主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2024, Vol. 32 ›› Issue (6): 34-45.doi: 10.16381/j.cnki.issn1003-207x.2021.2020

Previous Articles Next Articles

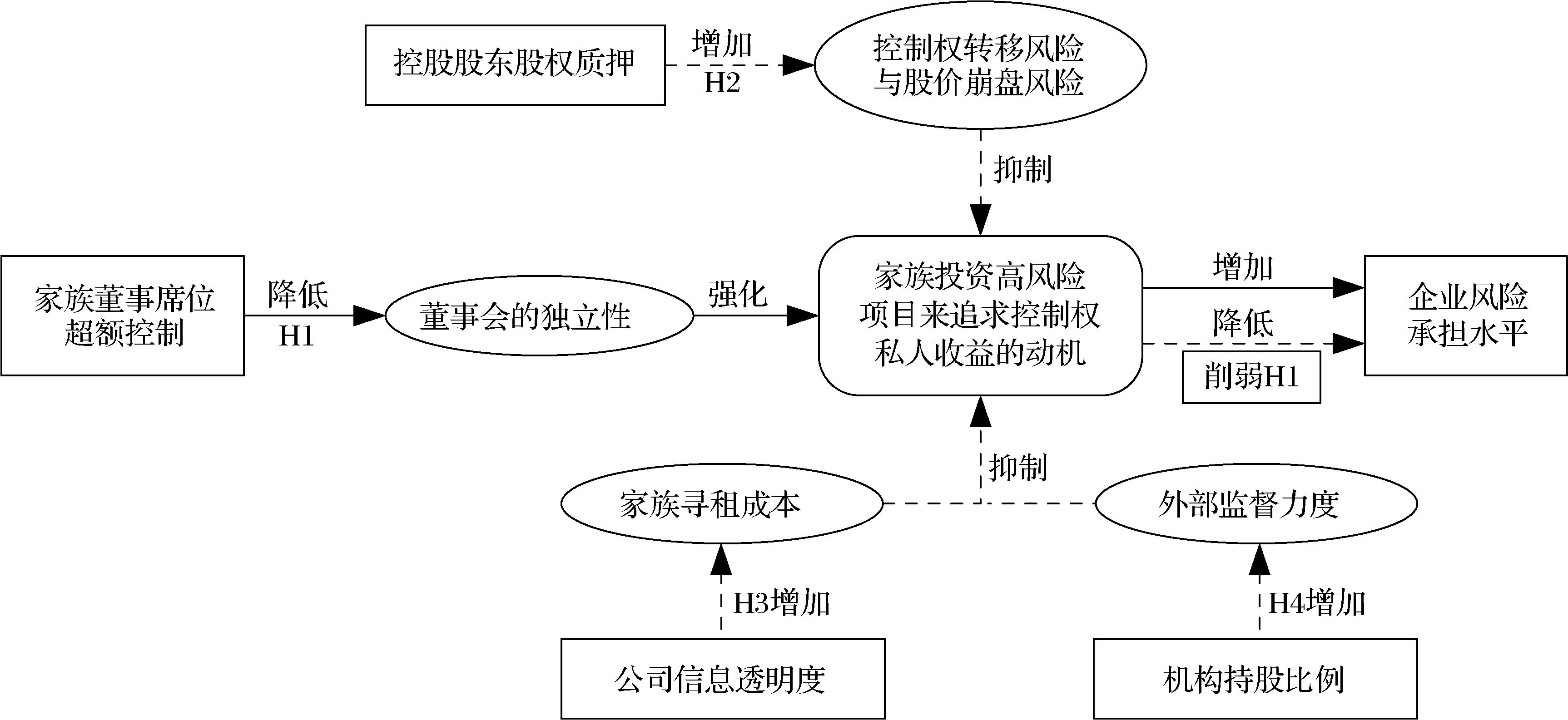

Chun Su1( ),Xing Liu2

),Xing Liu2

Received:2021-10-04

Revised:2022-02-22

Online:2024-06-25

Published:2024-07-03

Contact:

Chun Su

E-mail:suchongzhi@126.com

CLC Number:

Chun Su,Xing Liu. Does Excess Control of Family Board Seats Affect Corporate Risk-Taking?[J]. Chinese Journal of Management Science, 2024, 32(6): 34-45.

