主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (4): 24-35.doi: 10.16381/j.cnki.issn1003-207x.2023.1706

Previous Articles Next Articles

Yulei Rao, Hongbing Ouyang( ), Minchun Han, Zihong Wang

), Minchun Han, Zihong Wang

Received:2023-10-16

Revised:2024-02-06

Online:2025-04-25

Published:2025-04-29

Contact:

Hongbing Ouyang

E-mail:ouyanghb@hust.edu.cn

CLC Number:

Yulei Rao, Hongbing Ouyang, Minchun Han, Zihong Wang. Research on the Contagion Mechanism of Bank Liquidity Risk from the Perspective of Macro Liquidity Tightening[J]. Chinese Journal of Management Science, 2025, 33(4): 24-35.

"

"

"

| 银行 | PAB | NBCB | SPDB | HXB | CMB | NJCB | CIB | BOB | ABC | BCM | ICBC | CEB | CCB | BOC | ECITIC |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| PAB | 0 | 0.12 | 0 | 0 | 0.47 | 0 | 0 | 0 | 0 | 0 | 0.27 | 0.05 | 0.04 | 0.05 | 0 |

| NBCB | 0.33 | 0 | 0.04 | 0.25 | 0 | 0 | 0 | 0 | 0 | 0 | 0.38 | 0 | 0 | 0 | 0 |

| SPDB | 0 | 0 | 0 | 0 | 0.64 | 0 | 0 | 0 | 0 | 0 | 0.36 | 0 | 0 | 0 | 0 |

| HXB | 0 | 0.41 | 0.24 | 0 | 0.18 | 0.05 | 0.08 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.05 |

| CMB | 0 | 0 | 0 | 0 | 0 | 0 | 0.19 | 0.17 | 0 | 0 | 0.07 | 0 | 0 | 0 | 0.56 |

| NJCB | 0 | 0 | 0 | 0 | 0 | 0 | 0.89 | 0 | 0 | 0 | 0 | 0 | 0.11 | 0 | 0 |

| CIB | 0 | 0 | 0 | 0 | 0.49 | 0.18 | 0 | 0 | 0 | 0.25 | 0.08 | 0 | 0 | 0 | 0 |

| BOB | 0 | 0 | 0 | 0.54 | 0.38 | 0 | 0 | 0 | 0 | 0 | 0 | 0.08 | 0 | 0 | 0 |

| ABC | 0 | 0.74 | 0 | 0.22 | 0 | 0 | 0 | 0 | 0 | 0 | 0.04 | 0 | 0 | 0 | 0 |

| BCM | 0 | 0 | 0 | 0.31 | 0 | 0.69 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| ICBC | 0.37 | 0.1 | 0.05 | 0.13 | 0.01 | 0 | 0 | 0.13 | 0.06 | 0.05 | 0 | 0 | 0 | 0 | 0.08 |

| CEB | 0 | 0.1 | 0 | 0 | 0 | 0 | 0.9 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| CCB | 0.18 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.82 | 0 | 0 | 0 | 0 |

| BOC | 0 | 0 | 0 | 0.65 | 0 | 0 | 0 | 0 | 0 | 0 | 0.35 | 0 | 0 | 0 | 0 |

| ECITIC | 0.26 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.74 | 0 | 0 | 0 | 0 | 0 | 0 |

"

(1) lnLiquidity | (2) lnLiquidity | |

|---|---|---|

| 0.4522*** | 0.2639* | |

| (3.7550) | (1.7093) | |

| sigma2_e | 0.0056*** | 0.0061*** |

| (6.9094) | (5.8949) | |

| 控制变量 | 是 | 是 |

| 个体固定效应 | 是 | 是 |

| N | 420 | 300 |

"

| 变量 | 时期1 | 时期2 |

|---|---|---|

| 0.4522 | 0.2639 | |

| (3.7550) | (1.7093) | |

| 1.8254 | 1.3585 |

"

