主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2025, Vol. 33 ›› Issue (7): 54-67.doi: 10.16381/j.cnki.issn1003-207x.2022.2287

薛凯丽1,2, 匡海波1,3( ), 孟斌1,3

), 孟斌1,3

收稿日期:2022-10-25

修回日期:2023-09-07

出版日期:2025-07-25

发布日期:2025-08-06

通讯作者:

匡海波

E-mail:khb@dlmu.edu.cn

基金资助:

Kaili Xue1,2, Haibo Kuang1,3(), Bin Meng1,3

Received:2022-10-25

Revised:2023-09-07

Online:2025-07-25

Published:2025-08-06

Contact:

Haibo Kuang

E-mail:khb@dlmu.edu.cn

摘要:

当下国际航运市场格局及需求出现巨大变化,国际原油价格和油轮运价波动剧烈,有效控制风险是油轮市场投资组合多样化和风险管理的重要手段。本文同时考虑到关注不同时间范围市场波动的市场参与者、油轮船型对相依结构的影响及可能存在发生结构变化的情况,通过构建基于MODWT分解的时变MRS Copula模型,刻画原油市场与油轮市场间的多尺度多状态动态相依关系,并运用尾部风险依赖系数度量多尺度多状态下两市场间的风险传染效应。结果表明:(1)相依结构。不同时间尺度下原油市场与油轮市场间的相依结构均存在两种状态,说明不同时间尺度下原油市场与油轮市场间的相依结构发生变化。(2)相依性特征。不同时间尺度下油轮市场内部及原油市场与油轮市场间的动态相依性存在显著差异性、时变性和非对称性。随时间尺度的增大,相依性波动区间越来越小,最后趋于稳定。(3)油轮市场内部风险传染效应。随着时间尺度的增大,两种状态下的油轮市场内部尾部风险波动程度越来越小,最后在长期下趋于稳定,而风险传染效应随时间尺度的增大而增大。(4)原油市场与油轮市场间的风险传染效应。不同时间尺度下,原油市场与油轮整体市场间的时变尾部风险均值大于原油市场与油轮细分市场间,即油轮整体市场更易受到原油市场的影响。此外,两种状态下的时变尾部风险呈现非对称性和高相依状态大于低相依状态的特点。其中,高相依状态下的风险传染效应随时间尺度的增大而减小。

中图分类号:

薛凯丽, 匡海波, 孟斌. 考虑多尺度多状态的原油市场与油轮市场动态相依性及风险传染研究[J]. 中国管理科学, 2025, 33(7): 54-67.

Kaili Xue, Haibo Kuang, Bin Meng. Study on Dynamic Dependence and Risk Contagion Effect of Crude Oil Market and Tanker Market Considering Multi-scale and Multi-state[J]. Chinese Journal of Management Science, 2025, 33(7): 54-67.

表1

指标体系"

| 市场类型 | 市场名称 | 指标 | 数据来源 | 类型 | |

|---|---|---|---|---|---|

| 原油市场 | Brent原油市场 | Brent原油期货 | Wind | 月度 | |

| WTI原油市场 | WTI原油期货 | Wind | 月度 | ||

| 油轮市场 | 油轮整体市场 | 原油油轮市场 | BDTI (波罗的海原油运价指数) | Clarksons | 月度 |

| 成品油油轮市场 | BCTI (波罗的海成品油运价指数) | Clarksons | 月度 | ||

| 油轮细分市场 | VLCC型油轮市场 | VLCC Tanker (选取航线TD15: 260000t West Africa - China) | Clarksons | 月度 | |

| 阿芙拉型油轮市场 | Aframax Tanker (选取航线TD9: 70000mt, Caribbean to US Gulf) | Clarksons | 月度 | ||

| 巴拿马型油轮市场 | Panamax Tanker (选取航线TC5:55000mt, CPP/UNL naphtha condensate, Middle East/Japan) | Clarksons | 月度 | ||

| 苏伊士型油轮市场 | Suezmax Tanker (选取航线TD6:135000mt, Black Sea/Mediterranean) | Clarksons | 月度 | ||