"

"

| 变量名称 | 变量符号 | 变量度量 |

|---|---|---|

| 企业风险承担 | Risk1 | 等于经年度行业均值调整后的Roa的未来三年滚动极差 |

| Risk2 | 等于经年度行业均值调整后的Roa的未来三年滚动标准差 | |

| 家族董事席位超额控制 | ECFBS | 等于家族对公司董事席位控制比例与家族控制权之差 |

| 是否存在股权质押 | Pledge_dum | 家族控股股东年末存在股权质押取值为1,否则取值为0 |

| 股权质押率 | Pledge | 等于家族控股股东质押股票数/家族控股股东持有股票总数 |

| 公司信息透明度 | Transparency | 等于公司年末分析师跟踪人数 |

| 机构持股比例 | InsHold | 等于前十大股东中机构持股比例总和 |

| 公司规模 | Size | 等于Ln(期末总资产) |

| 公司年龄 | Age | 等于Ln(当年年份-公司成立年份) |

| 成长性 | Growth | 等于(本年营业收入-上年营业收入)/上年营业收入 |

| 财务杠杆率 | lev | 等于期末总负债/期末总资产 |

| 两权分离度 | Speration | 等于家族控制权与家族所有权之差 |

| 无形资产占比 | Intangible | 等于期末无形资产/期末总资产 |

| 董事会规模 | Board | 董事会总人数 |

| 独立董事比例 | Indep | 等于独立董事人数/董事会人数 |

| 两职合一 | Dual | 董事长与总经理由一人担任,取值为1,否则取值为0 |

| 家族持股比例 | Fsh | 等于前十大股东中所有家族成员持股比例之和 |

| 地区人均GDP | GDP_per | 等于Ln(各省份人均GDP) |

| 董事长年龄 | Chairman_age | 等于Ln(当年年份-董事长出生年份) |

| 董事长学历 | Chairman_edu | 取值1~5,依次代表中专及以下、大专、本科、硕士、博士学历 |

"

| 变量 | N | mean | sd | min | p25 | p50 | p75 | max |

|---|---|---|---|---|---|---|---|---|

| Risk1 | 6417 | 0.0603 | 0.0713 | 0.0032 | 0.0205 | 0.0365 | 0.0662 | 0.3778 |

| Risk2 | 6417 | 0.0321 | 0.0388 | 0.0016 | 0.0107 | 0.0191 | 0.0349 | 0.2075 |

| ECFBS | 6417 | -0.0786 | 0.1918 | -0.5587 | -0.2081 | -0.0777 | 0.0549 | 0.3710 |

| Pledge_dum | 6417 | 0.5005 | 0.5000 | 0.0000 | 0.0000 | 1.0000 | 1.0000 | 1.0000 |

| Pledge | 6417 | 0.2970 | 0.3581 | 0.0000 | 0.0000 | 0.0118 | 0.6138 | 1.0000 |

| Transparency | 6417 | 8.2216 | 8.8854 | 0.0000 | 1.0000 | 5.0000 | 12.0000 | 53.0000 |

| InsHold | 6417 | 0.0441 | 0.0445 | 0.0000 | 0.0073 | 0.0308 | 0.0686 | 0.2374 |

