主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2024, Vol. 32 ›› Issue (12): 173-182.doi: 10.16381/j.cnki.issn1003-207x.2022.1546

Previous Articles Next Articles

Hong Shen1( ), Chenyao Zhang1,2, Xiaoxing Liu2

), Chenyao Zhang1,2, Xiaoxing Liu2

Received:2022-07-15

Revised:2022-12-29

Online:2024-12-25

Published:2025-01-02

Contact:

Hong Shen

E-mail:shenhong@yzu.edu.cn

CLC Number:

Hong Shen, Chenyao Zhang, Xiaoxing Liu. Analysis of Risk Spillover Characteristics and Mechanism among Industries: Evidence from Multilayer Network[J]. Chinese Journal of Management Science, 2024, 32(12): 173-182.

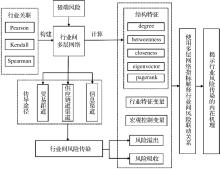

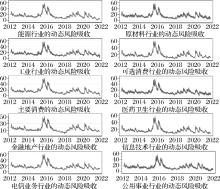

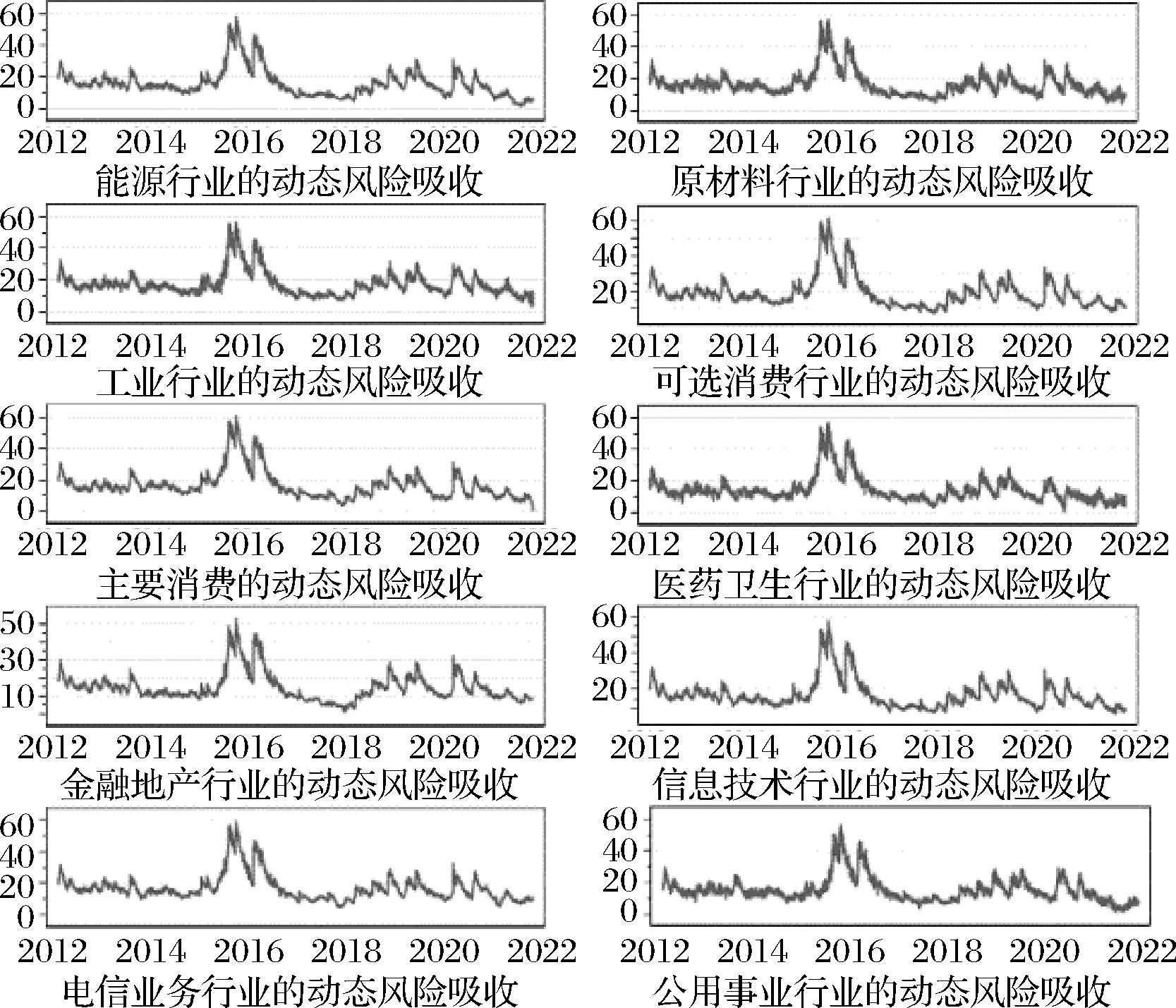

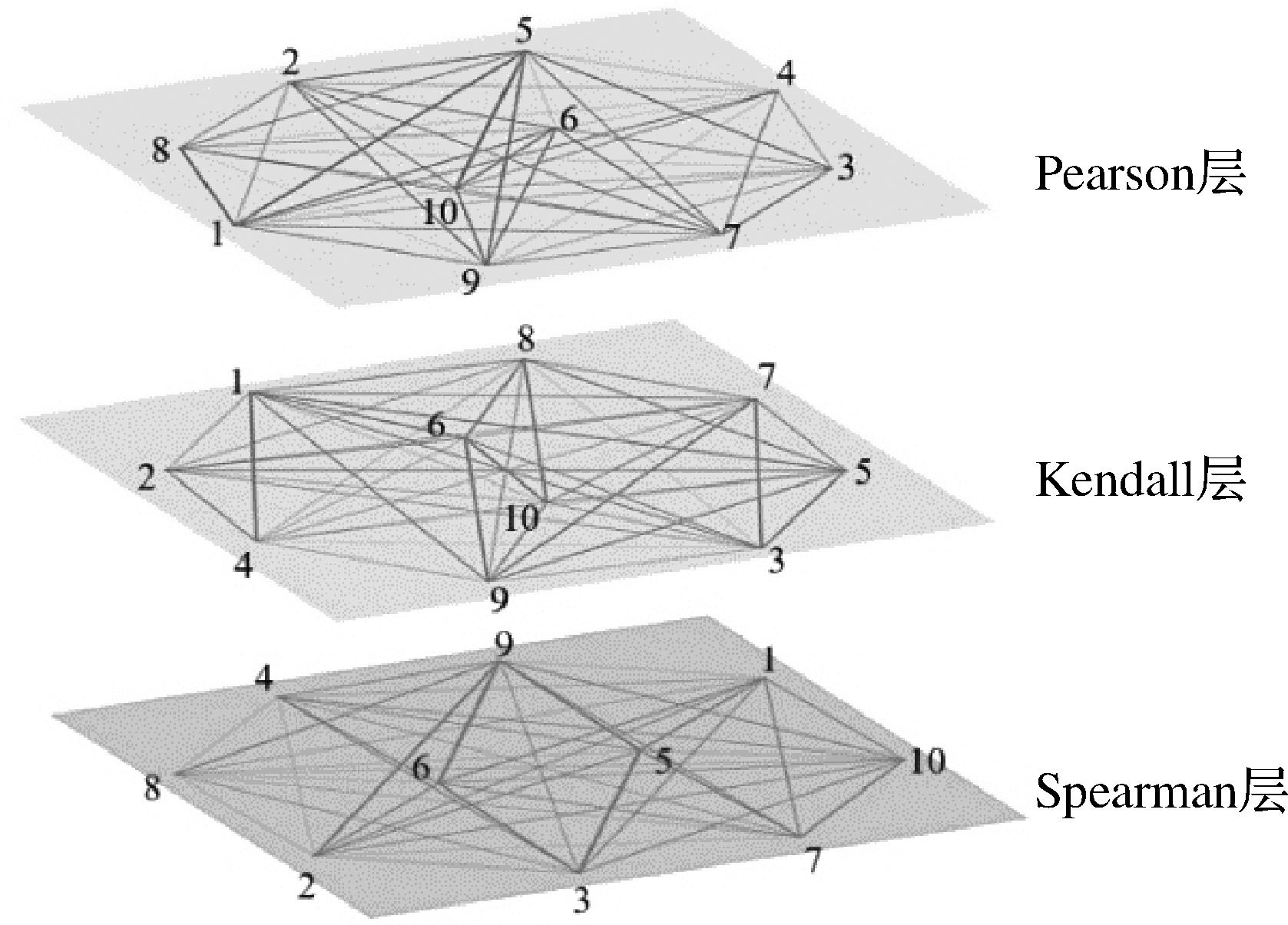

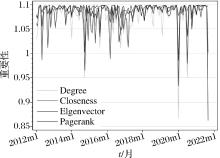

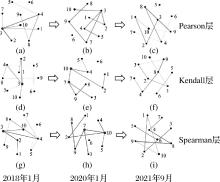

"

"

"

"

"

"

"

"

| 方法 | AIC | BIC | HQ | LL | R2 | Adj R^2 |

|---|---|---|---|---|---|---|

