主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (2): 232-241.doi: 10.16381/j.cnki.issn1003-207x.2020.2458

Previous Articles Next Articles

Mengdie Zhao, Changjun Wang( ), Saiyu Zhou

), Saiyu Zhou

Received:2020-12-25

Revised:2022-08-24

Online:2025-02-25

Published:2025-03-06

Contact:

Changjun Wang

E-mail:cjwang@dhu.edu.cn

CLC Number:

Mengdie Zhao, Changjun Wang, Saiyu Zhou. Scarce Price and Demand Data Driven Risk-averse Newsvendor Decisions[J]. Chinese Journal of Management Science, 2025, 33(2): 232-241.

"

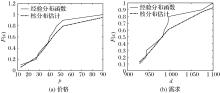

| No. | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| x | 46.64 | 38.58 | 43.69 | 12.61 | 29.21 | 89.86 | 33.49 | 27.41 | 39.99 | 52.62 |

| y | 944.2 | 996.7 | 982.8 | 1076 | 995.2 | 927.6 | 1211.7 | 1102 | 964.3 | 943.3 |

"

"

"

"

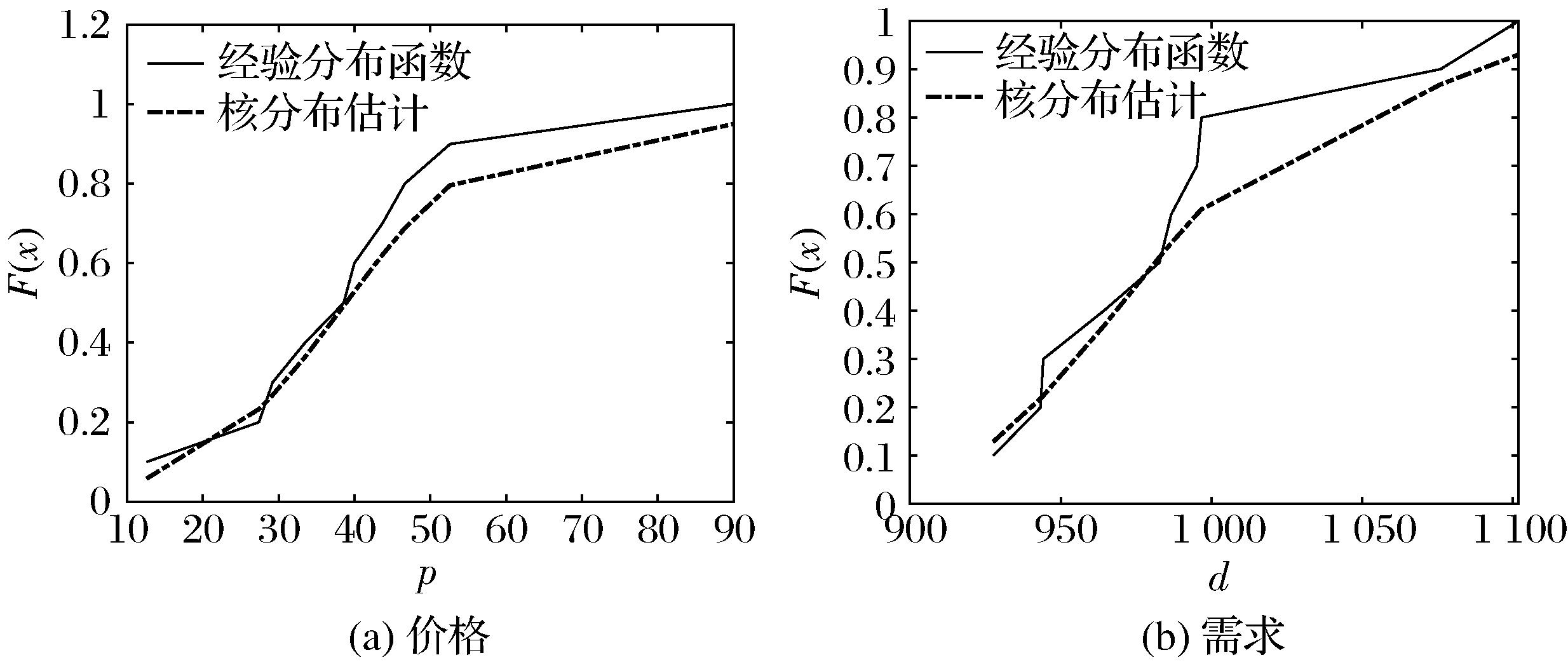

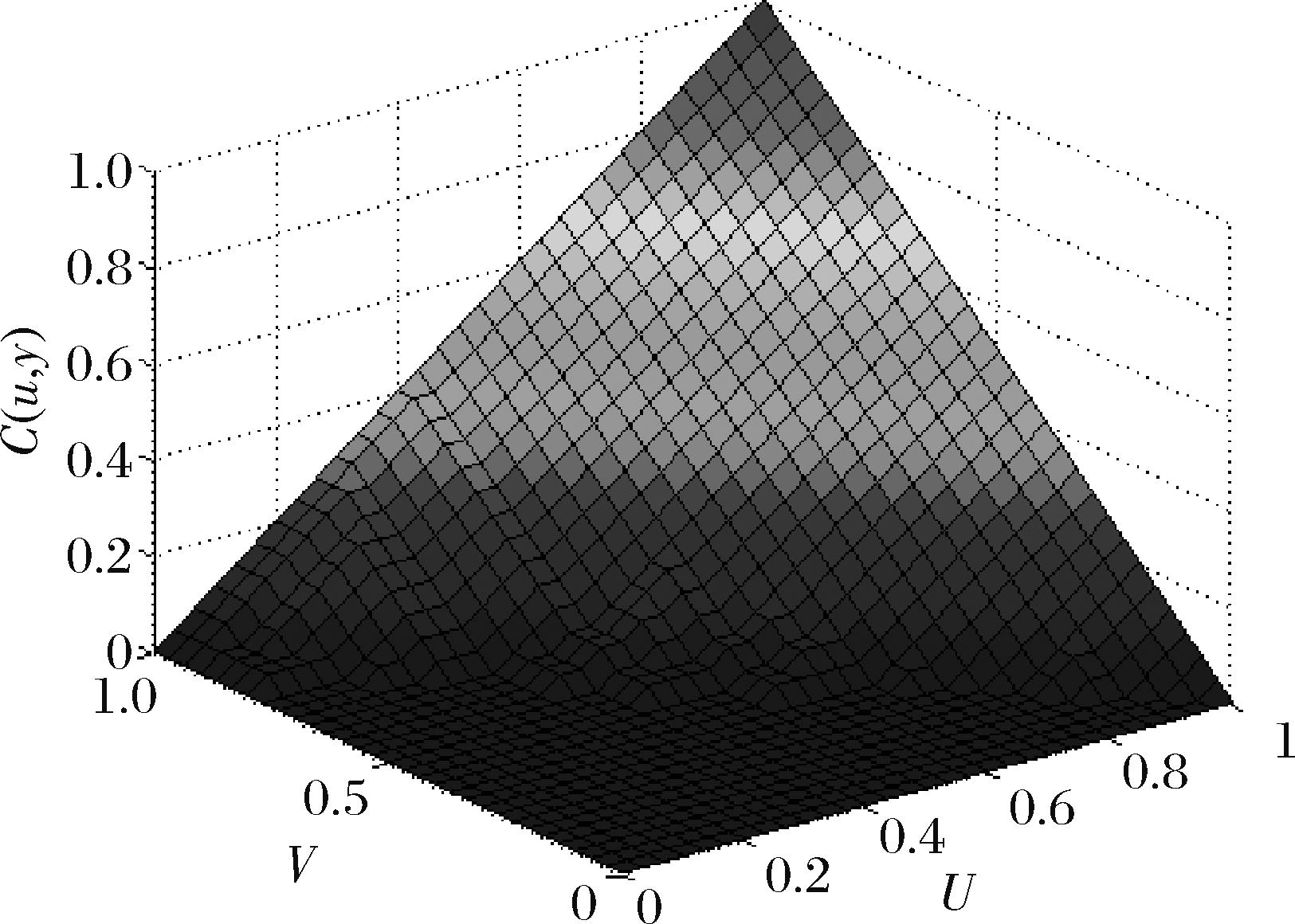

| 正态-Copula | t-Copula | Frank-Copula | |

|---|---|---|---|

| d2 | 0.0078 | 0.0111 | 0.0114 |

"

