主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2024, Vol. 32 ›› Issue (1): 54-64.doi: 10.16381/j.cnki.issn1003-207x.2021.1041

Previous Articles Next Articles

Lan Bai,Yu Wei( )

)

Received:2021-05-27

Revised:2022-06-24

Online:2024-01-25

Published:2024-02-08

Contact:

Yu Wei

E-mail:weiyusy@126.com

CLC Number:

Lan Bai,Yu Wei. Information Spillovers between Investor's Public Health Emergency Attention and Industrial Stocks: Empirical Evidence from TVP-VAR Model[J]. Chinese Journal of Management Science, 2024, 32(1): 54-64.

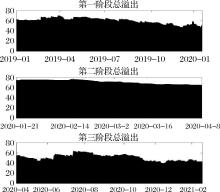

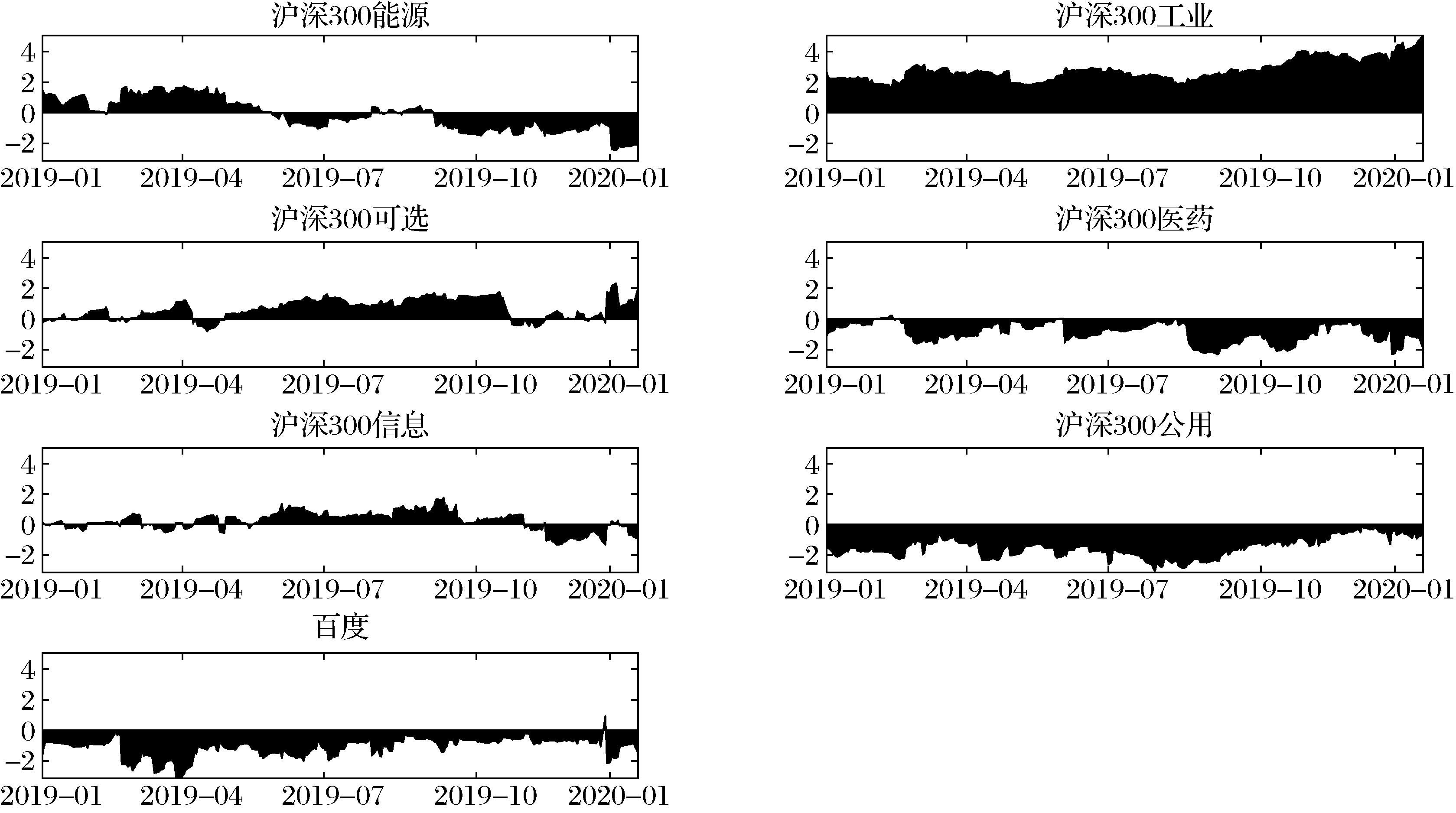

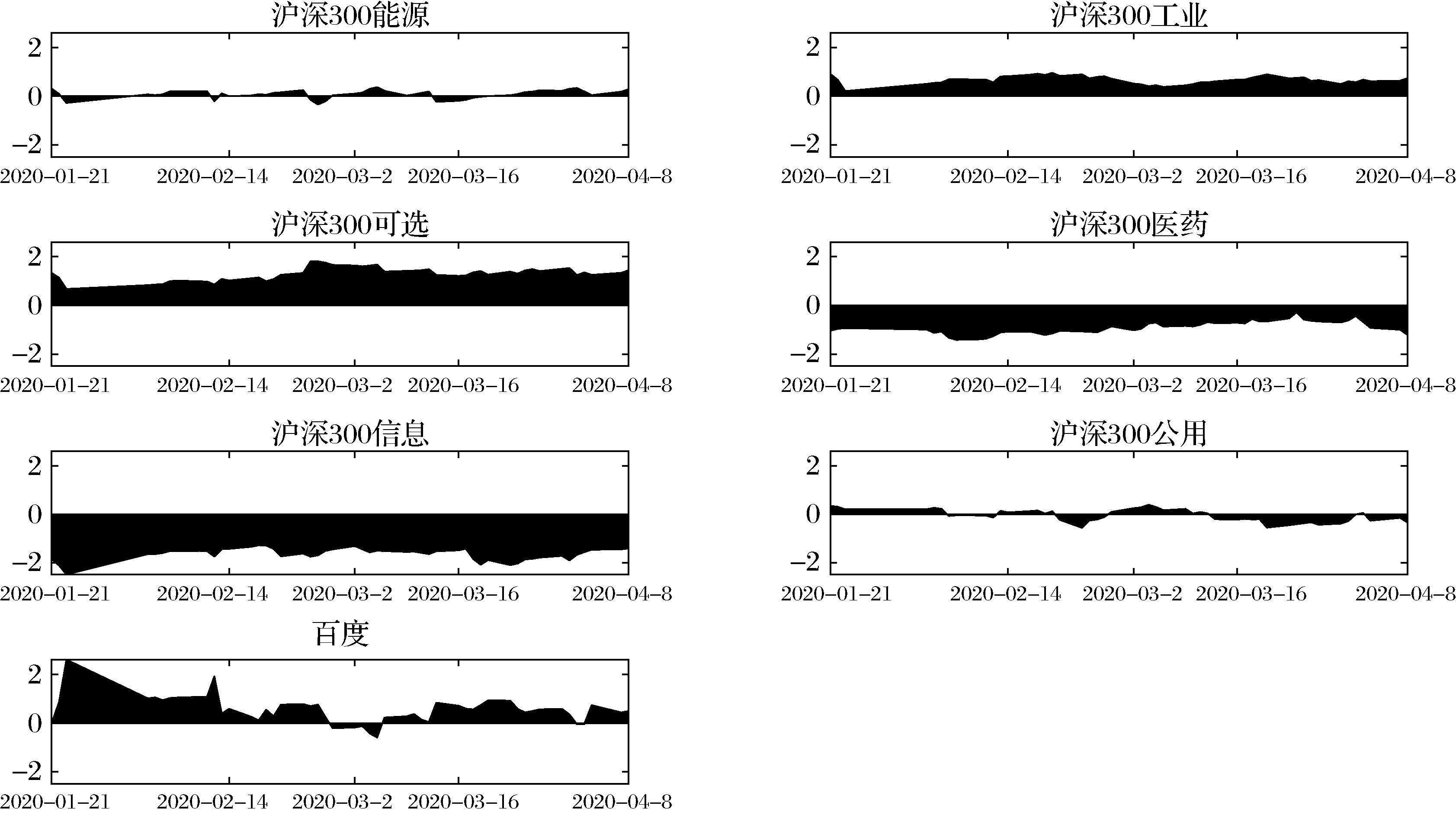

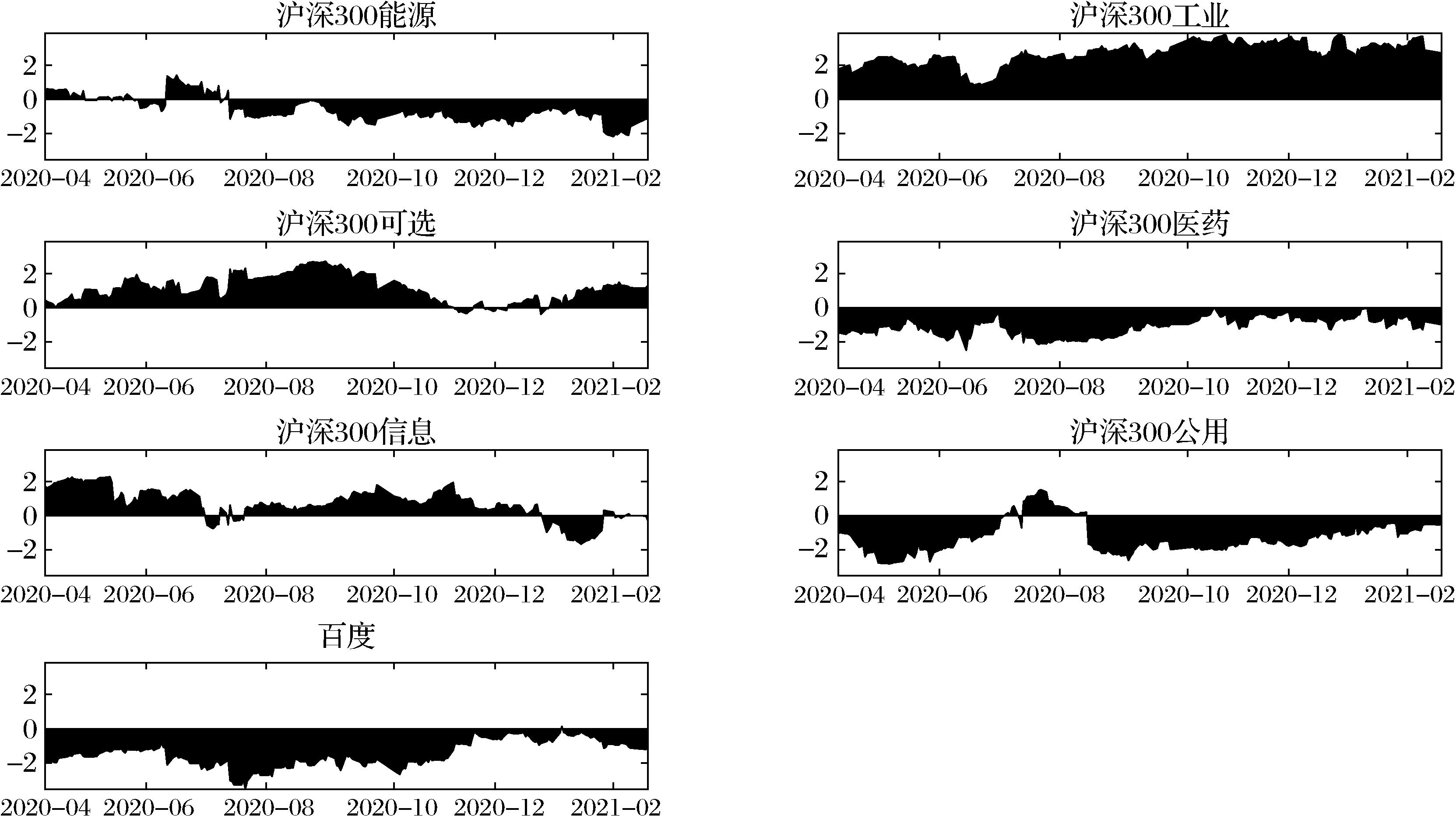

"

