主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (5): 1-12.doi: 10.16381/j.cnki.issn1003-207x.2021.0521

Chao Liu( ), Fengfeng Gao, Mengwan Zhang, Qiwei Xie

), Fengfeng Gao, Mengwan Zhang, Qiwei Xie

Received:2021-03-07

Revised:2021-08-25

Online:2025-05-25

Published:2025-06-04

Contact:

Chao Liu

E-mail:liuchao@bjut.edu.cn

CLC Number:

Chao Liu, Fengfeng Gao, Mengwan Zhang, Qiwei Xie. Research on Risk Spillover Effect, Impact Effect and Risk Early Warning in China's Financial Market[J]. Chinese Journal of Management Science, 2025, 33(5): 1-12.

"

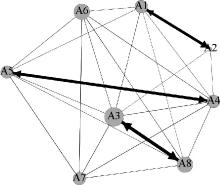

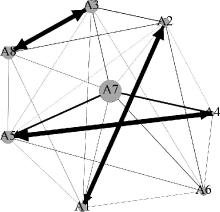

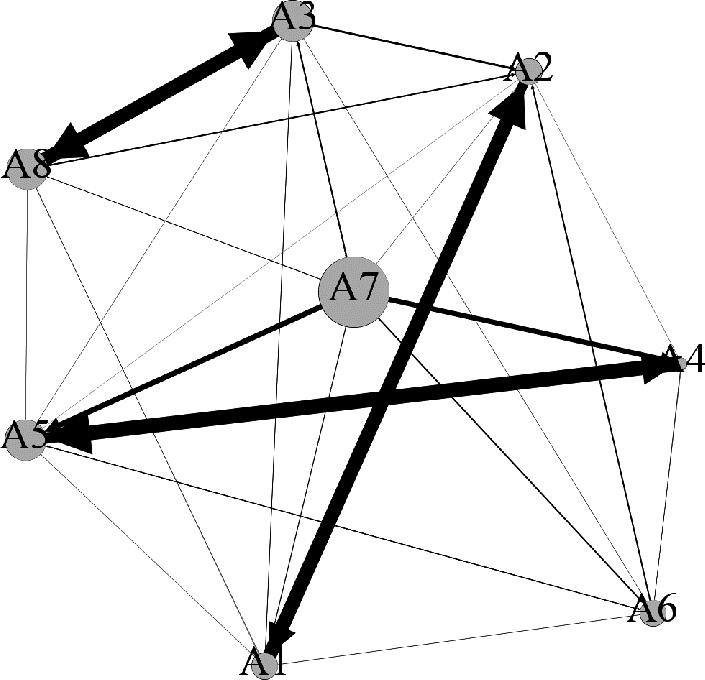

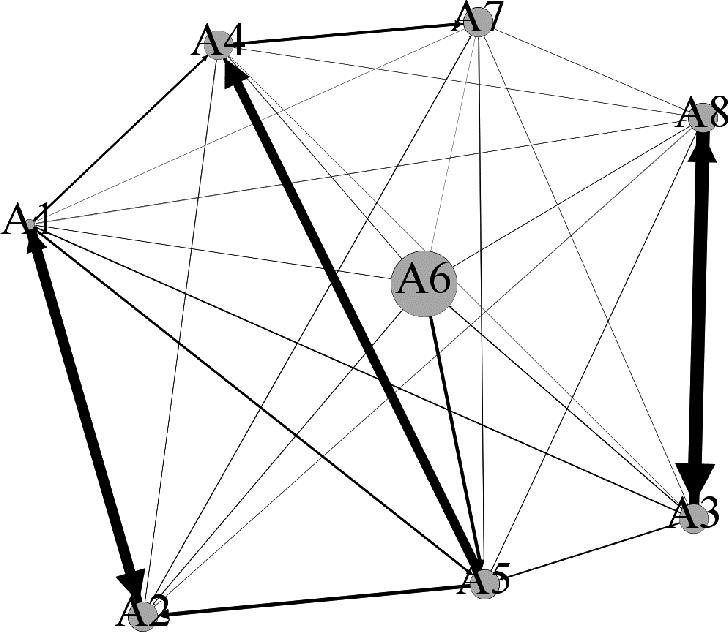

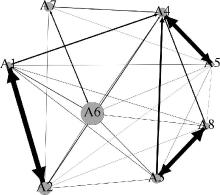

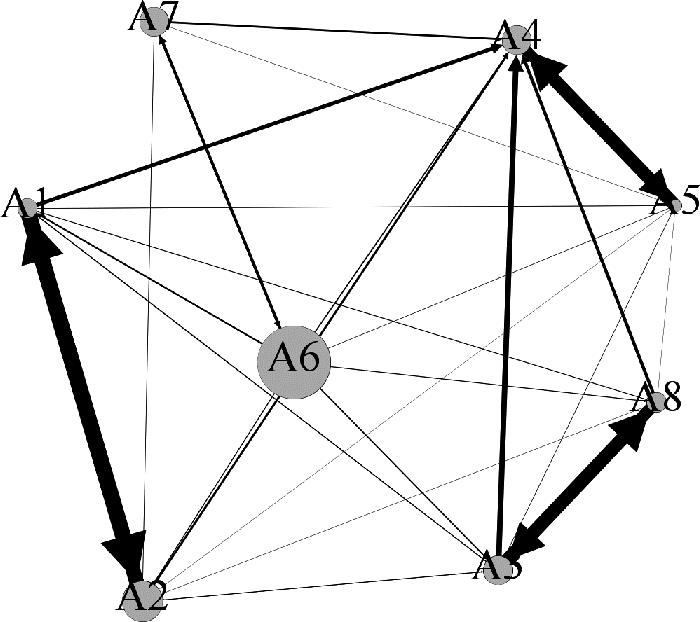

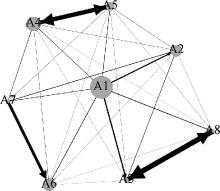

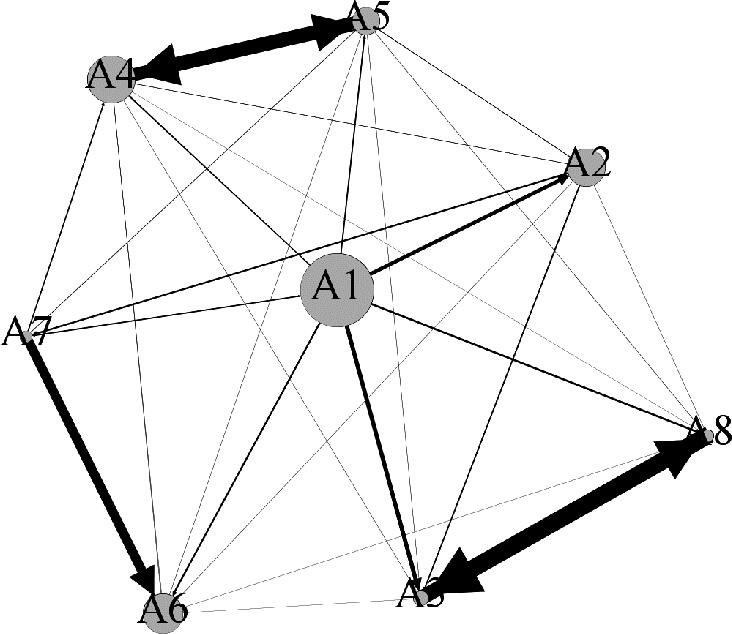

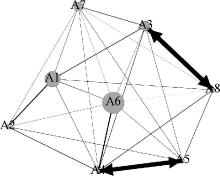

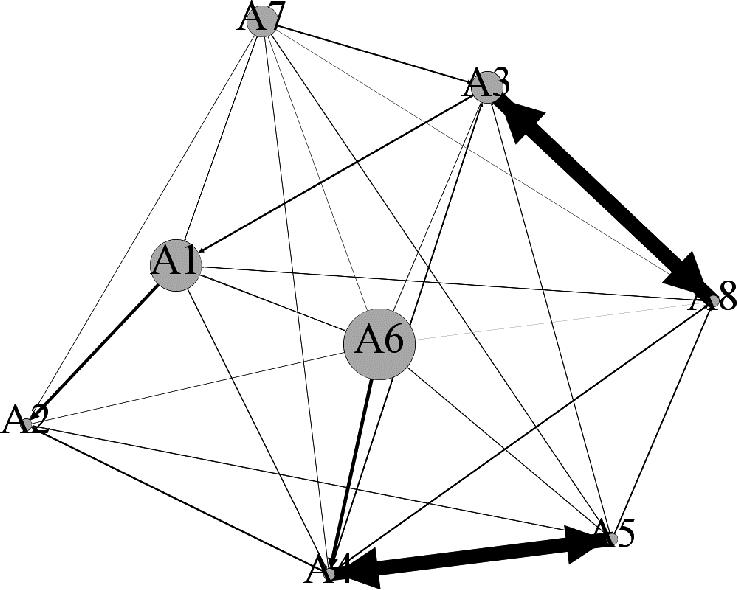

| 一级子市场 | 二级子市场 | 三级子市场 | 代理变量 | 单位 |

|---|---|---|---|---|

| 货币市场 | 同业拆借市场 | — | 银行间7天同业拆借利率(A1) | % |

| 回购市场 | — | 银行间7天加权回购利率(A2) | % | |