"

| 变量 | Risk1 | Risk2 | ECFBS | Pledge_dum | Pledge | Transparency | InsHold |

|---|---|---|---|---|---|---|---|

| Risk1 | 1.0000 | ||||||

| Risk2 | 0.9982*** | 1.0000 | |||||

| ECFBS | 0.0457*** | 0.0458*** | 1.0000 | ||||

| Pledge_dum | -0.1248*** | -0.1267*** | 0.0668*** | 1.0000 | |||

| Pledge | -0.1853*** | -0.1879*** | 0.0930*** | 0.0829*** | 1.0000 | ||

| Transparency | -0.0649*** | -0.0645*** | -0.0452*** | -0.0127 | -0.0767*** | 1.0000 | |

| InsHold | -0.01189*** | -0.0187*** | 0.1149*** | -0.0641*** | -0.0715*** | 0.3642*** | 1.0000 |

"

| 变量 | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

|---|---|---|---|---|---|---|---|---|

| Risk1 | Risk2 | Risk1 | Risk2 | Risk1 | Risk2 | Risk1 | Risk2 | |

| ECFBS | 0.0159** | 0.0087** | 0.0148** | 0.0081** | 0.0200*** | 0.0109*** | 0.0187*** | 0.0102*** |

| (2.10) | (2.12) | (2.02) | (2.04) | (2.73) | (2.76) | (2.61) | (2.63) | |

| Constant | -0.0792 | -0.0479 | -0.0334 | -0.0243 | 0.1080 | 0.0566 | 0.1427* | 0.0741 |

| (-1.07) | (-1.20) | (-0.41) | (-0.55) | (1.39) | (1.33) | (1.72) | (1.63) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry | NO | NO | Yes | Yes | NO | NO | Yes | Yes |

| Year | NO | NO | NO | NO | Yes | Yes | Yes | Yes |

| N | 6417 | 6417 | 6417 | 6417 | 6417 | 6417 | 6417 | 6417 |

| R2 | 0.0476 | 0.0485 | 0.0649 | 0.0658 | 0.1050 | 0.1057 | 0.1196 | 0.1202 |

"

| 变量 | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Risk1 | Risk2 | Risk1 | Risk2 | |

| ECFBS | 0.0251*** | 0.0136*** | 0.0214*** | 0.0115*** |

| (3.40) | (3.45) | (2.98) | (3.00) | |

| Pledge_dum | -0.0026*** | -0.0014*** | ||

| (-3.55) | (-3.60) | |||

| Pledge | -0.0042*** | -0.0023*** | ||

| (-4.28) | (-4.36) | |||

ECFBS× Pledge_dum | -0.0075*** | -0.0041*** | ||

| (-2.72) | (-2.72) | |||

ECFBS× Pledge | -0.0055*** | -0.0030*** | ||

| (-2.78) | (-2.75) | |||

| Constant | 0.1378* | 0.0714 | 0.1423* | 0.0738 |

| (1.67) | (1.59) | (1.73) | (1.64) | |

| Controls | Yes | Yes | Yes | Yes |

| Industry& Year | Yes | Yes | Yes | Yes |

| N | 6417 | 6417 | 6417 | 6417 |

| R2 | 0.1187 | 0.1192 | 0.1193 | 0.1198 |

"

| 变量 | (1) | (2) |

|---|---|---|

| Risk1 | Risk2 | |

| ECFBS | 0.0828*** | 0.0451*** |

| (8.92) | (8.93) | |

| Tansparency | -0.0009*** | -0.0005*** |

| (-3.14) | (-3.13) | |

| ECFBS×Tansparency | -0.0014** | -0.0007** |

| (-2.10) | (-2.06) | |

| Constant | 0.0556 | 0.0256 |

| (0.85) | (0.72) | |

| Controls | Yes | Yes |

| Industry& Year | Yes | Yes |

| N | 6417 | 6417 |

| R2 | 0.1428 | 0.1432 |

"