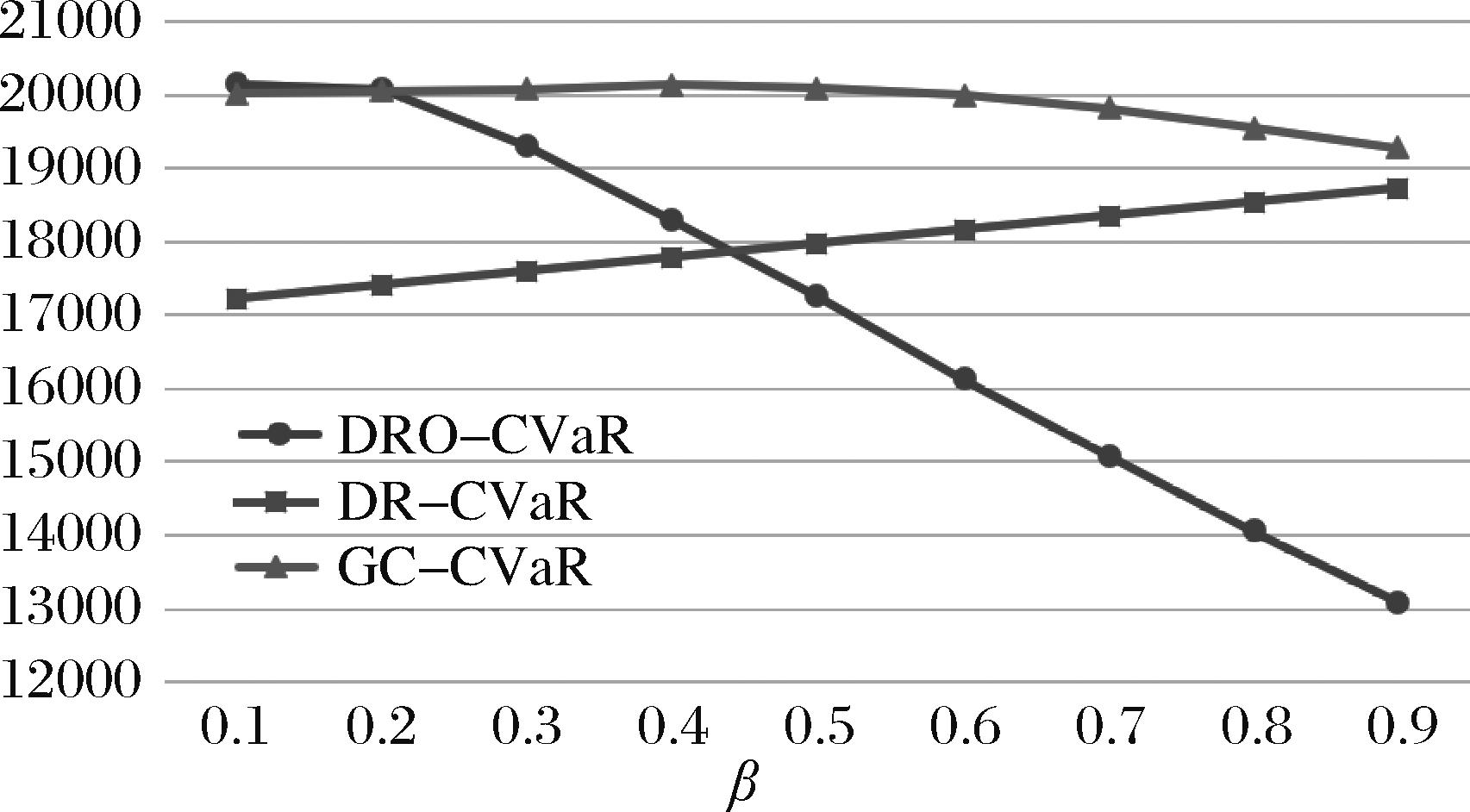

| DRO-CVaR | RC-CVaR | GC-CVaR | |

|---|---|---|---|

| 0.1 | 967.08 | 1000.78 | 1206.35 |

| 0.2 | 939.39 | 988.28 | 1193.85 |

| 0.3 | 901.96 | 975.78 | 1181.35 |

| 0.4 | 854.74 | 963.28 | 1168.85 |

| 0.5 | 806.12 | 950.78 | 1156.35 |

| 0.6 | 753.61 | 938.28 | 1143.85 |

| 0.7 | 704.52 | 925.78 | 1131.35 |

| 0.8 | 656.82 | 913.28 | 1118.85 |

| 0.9 | 611.30 | 900.78 | 1106.35 |

"

"

| 分布 | 正态分布 | Gamma分布 | 均匀分布 |

|---|---|---|---|

| 参数 |

"

| 模型 | β | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 正态 | Gamma | 均匀 | 正态(%) | Gamma(%) | 均匀(%) | ||||||

| DRO-CVaR | 0.1 | 967.08 | 20151.91 | 14643.03 | 9085.81 | 12559.81 | 12096.22 | -27.34 | -54.91 | -37.67 | 39.97 |

| 0.2 | 939.39 | 20087.79 | 14527.36 | 9100.97 | 12590.71 | 12073.01 | -27.68 | -54.69 | -37.32 | 39.90 | |

| 0.3 | 901.96 | 19311.00 | 13803.77 | 8887.22 | 12496.25 | 11729.08 | -28.52 | -53.98 | -35.29 | 39.26 | |

| 0.4 | 854.74 | 18299.89 | 13121.97 | 8633.99 | 12318.6 | 11358.19 | -28.29 | -52.82 | -32.68 | 37.93 | |

| 0.5 | 806.12 | 17258.99 | 12420.08 | 8168.58 | 12076.16 | 10888.27 | -28.04 | -52.67 | -30.03 | 36.91 | |

