主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2024, Vol. 32 ›› Issue (6): 1-12.doi: 10.16381/j.cnki.issn1003-207x.2021.0732

Changqing Luo1,2( ),Lan Liu1,Huiming Zhu2,Min Zhang1

),Lan Liu1,Huiming Zhu2,Min Zhang1

Received:2021-04-13

Revised:2021-08-11

Online:2024-06-25

Published:2024-07-03

Contact:

Changqing Luo

E-mail:changqingluo@hnu.edu.cn

CLC Number:

Changqing Luo,Lan Liu,Huiming Zhu,Min Zhang. An Empirical Study on the Dynamic Evolution of Crude Oil Market Pricing Power Based on Multi-scale Information Share Model[J]. Chinese Journal of Management Science, 2024, 32(6): 1-12.

"

"

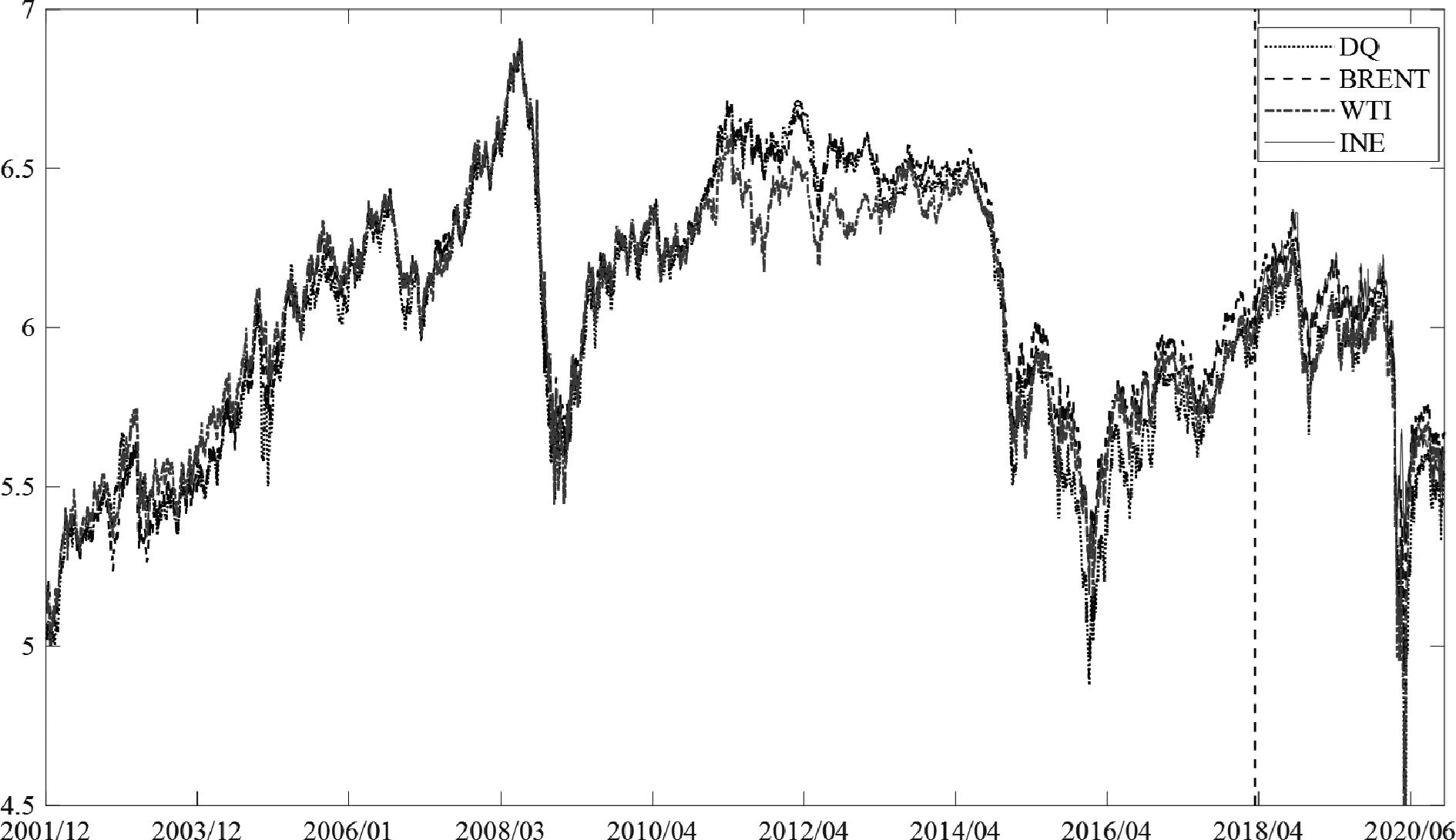

| 变量 | 均值 | 中间值 | 最大值 | 最小值 | 标准差 | 偏度 | 峰度 | J-B值 |

|---|---|---|---|---|---|---|---|---|

| 2001/12/26—2018/03/25 | ||||||||

| DQ | 6.0379 | 6.1059 | 6.8944 | 4.8775 | 0.4320 | -0.2664 | 2.0085 | 210.46(0.000) |

| BRENT | 6.0865 | 6.1569 | 6.9088 | 5.0263 | 0.4112 | -0.3684 | 2.1105 | 221.62(0.000) |

| WTI | 6.0555 | 6.1607 | 6.9034 | 5.0021 | 0.3755 | -0.3660 | 2.2037 | 194.34(0.000) |

| 2018/03/26—2020/11/18 | ||||||||

| DQ | 5.8525 | 5.9682 | 6.2816 | 4.4865 | 0.3133 | -1.4607 | 5.0218 | 327.66(0.000) |

| BRENT | 5.9741 | 6.0753 | 6.3744 | 4.9183 | 0.2792 | -1.3341 | 4.3615 | 232.91(0.000) |

| WTI | 5.8647 | 5.9635 | 6.2488 | 4.2602 | 0.2956 | -1.8773 | 7.5096 | 893.85(0.000) |

| INE | 5.9794 | 6.0813 | 6.3713 | 5.3176 | 0.2592 | -0.8865 | 2.4063 | 90.75(0.000) |

"