| 统计量 | 能源 | 工业 | 可选 | 医药 | 信息 | 公用 | 百度 |

|---|---|---|---|---|---|---|---|

| 均值 | 0.0025 | 0.1107 | 0.1567 | 0.1694 | 0.1497 | 0.0059 | -3.1291 |

| 标准差 | 1.2536 | 1.4399 | 1.6519 | 1.6900 | 2.0910 | 0.9421 | 11.8240 |

| 偏度 | -0.3445*** | -0.5481*** | -0.7347*** | -0.3814*** | -0.4944*** | -0.0780 | 3.0957*** |

| 峰度 | 5.5432*** | 4.9129*** | 3.0499*** | 0.8574*** | 2.1131*** | 1.5554*** | 27.0706*** |

| J-B | 672.1314*** | 545.8291*** | 246.8888*** | 28.3716*** | 117.2563*** | 52.6381*** | 16611.8711*** |

| Q(5) | 6.5790 | 6.5890 | 4.3820 | 1.9060 | 4.8440 | 6.1490 | 11.4250** |

| Q(20) | 23.0740 | 23.5450 | 16.3060 | 29.6200 | 17.4540 | 16.5020 | 77.1500*** |

| ADF | -21.1394*** | -21.7964*** | -22.3128*** | -22.3715*** | -22.1220*** | -22.8172*** | -20.3169*** |

| P-P | -21.1788*** | -21.8392*** | -22.3567*** | -22.4165*** | -22.1657*** | -22.8616*** | -20.3539*** |

"

| 行业 | 能源 | 工业 | 可选 | 医药 | 信息 | 公用 | 百度 | FROM |

|---|---|---|---|---|---|---|---|---|

| 能源 | 32.6 | 20.6 | 13.1 | 8.6 | 12.2 | 11.4 | 1.3 | 9.6 |

| 工业 | 16.7 | 26.1 | 16.7 | 11.7 | 16.8 | 11.2 | 0.8 | 10.6 |

| 可选 | 12.4 | 19.1 | 30.2 | 15.2 | 13.2 | 9.2 | 0.7 | 10.0 |

| 医药 | 9.5 | 15.4 | 17.7 | 35.3 | 13.7 | 7.6 | 0.9 | 9.2 |

| 信息 | 11.8 | 20.0 | 13.8 | 12.3 | 31.8 | 9.4 | 0.8 | 9.7 |

| 公用 | 13.4 | 16.2 | 11.2 | 8.2 | 12.0 | 37.6 | 1.4 | 8.9 |

| 百度 | 2.8 | 2.4 | 1.8 | 2.1 | 2.0 | 2.8 | 86.1 | 2.0 |

| TO | 9.5 | 13.4 | 10.6 | 8.3 | 10.0 | 7.4 | 0.9 | 60.0 |

| NET | -0.1 | 2.8 | 0.6 | -0.9 | 0.2 | -1.5 | -1.1 |

"

| 行业 | 能源 | 工业 | 可选 | 医药 | 信息 | 公用 | 百度 | FROM |

|---|---|---|---|---|---|---|---|---|

| 能源 | 20.9 | 18.0 | 16.5 | 10.8 | 10.7 | 16.8 | 6.3 | 11.3 |

| 工业 | 17.3 | 20.1 | 17.0 | 11.6 | 12.3 | 15.9 | 5.8 | 11.4 |

| 可选 | 15.6 | 16.6 | 19.7 | 14.2 | 15.0 | 13.7 | 5.2 | 11.5 |

| 医药 | 12.5 | 13.8 | 17.6 | 25 | 13.9 | 12.8 | 4.5 | 10.7 |

| 信息 | 12.7 | 15.0 | 18.5 | 13.9 | 24.3 | 11.4 | 4.3 | 10.8 |

| 公用 | 17.3 | 17.0 | 15.3 | 11.9 | 10.7 | 21.9 | 5.9 | 11.2 |

| 百度 | 4.4 | 4.2 | 4.5 | 6.3 | 1.7 | 7.0 | 71.9 | 4.0 |

| TO | 11.4 | 12.1 | 12.8 | 9.8 | 9.2 | 11.1 | 4.6 | 70.9 |

| NET | 0.1 | 0.7 | 1.3 | -0.9 | -1.6 | -0.1 | 0.5 |

"