| 0.6 | 753.61 | 16134.85 | 11653.48 | 7588.29 | 11619.31 | 10287.03 | -27.77 | -52.97 | -27.99 | 36.24 | |

| 0.7 | 704.52 | 15083.79 | 10894.35 | 7093.97 | 10935.70 | 9641.34 | -27.77 | -52.97 | -27.50 | 36.08 | |

| 0.8 | 656.82 | 14062.52 | 10156.73 | 6613.66 | 10195.28 | 8988.56 | -27.77 | -52.97 | -27.50 | 36.08 | |

| 0.9 | 611.30 | 13087.98 | 10156.73 | 6155.33 | 9488.744 | 8600.27 | -22.40 | -52.97 | -27.50 | 34.29 | |

| RC-CVaR | 0.1 | 1000.78 | 17232.43 | 13420.97 | 6417.91 | 10716.71 | 10185.20 | -22.12 | -62.76 | -37.81 | 40.90 |

| 0.2 | 988.28 | 17419.93 | 13613.39 | 6605.41 | 10888.25 | 10369.02 | -21.85 | -62.08 | -37.50 | 40.48 | |

| 0.3 | 975.78 | 17607.43 | 13735.59 | 6792.91 | 11051.86 | 10526.79 | -21.99 | -61.42 | -37.23 | 40.21 | |

| 0.4 | 963.28 | 17794.93 | 13869.59 | 6980.41 | 11215.46 | 10688.49 | -22.06 | -60.77 | -36.97 | 39.94 | |

| 0.5 | 950.78 | 17982.43 | 13963.49 | 7158.28 | 11369.80 | 10830.52 | -22.35 | -60.19 | -36.77 | 39.77 | |

| 0.6 | 938.28 | 18169.93 | 14137.03 | 7330.26 | 11521.39 | 10996.23 | -22.20 | -59.66 | -36.59 | 39.48 | |