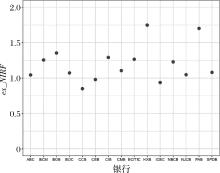

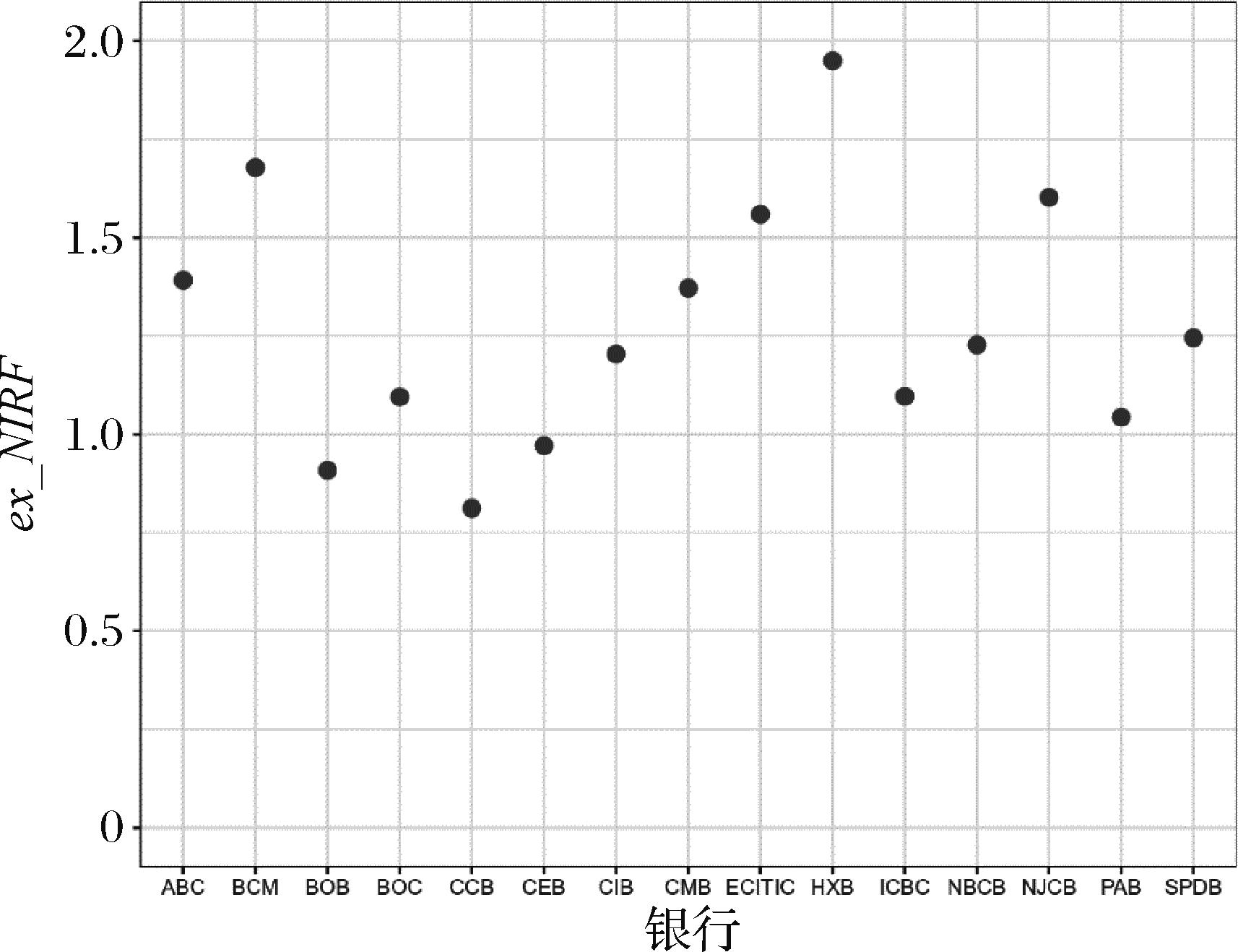

| 序号 | 时期1 | 时期2 | ||

|---|---|---|---|---|

| 银行 | NIRF | 银行 | NIRF | |

| 1 | HXB | 1.8696 | HXB | 2.1348 |

| 2 | PAB | 1.8208 | NJCB | 1.7402 |

| 3 | BOB | 1.4509 | BCM | 1.7273 |

| 4 | CIB | 1.3817 | ECITIC | 1.6486 |

| 5 | ECITIC | 1.3549 | CMB | 1.4649 |

| 6 | BCM | 1.3459 | ABC | 1.4302 |

| 7 | NBCB | 1.3128 | NBCB | 1.3322 |

| 8 | CMB | 1.1819 | SPDB | 1.2936 |

| 9 | SPDB | 1.1576 | CIB | 1.2593 |

| 10 | BOC | 1.1498 | ICBC | 1.1737 |

| 11 | NJCB | 1.1221 | PAB | 1.1245 |

| 12 | ABC | 1.1181 | BOC | 1.0818 |

| 13 | CEB | 1.0487 | CEB | 1.0226 |

| 14 | ICBC | 1.0015 | BOB | 0.9909 |

| 15 | CCB | 0.9116 | CCB | 0.8466 |

"