| 行业 | 能源 | 工业 | 可选 | 医药 | 信息 | 公用 | 百度 | FROM |

|---|---|---|---|---|---|---|---|---|

| 能源 | 46.2 | 17.2 | 11.2 | 2.0 | 8.0 | 12.9 | 2.6 | 7.7 |

| 工业 | 12.2 | 33.5 | 19.6 | 10.4 | 17.1 | 6.4 | 0.7 | 9.5 |

| 可选 | 8.4 | 21.3 | 36.8 | 10.4 | 17.1 | 4.4 | 1.7 | 9.0 |

| 医药 | 2.0 | 14.3 | 12.7 | 53.0 | 14.7 | 2.7 | 0.7 | 6.7 |

| 信息 | 7.0 | 19.8 | 17.5 | 11.4 | 38.4 | 4.8 | 1.1 | 8.8 |

| 公用 | 15.8 | 10.3 | 6.1 | 3.4 | 6.8 | 54.7 | 3.0 | 6.5 |

| 百度 | 4.3 | 2.7 | 3.9 | 1.6 | 2.6 | 5.3 | 79.7 | 2.9 |

| TO | 7.1 | 12.2 | 10.2 | 5.6 | 9.5 | 5.2 | 1.4 | 51.1 |

| NET | -0.6 | 2.7 | 1.1 | -1.1 | 0.7 | -1.3 | -1.5 |

"

"

"

"

| 1 | 方意, 于渤, 王炜.新冠疫情影响下的中国金融市场风险度量与防控研究[J].中央财经大学学报,2020(8): 116-128. |

| Fang Y, Yu B, Wang W. China’ s financial market risk measurement and controlling under covid-19 shock[J]. Journal of Central University of Finance and Economics,2020(8): 116-128. | |

| 2 | 杨子晖, 陈雨恬, 张平淼.重大突发公共事件下的宏观经济冲击、金融风险传导与治理应对[J].管理世界,2020, 36(5): 13-35+7. |

| Yang Z H, Chen Y T, Zhang P M. Macroeconomic shock, financial risk transmission and governance response to major public emergencies[J]. Journal of Management World,2020, 36(5): 13-35+7. | |

| 3 | 蒋海, 吴文洋, 韦施威.新冠肺炎疫情对全球股市风险的影响研究——基于ESA方法的跨市场检验[J].国际金融研究,2021(3): 3-13. |

| Jiang H, Wu W Y, Wei S W. Research on the impact of COVID-19 on the risks of global stock market: cross market test based on ESA method[J]. Studies of International Finance,2021(3): 3-13. | |

| 4 | Bouri E, Cepni O, Gabauer D, et al.Return connectedness across asset classes around the COVID-19 outbreak[J].International Review of Financial Analysis,2021, 73,101646. |

| 5 | 张宗新, 王海亮.投资者情绪、主观信念调整与市场波动[J].金融研究,2013(4): 142-155. |

| Zhang Z X, Wang H L. Investor sentiment, subjective belief adjustment and market fluctuation[J]. Journal of Financial Research,2013(4): 142-155. | |

| 6 | 唐振鹏, 吴俊传, 冉梦, 等.考虑投资者情绪的中国股市自激发效应研究[J].中国管理科学,2020, 28(7): 1-12. |

| Tang Z P, Wu J C, Ran M, et al. Research on the self-exciting effect of Chinese stock market considering investor sentiment[J]. Chinese Journal of Management Science,2020, 28(7): 1-12. | |

| 7 | 张国胜, 林宇.结构突变下投资者情绪与股市收益间的非线性溢出效应研究[J].数理统计与管理,2021, 40 (1): 148-161. |

| Zhang G S, Lin Y. Research on non-liner information spillover effect between investor sentiment and stock market return under structural break[J]. Journal of Applied Statistics and Management,2021, 40(1): 148-161. | |

| 8 | Al-Awadhi A M, Alsaifi K, Al-Awadhi A, et al.Death and contagious infectious diseases: impact of the COVID-19 virus on stock market returns[J].Journal of Behavioral and Experimental Finance,2020, 27: 100326. |

| 9 | Pham A V, Adrian C, Garg M, et al.State-level COVID-19 outbreak and stock returns[J].Finance Research Letters,2021, 43: 102002. |