| 0.7 | 925.78 | 18357.43 | 14252.18 | 7502.24 | 11672.98 | 11142.47 | -22.36 | -59.13 | -36.41 | 39.30 | |

| 0.8 | 913.28 | 18544.93 | 14351.18 | 7673.65 | 11809.66 | 11278.16 | -22.61 | -58.62 | -36.32 | 39.18 | |

| 0.9 | 900.78 | 18732.43 | 14447.53 | 7834.08 | 11939.68 | 11407.10 | -22.87 | -58.18 | -36.26 | 39.11 | |

| GC-CVaR | 0.1 | 1206.35 | 20031.81 | 14779.13 | 9120.16 | 8180.10 | 10693.13 | -26.22 | -54.47 | -59.16 | 46.62 |

| 0.2 | 1193.85 | 20065.02 | 14770.59 | 9094.12 | 8291.30 | 10718.67 | -26.39 | -54.68 | -58.68 | 46.58 | |

| 0.3 | 1181.35 | 20084.28 | 14755.99 | 9081.54 | 8351.24 | 10729.59 | -26.53 | -54.78 | -58.42 | 46.58 | |

| 0.4 | 1168.85 | 20146.46 | 14607.07 | 9076.25 | 8328.66 | 10670.66 | -27.50 | -54.95 | -58.66 | 47.03 | |

| 0.5 | 1156.35 | 20096.49 | 14474.63 | 9044.79 | 8228.96 | 10582.79 | -27.97 | -54.99 | -59.05 | 47.34 | |

| 0.6 | 1143.85 | 19997.98 | 14312.97 | 9013.33 | 8010.24 | 10445.51 | -28.43 | -54.93 | -59.94 | 47.77 | |

| 0.7 | 1131.35 | 19821.01 | 14147.68 | 8964.07 | 7538.38 | 10216.71 | -28.62 | -54.77 | -61.97 | 48.46 | |

| 0.8 | 1118.85 | 19553.39 | 13967.22 | 8923.75 | 7027.98 | 9972.99 | -28.57 | -54.36 | -64.06 | 49.00 | |

| 0.9 | 1106.35 | 19285.76 | 13786.75 | 8883.42 | 6540.94 | 9737.04 | -28.51 | -53.94 | -66.08 | 49.51 | |

| 1 | Qin Y, Wang R, Vakharia A J, et al. The newsvendor problem: Review and directions for future research[J]. European Journal of Operational Research, 2011, 213(2): 361-374. |

| 2 | Deyong G D. The price-setting newsvendor: Review and extensions[J]. International Journal of Production Research, 2020, 58(6): 1776-1804. |

| 3 | Tapiero C S, Kogan K. Risk-averse order policies with random prices in complete market and retailers’ private information[J]. European Journal of Operational Research, 2009, 196(2): 594-599. |

| 4 | Snyder V, Shen Z J M. Fundamentals of supply chain theory[M]. NJ: Wiley, 2019. |

| 5 | Van Parys B P G, Esfahani P M, Kuhn D. From data to decisions: Distributionally robust optimization is optimal [J]. Management Science,2021,67(6): 3387-3402. |

| 6 | 许民利, 李展. 需求依赖于价格情境下基于Copula-CVaR的报童决策[J]. 控制与决策, 2014, 29(6):1083-1090. |

| Xu M L, Li Z.Newsvendor decision based on Copula-CVaR with price-dependent demand[J]. Control and Decision, 2014, 29(6):1083-1090. | |

| 7 | Natarajan K, Sim M, Uichanco J. Asymmetry and ambiguity in Newsvendor models[J]. Management Science, 2018, 64(7): 3146-3167. |

| 8 | Nelson R B. An introduction to copulas[M]. New York: Springer, 2006. |

| 9 | Kakouris I, Rustem B. Robust portfolio optimization with copulas[J]. European Journal of Operational Research, 2014, 235(1): 28-37. |

| 10 | Delage E, Ye Y. Distributionally robust optimization under moment uncertainty with application to datadriven problems[J]. Operations Research, 2010, 58(3): 595-612. |