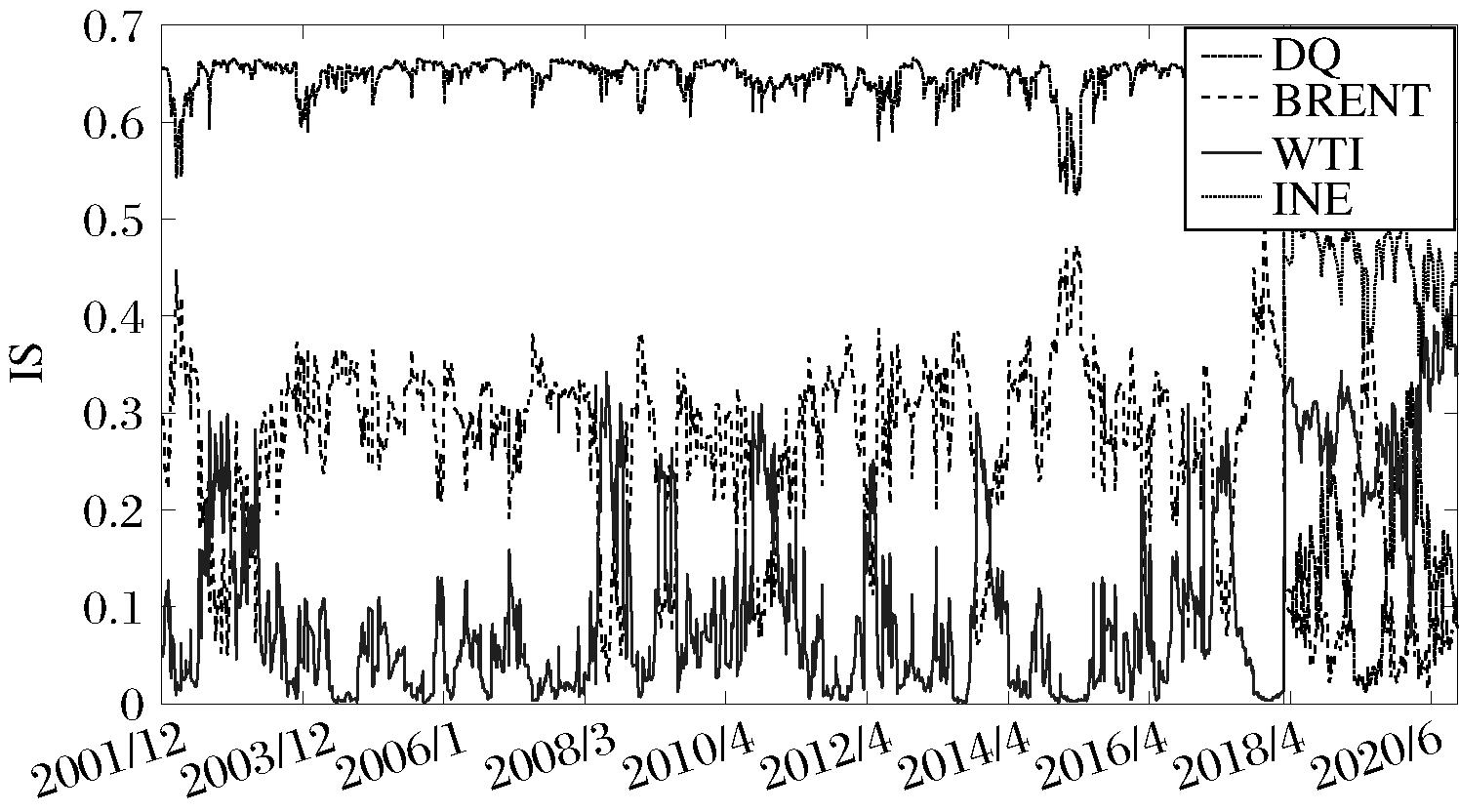

| 变量 | 静态信息份额 | 动态信息份额 | ||||||

|---|---|---|---|---|---|---|---|---|

| DQ | BRENT | WTI | INE | DQ | BRENT | WTI | INE | |

| IS1 | 0.3861 | 0.3966 | 0.2173 | / | 0.3779 | 0.3972 | 0.2249 | / |

| IS2 | 0.0936 | 0.3386 | 0.2825 | 0.2853 | 0.1022 | 0.3305 | 0.2789 | 0.2884 |

| ΔIS | -0.2925 | -0.0580 | 0.0652 | 0.2853 | -0.2757 | -0.0667 | 0.0540 | 0.2884 |

"

"

| 频域 | 变量 | 静态 | 动态 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| DQ | BRENT | WTI | INE | DQ | BRENT | WTI | INE | ||

| 高频 | IS1 | 0.5766 | 0.1818 | 0.2416 | / | 0.5642 | 0.1966 | 0.2392 | / |

| IS2 | 0.1842 | 0.2183 | 0.3388 | 0.2587 | 0.1872 | 0.1976 | 0.2998 | 0.3154 | |

| ΔIS | -0.3924 | 0.0365 | 0.0972 | 0.2587 | -0.3770 | 0.0010 | 0.0606 | 0.3154 | |

| 中频 | IS1 | 0.3672 | 0.3316 | 0.3011 | / | 0.3649 | 0.3148 | 0.3203 | / |

| IS2 | 0.2080 | 0.2818 | 0.2923 | 0.2179 | 0.2601 | 0.3072 | 0.2269 | 0.2058 | |