| 变量 | (1) | (2) |

|---|---|---|

| Risk1 | Risk2 | |

| ECFBS | 0.0756*** | 0.0413*** |

| (7.12) | (7.19) | |

| InsHold | -0.0195 | -0.0108 |

| (-0.79) | (-0.81) | |

| ECFBS×InsHold | -0.0222** | -0.0103* |

| (-2.21) | (-1.92) | |

| Constant | 0.0850 | 0.0419 |

| (1.13) | (1.03) | |

| Controls | Yes | Yes |

| Industry& Year | Yes | Yes |

| N | 6417 | 6417 |

| R2 | 0.1429 | 0.1435 |

"

| 变量 | Tunneling | |||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| ECFBS | 0.0097*** | 0.0088*** | ||

| (3.23) | (3.03) | |||

| Risk1 | 0.0172*** | 0.0268*** | ||

| (3.28) | (3.22) | |||

| Risk2 | 0.0313*** | 0.0524*** | ||

| (3.30) | (3.41) | |||

| ECFBS×Risk1 | 0.0160* | |||

| (1.95) | ||||

| ECFBS×Risk2 | 0.0330** | |||

| (2.18) | ||||

| Constant | 0.0497** | 0.0473** | 0.0440** | 0.0499** |

| (2.09) | (2.16) | (1.98) | (2.28) | |

| Controls | Yes | Yes | Yes | Yes |

| Industry& Year | Yes | Yes | Yes | Yes |

| N | 6417 | 6417 | 6417 | 6417 |

| R2 | 0.0254 | 0.0325 | 0.0253 | 0.0357 |

"

| 变量 | (1) | (2) | (3) | (4)sargen test | (5)sargen test | (6)2SLS | (7)2SLS |

|---|---|---|---|---|---|---|---|

| Risk1 | Risk2 | ECFBS | Risk1 | Risk2 | |||

| ECFBS_indaverage | 0.0736 | 0.0379 | 0.5421*** | 0.0604 | 0.0308 | ||

| (1.27) | (1.19) | (7.33) | (1.43) | (1.35) | |||

| ECFBS_proaverage | 0.0140 | 0.0092 | 0.1467*** | -0.0154 | -0.0072 | ||

| (0.55) | (0.67) | (5.83) | (-0.81) | (-0.71) | |||

| ECFBS | 0.0192*** | 0.0104*** | 0.1093** | 0.0599** | |||

| (2.68) | (2.70) | (2.26) | (2.32) | ||||

| Constant | 0.1394* | 0.0721 | 0.0115*** | 0.0322 | 0.0172 | 0.2701*** | 0.1446*** |

| (1.67) | (1.58) | (6.52) | (0.68) | (0.67) | (5.49) | (5.44) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry& Year | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 6417 | 6417 | 6417 | 6417 | 6417 | 6417 | 6417 |

| R2 | 0.1205 | 0.1211 | 0.4846 | 0.0019 | 0.0018 | 0.1163 | 0.1150 |

"

| 变量 | (1) | (2) |

|---|---|---|

| Risk1 | Risk2 | |

| ECFBS | 0.0136** | 0.0074** |

| (2.03) | (2.05) | |

| Constant | 0.1445* | 0.0737* |

| (1.85) | (1.75) | |

| Controls | Yes | Yes |

| Industry&Year | Yes | Yes |

| N | 6417 | 6417 |

| R2 | 0.1217 | 0.1228 |

| 1 | Lumpkin G T, Dess G G.Clarifying the entrepreneurial orientation construct and linking it to performance[J].The Academy of Management Review,1996,21(1):135-172. |

| 2 | 余明桂,李文贵,潘红波.管理者过度自信与企业风险承担[J].金融研究,2013(1):149-163. |

| Yu M G, Li W G, Pan H B. Managerial overconfidence and enterprise risk-taking[J]. Journal of Financial Research,2013(1):149-163. | |

| 3 | Morck R, Shleifer A, Vishny R W. Management ownership and market valuation:An empirical analysis[J].Journal of Financial Economics,1988,20(88):293-315. |

| 4 | Beasley M S.An empirical analysis of the relation between board of director composition and financial Statementfraud[J].The Accounting Review,1996,71(4):443-465. |