| Step | 2555 | 2781 | 2644 | -1220 | 0.526 | 0.446 |

| U-MIDAS | 2584 | 2698 | 2629 | -1263 | 0.412 | 0.366 |

| Almon | 2582 | 2752 | 2650 | -1248 | 0.454 | 0.387 |

| Beta | 2601 | 2771 | 2669 | -1257 | 0.435 | 0.364 |

"

| K | RMSE | K | RMSE | K | RMSE | K | RMSE |

|---|---|---|---|---|---|---|---|

| 1 | 172.9044 | 4 | 88.8952 | 7 | 177.1481 | 10 | 186.7621 |

| 2 | 200.0264 | 5 | 72.5107 | 8 | 380.3202 | 11 | 187.6261 |

| 3 | 118.0944 | 6 | 192.8008 | 9 | 664.6316 | 12 | 110.3181 |

"

| 模型 | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| DEG_L1 | 27.139** (11.026) | 12.901 (17.385) | ||||

| BET_L1 | -2.335 (2.247) | -3.721* (2.149) | ||||

| CLO_L1 | 26.839** (12.310) | 3.289 (18.404) | ||||

| EIG_L1 | 17.684* (9.104) | 4.030 (10.644) | ||||

| PAG_L1 | 81.299** (38.565) | 62.310 (41.913) | ||||

| 控制变量 | Yes | Yes | Yes | Yes | Yes | Yes |

| R-squared | 0.4444 | 0.4272 | 0.4334 | 0.4568 | 0.4660 | 0.5120 |

| Adj R-squared | 0.3996 | 0.3809 | 0.3876 | 0.4129 | 0.4228 | 0.4415 |

"

