决定了每个注意力头在进行自注意力计算时的特征压缩程度 |

| Transformer注意力头数量 | 6 | 在多头注意力机制中并行的注意力头数 |

| Transformer前馈网络维度 | 8 | 在Transformer块中前馈网络的内部维度 |

| Transformer丢弃率 | 0.01 | 一种正则化技术,用于防止神经网络过拟合 |

| Transformer激活函数 | Relu | 引入非线性因素 |

| LSTM激活函数 | Tanh | — |

| 优化器 | Adam | 用于更新参数和优化目标函数 |

| 学习率 | 0.001 | 决定了神经网络能否收敛到全局最小值 |

| 损失函数 | 分位数损失函数 | — |

| Epochs | 60 | 训练所需的次数 |

| Batch_size | 20 | 定义在更新内部模型参数之前需要处理的样本数量 |

"

"

"

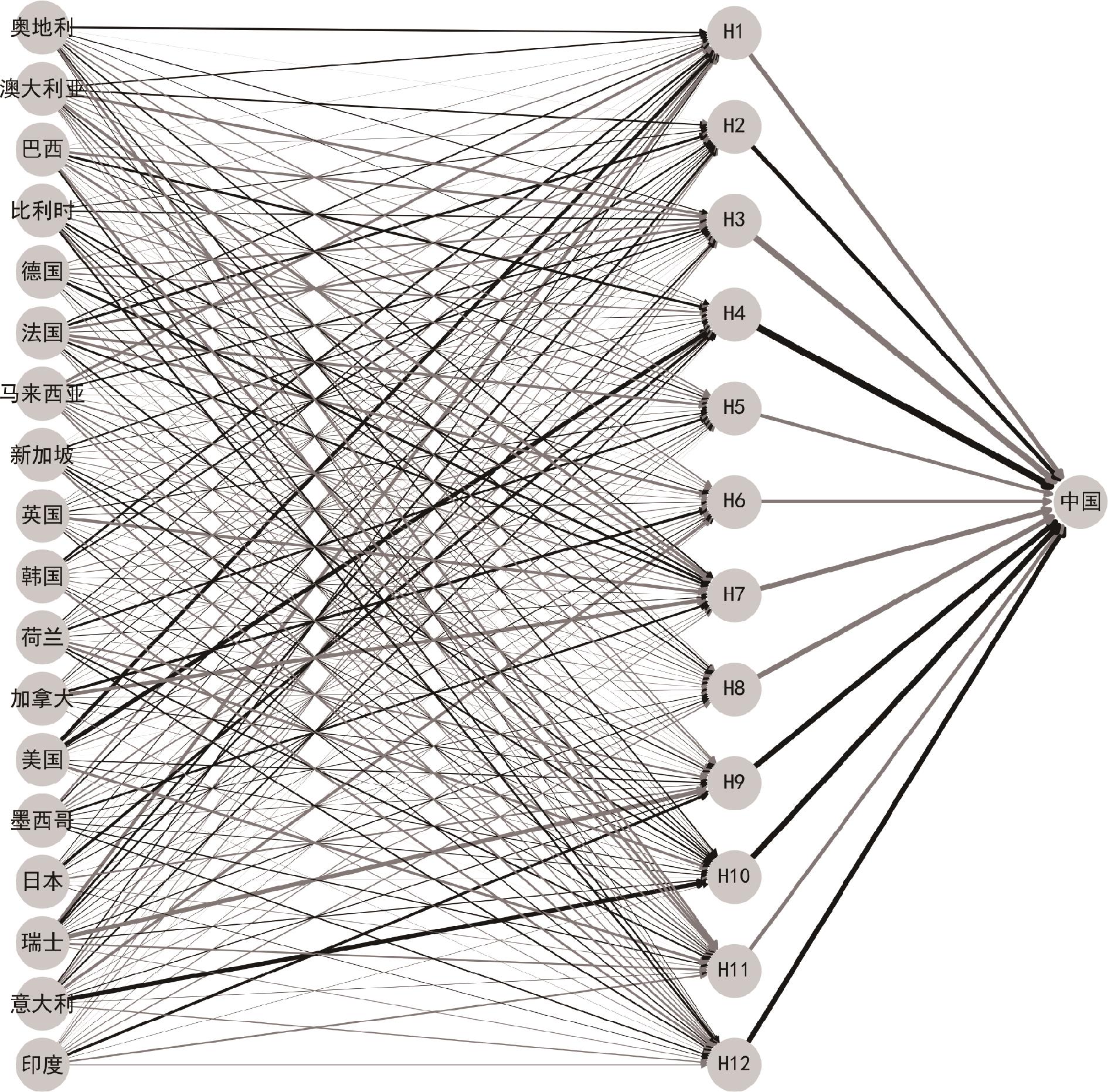

| 国家 | 模型 | ||

|---|---|---|---|

| MLP | LSTM | Transformer | |

| 中国 | 2.86*** | 5.16*** | 3.72*** |

| 奥地利 | 4.47*** | 3.14*** | 5.29*** |

| 澳大利亚 | 1.76* | 1.46* | 2.89*** |

| 巴西 | 5.46*** | 3.36*** | 5.90*** |

| 比利时 | 5.18*** | 3.64*** | 5.83*** |

| 德国 | 2.57*** | 2.09** | 3.65*** |

| 法国 | 1.89* | 3.94*** | 1.42* |

| 马来西亚 | 3.90*** | 3.38*** | 4.57*** |

| 新加坡 | 4.66*** | 2.66*** | 4.54*** |

| 英国 | 2.83*** | 4.52*** | 3.04*** |

| 韩国 | 2.13*** | 2.19** | 2.15** |

| 荷兰 | 5.18*** | 3.04*** | 5.80*** |

| 加拿大 | 2.76*** | 3.91*** | 2.69*** |

| 美国 | 4.98*** | 2.83*** | 5.72*** |

| 墨西哥 | 3.87*** | 2.25** | 4.50*** |

| 日本 | 1.78** | 4.20*** | 1.91* |

| 瑞士 | 4.39*** | 1.97** | 4.36*** |

| 意大利 | 3.58*** | 3.56*** | 3.48*** |

| 印度 | 2.41** | 2.63*** | 2.14** |

"

"

"

"

"

| 国家 | 模型 | ||

|---|---|---|---|

| MLP | LSTM | Transformer | |

| 中国 | 2.44** | 2.99*** | 2.45** |