"

"

"

"

(1) 时期1 | (2) 时期2 | (3) 时期1 | (4) 时期2 | |

|---|---|---|---|---|

| 0.2952*** | 0.2292*** | 0.4979*** | 0.2511** | |

| (3.9144) | (3.4321) | (5.6142) | (2.1329) | |

| sigma2_e | 0.0042*** | 0.0049*** | 0.0049*** | 0.0059*** |

| (6.1041) | (12.2384) | (6.8314) | (6.9337) | |

| 控制变量 | 是 | 是 | 是 | 是 |

| 个体固定效应 | 是 | 是 | 是 | 是 |

| N | 420 | 300 | 420 | 300 |

| 1 | Diamond D W, Dybvig P H. Bank runs, deposit insurance, and liquidity[J]. Journal of Political Economy, 1983, 91(3): 401-419. |

| 2 | Allen F, Gale D. Optimal financial crises[J]. The Journal of Finance, 1998, 53(4): 1245-1284. |

| 3 | Blasques F, Bräuning F, Lelyveld I. A dynamic network model of the unsecured interbank lending market[J]. Journal of Economic Dynamics and Control, 2018, 90: 310-342. |

| 4 | Acharya V V, Yorulmazer T. Too many to fail:An analysis of time-inconsistency in bank closure policies[J]. Journal of Financial Intermediation, 2007, 16(1): 1-31. |

| 5 | 魏旭, 周伊敏. 流动性监管、系统性风险与社会福利——一个理论分析框架[J]. 经济学(季刊), 2022, 22(5): 1619-1638. |

| Wei X, Zhou Y M. The impacts of liquidity regulation on systemic risk in banking sector[J]. China Economic Quarterly, 2022, 22(5): 1619-1638. | |

| 6 | 童中文, 解晓洋, 邓熳利. 中国银行业系统性风险的“社会性消化”机制研究[J]. 经济研究, 2018, 53(2): 124-139. |

| Tong Z W, Xie X Y, Deng M L. A study on the social-digestion mechanism of banks’systemic risk in China[J]. Economic Research Journal, 2018, 53(2): 124-139. | |

| 7 | Denbee E, Julliard C, Li Y, et al. Network risk and key players: A structural analysis of interbank liquidity[J]. Journal of Financial Economics, 2021, 141(3): 831-859. |

| 8 | Freixas X, Parigi B M, Rochet J C. Systemic risk, interbank relations, and liquidity provision by the central bank[J]. Journal of Money, Credit and Banking, 2000, 32(3): 611-638. |

| 9 | Angelini P, Maresca G, Russo D. Systemic risk in the netting system[J]. Journal of Banking & Finance, 1996, 20(5): 853-868. |

| 10 | Furfine C H. Interbank exposures: Quantifying the risk of contagion[J]. Journal of Money, Credit and Banking, 2003, 35(1): 111-128. |

| 11 | Upper C, Worms A. Estimating bilateral exposures in the German interbank market: Is there a danger of contagion?[J]. European Economic Review, 2004, 48(4): 827-849. |

| 12 | 马君潞, 范小云, 曹元涛. 中国银行间市场双边传染的风险估测及其系统性特征分析[J]. 经济研究, 2007(1): 68-78+142. |

| Ma J L, Fan X Y, Cao Y T. Estimating bilateral exposures in the China interbank market:ls there a systemic contagion?[J]. Economic Research Journal, 2007(1): 68-78+142. | |

| 13 | 唐振鹏, 谢智超, 冉梦, 等. 网络视角下我国上市银行间市场系统性风险实证研究[J]. 中国管理科学, 2016, 24(S1): 489-494. |

| Tang Z P, Xie Z C, Ran M, et al. Systemic risk empiricalstudy of China listed bank market under the network perspective[J]. Chinese Journal of Management Science, 2016, 24(S1): 489-494. | |

| 14 | 杨海军, 胡敏文. 基于核心-边缘网络的中国银行风险传染[J]. 管理科学学报, 2017, 20(10): 44-56. |

| Yang H J, Hu M W. Risk contagion of Chinese interbank markets based on core-periphery network[J]. Journal of Management Sciences in China, 2017, 20(10): 44-56. | |