| 11 | Scarf H. A min-max solution of an inventory problem[M]//Arrow K J,Karlin S,Scarf H. Studies in the Mathematical Theory of Inventory and Production. CA: Stanford University Press,1958:201-209. |

| 12 | Yue J, Chen B, Wang M C. Expected value of distribution information for the newsvendor problem[J]. Operations Research, 2006, 54(6): 1128-1136. |

| 13 | Laan N V D, Teunter R H, Romeijnders W, et al. The data-driven newsvendor problem: Achieving on-target service-levels using distributionally robust chance-constrained optimization[J]. International Journal of Production Economics,2022,249:108509. |

| 14 | 黎俊, 王曙明. 基于截断需求的分布鲁棒报童问题[J].系统工程理论与实践,2022,42(5):1260-1276. |

| Li J, Wang S M. Distributionally robust newsvendor problem with censored demand[J].Systems Engineering- Theory & Practice,2022,42(5):1260-1276. | |

| 15 | Fu Q, Sim C K, Teo C P. Profit sharing agreements in decentralized supply chains: A distributionally robust approach[J]. Operations Research, 2018, 66(2): 500-513. |

| 16 | Rubio-Herrero J, Baykal-Gürsoy M. Mean-variance analysis of the newsvendor problem with price-dependent, isoelastic demand[J]. European Journal of Operational Research, 2020, 283: 942-953. |

| 17 | Choi T M, Li D, Yan H. Mean-variance analysis for the newsvendor problem[J]. IEEE Transactions on Systems Man & Cybernetics Part A: Systems & Humans, 2008, 38(5): 1169-1180. |

| 18 | Tapiero C S. Value at risk and inventory control [J]. European Journal of Operational Research, 2005, 163(3): 769-775. |

| 19 | Chiu C H, Choi T M. Optimal pricing and stocking decisions for newsvendor problem with value-at-risk consideration[J]. IEEE Transactions on Systems Man & Cybernetics Part A:Systems & Humans, 2010, 40(5): 1116-1119. |

| 20 | Lin S, Chen F, Li Y, et al. Data-Driven Newsvendor with Profit Risk Consideration[J]. Production and Operations Management, 2022, 31(4): 1630-1644. |

| 21 | Rockafellar R T, Uryasev S. Optimization of conditional Value-At-Risk[J]. Journal of Risk, 1999, 29(1):1071-1074. |

| 22 | Filippi C, Guastaroba G, Speranza M G. Conditional Value-at-Risk beyond finance: A survey[J]. International Transactions in Operational Research, 2020, 27: 1277-1319. |

| 23 | Zhang J, Chan F T S, Xu X. The optimal order decisions of a risk-averse newsvendor under backlogging[J]. Annals of Operations Research, 2023,329:225-247. |

| 24 | Chen X, Sim M, Simchi-Levi D, et al. Risk aversion in inventory management[J]. Operations Research, 2007, 55(5): 828-842. |

| 25 | Qiu R, Shang J, Huang X. Robust inventory decision under distribution uncertainty: A CVaR -based optimization approach[J]. International Journal of Production Economics, 2014, 153: 13-23. |

| 26 | 孙艺萌,邱若臻,张多琦,等.不确定条件下的零售商库存鲁棒均值-CVaR决策模型[J].计算机集成制造系统,2020,26(10):2812-2826. |

| Sun Y M, Qiu R Z, Zhang D Q, et al.Robust mean-CVaR-based inventory decision model for retailer under uncertainty[J]. Computer Integrated Manufacturing Systems,2020,26(10):2812-2826. | |

| 27 | 邱若臻, 张多琦, 孙艺萌, 等.供需不确定条件下基于CVaR的零售商库存鲁棒优化模型[J].中国管理科学,2020,28(12):98-107. |

| Qiu R Z, Zhang D Q, Sun Y M, et al.The CVaR-based robust optimization model for retailer’s inventory management under supply and demand uncertainties[J].Chinese Journal of Management Science, 2020,28(12):98-107. | |

| 28 | Sion M. On general minimax theorems[J]. Pacific Journal of Mathematics, 1958, 8(1): 171-176. |