| 资本市场 | 股票市场 | — | 沪深300指数 (A3) | — |

| 债券市场 | 银行间债券市场 | 中债综合净价指数 (A4) | — | |

| 交易所债券市场 | 中债国债净价指数(A5) | — | ||

| 外汇市场 | — | — | 中间价美元兑换人民币(A6) | — |

| 黄金市场 | — | — | AU9995黄金现货价格(A7) | 元/克 |

| 房地产市场 | — | — | 房地产板块指数 (A8) | — |

"

| 市场 | A1 | A2 | A3 | A4 | A5 | A6 | A7 | A8 | ||

|---|---|---|---|---|---|---|---|---|---|---|

| 货币市场 | A1 | 60.797 | 28.478 | 1.767 | 2.275 | 2.389 | 1.592 | 1.253 | 1.449 | 39.203 |

| A2 | 23.743 | 69.116 | 0.973 | 1.77 | 1.391 | 0.938 | 0.95 | 1.119 | 30.884 | |

| 资本市场 | A3 | 2.643 | 1.856 | 52.331 | 3.011 | 2.154 | 1.825 | 2.28 | 33.9 | 47.669 |

| A4 | 1.275 | 1.033 | 1.601 | 62.841 | 26.919 | 2.432 | 2.081 | 1.817 | 37.159 | |

| A5 | 1.412 | 1.411 | 1.861 | 29.301 | 60.194 | 1.523 | 2.66 | 1.638 | 39.806 | |

| 外汇市场 | A6 | 1.638 | 1.309 | 1.935 | 2.753 | 2.35 | 84.063 | 3.467 | 2.486 | 15.937 |

| 黄金市场 | A7 | 1.398 | 1.116 | 1.802 | 3.516 | 3.187 | 3.796 | 83.222 | 1.962 | 16.778 |

| 房地产市场 | A8 | 1.808 | 1.343 | 33.496 | 2.467 | 2.001 | 1.673 | 1.993 | 55.219 | 44.781 |

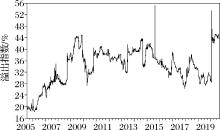

| 33.918 | 36.547 | 43.435 | 45.092 | 40.391 | 13.779 | 14.684 | 44.371 | 34.027 | ||