| 15 | 陈暮紫, 汤婧, 张小溪, 等. 信用和流动风险冲击下的中国银行业传染分析[J]. 系统工程理论与实践, 2021, 41(6): 1412-1427. |

| Chen M Z, Tang J, Zhang X X, et al. Contagion analysis of China’s banking industry under the impact of credit and liquidity risk[J]. Systems Engineering-Theory & Practice, 2021, 41(6): 1412-1427. | |

| 16 | Anand K, Craig B, Von Peter G. Filling in the blanks: Network structure and interbank contagion[J]. Quantitative Finance, 2015, 15(4): 625-636. |

| 17 | Fan H, Liu R. Research on financial systemic risk in ASEAN region[J]. Entropy, 2021, 23(9): 1131. |

| 18 | 范小云, 荣宇浩, 王博. 我国系统重要性银行评估:网络层次结构视角[J]. 管理科学学报, 2021, 24(2): 48-74. |

| Fan X Y, Rong Y H, Wang B. Identifying systemically important banks in China: A network hierarchy structure perspective[J]. Journal of Management Sciences in China, 2021, 24(2): 48-74. | |

| 19 | 严冠, 刘志东. 基于贝叶斯方法的中国商业银行同业借贷网络中系统风险研究[J]. 中国管理科学, 2020, 28(4): 14-26. |

| Yan G, Liu Z D. Systemic risk in China’s interbank liability networks based on the bayesian methodology[J]. Chinese Journal of Management Science, 2020, 28(4): 14-26. | |

| 20 | Acemoglu D, Ozdaglar A, Tahbaz-Salehi A. Systemic risk and stability in financial networks[J]. American Economic Review, 2015, 105(2): 564-608. |

| 21 | Glasserman P, Young H P. How likely is contagion in financial networks?[J]. Journal of Banking & Finance, 2015, 50: 383-399. |

| 22 | 范小云, 王道平, 刘澜飚. 规模、关联性与中国系统重要性银行的衡量[J]. 金融研究, 2012(11): 16-30. |

| Fan X Y, Wang D P, Liu L B. The SIFIS: “Too Big to Fail” or “Too Connected To Fail”-An analysis of China’s banking sector[J]. Journal of Financial Research, 2012(11): 16-30. | |

| 23 | 高国华, 潘英丽. 基于资产负债表关联的银行系统性风险研究[J]. 管理工程学报, 2012, 26(4): 162-168. |

| Gao G H, Pan Y L. Financial interlinkages and contagion risk in the interbank market in China[J]. Journal of Industrial Engineering and Engineering Management, 2012, 26(4): 162-168. | |

| 24 | 贾彦东. 金融机构的系统重要性分析——金融网络中的系统风险衡量与成本分担[J]. 金融研究, 2011(10): 17-33. |

| Jia Y D. Measuring the systemic importance of financial institutions:Methodology and policy applications[J]. Journal of Financial Research, 2011(10): 17-33. | |

| 25 | Furfine C H. The microstructure of the federal funds market[J]. Financial Markets, Institutions & Instruments, 1999, 8(5): 24-44. |

| 26 | 傅强, 石泽龙. 系统性金融风险的联合网络关联度测量及频率研究——基于局部平稳的非参数时变VHAR模型[J]. 中国管理科学, 2024, 32(2): 1-10. |

| Fu Q, Shi Z L. Research on frequency of the joint network connectedness of systemic financial risks in China based on the locally stationary non-parametric time-varying vector HAR model[J]. Chinese Journal of Management Science, 2024, 32(2): 1-10. | |

| 27 | Affinito M. Do interbank customer relationships exist?And how did they function in the crisis?Learning from Italy[J]. Journal of Banking & Finance, 2012, 36(12): 3163-3184. |

| 28 | Williamson O E. Transaction cost economics: The natural progression[J].American Economic Review, 2010, 100(3): 673-690. |

| 29 | Furfine C H. Banks as monitors of other banks: Evidence from the overnight federal funds market[J]. The Journal of Business, 2001, 74(1): 33-57. |

| 30 | Chiu J, Eisenschmidt J, Monnet C. Relationships in the interbank market[J]. Review of Economic Dynamics, 2020, 35: 170-191. |

| 31 | Ashcraft A B, Duffie D. Systemic illiquidity in the federal funds market[J]. American Economic Review, 2007, 97(2): 221-225. |

| 32 | Cocco J F, Gomes F J, Martins N C. Lending relationships in the interbank market[J]. Journal of Financial Intermediation, 2009, 18(1): 24-48. |