| 5 | Akbar S, Kharabsheh B, Poletti-Hughe J,et al. Board structure and corporate risk taking in the UK financial sector[J].International Review of Financial Analysis,2017,50(C):101-110. |

| 6 | 孟焰,赖建阳.董事来源异质性对风险承担的影响研究[J].会计研究,2019(7): 35-42. |

| Meng Y, Lai J Y. The influence of directors’ sources diversity on risk-taking[J].Accounting Research,2019(7):35-42. | |

| 7 | Villalonga B, Amit R.How are U.S. family firms controled?[J].Review of Financial Studies,2009,22(8):3047-3091. |

| 8 | Amit R, Ding Y, Villalonga B,et al. The role of instituteonal development in the prevalence and performanceof entrepreneur and family-controlled firms[J]. Journal of Corporate Finance,2015,31:284-305. |

| 9 | 刘星,苏春,邵欢. 家族董事席位配置偏好影响企业投资效率吗[J].南开管理评论,2020,23(4):131-141. |

| Liu X, Su C, Shao H. Does the preference of family board seats allocation influence corporate investment efficiency[J]. Nankai Business Review,2020,23(4):131-141. | |

| 10 | 刘星,苏春,邵欢. 家族董事席位超额控制与股价崩盘风险——基于关联交易的视角[J].中国管理科学,2021,29(5):1-13. |

| Liu X, Su C, Shao H. Excess control of family board seats and stock price crash risk:Based on the perspective of related party trasactions[J]. Chinese Journal of Management Science,2021,29(5):1-13. | |

| 11 | 陈德球,魏刚,肖泽忠.法律制度效率、金融深化与家族控制权偏好[J].经济研究,2013,48(10):55-68. |

| Chen D Q, Wei G, Xiao Z Z. Law efficiency,financial deepening and family control preferences[J]. Economic Research Journal,2013,48(10):55-68. | |

| 12 | 刘星,苏春,邵欢. 代际传承与家族董事席位超额控制[J].经济研究,2021,56(12):111-129. |

| Liu X, Su C, Shao H. Intergenerational successsion and excess control of family board seats[J]. Economic Research Journal,2021,56(12):111-129. | |

| 13 | 陈德球, 叶陈刚, 李楠.控制权配置、代理冲突与审计供求——来自中国家族上市公司的经验证据[J].审计研究, 2011(5):57-64. |

| Chen D Q, Ye C G, Li N. Control rights allocateion,agency conflicts and auditor demand and supply:Empirical evidence from the Chinese family listed companies[J]. Auditing Research,2011(5):57-64. | |

| 14 | 陈德球,李思飞,雷光勇.政府治理、控制权结构与投资决策——基于家族上市公司的经验证据[J].金融研究,2012(3)124-138. |

| Chen D Q, Li S F, Lei G Y. Governance,controlstructure and investment decision: Empirical evidence from family listed firm[J]. Journal of Financial Research,2012(3):124-138. | |

| 15 | 陈德球,肖泽忠,董志勇.家族控制权结构与银行信贷合约:寻租还是效率?[J].管理世界,2013(9):130-143. |

| Chen D Q, Xao Z Z, Dong Z Y. The composition of the family control rights and the credit contract of banks: Is it rent-seeking or efficiency?[J]. Management World,2013(9):130-143. | |

| 16 | 赵宜一,吕长江.家族成员在董事会中的角色研究——基于家族非执行董事的视角[J].管理世界,2017(9):155-165. |

| Zhao Y Y, Lv C J. Research on the role of family members in the board from the perspective of the family’s non: Executive directors[J].Management World,2017(9):155-165. | |

| 17 | 于洪涛.董事会特征、风险承担与公司绩效[D].大连:东北财经大学,2019. |

| Yu H T. Board characteristics,risk-taking and corporation performance[D]. Dalian:Dongbei University of Finance and Economics,2019. | |