| 奥地利 | 3.76*** | 2.21** | 4.35*** |

| 澳大利亚 | 2.30** | 2.14** | 2.18*** |

| 巴西 | 4.70*** | 3.84*** | 5.05*** |

| 比利时 | 4.84*** | 4.34*** | 4.71*** |

| 德国 | 2.42** | 1.66* | 3.92*** |

| 法国 | 2.53** | 2.30** | 2.17** |

| 马来西亚 | 4.45*** | 2.24** | 4.33*** |

| 新加坡 | 5.21*** | 3.24*** | 5.24*** |

| 英国 | 2.83** | 2.86*** | 2.53** |

| 韩国 | 2.78** | 3.54*** | 3.95*** |

| 荷兰 | 5.43*** | 2.42** | 4.20*** |

| 加拿大 | 2.02** | 3.11*** | 2.21** |

| 美国 | 5.75*** | 3.87*** | 5.60*** |

| 墨西哥 | 3.46*** | 2.31** | 3.39*** |

| 日本 | 1.84* | 2.63*** | 3.26** |

| 瑞士 | 5.08*** | 2.54** | 4.94*** |

| 意大利 | 3.43*** | 2.38** | 4.25*** |

| 印度 | 2.09** | 2.55** | 3.75*** |

| [1] | 王纲金, 马欣宇, 谢赤. 基于尾部风险溢出网络的全球外汇市场关联性研究[J]. 中国管理科学, 2025, 33(3): 13-23. |

| Wang G J, Ma X Y, Xie C. Measuring interconnectedness of global foreign exchange markets using tail risk spillover network[J]. Chinese Journal of Management Science, 2025, 33(3): 13-23. | |

| [2] | Cavallaro E, Villani I. Beyond financial deepening: Rethinking the finance-growth relationship in an uneven world[J]. Economic Modelling, 2022, 116: 106009. |

| [3] | 谭小芬, 虞梦微, 王欣康. 跨境资本流动的新特征、新风险及其政策建议[J]. 国际金融研究, 2023(4): 17-28. |

| Tan X F, Yu M W, Wang X K. New features, new risks and policy recommendations of cross-border capital flows[J]. Studies of International Finance, 2023(4): 17-28. | |