| 模型 | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| DEG_L1 | 28.121** (11.043) | 16.776 (17.397) | ||||

| BET_L1 | -4.614** (2.232) | -5.793*** (2.151) | ||||

| CLO_L1 | 27.785** (12.313) | 3.406 (18.416) | ||||

| EIG_L1 | 13.465 (9.171) | -0.453 (10.651) | ||||

| PAG_L1 | 76.188** (38.727) | 65.495 (41.941) | ||||

| 控制变量 | Yes | Yes | Yes | Yes | Yes | Yes |

| R-squared | 0.3789 | 0.3697 | 0.3680 | 0.3856 | 0.3997 | 0.4553 |

| Adj R-squared | 0.3287 | 0.3188 | 0.3170 | 0.3360 | 0.3512 | 0.3766 |

| 1 | Adrian T, Brunnermeier K. Covar[J]. American Economic Review, 2016(7):1705-1741. |

| 2 | Acharya V V, Pedersen L H, Philippon T, et al. Measuring systemic risk[J]. The Review of Financial Studies, 2017,30(1):2-47. |

| 3 | Dan G, Li Y, Lourie B, et al. Key performance indicators as supplements to earnings: Incremental informativeness, demand factors, measurement issues, and properties of their forecasts[J]. Review of Accounting Studies, 2019,24(1):1147-1183. |

