主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2024, Vol. 32 ›› Issue (11): 13-24.doi: 10.16381/j.cnki.issn1003-207x.2022.0197

Previous Articles Next Articles

Kun Yang1, Yu Wei2( ), Qianting Ma3, Jianmin He4, Wenhua Yu1

), Qianting Ma3, Jianmin He4, Wenhua Yu1

Received:2022-01-28

Revised:2022-06-19

Online:2024-11-25

Published:2024-12-09

Contact:

Yu Wei

CLC Number:

Kun Yang, Yu Wei, Qianting Ma, Jianmin He, Wenhua Yu. The International Pricing Power of China's Crude Oil Futures: Comparative Analyses from the Perspective of Dynamic Information Spillover[J]. Chinese Journal of Management Science, 2024, 32(11): 13-24.

"

| 原油期现货市场 | 平均值 | 最小值 | 最大值 | 标准差 | 偏度 | 峰度 | LM | ADF |

|---|---|---|---|---|---|---|---|---|

| Panel A:原油期货 | ||||||||

| WTI | 0.001 | -0.350 | 0.157 | 0.157 | -3.663*** | 49.887*** | 109.100*** | -9.234*** |

| Brent | 0.001 | -0.203 | 0.151 | 0.151 | -1.156*** | 20.826*** | 52.419*** | -6.079*** |

| Oman | 0.001 | -0.217 | 0.279 | 0.279 | 0.560*** | 37.842*** | 37.343*** | -6.595*** |

| SC | 0.001 | -0.105 | 0.072 | 0.072 | -0.695*** | 3.020*** | 55.635*** | -8.079*** |

| Panel B:亚洲原油现货 | ||||||||

| Daqing | 0.001 | -0.310 | 0.257 | 0.257 | -1.180*** | 36.567*** | 30.501*** | -6.283*** |

| Shengli | 0.001 | -0.223 | 0.190 | 0.190 | -0.933*** | 23.697*** | 31.450*** | -6.137*** |

| Minas | 0.001 | -0.294 | 0.288 | 0.288 | -0.677*** | 40.889*** | 33.420*** | -5.979*** |

| Cinta | 0.000 | -0.299 | 0.257 | 0.257 | -1.053*** | 33.331*** | 29.590*** | -6.386*** |

| Duri | 0.001 | -0.193 | 0.170 | 0.170 | -0.813*** | 19.850*** | 34.175*** | -6.041*** |

| Tapis | 0.001 | -0.253 | 0.228 | 0.228 | -0.799*** | 30.803*** | 41.633*** | -6.511*** |

"

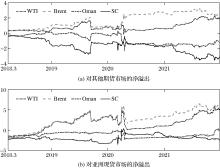

| 指标 | WTI | Brent | Oman | SC | Daqing | Shengli | Minas | Cinta | Duri | Tapis |

|---|---|---|---|---|---|---|---|---|---|---|

| Panel A:总样本区间(2018.3.26—2021.12.31) | ||||||||||

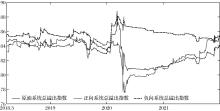

| 溢出 | 97.2 | 119.0 | 62.9 | 37.4 | 86.5 | 85.9 | 85.4 | 86.8 | 84.0 | 85.4 |

| 溢入 | 72.7 | 74.5 | 82.2 | 74.4 | 87.9 | 88.1 | 87.5 | 87.7 | 88.0 | 87.6 |

| 净溢出 | 24.5 | 44.6 | -19.2 | -36.9 | -1.5 | -2.2 | -2.1 | -0.9 | -4.0 | -2.2 |

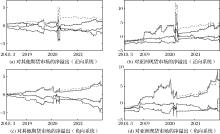

| 对其他期货市场的净溢出 | 7.3 | 17.3 | -7.2 | -17.4 | ||||||

| 对亚洲现货市场的净溢出 | 17.2 | 27.2 | -12.0 | -19.5 | ||||||

| Panel B:COVID-19爆发前(2018.3.26—2019.12.30) | ||||||||||

| 溢出 | 88.8 | 99.1 | 74.0 | 43.9 | 91.0 | 90.7 | 87.0 | 91.6 | 88.1 | 87.1 |

| 溢入 | 74.7 | 78.1 | 83.2 | 80.1 | 87.7 | 87.9 | 86.9 | 87.7 | 87.8 | 87.3 |

| 净溢出 | 14.1 | 21.0 | -9.1 | -36.2 | 3.3 | 2.8 | 0.1 | 4.0 | 0.3 | -0.2 |

| 对其他期货市场的净溢出 | 3.8 | 8.7 | 0.2 | -12.7 | ||||||

| 对亚洲现货市场的净溢出 | 10.3 | 12.3 | -9.3 | -23.5 | ||||||

| Panel C:COVID-19爆发后(2019.12.31—2021.12.31) | ||||||||||

| 溢出 | 103.7 | 134.7 | 54.2 | 32.4 | 82.9 | 82.2 | 84.0 | 83.0 | 80.9 | 84.0 |

| 溢入 | 71.1 | 71.7 | 81.4 | 69.9 | 88.1 | 88.3 | 87.9 | 87.7 | 88.2 | 87.8 |

| 净溢出 | 32.7 | 63.1 | -27.2 | -37.5 | -5.2 | -6.2 | -3.8 | -4.7 | -7.3 | -3.8 |

| 对其他期货市场的净溢出 | 10.1 | 24.1 | -13.1 | -21.1 | ||||||

| 对亚洲现货市场的净溢出 | 22.6 | 39.0 | -14.1 | -16.4 | ||||||

"