| 10 | 易行健.新冠肺炎疫情对经济金融的冲击研究——基于国际文献综述及其扩展分析[J].金融经济学研究,2020, 35(3): 3-16. |

| Yi X J. The economic and financial impacts of the COVID-19 pandemic: discussions based on international literature review and related conclusions[J]. Financial Economics Research,2020, 35(3): 3-16. | |

| 11 | 程晨, 刘珂.新冠肺炎疫情下资本市场的冲击研究——基于股价同步性视角[J].工业技术经济,2021, 40(3): 125-135. |

| Cheng C, Liu K. Research on the impact of capital markets under COVID-19: based on stock price synchronization[J]. Journal of Industrial Technological Economics,2021, 40(3): 125-135. | |

| 12 | 陈奉功.新冠肺炎疫情对我国企业的异质性影响——基于股价波动视角的实证研究[J].工业技术经济,2020, 39(10): 3-14. |

| Chen F G.The heterogeneous impact of COVID-19 on chinese enterprises: empirical research based on the perspective of stock price fluctuations[J]. Journal of Industrial Technological Economics,2020, 39(10): 3-14. | |

| 13 | 田金方, 杨晓彤, 薛瑞, 等. 不确定性事件、投资者关注与股市异质特征——以COVID-19概念股为例[J].财经研究,2020, 46 (11): 19-33. |

| Tian J F, Yang X T, Xue R, et al. Uncertain event,investor attention and heterogeneity of the stock market:a case study on COVID-19[J]. Journal of Finance and Economics,2020, 46 (11): 19-33. | |

| 14 | 巫细波, 张小英, 葛志专, 等.我国COVID-19疫情时空演变特征研究——基于314个城市329天面板数据[J].地域研究与开发,2021, 40(1): 1-6. |

| Wu X B, Zhang X Y, Ge Z Z, et al. Study on characteristics of spatio-temporal evolution of COVID-19 epidemic in china: based on 329 days panel data of 314 cities[J]. Areal Research and Development,2021, 40(1): 1-6. | |

| 15 | 张建平, 朱雅锡.后疫情时代下新冠肺炎疫情对中国服务经济影响——基于多期双重差分模型的研究[J].工业技术经济,2021, 40(4): 58-67. |

| Zhang J P, Zhu Y X. The impact of COVID-19 epidemic on china's service economy in post epidemic era: a study based on a multi period double difference model[J].Journal of Industrial Technological Economics,2021, 40(4): 58-67. | |

| 16 | 王箐, 王钟黎, 李士雪, 等.“新冠肺炎”疫情对中国股市价格波动的短期影响[J].经济与管理评论,2020, 36(6): 16-27. |

| Wang Q, Wang Z L, Li S X, et al. The immediate impact of COVID-19 on china’s stock price fluctuation[J]. Review of Economy and Management,2020, 36(6): 16-27. | |

| 17 | Baig A S, Butt H A, Haroon O, et al.Deaths, panic, lockdowns and US equity markets: The case of COVID-19 pandemic[J].Finance Research Letters,2021,38: 101701. |

| 18 | 陈林, 曲晓辉.传染性公共卫生事件的市场反应研究——基于新冠肺炎疫情对中国股市的影响[J].金融论坛,2020, 25(7): 25-33+65. |

| Chen L, Qu X H. Market response to contagious public health events:a research based on COVID-19’s impact on chinese stock market[J]. Finance Forum,2020, 25(7): 25-33+65. | |

| 19 | Primiceri G E.Time varying structural vector autoregressions and monetary policy[J].Review of Economic Studies,2005, 72(3): 821-852. |

| 20 | Wen F H, Zhang M Z, Deng M, et al.Exploring the dynamic effects of financial factors on oil prices based on a TVP-VAR model[J].Physica A-Statistical Mechanics and Its Applications,2019, 532: 121881. |

| 21 | 袁晨, 傅强, 彭选华.我国股票与债券、黄金间的资产组合功能研究——基于DCC-MVGARCH模型的动态相关性分析[J].数理统计与管理,2014, 33(4): 714-723. |

| Yuan C, Fu Q, Peng X H. Research on the portfolio implications of stocks, bonds and gold in china——an analysis of dynamic relationships based on DCC-MVGARCH model[J]. Journal of Applied Statistics and Management,2014, 33(4): 714-723. | |