| ΔIS | -0.1592 | -0.0498 | -0.0088 | 0.2179 | -0.1048 | -0.0076 | -0.0934 | 0.2058 | |

| 低频 | IS1 | 0.6543 | 0.2939 | 0.0518 | / | 0.6452 | 0.2787 | 0.0761 | / |

| IS2 | 0.1056 | 0.0969 | 0.3325 | 0.4651 | 0.1396 | 0.1173 | 0.2873 | 0.4558 | |

| ΔIS | -0.5487 | -0.1970 | 0.2807 | 0.4651 | -0.5056 | -0.1614 | 0.2112 | 0.4558 | |

"

"

"

| 1 | Futures Industry Association. Global futures and options trading reaches record level in 2020[EB/OL]. , 2021. |

| 2 | Silvério R, Szklo A. The effect of the financial sector on the evolution of oil prices: Analysis of the contribution of the futures market to the price discovery process in the WTI spot market[J]. Energy Economics, 2012, 34(6): 1799–1808. |

| 3 | 田洪志, 姚峰, 李慧. 中国是否拥有原油的国际定价权?——基于油价间独立性与传导性视角[J].中国管理科学, 2020, 28(11): 90-99. |

| Tian H Z, Yao F, Li H. Does China have the international pricing power for crude oil?Based on a perspective of independence and conductivity between oil price[J]. Chinese Journal of Management Science, 2020, 28(11): 90-99. | |