"

"

"

"

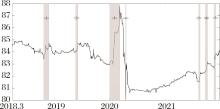

| 1 |

|

| 2 |

|

| 3 |

|

| 4 |

|

| 5 |

|

| 6 |

|

| 7 |

张大永, 姬强. 中国原油期货动态风险溢出研究[J]. 中国管理科学, 2018, 26(11): 42-49.

|

|

|

|

| 8 |

|

| 9 |

|

| 10 |

|

| 11 |

|

| 12 |

田洪志, 姚峰, 李慧. 中国是否拥有原油的国际定价权?——基于油价间独立性与传导性视角[J]. 中国管理科学, 2020, 28(11): 90-99.

|

|

|

|

| 13 |

|

| 14 |

|

| 15 |

田洪志, 姚峰, 李慧. 国际油价波动下的东亚原油市场格局[J]. 日本学刊, 2022(3): 28-49+149-150+152.

|

|

|

|

| 16 |

|

| 17 |

|

| 18 |

|

| 19 |

田洪志, 姚峰, 罗浩, 等. 中国原油价格争取成为国际基准指标的进程研判[J].中国软科学, 2020(12): 11-21.

|

|

|

|

| 20 |

|

| 21 |

|

| 22 |

|

| 23 |

卜林, 李晓艳, 朱明皓. 上海原油期货的价格发现功能及其国际比较研究[J]. 国际贸易问题, 2020(9): 160-174.

|

|

|

|

| 24 |

杨子晖, 陈雨恬, 张平淼. 重大突发公共事件下的宏观经济冲击、金融风险传导与治理应对[J]. 管理世界, 2020, 36(5): 13-35.

|

|

|

|

| 25 |

|

| 26 |

|

| 27 |

|

| 28 |

|

| 29 |

|

| 30 |

|

| 31 |

|

| 32 |

|

| 33 |

|

| 34 |

|

| 35 |

陈昊, 陈平, 杨海生, 等. 离岸与在岸人民币利率定价权的实证分析——基于溢出指数及其动态路径研究[J]. 国际金融研究, 2016(6): 86-96.

|

|

|

|

| 36 |

朱学红, 谌金宇, 邵留国. 信息溢出视角下的中国金属期货市场国际定价能力研究[J]. 中国管理科学, 2016, 24(9): 28-35.

|

|

|

|

| 37 |

|

| 38 |

郑挺国, 刘堂勇. 股市波动溢出效应及其影响因素分析[J]. 经济学(季刊), 2018, 17(2): 669-692.

|

|

|

|

| 39 |

|

| 40 |

|

| 41 |

|

| 42 |

|

| 43 |

杨子晖, 周颖刚. 全球系统性金融风险溢出与外部冲击[J]. 中国社会科学, 2018(12): 69-90+200-201.

|

|

|

|

| 44 |

|

| 45 |

|

| 46 |

|

| 47 |

张晓晶, 刘磊. 宏观分析新范式下的金融风险与经济增长——兼论新型冠状病毒肺炎疫情冲击与在险增长[J]. 经济研究, 2020, 55(6): 4-21.

|

|

|

|

| 48 |

|

| 49 |

|

| 50 |

|

| [1] | Lan Bai,Yu Wei. Information Spillovers between Investor's Public Health Emergency Attention and Industrial Stocks: Empirical Evidence from TVP-VAR Model [J]. Chinese Journal of Management Science, 2024, 32(1): 54-64. |

| [2] | ZHU Li, LIU Xiang-li, YANG Xiao-guang. Does Investor Sentiment Affect the Price Dynamic Relationship of Stock Index Futures-spot Market? [J]. Chinese Journal of Management Science, 2022, 30(4): 52-62. |

| [3] | ZHONG Wan-ling, LI Hai-qi. Tail Risk Spillover Effects among Crude Oil Price, Macroeconomic Variables and China’s Stock Market [J]. Chinese Journal of Management Science, 2022, 30(2): 27-37. |

| [4] | ZHANG Xiao-wan, YI Rong-hua, YU Ying, WANG Ying. The Measure of Volatility Spillover Effect of Shanghai-Hong Kong Stock Connect Based on Rolling Window VAR [J]. Chinese Journal of Management Science, 2022, 30(11): 42-51. |

| [5] | LIN Qiang, SONG Jia-qi, FU Wen-hui. The Impact of Fairness Preference on the Equilibrium Decisions of Retailer-led Supply Chain [J]. Chinese Journal of Management Science, 2021, 29(6): 149-159. |

| [6] | ZHU Peng-fei, TANG Yong, HONG Xiao-mei, LU Tuan-tuan. Does the P2P Lending Interest Rate Have Volatility Spillovers?——An Empirical Study Based on Time-frequency Domains Spillover Index [J]. Chinese Journal of Management Science, 2021, 29(4): 82-92. |

| [7] | LIU Xiao-jun, JIANG Wei, HU Jing-song. A Study on Confidence, Monetary Policy and China's Economic Fluctuation Based on TVP-VAR Model [J]. Chinese Journal of Management Science, 2019, 27(8): 37-46. |

| [8] | ZHU Xue-hong, CHEN Jin-yu, SHAO Liu-guo. The International Pricing Power of Chinese Metal Futures Market Based on Information Spillover [J]. Chinese Journal of Management Science, 2016, 24(9): 28-35. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||