表2

原油市场及油轮市场收益序列的描述性统计"

| 统计量 | rBrent | rWTI | rBDTI | rBCTI | rVLCC | rAframax | rPanamax | rSuezmax |

|---|---|---|---|---|---|---|---|---|

| 均值 | 0.3303 | 0.3094 | -0.0226 | 0.2188 | -0.1477 | -0.0327 | 0.2524 | -0.0784 |

| 中值 | 1.2798 | 1.7945 | -0.5129 | -1.0773 | 0.3306 | -1.5025 | 0.3863 | 1.2144 |

| 最大值 | 35.6977 | 63.3269 | 56.9910 | 50.1292 | 90.6575 | 70.9432 | 68.5807 | 92.3002 |

| 最小值 | -63.3933 | -78.1866 | -57.8084 | -70.1012 | -91.4878 | -87.7757 | -113.6044 | -77.0168 |

| 标准差 | 10.2021 | 11.8259 | 16.4442 | 15.5255 | 20.3595 | 25.5776 | 20.8838 | 24.5681 |

| 偏度 | -1.4549 | -1.0037 | 0.1349 | 0.0152 | 0.2674 | -0.1471 | -0.4852 | 0.0439 |

| 峰度 | 11.0151 | 15.3572 | 4.9196 | 5.5277 | 7.6859 | 3.6109 | 7.2853 | 4.7488 |

| J-B检验 | 618.0228 | 1332.2060 | 31.9401 | 54.3161 | 189.0685 | 3.9079 | 164.0962 | 26.0603 |

| ADF | -11.0802*** | -11.5743*** | -11.3384*** | -11.6977*** | -14.4317*** | -13.3355*** | -12.8128*** | -12.3066*** |

| ARCH | 8.0660 | 26.1399 | 5.8752 | 13.1681 | 5.4215 | 12.5833 | 11.4763 | 3.1792 |

| [0.0004] | [0.0000] | [0.0162] | [0.0004] | [0.0209] | [0.0005] | [0.0000] | [0.0437] | |

| 样本量 | 204 | 204 | 204 | 204 | 204 | 204 | 204 | 204 |

表3

收益率序列的边缘分布参数估计结果"

| 参数 | rBrent | rWTI | rBDTI | rBCTI | rVLCC | rAframax | rPanamax | rSuezmax |

|---|---|---|---|---|---|---|---|---|

| a | -0.2359 | -0.3240 | -0.5798 | -0.5680 | -0.6887 | -0.5162 | 0.6657 | 0.6654 |

| (0. 3705) | (0.5273) | (0.1824) | (0.1829) | (0.1779) | (0.1897) | (0.0737) | (0.0599) | |

| b | 0.4124 | 0.4324 | 0.7557 | 0.7326 | 0.7899 | 0.3899 | -0.9310 | -0.9288 |

| (0.3468) | (0.5076) | (0.1336) | (0.1399) | (0.1561) | (0.2392) | (0.0370) | (0.0314) | |

| α | 0.6751 | 0.5756 | 0.2462 | 0.3579 | 0.6065 | 0.8157 | 0.6857 | 0.6432 |

| (0.1309) | (0.1754) | (0.1634) | (0.1941) | (0.2342) | (0.1710) | (0.1722) | (0.1952) | |

| β | 0.1980 | 0.2018 | 0.6028 | 0.4969 | 0.1625 | 0.1092 | 0.2112 | 0.2055 |

| (0.1087) | (0.1157) | (0.2031) | (0.2420) | (0.1108) | (0.0920) | (0.1071) | (0.1253) | |

| Dof | 5.8101 | 5.3430 | 5.5581 | 4.9535 | 3.6322 | 15.5380 | 5.1129 | 4.7100 |

| ARCH | 1.7865 | 1.0988 | 0.5673 | 0.4544 | 0.2249 | 2.3687 | 1.1265 | 0.1958 |

| [0.1092] | [0.3679] | [0.6653] | [0.7115] | [0.5083] | [0.0871] | [0.1479] | [0.6096] |