| 22 | 曹栋, 张佳.基于GARCH-M模型的股指期货对股市波动影响的研究[J].中国管理科学,2017, 25(1): 27-34. |

| Cao D, Zhang J. The impact of index future on stock market volatility based on the GARCH-M-model[J].Chinese Journal of Management Science,2017, 25(1): 27-34. | |

| 23 | 周开国, 邢子煜, 彭诗渊.中国股市行业风险与宏观经济之间的风险传导机制[J].金融研究,2020(12): 151-168. |

| Zhou K G, Xing Z Y, Peng S Y. The contagion mechanism between industrial risk and the macro economy in china[J]. Journal of Financial Research,2020(12): 151-168. | |

| 24 | 蔚立柱, 赵越强, 张凡, 等.新冠肺炎疫情前后人民币与非美货币溢出效应特征的变化:来自30分钟高频数据的证据[J].世界经济研究,2021(4): 56-69+135. |

| Wei L Z, Zhao Y Q, Zhang F, et al. The change of the spillover effect of rmb and non us currency before and after the COVID-19: evidence from 30 minutes high frequency data[J]. World Economy Studies,2021(4): 56-69+135. | |

| 25 | Diebold F X, Yilmaz K.On the network topology of variance decompositions: measuring the connectedness of financial firms[J].Journal of Econometrics,2014, 182 (1): 119-134. |

| 26 | Antonakakis N, Chatziantoniou I, Gabauer D.Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions[J].Journal of Risk and Financial Management,2020, 13(4): 84. |

| 27 | Esmaeili P, Rafei M.Dynamics analysis of factors affecting electricity consumption fluctuations based on economic conditions: application of SVAR and TVP-VAR models[J].Energy,2021, 226: 120340. |

| 28 | 刘金全, 王国志.金融周期与经济周期关联机制研究——基于DY动态溢出指数和时变格兰杰因果关系双重检验[J].暨南学报(哲学社会科学版),2021, 43(4): 84-99. |

| Liu J Q, Wang G Z. Research on the correlation mechanism between financial cycle and business cycle: double test based on dy dynamic spillover index and time-varying granger causality[J]. Jinan Journal(Philosophy & Social Sciences),2021, 43(4): 84-99. | |

| 29 | Nakajima J, Kasuya M, Watanabe T.Bayesian analysis of time-varying parameter vector autoregressive model for the Japanese economy and monetary policy[J].Journal of the Japanese and International Economies,2011, 25(3): 225-245. |

| 30 | Belomestny D, Krymova E, Polbin A.Bayesian TVP-VARX models with time invariant long-run multipliers[J].Economic Modelling,2021, 101: 105531. |

| 31 | 赵儒煜, 聂逯松.“双循环”背景下国际贸易冲击的宏观经济效应——理论模拟与动态计量检验[J].经济问题探索,2021(5): 136-145. |

| Zhao R Y, Nie L S. Macroeconomic effects of international trade shocks under the background of “double cycle” ——theoretical simulation and dynamic empirical analysis[J]. Inquiry into Economic Issues,2021(5): 136-145. | |

| 32 | 任永平, 李伟.经济政策不确定性、投资者情绪与股价同步性——基于TVP-VAR模型的时变参数[J].上海大学学报(自然科学版),2020, 26(5): 769-781. |

| Ren Y P, Li W. Economic policy uncertainty, investor’s sentiment and stock price synchronicity: a time-varying analysis based on TVP-VAR model[J]. Journal of Shanghai University(Natural Science Edition),2020, 26(5): 769-781. | |

| 33 | 姜伟.突发大规模疫情对经济发展的影响——基于公众关注和媒体关注的视角[J].经济与管理研究,2020, 41(10): 21-41. |

| Jiang W. The Impact of the large-scale epidemic outbreak on economic growth—based on the public and media attention[J]. Research on Economics and Management,2020, 41(10): 21-41. | |

| 34 | 张同辉, 苑莹, 曾文.投资者关注能提高市场波动率预测精度吗?——基于中国股票市场高频数据的实证研究[J].中国管理科学,2020, 28(11): 192-205. |