| -5.284 | 5.663 | -4.235 | 7.933 | 0.585 | -2.158 | -2.093 | -0.411 | |||

"

"

"

"

"

"

"

"

"

"

"

"

| 模型 | MSE | MAE | MAPE |

|---|---|---|---|

| DBNS | 0.015 | 0.089 | 0.520 |

| RBM | 0.029 | 0.170 | 1.366 |

| BP | 0.030 | 0.172 | 1.242 |

"

| 宏观经济景气一致指数 | 消费者预期指数 | 网络结构 | |

|---|---|---|---|

系数 (标注误差) | -0.271*** (0.053) | -0.199*** (0.036) | 8.267 (19.464) |

z值 p值 | -5.142 (0.000) | -5.549 (0.000) | 0.425 (0.671) |

| 1 | Kaewkheaw M, Leeahtam P C, Chaiboosri. An analysis of relationship between gold price and US dollar index by using bivariate extreme value copulas[J]. Advances in Intelligent Systems and Computing, 2014(251): 455-462. |

| 2 | 周爱民, 韩菲. 股票市场和外汇市场间风险溢出效应研究——基于GARCH-时变Copula-CoVaR模型的分析[J]. 国际金融研究, 2017(11): 54-64. |

| Zhou A M, Han F. Research on the risk spillovers between stock and exchange rate market——Based on the GARCH-TVP Copula-CoVaR model[J]. Studies of International Finance, 2017(11): 54-64. | |

| 3 | 刘超.系统科学金融理论[M].北京:科学出版社,2013. |

| Liu C. The financial theory of systems science[M].Beijing: Science Press, 2013. | |