| 18 | Wang C J.Board size and firm risk-taking[J].Review of Quantitative Finance and Accounting,2012,38(4):519-542. |

| 19 | Cheng S.Board size and the variability of corporate performance[J].Journal of Financial Economics,2008,87(1):157-176. |

| 20 | Nakano M, Nguyen P.Board size and corporate risk taking:Further evidence from Japan[J]. Corporate Governance:An International Review,2012,20(4):369-387. |

| 21 | Bernile G, Bhagwat V, Yonker S.Board diversity,firm risk,and corporate policies[J]. Journalof Financial Economics,2018,127(3):588-612. |

| 22 | 姜付秀,郑晓佳, 蔡文婧.控股家族的“垂帘听政”与公司财务决策[J].管理世界, 2017(3):125-145. |

| Jiang F X, Zheng X J, Cai W J. Controlling family’s“from behind the curtain”and company’s financial decision[J]. Management World,2017(3):125-145. | |

| 23 | Chua J H, Chrisman J J, Sharma P.Defining the family business by behavior[J].Entrepreneurship Theory and Practice,1999,23(4):19-39. |

| 24 | Jensen M C, Meckling W H.Theory of the firm:Managerial behavior,agency costs and ownership structure[J].Journal of Financial Economics,1976,3(4):305-360. |

| 25 | Ali A, Chen T, Radhakrishnan S. Corporate disclosures by family firms[J]. Journal of Accounting and Economics,2007,44(1-2): 238-286. |

| 26 | La Porta R, Lopez-De-Silanes F, Shleifer A. Corporate ownership around the world[J]. Journal of Finance,1999,54(2):471-517. |

| 27 | 马磊,徐向艺.两权分离度与公司治理绩效实证研究[J]. 中国工业经济,2010(12):108—116. |

| Ma L, Xu X Y. Empirical study on the relationship between the separation degree and corporate governance performance[J].China Industrial Economics,2010(12):108-116. | |

| 28 | Johnson S, La Porta R, Lo’Pez-De-Silanes F,et al. Tunneling[J]. American Economic Review,2000,90(2):22-27. |

| 29 | 李常青,李宇坤,李茂良.控股股东股权质押与企业创新投入[J].金融研究,2018(7):143-157. |

| Li C Q, Li Y K, Li M L. Control shareholder’s share pledge and firms’ innovation investment[J]. Journal of Financial Research,2018(7):143-157. | |

| 30 | 谢德仁,郑登津,崔宸瑜.控股股东股权质押是潜在的“地雷”吗?——基于股价崩盘风险视角的研究[J].管理世界, 2016(5):128-140. |

| Xie D R, Zheng D J, Cui C Y. Is controlling Shareholder’s share pledge a potential“mine”: Research based on the perspective of stock price crash risk[J]. Management World,2016(5):128-140. | |

| 31 | 何威风,刘怡君,吴玉宇.大股东股权质押和企业风险承担研究[J].中国软科学, 2018(5):110-122. |

| He W F, Liu Y J, Wu Y Y. Research on the pledging of stock rights by large shareholders and corporate risk-taking[J]. China Soft Science,2018(5):110-122. | |

| 32 | 王克敏,姬美光,李薇.公司信息透明度与大股东资金占用研究[J].南开管理评论, 2009,12(4):83-91. |

| Wang K M, Ji M G, Li W. Corporate transparency and expropriation by large shareholders[J]. Nankai Business Review,2009,12(4):83-91. | |

| 33 | Lin C, Ma Y, Malatesta P,et al. Corporate ownership structure and bank loan syndicate structure[J]. Journal of Financial Economics,2012,104(1):1-22. |

| 34 | Chaganti R, Damanpour F.Institutional ownership,capital structure,and firm performance[J]. Strategic Management Journal,1991,12(7):479-491. |

| 35 | Ajinkya B, Bhojraj S, Sengupta P.The association between outside directors,institutional investors and the properties of management earnings forecasts[J].Journal of Accounting Research,2005,43(3):343-376. |