| 4 | Cheikh N B, Zaied Y B. Revisiting the pass-through of exchange rate in the transition economies: New evidence from new EU member states[J]. Journal of International Money and Finance, 2020,100:102093. |

| 5 | 许启发, 王侠英, 蒋翠侠, 等. 基于藤Copula-CAVia方法的股市风险溢出效应研究[J].系统工程理论与实践,2018,38(11):2738-2749. |

| Xu Q F, Wang X Y, Jiang C X, et al. Investigating risk spillover effects among stock markets: A vine copula-CAViaR approach[J]. Systems Engineering - Theory & Practice, 2018,38(11):2738-2749. | |

| 6 | 杨子晖, 陈雨恬, 陈里璇. 极端金融风险的有效测度与非线性传染[J]. 经济研究, 2019,54(5):63-80. |

| Yang Z H, Chen Y T, Chen L X. Effective measurement and nonlinear contagion of extreme financial risk[J]. Economic Research Journal, 2019,54(5):63-80. | |

| 7 | 刘晓星, 张旭, 李守伟. 中国宏观经济韧性测度——基于系统性风险的视角[J]. 中国社会科学, 2021(1):12-32. |

| Liu X X, Zhang X, Li S W.Measurement of China’s macroeconomic resilience: A systemic risk perspective[J].Social Sciences in China, 2021(1):12-32. | |

| 8 | Martinez J S, AlexandrovaK B, BravoB B, et al. An empirical study of the Mexican banking system's network and its implications for systemic risk[J]. Journal of Economic Dynamics & Control, 2014,40(3):242-265. |

| 9 | Musmeci N, Nicosia V, Aste T, et al. The multiplex dependency structure of financial markets[J].Lse Research Online Documents on Economics, 2016,2017(2):1-13. |

| 10 | Baruník J, Koenda E, Vácha L. Asymmetric volatility connectedness on the forex market[J]. Journal of International Money and Finance, 2017,77:39-56. |

| 11 | Gross C, Siklos P. Analyzing credit risk transmission to the nonfinancial sector in Europe: A network approach[J]. Journal of Applied Econometrics, 2020,35(1):61-81. |

| 12 | 李守伟, 文世航, 王磊, 等. 多层网络视角下金融机构关联性的演化特征研究[J]. 中国管理科学, 2020,12(28):35-43. |

| Li S W, Wen S H, Wang L, et al. Evolution characteristics of financial institutions’ interrelationships from the perspective of multilayer network[J]. Chinese Journal of Management Science, 2020,12(28):35-43. | |

| 13 | 赵万里, 范英, 姬强, 等.“一带一路”国家金融风险溢出研究——基于TENET网络方法[J].系统工程理论与实践,2022,42(1):24-36. |

| Zhao W L, Fan Y, Ji Q, et al.Research on financial risk spillover of the countries along the Belt and Road:Based on TENETmethod[J].Systems Engineering - Theory & Practice,2022,42(1): 24-36. | |

| 14 | Ahern K R, Harford J. The importance of industry links in merger waves[J]. The Journal of Finance, 2014,69(2):527-576. |

| 15 | Acharya V V, Pedersen L H, Philippon T, et al. Measuring systemic risk[J]. The Review of Financial Studies, 2017,30(1):2-47. |

| 16 | Nguyen L, Mateut S, Chevapatrakul T. Business-linkage volatility spillovers between US industries[J]. Journal of Banking &Finance, 2020,111(2):1-26. |

| 17 | 赵飞, 陈彩虹. 技术关联、商业信用与风险跨行业传染[J].现代财经(天津财经大学学报), 2022,42(5): 15-35. |

| Zhao F, Chen C H. Technology association,trade credit and risk contagion cross industry[J]. Modern Finance and Economics (Journal of Tianjin University of Finance and Economics), 2022,42(5):15-35. | |

| 18 | Ghysels E, Valkanov R. The MIDAS touch: Mixed data sampling regression models[J]. Cirano Working Papers, 2004,5(1):512-517. |

| 19 | Owyang M T, Armesto M T, Engemann K M. Forecasting with mixed frequencies[J]. Federal Reserve Bank of St. Louis Review, 2010,92(6):521-536. |