| Zhang T H, Yuan Y, Zeng W. Can investor attention help to predict stock market volatility? An empirical research based on chinese stock market high-frequency data[J]. Chinese Journal of Management Science,2020, 28(11): 192-205. | |

| 35 | 林娟娟, 唐勇, 周小亮,等.北上资金、百度指数与股市关联性的时频域研究——基于协高阶矩视角[J].中国管理科学,2022, 30(1): 20-31. |

| Lin J J, Tang Y, Zhou X L, et al. Research on the relationship between northward capital, baidu index and stock market in time and frequency domain——based on the perspective of higher order co-moments[J].Chinese Journal of Management Science,2022, 30(1): 20-31. | |

| 36 | 刘晓君, 姜伟, 胡劲松.基于TVP-VAR模型的信心、货币政策与中国经济波动研究[J].中国管理科学,2019, 27(8): 37-46. |

| Liu X J, Jiang W, Hu J S. A study on confidence, monetary policy and China’s economic fluctuation based on TVP-VAR model[J].Chinese Journal of Management Science,2019, 27(8): 37-46. | |

| 37 | 齐红倩, 刘岩.人口年龄结构变动对经常账户和经济增长的动态影响研究——基于TVP-VAR模型的实证分析[J].中南大学学报(社会科学版),2020,26 (6): 90-102. |

| Qi H Q, Liu Y. Research on the dynamic effects of changes in population age structure on current account and economic growth: empirical analysis based on TVP-VAR model[J]. Journal of Central South University (Social Sciences),2020, 26(6): 90-102. | |

| 38 | 李成刚, 李峰, 赵光辉.货币政策规则对国际资本流动与人民币汇率的时变影响——基于TVP-SV-VAR模型的实证检验[J].中国管理科学,2021, 29(10): 35-46. |

| Li C G, Li F, Zhao G H. The time-varying effects of monetary policy rules on international capital flow and rmb exchange rate: empirical test based on TVP-SV-VAR model[J]. Chinese Journal of Management Science,2021, 29(10): 35-46. | |

| 39 | 杨涛, 郭萌萌.投资者关注度与股票市场——以PM2.5概念股为例[J].金融研究,2019(5): 190-206. |

| Yang T, Guo M M. Investor attention and the stock market: a new perspective on pm2.5 concept stocks[J]. Journal of Financial Research,2019(5): 190-206. | |

| 40 | 梁超, 魏宇, 马锋, 等.投资者关注对中国黄金价格波动率的影响研究[J].系统工程理论与实践,2022, 42(2): 320-332. |

| Liang C, Wei Y, Ma F, et al. A study on the impact of investor attention on Chinese gold volatility[J]. Systems Engineering—Theory & Practice, 2022, 42(2): 320-332 . |

| [1] | Song Shi,Ping Shi. Research on Supply Disruption of Epidemic Prevention Products Considering Product Competition and Social Learning under COVID-19 [J]. Chinese Journal of Management Science, 2024, 32(5): 171-178. |

| [2] | Fengjiao Chen,Dehai Liu. Evolutionary Path Analysis of Multi-channel Epidemic Information Release of Major Infectious Diseases [J]. Chinese Journal of Management Science, 2024, 32(4): 237-249. |

| [3] | CAI Jian-ping, WANG Jing, JIAO Zi-hao. Precise Screening Strategy of Public Health Emergency Based on Robust Optimization [J]. Chinese Journal of Management Science, 2022, 30(7): 1-8. |

| [4] | OUYANG Yan-min, WANG Chang-feng, LIU Liu, YUAN Hong-min. Study on the Risk Early Warning Interval Model Based on Improved Adaptive Optimal Partition Method——Large-scale Public Health Emergency [J]. Chinese Journal of Management Science, 2022, 30(11): 196-206. |

| [5] | LIU Xiao-jun, JIANG Wei, HU Jing-song. A Study on Confidence, Monetary Policy and China's Economic Fluctuation Based on TVP-VAR Model [J]. Chinese Journal of Management Science, 2019, 27(8): 37-46. |

| [6] | ZHU Xue-hong, CHEN Jin-yu, SHAO Liu-guo. The International Pricing Power of Chinese Metal Futures Market Based on Information Spillover [J]. Chinese Journal of Management Science, 2016, 24(9): 28-35. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||