| [4] | 刘志峰, 张子汸, 戴鹏飞, 等. 碳市场与股票市场间的崩盘风险溢出效应研究: 新冠疫情、投资者情绪与经济政策不确定性[J]. 系统工程理论与实践, 2023,43(3): 740-754. |

| Liu Z F, Zhang Z P, Dai P F, et al. A study on the spillover effect of crash risk between carbon and stock markets: COVID-19, investor sentiment and economic policy uncertainty[J]. Systems Engineering-Theory & Practice, 2023, 43(3): 740-754. | |

| [5] | 李兆东, 曾志坚, 谢赤, 等. 多周期视角下全球股市行业间联动性与突发事件冲击影响——一个基于复杂网络的实证研究[J]. 系统工程理论与实践, 2023, 43(11): 3197-3213. |

| Li Z D, Zeng Z J, Xie C, et al. Co-movement among industries in global stock market and shocks of emergencies from a multi-periods perspective: An empirical research based on complex networks[J].Systems Engineering-Theory & Practice, 2023,43(11): 3197-3213. | |

| [6] | Ren Y, Zhao W, You W, et al. Multiscale features of extreme risk spillover networks among global stock markets[J]. The North American Journal of Economics and Finance, 2022, 62: 101754. |

| [7] | Pineda J, Cortés L M, Perote J. Financial contagion drivers during recent global crises[J]. Economic Modelling, 2022, 117: 106067. |

| [8] | Ouyang Z, Zhou X, Lai Y. Global stock markets risk contagion: Evidence from multilayer connectedness networks in the frequency domain[J]. The North American Journal of Economics and Finance, 2023, 68: 101973. |

| [9] | 朱晓谦, 李靖宇, 李建平, 等. 基于危机条件概率的系统性风险度量研究[J]. 中国管理科学, 2018, 26(6): 1-7. |

| Zhu X Q, Li J Y, Li J P, et al. An indicator of conditional probability of crisis for systemic risk measurement[J]. Chinese Journal of Management Science, 2018, 26(6): 1-7. | |

| [10] | Morgan J. RiskmetricsTM: Technical document[R]. Working Paper, Morgan Guaranty Trust Company, 1996. |

| [11] | 王江涛, 蔡雅, 郑承利. 一类自适应的风险预测算法及其应用[J]. 中国管理科学, 2023, 31(8): 1-8. |

| Wang J T, Cai Y, Zheng C L. An adaptive algorithm for prediction of risk and its application[J]. Chinese Journal of Management Science, 2023, 31(8): 1-8. | |

| [12] | Adrian T, Brunnermeier M K. CoVaR[J]. American Economic Review, 2016, 106(7): 1705-1741. |

| [13] | 叶五一, 李艾琳, 焦守坤. 基于动态模型平均的大豆期货市场风险溢出研究[J]. 中国管理科学, 2023, 31(12): 1-10. |

| Ye W Y, Li A L, Jiao S K. Risk spillover of soybean futures market based on dynamic model averaging[J]. Chinese Journal of Management Science, 2023, 31(12): 1-10. | |

| [14] | 姚海祥, 刘秋瑜, 杨晓光. 增强还是减弱:新型金融与传统金融行业之间系统性风险溢出[J]. 中国管理科学,2025,33(3):1-12. |

| Yao H X, Liu Q Y, Yang X G. Strengthening or Weakening: Systemic Risk Spillovers between Diversified Financial in Dustries and Traditional Financial Industries [J]. Chinese Journal of Management Science, 2025,33(3):1-12. | |

| [15] | Liu B Y, Fan Y, Ji Q, et al. High-dimensional CoVaR network connectedness for measuring conditional financial contagion and risk spillovers from oil markets to the G20 stock system[J]. Energy Economics, 2022, 105: 105749. |

| [16] | Wu F, Zhang Z, Zhang D, et al. Identifying systemically important financial institutions in China: New evidence from a dynamic copula-CoVaR approach[J]. Annals of Operations Research,2023,330(1): 119-153. |

| [17] | 吴金宴, 王鹏. 哪些因素影响了股市风险传染——来自行业数据的证据[J]. 中国管理科学, 2022, 30(8): 57-68. |

| Wu J Y, Wang P. Factors affecting the risk contagion of the stock market: An evidence from industry-level data[J]. Chinese Journal of Management Science, 2022, 30(8): 57-68. | |