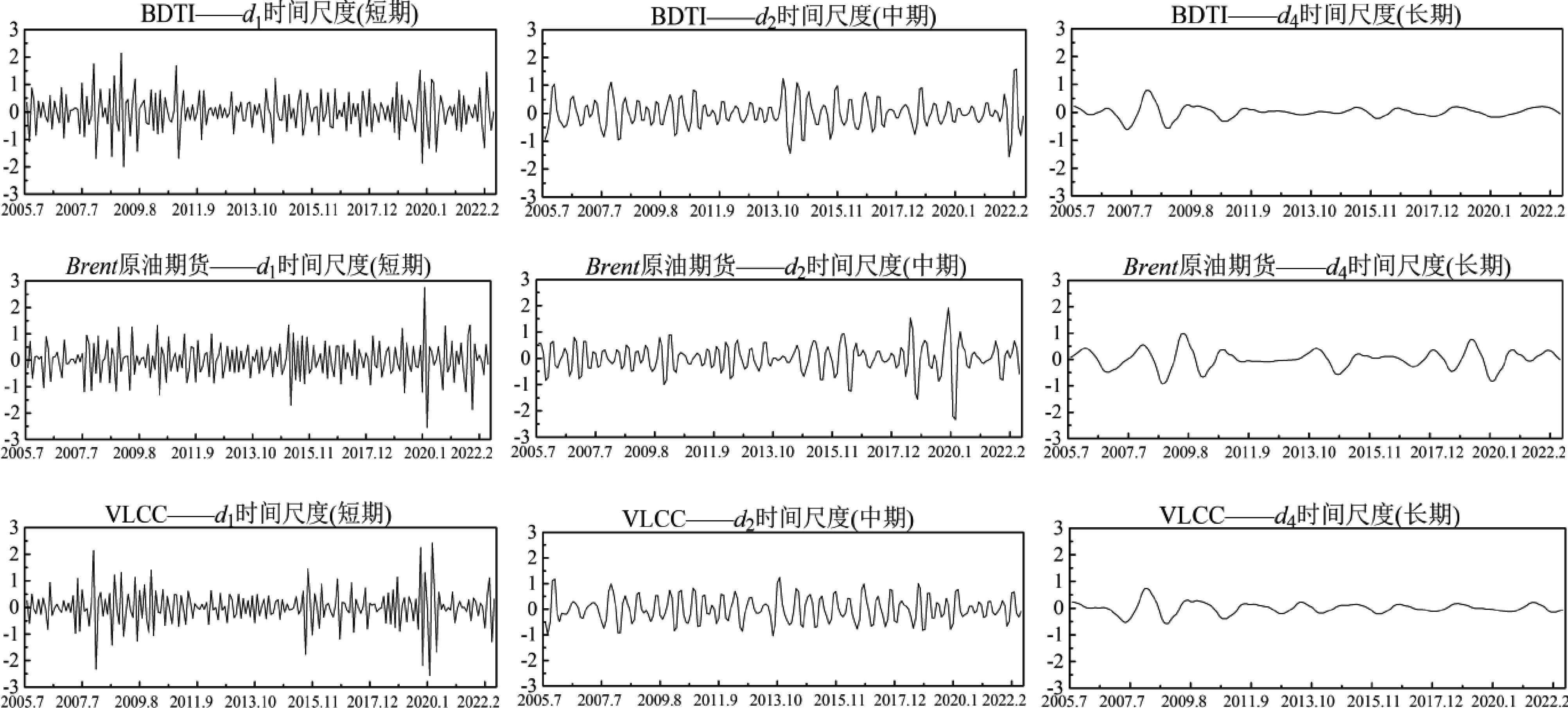

图1

部分变量的小波分解序列"

图2

不同时间尺度下(uWTI, vBCTI)间的时变参数"

图3

不同时间尺度下(uWTI, vBCTI)间平滑转移概率"

表4

不同时间尺度下Brent原油市场与油轮细分市场间最优时变MRS Copula函数的时变参数估计结果"

| 时间尺度 | 收益对 | 最优模型 | 时变参数 | 最小值 | 最大值 | 均值 | 标准差 | 时变参数 | 最小值 | 最大值 | 均值 | 标准差 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| d1时间尺度(短期) | (uBrent, vAframax) | 时变MRS Clayton | θ0 | 0.0046 | 6.1223 | 1.9650 | 1.1090 | θ1 | 0.0001 | 0.6303 | 0.0796 | 0.1041 |

| (uBrent, vPanamax) | 时变MRS Clayton | θ0 | 0.0001 | 36.8231 | 12.3186 | 10.5259 | θ1 | 0.0001 | 1.1028 | 0.1690 | 0.2193 | |

| (uBrent, vSuezmax) | 时变MRS Clayton | θ0 | 0.0001 | 10.0100 | 4.5858 | 4.5921 | θ1 | 0.0001 | 0.0296 | 0.0039 | 0.0046 | |

| (uBrent, vVLCC) | 时变MRS Clayton | θ0 | 0.0001 | 37.1588 | 12.8850 | 10.6466 | θ1 | 0.0001 | 2.4148 | 1.1209 | 0.5045 | |

| d2时间尺度(中期) | (uBrent, vAframax) | 时变MRS SJC Copula | τ0L | 0.0000 | 0.8781 | 0.2572 | 0.2356 | τ1L | 0.0000 | 0.0010 | 0.0010 | 0.0001 |

| τ0U | 0.0000 | 0.9858 | 0.6024 | 0.3275 | τ1U | 0.0000 | 0.0010 | 0.0010 | 0.0001 | |||