| 33 | Bräuning F, Fecht F. Relationship lending in the interbank market and the price of liquidity[J]. Review of Finance, 2017, 21(1): 33-75. |

| 34 | Ballester C, Calvó-Armengol A, Zenou Y. Who’s who in networks. Wanted: The key player[J]. Econometrica, 2006, 74(5): 1403-1417. |

| 35 | Calvó-Armengol A, Patacchini E, Zenou Y.Peer effects and social networks in education[J]. The Review of Economic Studies, 2009, 76(4): 1239-1267. |

| 36 | 朱平芳, 张征宇, 姜国麟. FDI与环境规制:基于地方分权视角的实证研究[J]. 经济研究, 2011, 46(6): 133-145. |

| Zhu P F, Zhang Z Y, Jiang G L. Empirical study of the relationship between FDI and environmental regulation: An intergovernmental competition perspective[J]. Economic Research Journal, 2011, 46(6): 133-145. | |

| 37 | 潘彬,王去非,易振华.同业业务、流动性波动与中央银行流动性管理[J].经济研究,2018,53(6):21-35. |

| Pan B, Wang Q F, Yi Z H. Interbank business, liquidity fluctuation and central bank liquidity management[J].Economic Research Journal, 2018, 53(6):21-35. | |

| 38 | 田国强,李双建.经济政策不确定性与银行流动性创造:来自中国的经验证据[J].经济研究,2020,55(11):19-35. |

| Tian G Q, Li S J. Economic policy uncertainty and the creation of bank liquidity:Empirical[J].Economic Research Journal,2020,55(11):19-35. |

| [1] | SHI Yu-shan, LIU Hai-long, HU You-qun. Optimal Pricing Model of Stock Loan-to-value Ratio Considering Liquidity Risk and Portfolio Rebalancing Risk [J]. Chinese Journal of Management Science, 2018, 26(1): 81-89. |

| [2] | HUANG Qi, TAO Jian-ping, ZHANG Hong-mei. Market Structure of Agricultural Insurance, Spatial Dependence and Agricultural Insurance Conditional Convergence [J]. Chinese Journal of Management Science, 2017, 25(5): 25-32. |

| [3] | SU Xin, ZHOU Yong. Liquidity, Liquidity Risk and Performance——A Empirical Study on Chinese Open-End Mutual Funds [J]. Chinese Journal of Management Science, 2015, 23(7): 1-9. |

| [4] | ZHOU Fang, ZHANG Wei, ZHOU Bing. Capital Asset Pricing Model Based on Liquidity Risk [J]. Chinese Journal of Management Science, 2013, 21(5): 1-7. |

| [5] | CUI Chang-feng, LIU Hai-long. The Pricing of Defaultable Bond Based on Claim Termination [J]. Chinese Journal of Management Science, 2012, (4): 8-17. |

| [6] | LI Yan-ni, RAN Mao-sheng. The Study of Commercial Bank Liquidity Risk Management Method and Improvement——Application of Dynamic Programs with Simple Recourse Under Fuzzy Qualitative Constraints [J]. Chinese Journal of Management Science, 2011, 19(3): 19-25. |

| [7] | WANG Ming-tao, ZHUANG Ya-ming. New Models for Measuring the Liquidity Risk of Stocks [J]. Chinese Journal of Management Science, 2011, 19(2): 1-9. |

| [8] | XIAO Yuan, HU Xiao-ping, DANG Feng-shun. Research on the Model of Risk Measurement in China’s Open-end Fund Market [J]. Chinese Journal of Management Science, 2009, 17(6): 25-32. |

| [9] | HAN Guo-wen, YANG Wei. A New Model and Its Tests for Measuring the Liquidity Risk of Stocks [J]. Chinese Journal of Management Science, 2008, 16(2): 1-6. |

| [10] | LUO Deng-yue, WANG Chun-feng, FANG Zhen-ming. An Empirical Research on the Relationship between Aggregate Liquidity and Asset Pricing in China Stock Market [J]. Chinese Journal of Management Science, 2007, 15(2): 33-38. |

| [11] | ZHU Xiao-bin. Measuring Model of Stock Investment Portfolio’s Liquidity Risk:Construction and Test [J]. Chinese Journal of Management Science, 2007, 15(1): 6-11. |

| [12] | LU Jing, TANG Xiao-wo. The Empirical Study on Multi-Factor Pricing Model Based on Liquidity Risk [J]. Chinese Journal of Management Science, 2006, (5): 45-51. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||