| [18] | Girardi G, Tolga Ergün A. Systemic risk measurement: Multivariate GARCH estimation of CoVaR[J]. Journal of Banking & Finance, 2013, 37(8): 3169-3180. |

| [19] | Chen Q, Huang Z, Liang F. Measuring systemic risk with high-frequency data:A realized GARCH approach[J]. Finance Research Letters, 2023, 54: 103753. |

| [20] | Tian M, Alshater M M, Yoon S M. Dynamic risk spillovers from oil to stock markets: Fresh evidence from GARCH copula quantile regression-based CoVaR model[J]. Energy Economics, 2022, 115: 106341. |

| [21] | 侯县平, 傅春燕, 林子枭, 等. 极端风险溢出效应的定量测度及非对称性——来自中国股市与债市的经验证据[J]. 管理评论, 2020, 32(9): 55-67. |

| Hou X P, Fu C Y, Lin Z X, et al. Quantitative measurements and asymmetries of extreme risk spillover effects: Evidence from China’s stock and bond markets[J]. Management Review, 2020, 32(9): 55-67. | |

| [22] | 李竹薇, 刘森楠, 李小凤, 等. 互联网金融与传统金融之间的广义动态风险溢出——基于Copula-ARMA-GARCH-CoVaR的实证研究[J]. 系统工程, 2021, 39(4): 126-138. |

| Li Z W, Liu S N, Li X F, et al. Generalized dynamic risk spillover between Internet finance and traditional finance: An empirical study based on copula-ARMA-GARCH-CoVaR[J]. Systems Engineering, 2021, 39(4): 126-138. | |

| [23] | 任英华, 赵婉茹, 罗良清. 基于Copula函数的股票市场风险溢出网络特征研究[J]. 统计与信息论坛, 2020, 35(8): 53-63. |

| Ren Y H, Zhao W R, Luo L Q. Research on risk spillover networks among major global stock markets based on copula function[J]. Statistics & Information Forum, 2020, 35(8): 53-63. | |

| [24] | Jiang C, Li Y, Xu Q, et al. Measuring risk spillovers from multiple developed stock markets to China: A vine-copula-GARCH-MIDAS model[J]. International Review of Economics & Finance, 2021, 75: 386-398. |

| [25] | 胡毅, 李瑞, 张希, 等.基于分位数回归的系统性风险和经济增长关系研究[J].管理评论,2019, 31(12): 3-14. |

| Hu Y, Li R, Zhang X, et al. A study of the relationship between systemic risk and economic growth based on quantile regression[J]. Management Review, 2019, 31(12): 3-14. | |

| [26] | Ziadat S A, Mensi W, Al-Kharusi S, et al. Are clean energy markets hedges for stock markets A tail quantile connectedness regression[J]. Energy Economics, 2024, 136: 107757. |

| [27] | 林娟, 赵海龙. 沪深股市和香港股市的风险溢出效应研究——基于时变ΔCoVaR模型的分析[J]. 系统工程理论与实践, 2020, 40(6): 1533-1544. |

| Lin J, Zhao H L. Research on the risk spillovers between Shanghai, Shenzhen and Hong Kong stock markets: Based on the time varying ΔCoVaR model[J]. Systems Engineering-Theory & Practice, 2020, 40(6): 1533-1544. | |

| [28] | Yang L, Cui X, Yang L, et al. Risk spillover from international financial markets and China’s macro-economy: A MIDAS-CoVaR-QR model[J]. International Review of Economics & Finance, 2023, 84: 55-69. |

| [29] | 张兴敏, 傅强, 张帅, 等. 金融系统的网络结构及尾部风险度量——基于动态半参数分位数回归模型[J]. 管理评论, 2021, 33(4): 59-70. |

| Zhang X M, Fu Q, Zhang S, et al. Financial system network contagion structure and tail risk measurement based on dynamic semiparametric quantile regression model[J]. Management Review,2021,33(4): 59-70. | |

| [30] | Taylor J W. A quantile regression neural network approach to estimating the conditional density of multiperiod returns[J]. Journal of Forecasting, 2000, 19(4): 299-311. |

| [31] | 许启发, 徐金菊, 蒋翠侠, 等. 基于神经网络分位数回归的VaR金融风险测度[J]. 合肥工业大学学报(自然科学版), 2014, 37(12): 1518-1522. |

| Xu Q F, Xu J J, Jiang C X, et al. Financial risk measure of VaR based on quantile regression neural network[J]. Journal of Hefei University of Technology (Natural Science), 2014, 37(12): 1518-1522. | |