| 4 | 陆凤彬, 李艺, 王栓红, 等. 全球原油市场间信息溢出的实证研究——基于CCF方法与ECM模型[J]. 系统工程理论与实践, 2008, 28(3): 25-34, 43. |

| Lu F B, Li Y, Wang S H, et al. Information spillovers among international crude oil markets: An empirical analysis based on CCF Method and ECM. Systems Engineering- Theory & Practice, 2008, 28(3): 25-34, 43. | |

| 5 | Hasbrouck J. One security, many markets: Determining the contributions to price discovery[J]. The Journal of Finance, 1995, 50(4): 1175-1199. |

| 6 | Gonzalo J, Granger C. Estimation of common long-memory components in cointegrated systems[J]. Journal of Business and Economic Statistics, 1995, 13(1): 27-35. |

| 7 | Baillie R T, Booth G G, Tse Y, et al. Price discovery and common factor models[J]. Journal of financial markets, 2002, 5(3): 309-321. |

| 8 | 周舟, 成思危. 沪深300股指期货市场中的宏观经济信息发布与价格发现[J]. 系统工程理论与实践, 2013, 33(12): 3045-3053. |

| Zhou Z, Cheng S W. Macroeconomic and announcements and price discovery in the CSI 300 Stock index futures market[J]. Systems Engineering—Theory & Practice, 2013, 33(12): 3045-3053. | |

| 9 | 张劲帆, 汤莹玮, 刚健华, 等. 中国利率市场的价格发现——对国债现货、期货以及利率互换市场的研究[J]. 金融研究, 2019, 463(1): 19-34. |

| Zhang J F, Tang Y W, Guang J H, et al. Price discovery in China’s interest rate markets: Evidence from treasury spot, futures, and interest rate swaps markets[J]. Journal of Financial Research, 2019, 463(1):19-34. | |

| 10 | 王群勇, 张晓峒. 原油期货市场的价格发现功能——基于信息份额模型的分析[J]. 统计与决策, 2005, 24(12): 77-79. |

| Wang Q Y, Zhang X D. Price discovery on crude oil futures market: Based on IS model[J]. Statistical and Decision, 2005, 24(12): 77-79. | |

| 11 | Zhao L T, Yan J L, Cheng L, et al. Empirical study of the functional changes in price discovery in the brent crude oil market[J]. Energy Procedia, 2017, 142(37): 2917-2922. |

| 12 | Kao C W, Wan J Y. Price discount, inventories and the distortion of WTI benchmark[J]. Energy Economics, 2012, 34(1): 117-124. |

| 13 | Avino D, Lazar E, Varotto S. Time varying price discovery[J]. Economics Letters, 2015, 126(1): 18-21. |

| 14 | 方雯, 冯耕中, 陆凤彬, 等. 中国钢材交易市场价格发现动态演化研究[J]. 系统工程理论与实践, 2019, 39(1): 49-59. |

| Fang W, Feng G Z, Lu F B, et al. Dynamic price discovery of steel trading markets in China[J]. Systems Engineering—Theory & Practice, 2019, 39(1): 49-59. | |

| 15 | Geng J B, Ji Q, Fan Y. The behavior mechanism analysis of regional natural gas prices: A multi-scale perspective[J]. Energy, 2016, 101(8): 266-277. |

| 16 | Liu C, Sun X L, Wang J, et al. Multiscale information transmission between commodity markets: An EMD-based transfer entropy network[J]. Research in International Business and Finance, 2021, 55(1): 101318. |

| 17 | Sun X L, Chen X W, Wang J, et al. Multi-scale interactions between economic policy uncertainty and oil prices in time-frequency domains[J]. The North American Journal of Economics and Finance, 2020, 51(1): 100854. |

| 18 | 刘映琳, 刘永辉, 鞠卓. 国际原油价格波动对中国商品期货的影响——基于多重相关性结构断点的分析[J]. 中国管理科学, 2019, 27(2): 31-40. |

| Liu Y L, Liu Y H, Ju Z. The impact of international crude oil price fluctuation on Chinese commodity futures: Based on the correlation structure breakpoint model[J]. Chinese Journal of Management Science, 2019, 27(2): 31-40. | |

| 19 | Bi F R, Ma T, Wang X. Development of a novel knock characteristic detection method for gasoline engines based on wavelet-denoising and EMD decomposition[J]. Mechanical Systems and Signal Processing, 2019, 117(4): 517-536. |