| 4 | 刘超, 徐君慧, 周文文. 中国金融市场的风险溢出效应研究——基于溢出指数和复杂网络方法[J]. 系统工程理论与实践, 2017,37(4): 831-842. |

| Liu C, Xu J H, Zhou W W. Study on risk spillover effect of financial markets in China based on methods of spillover index and complex network[J]. Systems Engineering-Theory & Practice,2017,37(4): 831-842. | |

| 5 | 宫晓莉, 熊熊, 张维. 我国金融机构系统性风险度量与外溢效应研究[J]. 管理世界, 2020,36(8): 65-83. |

| Gong X L, Xiong X, Zhang W. Research on systemic risk measurement and spillover effect of financial institutions in China[J]. Management World, 2020,36(8): 65-83. | |

| 6 | Yartey, A C. The institutional and macroeconomic determinants of stock market development in emerging economies[J]. Applied Financial Economics, 2010,20(21): 1615-1625. |

| 7 | 钟婉玲,李海奇,杨胜刚.国际油价、宏观经济变量与中国股市的尾部风险溢出效应研究[J].中国管理科学,2022,30(2):27-37. |

| Zhong W L, Li H W, Yang S G. Tail risk spillover effects among crude oil price, macroeconomic variables and China’s stock market[J]. Chinese Journal of Management Science,2022,30(2):27-37. | |

| 8 | Giglio S, Kelly B T, Pruitt S, et al. Systemic risk and the macroeconomy:An empirical evaluation[J]. Journal of Financial Economics, 2016,119(3):457-471. |

| 9 | 邓创, 张甜, 徐曼, 等. 中国金融市场风险与宏观经济景气之间的关联动态研究[J]. 南方经济, 2018(4): 1-19. |

| Deng C, Zhang T, Xu M, et al. The dynamic association between financial market risk and business cycle in China[J]. South China Journal of Economics, 2018(4): 1-19. | |

| 10 | Śmiech S, Papież M, Shahzad S J H. Spillover among financial, industrial and consumer uncertainties. The case of EU member states[J]. International Review of Financial Analysis, 2020,70:101497. |

| 11 | 欧阳资生,杨希特,黄颖.嵌入网络舆情指数的中国金融机构系统性风险传染效应研究[J].中国管理科学,2022,30(4):1-12. |

| Ouyang Z S, Yang X T, Huang Y. Research on systemic risk contagion effect of Chinese financial institutions considering network public opinion index[J]. Chinese Journal of Management Science,2022,30(4):1-12. | |

| 12 | 张一, 惠晓峰, 吴宝秀. 宏观经济信息发布对国际金融危机传染效应的影响研究[J]. 管理评论, 2017,29(4):3-11+24. |

| Zhang Y, Hui X F, Wu B X. The effect of macroeconomic news on financial crisis contagion[J]. Management Review, 2017,29(4):3-11+24. | |

| 13 | 方意, 陈敏, 杨嬿平. 金融市场对银行业系统性风险的溢出效应及渠道识别研究[J]. 南开经济研究, 2018(5): 58-75. |

| Fang Y, Chen M, Yang Y P. The spillover effect and channel identification of financial market to banking systemic risk[J]. Nankai Economic Studies, 2018(5): 58-75. | |

| 14 | 王春丽, 胡玲. 基于马尔科夫区制转移模型的中国金融风险预警研究[J]. 金融研究, 2014(9): 99-114. |

| Wang C L, Hu L. An empirical research on early-warming of financial risk in China[J]. Journal of Financial Research, 2014(9): 99-114. | |

| 15 | Li J S, Ng A C Y, Chan W S. Managing financial risk in Chinese stock markets: Option pricing and modeling under a multivariate threshold autoregression[J]. International Review of Economics & Finance, 2015,40: 217-230. |

| 16 | Zhao J, Yang Z J, Xu Y T. Nonparallel least square support vector machine for classification[J]. Applied Intelligence, 2016,45(4):1119-1128. |

| 17 | Ince H, Cebeci A F, Imamoglu S Z. An artificial neural network-based approach to the monetary model of exchange rate[J]. Computational Economics, 2019, 53(2):817-831. |

| 18 | Chatzis S P, Siakoulis V, Petropoulos A, et al. Forecasting stock market crisis events using deep and statistical machine learning techniques[J]. Expert Systems With Applications, 2018,112: 353-371. |

| 19 | Huang A, Qiu L, Li Z. Applying deep learning method in TVP-VAR model under systematic financial risk monitoring and early warning[J]. Journal of Computational and Applied Mathematics, 2021,382: 113065. |