| [32] | Naeem M A, Karim S, Tiwari A K. Quantifying systemic risk in US industries using neural network quantile regression[J]. Research in International Business and Finance, 2022, 61: 101648. |

| [33] | Naeem M A, Karim S, Yarovaya L, et al. Systemic risk contagion of green and Islamic markets with conventional markets[J]. Annals of Operations Research, 2025,347: 265-287. |

| [34] | Keilbar G, Wang W. Modelling systemic risk using neural network quantile regression[J]. Empirical Economics, 2022, 62(1): 93-118. |

| [35] | Aprea I L, Scognamiglio S, Zanetti P. Systemic risk measurement: A Quantile Long Short-Term Memory network approach[J]. Applied Soft Computing, 2024, 152: 111224. |

| [36] | Christoffersen P. Value-at-risk models[M]//Handbook of Financial Time Series. Berlin, Heidelberg: Springer Berlin Heidelberg, 2009: 753-766. |

| [37] | 张伟平, 庄新田, 王健. 中国股市跨行业系统性风险空间溢出关联及风险预测分析——基于尾部风险网络模型[J]. 中国管理科学, 2021, 29(12): 15-28. |

| Zhang W P, Zhuang X T, Wang J. Systematic risk spatial spillover correlation and risk prediction analysis of cross-industry in China’ stock market: Based on the tail risk network model[J]. Chinese Journal of Management Science, 2021, 29(12): 15-28. | |

| [38] | Engle R F, Manganelli S. CAViaR: Conditional autoregressive value at risk by regression quantiles[J]. Journal of Business & Economic Statistics, 2004, 22(4): 367-381. |

| [39] | Koenker R, Bassett G J. Regression quantiles[J]. Econometrica: Journal of the Econometric Society, 1978,46(1): 33-50. |

| [40] | Vaswani A, Shazeer N, Parmar N, et al. Attention is all you need[C]//Proceedings of the 31st International Conference on Neural Information Processing Systems (NIPS'17), NY, USA, December 4-9 , Curran Associates Inc., Red Hook, 2017: 6000-6010. |

| [41] | Hochreiter S, Schmidhuber J. Long short-term memory[J]. Neural Computation, 1997, 9(8): 1735-1780. |

| [42] | Diebold F X, Mariano R S. Comparing predictive accuracy[J]. Journal of Business & Economic Statistics, 1995, 13(3): 253-263. |

| [43] | Diebold F X, Yilmaz K. Measuring financial asset return and volatility spillovers, with application to global equity markets[J]. The Economic Journal, 2009, 119(534): 158-171. |

| [44] | 荆中博, 胡佳楠, 方意. 宏观金融波动与中国银行业系统性风险: 金融周期视角[J]. 系统工程理论与实践, 2023, 43(7): 1940-1959. |

| Jing Z B, Hu J N, Fang Y. Macro financial fluctuation and China’s banking systemic risk: A financial cycle perspective[J]. Systems Engineering-Theory & Practice, 2023, 43(7): 1940-1959. | |

| [45] | 赵万里, 范英, 姬强, 等. “一带一路” 国家金融风险溢出研究——基于TENET网络方法[J]. 系统工程理论与实践, 2022, 42(1): 24-36. |

| Zhao W L, Fan Y, Ji Q, et al. Research on financial risk spillover of the countries along the Belt and Road: Based on TENET method[J]. Systems Engineering-Theory & Practice, 2022, 42(1): 24-36. | |

| [46] | Wang C, Chen Y, Zhang S, et al. Stock market index prediction using deep Transformer model[J]. Expert Systems with Applications, 2022, 208: 118128. |

| [47] | 张雪彤, 张卫国, 王超. 发达市场与新兴市场的尾部风险——溢出、传染与传染动因检验[J]. 中国管理科学, 2024, 32(4): 14-25. |

| Zhang X T, Zhang W G, Wang C. Tail risks in developed and emerging markets: Test of spillover, contagion and contagion determinants[J]. Chinese Journal of Management Science, 2024, 32(4): 14-25. | |

| [48] | 钟婉玲, 李海奇. 股市互联与尾部风险溢出效应研究[J]. 计量经济学报, 2024, 4(2): 467-486. |

| Zhong W L, Li H Q. Stock market interconnection and tail risk spillover effects[J]. China Journal of Econometrics, 2024, 4(2): 467-486. | |