| 20 | Andreou E, Ghysels E, Kourtellos A. Should macroeconomic forecasters use daily financial data and how?[J]. Social Science Electronic Publishing, 2013,31(2):240-251. |

| 21 | 尚玉皇, 郑挺国. 中国金融形势指数混频测度及其预警行为研究[J]. 金融研究, 2018(3):21-35. |

| Shang Y H, Zheng T G. The mixed frequency measuring of Chinese FCI and its risk warning behavior[J]. Journal of Financial Research, 2018(3):21-35. | |

| 22 | 杨小玄, 王一飞. 我国系统性风险度量指标构建及预警能力分析—基于混频数据动态因子模型[J]. 南方金融, 2019(6):3-15. |

| Yang X X, Wang Y F. Construction of China's systematic risk measurement indicators and analysis of early warning capability:Based on dynamic factor model of mixing data[J]. South China Finance, 2019(6):3-15. | |

| 23 | 杨子晖. 金融市场与宏观经济的风险传染关系——基于混合频率的实证研究[J]. 中国社会科学, 2020 (12):160-180. |

| Yang Z H. The risk contagion relationship between the financial market and the macro economy: A mixed-frequency based empirical research[J]. Social Sciences in China, 2020(12):160-180. | |

| 24 | Jondeau E, Rockinger M. The Copula-GARCH model of conditional dependencies: An international stock market application[J]. Journal of International Money and Finance, 2006,25(5):827-853. |

| 25 | Engle R F. Dynamic conditional correlation a simple class of multivariate GARCH models[J]. Journal of Business and Economic Statistics, 2002,20(3):339-350. |

| 26 | 吴金宴, 王鹏. 哪些因素影响了股市风险传染?——来自行业数据的证据[J].中国管理科学,2022,30 (8):57-68. |

| Wu J Y, Wang P. Factors affecting the risk contagion of the stock market: An evidence from industry-level data[J].Chinese Journal of Management Science, 2022,30(8):57-68. | |

| 27 | Bonaccolto G, Caporin M, Panzica R. Estimation and model-based combination of causality networks among large US banks and insurance companies[J]. Journal of Empirical Finance,2019,54(C):1-21. |

| 28 | Hmimida M, Kanawati R. Community detection in multiplex networks: A seed-centric approach[J]. Networks and Heterogeneous Media, 2015,10(1):71-85. |

| 29 | Debarsy N, Dossougoin C, Ertur C, et al. Measuring sovereign risk spillovers and assessing the role of transmission channels: A spatial econometrics approach[J]. Journal of Economic Dynamics and Control,2018,87:21-45. |

| 30 | 赵飞. 实体行业风险溢出机制与特征分析[J].财经论丛,2021(9):49-59. |

| Zhao F. Analysis of risk spillover mechanism and characteristics among real industry[J].Collected Essays on Finance and Economics,2021(9):49-59. | |

| 31 | 苏帆. 系统性金融风险测度及其网络传染机制研究[D].武汉:中南财经政法大学博士学位论文,2017. |

| Su Fan. A research on measuring the systemic risk and its contagion in networks[D].Wuhan: Zhongnan University of Economics and Law,2017. | |

| 32 | Mantegna R N. Hierarchical structure in financial markets[J]. Computer Physics Communications, 1999,121(1):153-156. |

| 33 | Rosen K H. 《离散数学及其应用(原书第7版)》[M].北京:机械工业出版社, 2015.RosenK H. Discrete mathematics and its applications[M]. Beijing: China Machinery Industry Press, 2015. |

| 34 | Long H, Zhang J, Tang N. Does network topology influence systemic risk contribution? A perspective from the industry indices in Chinese stock market[J]. PLOS one,2017,12(7): 1-19. |

| 35 | 李守伟, 解一苇, 杨坤, 等. 商业银行多层网络结构对系统性风险影响研究[J].东南大学学报(哲学社会科学版),2019,21(4):77-84+147. |