| 20 | Diebold F X, Yilmaz K. Better to give than to receive: Predictive directional measurement of volatility spillovers[J]. International Journal of Forecasting, 2012,28(1):57-66. |

| 21 | 张晓朴. 金融风险研究:演进、成因与监管[J]. 国际金融研究, 2010(7): 58-67. |

| Zhang X P. A study on systemic financial risk: Evolution, causes and supervision[J]. Studies of International Finance, 2010(7): 58-67. |

| [1] | Zhongyi Hu, Diancheng Shui, Jiang Wu. Measurement and Evolution of Digitization Level of Chinese Listed Companies: Empirical Evidence from Annual Report Text [J]. Chinese Journal of Management Science, 2025, 33(4): 36-49. |

| [2] | Xin Li, Xu Zhang, Lean Yu, Shouyang Wang. Enhancing Short-term Tourist Flow Forecasting and Evaluation Using an Improved Transformer Framework [J]. Chinese Journal of Management Science, 2025, 33(2): 105-117. |

| [3] | Jiang-ze DU,Xi-zhuo CHEN,Le-an YU. Can Executives with IT Background Promote FinTech Innovation? [J]. Chinese Journal of Management Science, 2023, 31(12): 69-78. |

| [4] | Dong-xiao NIU,Zhuo-ya SIQIN,Dong-yu WANG,Xiao-min XU,Huan-fen ZHANG. Method and Application of Multi-value Chain Collaborative Data Mining in Power Equipment Enterprises Based on Deep Learning [J]. Chinese Journal of Management Science, 2023, 31(11): 321-331. |

| [5] | OUYANG Yan-min, WANG Chang-feng, LIU Liu, YUAN Hong-min. Study on the Risk Early Warning Interval Model Based on Improved Adaptive Optimal Partition Method——Large-scale Public Health Emergency [J]. Chinese Journal of Management Science, 2022, 30(11): 196-206. |

| [6] | OUYANG Hong-bing, HUANG Kang, YAN Hong-ju. Prediction of Financial Time Series Based on LSTM Neural Network [J]. Chinese Journal of Management Science, 2020, 28(4): 27-35. |

| [7] | LI Ling, DING Shuai, LI Xiao-jian, YANG Shan-lin. Research on Smart Decision-Making Method for Upper Gastrointestinal Diseases Based on Electronic Gastroscopic Video [J]. Chinese Journal of Management Science, 2019, 27(11): 211-216. |

| [8] | KONG Fan-hui, LI Jian. Resilient Operation and Promotion Strategy of OEM Supply Chain under Supply Disruption Risk [J]. Chinese Journal of Management Science, 2018, 26(2): 152-159. |

| [9] | WANG Zeng-wen. Analysis of Balanced Portfolio Strategy and Determinants on China's Social Security Fund under the New Normal Economic State——Based on the Comparison of Shanghai and Shenzhen [J]. Chinese Journal of Management Science, 2017, 25(8): 30-38. |

| [10] | XIONG Zheng de, HAN Li jun. An Empirical Study on the Volatility Spillover Effect between Financial Markets——GC-MSV Model and Application [J]. Chinese Journal of Management Science, 2013, (2): 32-41. |

| [11] | LIN Yu. Study on Dynamic VaR Measurement with Hyperbolic Memory GARCH [J]. Chinese Journal of Management Science, 2011, 19(6): 15-24. |

| [12] | CHAI Shang-lei, GUO Chong-hui, SU Mu-ya. Volatility Spillover from International Stock Index Futures and Spot Markets to Chinese Stock Market Based on ICA Model [J]. Chinese Journal of Management Science, 2011, 19(3): 11-18. |

| [13] | LI Hong-quan, WANG Shou-yang, MA Chao-qun. What’s the Nature of Volatility in Stock Prices?——Based on the Nonlinear Dynamical Analysis Principle [J]. Chinese Journal of Management Science, 2008, 16(5): 1-8. |

| [14] | ZHANG Rui-feng, ZHANG Shi-ying, TANG Yong. The Volatility Spillover Analysis and Empirical Study of the Financial Markets [J]. Chinese Journal of Management Science, 2006, (5): 14-22. |

| [15] | JIA Xiao-xia, YANG Nai-ding, JIANG Ji-jiao. Identification and Early Warning Study on Investment Regional Risks of Projects [J]. Chinese Journal of Management Science, 2004, (3): 48-53. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||