| 29 | 周赛玉, 王长军, 邵栗. Copula-CVaR下考虑随机成本和需求的单周期订货决策研究[J].运筹与管理, 2020, 29(4): 138-146. |

| Zhou S Y, Wang C J, Shao L.Decision on single-period optimal order quantity by using Copula-CVaR based on stochastic cost and price[J].Operations Research and Management Science, 2020,29(4): 138-146. | |

| 30 | Kaki A, Salo A, Talluri S. Scenario-based modeling of interdependent demand and supply uncertainties[J]. IEEE Transactions on Engineering Management, 2014, 61(1): 101-113. |

| 31 | Nakao H, Shen S, Chen Z. Network design in scarce data environment using moment-based distributionally robust optimization[J].Computers & Operations Research, 2017, 88: 44-57. |

| 32 | Wang C, Chen S. A distributionally robust optimization for blood supply network considering disasters[J]. Transportation Research Part E: Logistics and Transportation Review, 2020, 134: 1-30. |

| 33 | Boyd S, Vandenberghe L. Convex optimization[M]. Cambridge: Cambridge University Press, 2004. |

| 34 | Rockafellar R T, Uryasev S. Conditional value-at-risk for general loss distributions[J]. Journal of Banking and Finance, 2002, 26(7): 1443-1471. |

| [1] | Ling Zhang, Jinpeng Li, Shengqun Chen. Research on Distributed Robust Optimization Scheme of Emergency Blood Supply Network Configuration Based on Data Driven [J]. Chinese Journal of Management Science, 2025, 33(2): 131-140. |

| [2] | Wenqiang Dai,Weijia Chu,Jing Zhong. Online Display Advertising Optimization Based on Guaranteed Delivery Contract under CPC Model [J]. Chinese Journal of Management Science, 2024, 32(10): 256-264. |

| [3] | HU Hai-qing, Pandu R Tadikamalla. Twostage Inventory Model Considering Forecast Accuracy of Online Fast Fashion Products [J]. Chinese Journal of Management Science, 2023, 31(7): 256-265. |

| [4] | Rui-zhen XIE,Yao ZHANG. Inventory Decision Considering Returns under Omni-channel Retailing [J]. Chinese Journal of Management Science, 2023, 31(12): 128-137. |

| [5] | HAI Jiang-tao, LI Xu. Government's Optimal Subsidiesduring the Adoption of Green Products under Uncertain Demand [J]. Chinese Journal of Management Science, 2021, 29(5): 180-189. |

| [6] | WU Bo, GUAN Yu-xian, CHEN Jie, CHEN Zhi-xiang. Multi-product Newsvendor Model with Markov Competitive Factors [J]. Chinese Journal of Management Science, 2019, 27(5): 96-108. |

| [7] | CHEN Jing-xian, LIANG Liang. Pre-positioning Decisions of Stockpiling Multiple Relief Materials: An Extended Newsvendor Approach [J]. Chinese Journal of Management Science, 2018, 26(6): 143-152. |

| [8] | WANG Hai-yan, JUAN Zhi-ru, Henry Xu. Newsvendor Decision-making under Uncertainty of Demand Distribution [J]. Chinese Journal of Management Science, 2018, 26(4): 22-29. |

| [9] | CHEN Jie, TANG Ping, GAO Teng. Multi-product Newsvendor Model with Multivariate Markovian Demand [J]. Chinese Journal of Management Science, 2017, 25(2): 57-67. |

| [10] | LI Hui, QI Er-shi. Advance Sellingin the Presence of Uncertainty Market Size [J]. Chinese Journal of Management Science, 2017, 25(2): 50-56. |

| [11] | CHEN Ming-qin, LIU Xing. Optimal Cash Holding Structure:A Perspective on the Value of Capital Supply Chain [J]. Chinese Journal of Management Science, 2015, 23(8): 92-101. |

| [12] | YAN Ni-na, HUANG Xiao-yuan, MA Long-long. Research on Robust Stochastic Optimization of Multi-Retailers Competition under Demand Uncertainty [J]. Chinese Journal of Management Science, 2008, 16(4): 50-54. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||