| Li S W, Xie Y W, Yang K, et al. Impact of multiplex network structures of banks on systemic risk[J].Journal of Southeast University (Philosophy and Social Science),2019,21(4):77-84+147. |

| [1] | Xinyu Wu,Haibin Xie,Chaoqun Ma. Economic Policy Uncertainty and Renminbi Exchange Rate Volatility: Evidence from CARR-MIDAS Model [J]. Chinese Journal of Management Science, 2024, 32(8): 1-14. |

| [2] | Wenyang Wu,Hai Jiang,Shenfeng Tang. Digital Transformation, Network Relevance and Banking Systemic Risk [J]. Chinese Journal of Management Science, 2024, 32(3): 9-19. |

| [3] | Qiang Fu,Zelong Shi. Research on Frequency of the Joint Network Connectedness of Systemic Financial Risks in China ——Based on the Locally Stationary Non-parametric Time-varying Vector HAR Model [J]. Chinese Journal of Management Science, 2024, 32(2): 1-10. |

| [4] | Qifa Xu, Zezhou Wang, Cuixia Jiang. Research on Mixed Frequency Asset Pricing Based on Generative Adversarial Network [J]. Chinese Journal of Management Science, 2024, 32(11): 53-64. |

| [5] | Ranran Guo,Wuyi Ye,Xiaoquan Liu,Baiqi Miao. The Tail Dependence Between Commodity Futures Portfolios:Based on qpr-MIDAS Model [J]. Chinese Journal of Management Science, 2024, 32(10): 11-19. |

| [6] | Yangli Guo,Feng MA. Forecasting the Chinese Gold Futures Market Volatility Using Markov-Switching Regime and Mixed Data Sampling Model [J]. Chinese Journal of Management Science, 2024, 32(1): 13-22. |

| [7] | ZHAO Jing, GUO Ye. Stronger Financial Regulation, Shadow Banking and Bank Systemic Risk [J]. Chinese Journal of Management Science, 2023, 31(7): 50-59. |

| [8] | WANG Hu, LI Shou-wei, MA Yu-yin, LIU Xiao-xing. Research on the Systemic Risk of Funds Based on the Network of Common Asset Holdings [J]. Chinese Journal of Management Science, 2023, 31(6): 82-90. |

| [9] | Wu-yi YE,Ai-lin LI,Shou-kun JIAO. Risk Spillover of Soybean Futures Market Based on Dynamic Model Averaging [J]. Chinese Journal of Management Science, 2023, 31(12): 1-10. |

| [10] | OUYANG Zi-sheng, YANG Xi-te, HUANG Ying. Research on Systemic Risk Contagion Effect of Chinese Financial Institutions Considering Network Public Opinion Index [J]. Chinese Journal of Management Science, 2022, 30(4): 1-12. |

| [11] | LIU Zhi-dong, ZHANG Pei-yuan, JING Zhong-bo. Research on the Systemic Risk of China’s Banking Industry under the Impact of Cross-industry Risk Spillover [J]. Chinese Journal of Management Science, 2022, 30(12): 1-12. |

| [12] | ZHANG Fei-peng, XU Yi-xiong, ZOU Sheng-xuan, CHEN Yan. An Empirical Study on the Systemic Risk of Chinese A-Share Listed Companies Based on Multi-layer Network [J]. Chinese Journal of Management Science, 2022, 30(12): 13-25. |

| [13] | TAN De-kai, TIAN Li-hui. Is Gold a Safe Haven of the Stock Market?——Based on Dynamic Conditional Correlation Mixed Data Sampling Model [J]. Chinese Journal of Management Science, 2022, 30(10): 14-24. |

| [14] | GAO Qian-qian, FAN Hong. Study on Systematic Risk and Investment Strategy Based on Bank-Asset Bipartite Network Model [J]. Chinese Journal of Management Science, 2021, 29(7): 1-12. |

| [15] | ZHAO Lin-hai, CHEN Ming-zhi. Systemic Risk Spillovers and Systemic Risk Contributions of Financial Institutions in China: A Perspective of Dual Time-varying Dependence of Rolling Window Dynamic Copula Model [J]. Chinese Journal of Management Science, 2021, 29(7): 71-83. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||