| 20 | 王书平, 朱艳云.基于多尺度分析的小麦价格预测研究[J]. 中国管理科学, 2016, 24(5): 85-91. |

| Wang S P, Zhu Y Y. Forecasting of wheat price based on multiscale analysis[J]. Chinese Journal of Management Science, 2016, 24(5): 85-91. | |

| 21 | 李霞, 李守伟. 基于EMD与DVG的非线性时间序列预测模型及其应用研究[J]. 中国管理科学, 2022, 30(9): 275-286. |

| Li X, Li S W. Non-linear time series prediction model based on EMD and DVG and its application[J]. 2022, 30(9): 275-286. | |

| 22 | Huang N E, Shen Z, Long S R, et al. The empirical mode decomposition and the Hilbert spectrum for nonlinear and non-stationary time series analysis[J]. Proceedings of the Royal Society of London. Series A: Mathematical, Physical and Engineering Sciences, 1998, 454(3): 903-995. |

| 23 | Li J P, Hao J, Sun X L, et al. Forecasting China’s sovereign CDS with a decomposition reconstruction strategy[J]. Applied Soft Computing, 2021, 105(7): 107291. |

| 24 | 孙晓蕾, 姚晓阳, 杨玉英, 等. 国家风险动态性的多尺度特征提取与识别:以OPEC国家为例[J]. 中国管理科学, 2015, 23(4): 1-10. |

| Sun X L, Yao X Y, Yang Y Y, et al. Multi-scale feature extraction and identification of country risk dynamics[J]. Chinese Journal of Management Science, 2015, 23(4): 1-10. | |

| 25 | Cox C C. Futures trading and market information[J]. Journal of Political Economy, 1976, 84(6): 1215-1237. |

| 26 | Meyler A. The pass through of oil prices into euro area consumer liquid fuel prices in an environment of high and volatile oil prices[J]. Energy Economics, 2009, 31(6): 867-881. |

| 27 | 徐鹏, 刘强. 国际原油价格的驱动因素:需求、供给还是金融——基于历史分解法的分析[J]. 宏观经济研究, 2019(7): 84-97. |

| Xu P, Liu Q. Drivers of international crude oil price demand, supply, or finance: An analysis based on historical decomposition[J]. Macroeconomics, 2019(7): 84-97. | |

| 28 | Klein T. Trends and contagion in WTI and Brent crude oil spot and futures markets: The role of OPEC in the last decade[J]. Energy Economics, 2018, 75(7): 636-646. |

| 29 | Liu J, Ma F, Tang Y K, Zhang Y J. Geopolitical risk and oil volatility: A new insight[J]. Energy Economics,2019, 84(9): 104548. |

| 30 | Brandt M W, Gao L. Macro fundamentals or geopolitical events? A textual analysis of news events for crude oil[J]. Social Science Electronic Publishing, 2019, 51(2):64-94. |

| 31 | Natoli F. Financialization of commodities before and after great financial crisis[J]. Journal of Economic Surveys, 2021, 35(2): 488–511. |

| 32 | 张跃军, 邢丽敏. 国际原油价格预测的研究动态与展望[J]. 电子科技大学学报(社科版), 2021, 23(4): 92-105. |

| Zhang Y J, Xing L M. Research trend and prospect of international crude oil price forecast[J]. Journal of UESTC(Social Sciences Edition), 2021, 23(4): 92-105. | |

| 33 | 王盼盼, 夏婷, 石建勋, 等. “石油-美元”动态关联的时变特征及影响因素研究[J]. 国际金融研究, 2020, 343(11): 35-44. |

| Wang P P, Xia T, Shi J X, et al. Time-Varying characteristics and influencing factors of “Oil-Dollar” dynamic correlation[J]. Studies of International Finance, 2020, 343(11): 35–44. | |

| 34 | Lv F, Yang C, Fang L B. Do the crude oil futures of the shanghai international energy exchange improve asset allocation of Chinese petrochemical-related stocks?[J]. International Review of Financial Analysis, 2020, 71(5): 101537. |

| 35 | Palao F, Pardo Á, Roig M. Is the leadership of the Brent-WTI threatened by China’s new crude oil futures market?[J]. Journal of Asian Economics, 2020, 70(5): 101237. |

| 36 | 曹洁, 雷良海. 中美贸易争端加剧了商品期货市场的风险传染吗?——基于动态M-Copula模型的实证研究[J]. 投资研究, 2019, 38(7): 39-50. |