| (uBrent, vPanamax) | 时变MRS SJC Copula | τ0L | 0.0000 | 0.9493 | 0.7944 | 0.1079 | τ1L | 0.0000 | 0.0010 | 0.0010 | 0.0001 | |

| τ0U | 0.0002 | 0.0012 | 0.0010 | 0.0001 | τ1U | 0.0002 | 0.0010 | 0.0010 | 0.0001 | |||

| (uBrent, vSuezmax) | 时变MRS Clayton | θ0 | 0.0001 | 55.9061 | 17.2179 | 15.6236 | θ1 | 0.0001 | 1.8828 | 0.1193 | 0.1937 | |

| (uBrent, vVLCC) | 时变MRS Clayton | θ0 | 0.0001 | 45.1563 | 12.9884 | 11.2706 | θ1 | 0.0001 | 2.3159 | 0.2912 | 0.3899 | |

| d4时间尺度(长期) | (uBrent, vAframax) | 时变MRS SJC Copula | τ0L | 0.0005 | 0.9867 | 0.6066 | 0.3562 | τ1L | 0.0005 | 0.0011 | 0.0010 | 0.0000 |

| τ0U | 0.0000 | 0.2897 | 0.1186 | 0.0640 | τ1U | 0.0000 | 0.0010 | 0.0010 | 0.0001 | |||

| (uBrent, vPanamax) | 时变MRS Clayton | θ0 | 0.0001 | 49.4121 | 14.2155 | 12.9225 | θ1 | 0.0001 | 4.2503 | 1.5005 | 0.9502 | |

| (uBrent, vSuezmax) | 时变MRS SJC Copula | τ0L | 0.0000 | 0.9758 | 0.9090 | 0.0735 | τ1L | 0.0000 | 0.0010 | 0.0010 | 0.0001 | |

| τ0U | 0.0009 | 0.0010 | 0.0010 | 0.0000 | τ1U | 0.0009 | 0.0010 | 0.0010 | 0.0000 | |||

| (uBrent, vVLCC) | 时变MRS SJC Copula | τ0L | 0.0010 | 0.9047 | 0.1204 | 0.2116 | τ1L | 0.0010 | 0.0654 | 0.0013 | 0.0045 | |

| τ0U | 0.0032 | 0.3824 | 0.1296 | 0.0967 | τ1U | 0.0010 | 0.0912 | 0.0014 | 0.0063 |

图4

不同时间尺度下油轮整体市场(uBDTI与vBCTI)间的时变尾部风险"

表5

不同尺度下油轮整体市场与油轮细分市场间的时变尾部风险依赖结果"

| 时间尺度 | 收益对 | 尾部风险(S0) | 最小值 | 最大值 | 均值 | 标准差 | 尾部风险(S1) | 最小值 | 最大值 | 均值 | 标准差 |

|---|---|---|---|---|---|---|---|---|---|---|---|

d1 时间 尺度 (短期) | (uBTI, vAframax) | λ0L | 0.1474 | 0.5381 | 0.2767 | 0.0842 | λ1L | 0.4801 | 0.9148 | 0.6878 | 0.0737 |

| λ0U | 0.0479 | 0.4080 | 0.0603 | 0.0266 | λ1U | 0.4080 | 0.8226 | 0.7124 | 0.0872 | ||

| (uBTI,vPanamax) | λ0L | 0.1588 | 0.4048 | 0.1829 | 0.0209 | λ1L | 0.4048 | 0.8643 | 0.8415 | 0.0340 | |

| λ0U | 0.0614 | 0.7607 | 0.3006 | 0.1766 | λ1U | 0.3134 | 0.9475 | 0.7595 | 0.1572 | ||

| (uBTI,vSuezmax) | λ0L | 0.4355 | 0.7290 | 0.6310 | 0.0421 | λ1L | 0.1646 | 0.5118 | 0.2971 | 0.0383 | |

| λ0U | 0.0650 | 0.9313 | 0.6428 | 0.2026 | λ1U | 0.0103 | 0.6882 | 0.2644 | 0.1613 | ||

d2 时间 尺度 (中期) | (uBTI, vAframax) | λ0L | 0.0612 | 0.8925 | 0.5219 | 0.1613 | λ1L | 0.0010 | 0.3657 | 0.0028 | 0.0255 |

| λ0U | 0.0800 | 0.9283 | 0.5947 | 0.1572 | λ1U | 0.0049 | 0.4725 | 0.0906 | 0.0631 | ||

| (uBTI,vPanamax) | λ0L | 0.2187 | 0.8101 | 0.7138 | 0.0483 | λ1L | 0.0010 | 0.2187 | 0.0021 | 0.0152 | |