| 36 | 石美娟,童卫华.机构投资者提升公司价值吗?——来自后股改时期的经验证据[J].金融研究,2009(10):150-161. |

| Shi M J, Tong W H. Do institutional investors increase company value:Empirical evidence from the postshare Reform Period[J]. Journal of Financial Research,2009(10):150-161. | |

| 37 | Xu N, Yuan Q, Jiang X,et al.Founder`s political conections,second generation involvement,and family firm performance:Evidence from China[J]. Journal of Corporate Finance,2015,33(3):243-259. |

| 38 | 刘白璐,吕长江.中国家族企业家族所有权配置效应研究[J].经济研究,2016,51(11):140-152. |

| Liu B L, Lv C J. The effect of ownership structure among family members in Chinese family fiirms[J].Economic Research Journal,2016,51(11): 140-152. | |

| 39 | Anderson R C, Reeb D M. Founding-family ownership and firm performance:Evidence from the S&P 500[J].The Journal of Finance,2003,58(3):1301-1327. |

| 40 | 巩键,陈凌,王健茜,等.从众还是独具一格?——中国家族企业战略趋同的实证研究[J].管理世界,2016(11):110-124. |

| Gong J, Chen L, Wang J X,et al. Follow the crowd or keep unique:An empirical study on the strategic convergence of Chinese family firms[J]. Management World,2016(11):110-124. | |

| 41 | Coles J L, Daniel N D, Naveen L. Managerial incentives and risk-taking[J]. Journal of Financial Economics,2006,79(2):431-468. |

| 42 | 王元芳,徐业坤.保守还是激进:管理者从军经历对公司风险承担的影响[J].外国经济与管理,2019,41(9):17-30. |

| Wang Y F, Xu Y K. Conservative or radical: The influence of managers’ military experience on the company’s risk-taking[J]. Foreign Economics & Management,2019,41(9):17-30. | |

| 43 | John K, Litov L, Yeung B.Corporate governance and risk-taking[J]. Journal of Finance,2008,63(4):1679-1728. |

| 44 | Faccio M, Marchica M T, Mura R. Large shareholder diversification and corporate risk-taking[J]. Review of Financial Studies,2011,24(11):3601-3641. |

| 45 | 肖金利,潘越,戴亦一.“保守”的婚姻:夫妻共同持股与公司风险承担[J].经济研究,2018,53(5):190-204. |

| Xiao J L, Pan Y, Dai Y Y. Marriage of “conservative”:Couples’ joint holdings and corporate risk-taking[J]. Economic Research Journal,2018,53(5):190-204. | |

| 46 | Bharath S T, Dahiya S, Saunders A,et al.Lendingrelationships and loan contract terms[J].Review of Financial Studies,2011,24(4):1141-1203. |

| 47 | 陈爽英,井润田,龙小宁,等.民营企业家社会关系资本对研发投资决策影响的实证研究[J].管理世界,2010(1):88-97. |

| Chen S Y, Jing R T, Long X N,et al. An empirical study on the impact of private entrepreneurs’ social relationship capital on R&D investment decisi-ons[J]. Management World,2010(1):88-97. |

| [1] | YU Hui, WANG Qi. Supply Chain Analysis about Enterprise's Exchange Rate Risk Management Based on the Risk-taking Mechanism [J]. Chinese Journal of Management Science, 2021, 29(9): 44-53. |

| [2] | LIU Xing, SU Chun, SHAO Huan. Excess Control of Family Board Seats and Stock Price Crash Risk——Based on the Perspective of Related Party Transactions [J]. Chinese Journal of Management Science, 2021, 29(5): 1-13. |

| [3] | WANG Ming-hao, CHEN Zhong, CAI Xiao-yu. A Study of the Effect of Relative Performance on the Risk-taking Behavior of Mutual Funds [J]. Chinese Journal of Management Science, 2004, (5): 1-5. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||