| [49] | 杨子晖, 王姝黛. 突发公共卫生事件下的全球股市系统性金融风险传染——来自新冠疫情的证据[J]. 经济研究, 2021, 56(8): 22-38. |

| Yang Z H, Wang S D. Systemic financial risk contagion of global stock market under public health emergency: Empirical evidence from COVID19 epidemic[J].Economic Research Journal, 2021,56(8): 22-38. |

| [1] | Ke Yang, Xin Liu, Fengping Tian. Cross-Market Contagion of Stock Market's Extreme Risks between China and Other Major Emerging Market Countries [J]. Chinese Journal of Management Science, 2025, 33(7): 44-53. |

| [2] | Hongfeng Peng, Shiqun Ma, Xuetong Wang. Research on Cross-country Dynamic Spillover Effect of Economic Policy Uncertainty: From the Perspective of Network Multi-layer Structure [J]. Chinese Journal of Management Science, 2025, 33(7): 79-91. |

| [3] | Liukai Wang, Xiaobo Zhang, Weiqing Wang, Cheng Liu. MIDAS-SVQR: A Novel Model for Measuring VaR of Supply Chain Finance Pledge [J]. Chinese Journal of Management Science, 2025, 33(3): 80-92. |

| [4] | Yuting Yan,Wenjie Bi. A Data-driven Single-Period Newsvendor Problem Based on XGBoost Algorithm [J]. Chinese Journal of Management Science, 2024, 32(1): 260-267. |

| [5] | Jiang-tao WANG,Ya CAI,Cheng-li ZHENG. An Adaptive Algorithm for Prediction of Risk and Its Application [J]. Chinese Journal of Management Science, 2023, 31(8): 1-8. |

| [6] | Wu-yi YE,Ai-lin LI,Shou-kun JIAO. Risk Spillover of Soybean Futures Market Based on Dynamic Model Averaging [J]. Chinese Journal of Management Science, 2023, 31(12): 1-10. |

| [7] | QU Hui, SHEN Wei. Investor Attention and Covariance Forecasting in China’s Stock Markets——A Study Based on the MHAR Type Models [J]. Chinese Journal of Management Science, 2022, 30(7): 9-19. |

| [8] | ZHOU Zhong-bao, DENG Li, XIAO He-lu, WU Shi-jian, LIU Wen-bin. The Impact of Foreign Direct Investment on China’s High-quality Economic Development——Index DEA and Panel Partition Regression Analysis [J]. Chinese Journal of Management Science, 2022, 30(5): 118-130. |

| [9] | OUYANG Zi-sheng, YANG Xi-te, HUANG Ying. Research on Systemic Risk Contagion Effect of Chinese Financial Institutions Considering Network Public Opinion Index [J]. Chinese Journal of Management Science, 2022, 30(4): 1-12. |

| [10] | ZHAO Wei-hua, WANG Ling, CHENG Zhe, ZHANG Ri-quan. Variable Selection of Proportional Data Based on Tobit Quantile Regression Model [J]. Chinese Journal of Management Science, 2022, 30(4): 63-73. |

| [11] | LIU Zhi-dong, ZHANG Pei-yuan, JING Zhong-bo. Research on the Systemic Risk of China’s Banking Industry under the Impact of Cross-industry Risk Spillover [J]. Chinese Journal of Management Science, 2022, 30(12): 1-12. |

| [12] | WANG Xiao-yan, YUAN Teng, DUAN Xiang-bin. Loan Default Forecasting Based on Zero-inflated Quantile Two-part Model [J]. Chinese Journal of Management Science, 2022, 30(10): 1-13. |

| [13] | XU Qi-fa, LIU Shu-ting, JIANG Cui-xia. Portfolio Selection with Conditional Skewness Estimated via MIDAS Quantile Regressions [J]. Chinese Journal of Management Science, 2021, 29(3): 24-36. |

| [14] | Yuan Hui-ling, XU Lu, Zhou Yong. Leverage Effect Combining Trading Information with Stochastic Microstructure Noise [J]. Chinese Journal of Management Science, 2020, 28(9): 12-22. |

| [15] | QU Hui, ZHANG Yi. The Study of High-dimensional Volatility Estimators and Forecasting Models based on Volatility Timing Performance [J]. Chinese Journal of Management Science, 2020, 28(5): 62-70. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||