| Cao J, Lei L H. Do Sino-US trade disputes aggravate risk contagion between commodity futures markets?Empirical research based on the dynamic M-Copula model[J]. Review of Investment Studies, 2019, 38(7): 39-50. | |

| 37 | Scheitrum D P, Carter C A, Revoredo-Giha C. WTI and Brent futures pricing structure[J]. Energy Economics, 2018, 72(4): 462-469. |

| 38 | Zhu B Z, Huang L Q, Yuan L L, et al. Exploring the risk spillover effects between carbon market and electricity market: A bidimensional empirical mode decomposition based conditional value at risk approach[J]. International Review of Economics and Finance, 2020, 67(3): 163-175. |

| 39 | 王良, 李璧肖, 马续涛, 等. 中国原油期货与国际原油期货的价格波动溢出效应及其持续性——基于BEKK-MGARCH模型的研究[J]. 系统工程, 2020, 39(3): 1-22. |

| Wang L, Li B X, Ma X T, et al. The price volatility spillover effect and its sustainability between Chinese crude oil future and international crude oil futures: Based on the BEKK-MGARCH model[J]. Systems Engineering, 2020, 39(3): 1-22. |

| [1] | GAO Xiao-hui, ZHOU Kun, LI Lian-shui. Hybrid Air Quality Early Warning System Based on XGBoost and ELM: A Case Study of Nanjing [J]. Chinese Journal of Management Science, 2023, 31(5): 269-278. |

| [2] | ZHANG Yue-jun, ZHANG Han, WANG Jin-li. Volatility Forecasting of Crude Oil Market Based on Structural Changes and Long Memory [J]. Chinese Journal of Management Science, 2021, 29(9): 54-64. |

| [3] | LIN Qiang, SONG Jia-qi, FU Wen-hui. The Impact of Fairness Preference on the Equilibrium Decisions of Retailer-led Supply Chain [J]. Chinese Journal of Management Science, 2021, 29(6): 149-159. |

| [4] | FANG Xue-qing, WU Chun-yin, YU Shou-hua, ZHANG Da-bin, OU Yang-qing. Research on Short-Term Forecast Model of Agricultural Product Price Based on EEMD-LSTM [J]. Chinese Journal of Management Science, 2021, 29(11): 68-77. |

| [5] | LIANG Xiao-zhen, WU Zhi-kun, YANG Ming-ge, WANG Shou-yang. Air Passenger Demand Forecasting Based on a Dual Decomposition Strategy and Fuzzy Time Series Model [J]. Chinese Journal of Management Science, 2020, 28(12): 108-117. |

| [6] | ZHU Peng-fei, TANG Yong, ZHONG Li. Portfolio Strategy Based on Wavelet-High Order Moments model-Take the International Crude Oil Markets as An Research Objects [J]. Chinese Journal of Management Science, 2020, 28(10): 24-35. |

| [7] | PAN He-ping, ZHANG Cheng-zhao. FEPA: An Adaptive Integrated Prediction Model of Financial Time Series [J]. Chinese Journal of Management Science, 2018, 26(6): 26-38. |

| [8] | YANG Kun, YU Wen-hua, WEI Yu. Dynamic Measurement of Extreme Risk among Various Crude Oil Markets Based on R-vine copula [J]. Chinese Journal of Management Science, 2017, 25(8): 19-29. |

| [9] | LI Hai-tao, LUO Dang, WEI Bao-lei. Method for Large Group Decision-making with Uncertain Linguistic Assessment Information Based on MC-EMD [J]. Chinese Journal of Management Science, 2017, 25(4): 164-173. |

| [10] | ZHU Xue-hong, CHEN Jin-yu, SHAO Liu-guo. The International Pricing Power of Chinese Metal Futures Market Based on Information Spillover [J]. Chinese Journal of Management Science, 2016, 24(9): 28-35. |

| [11] | ZHANG Guo-xing, ZHANG Zhen-hua, LIU Peng, LIU Ming-xing. The Running Mechanism and Prediction of the Growth Rate of China's Carbon Emissions [J]. Chinese Journal of Management Science, 2015, 23(12): 86-93. |

| [12] | RUAN Lian-fa, BAO Hong-jie. An Empirical Analysis on Periodic Fluctuations of Real Estate Price Based on EMD [J]. Chinese Journal of Management Science, 2012, (3): 41-46. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||