| λ0U | 0.0257 | 0.8695 | 0.5679 | 0.1731 | λ1U | 0.0010 | 0.0257 | 0.0011 | 0.0017 | ||

| (uBTI,vSuezmax) | λ0L | 0.0677 | 0.9567 | 0.7401 | 0.1414 | λ1L | 0.0294 | 0.8354 | 0.3636 | 0.2219 | |

| λ0U | 0.5389 | 0.9549 | 0.8411 | 0.0544 | λ1U | 0.1897 | 0.6584 | 0.4050 | 0.0645 | ||

d4 时间 尺度 (长期) | (uBTI, vAframax) | λ0L | 0.3616 | 0.8997 | 0.8823 | 0.0376 | λ1L | 0.1416 | 0.3616 | 0.1728 | 0.0181 |

| λ0U | 0.5455 | 0.8834 | 0.8632 | 0.0248 | λ1U | 0.2161 | 0.5455 | 0.2641 | 0.0274 | ||

| (uBTI,vPanamax) | λ0L | 0.4798 | 0.6927 | 0.5931 | 0.0366 | λ1L | 0.6927 | 0.9345 | 0.8935 | 0.0226 | |

| λ0U | 0.3181 | 0.9064 | 0.8049 | 0.1199 | λ1U | 0.0385 | 0.7510 | 0.1136 | 0.0667 | ||

| (uBTI,vSuezmax) | λ0L | 0.6304 | 0.8601 | 0.8306 | 0.0313 | λ1L | 0.0010 | 0.7937 | 0.0050 | 0.0555 | |

| λ0U | 0.1206 | 0.8839 | 0.7892 | 0.1146 | λ1U | 0.0010 | 0.7112 | 0.0047 | 0.0497 |

表6

不同时间尺度下Brent原油市场与油轮整体市场间的时变尾部风险依赖结果"

| 时间尺度 | 收益对 | 尾部风险(S0) | 最小值 | 最大值 | 均值 | 标准差 | 尾部风险(S1) | 最小值 | 最大值 | 均值 | 标准差 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| d1时间尺度(短期) | (uBrent,vBDTI) | λ0L | 0.0003 | 0.9713 | 0.9363 | 0.0681 | λ1L | 0.0003 | 0.0010 | 0.0010 | 0.0000 |

| λ0U | 0.0000 | 0.9462 | 0.8492 | 0.0718 | λ1U | 0.0000 | 0.0010 | 0.0010 | 0.0001 | ||

| (uWTI, vBDTI) | λ0L | 0.0004 | 0.9703 | 0.9369 | 0.0681 | λ1L | 0.0004 | 0.0010 | 0.0010 | 0.0000 | |

| λ0U | 0.0000 | 0.9240 | 0.7946 | 0.0765 | λ1U | 0.0000 | 0.0010 | 0.0010 | 0.0001 | ||

| (uBrent, vBCTI) | λ0L | 0.0000 | 0.9198 | 0.8231 | 0.0930 | λ1L | 0.0000 | 0.0010 | 0.0010 | 0.0001 | |

| λ0U | 0.0000 | 0.9644 | 0.9142 | 0.0763 | λ1U | 0.0000 | 0.0010 | 0.0010 | 0.0001 | ||

| (uWTI, vBCTI) | η0L | 0.0000 | 0.9825 | 0.7749 | 0.3115 | η1L | 0.0000 | 0.6826 | 0.0723 | 0.1341 | |

| d2时间尺度(中期) | (uBrent,vBDTI) | λ0L | 0.0000 | 0.0012 | 0.0010 | 0.0001 | λ1L | 0.0000 | 0.0010 | 0.0010 | 0.0001 |

| λ0U | 0.0000 | 0.8199 | 0.6837 | 0.0896 | λ1U | 0.0000 | 0.0010 | 0.0010 | 0.0001 | ||

| (uWTI, vBDTI) | λ0L | 0.0000 | 0.0010 | 0.0010 | 0.0001 | λ1L | 0.0000 | 0.0010 | 0.0010 | 0.0001 | |

| λ0U | 0.0000 | 0.7718 | 0.6100 | 0.0967 | λ1U | 0.0000 | 0.0010 | 0.0010 | 0.0001 | ||

| (uBrent, vBCTI) | η0L | 0.0000 | 0.8685 | 0.7981 | 0.0716 | η1L | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| (uWTI, vBCTI) | η0L | 0.0000 | 0.8314 | 0.7921 | 0.0564 | η1L | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| d4时间尺度(长期) | (uBrent,vBDTI) | λ0L | 0.1263 | 0.6167 | 0.4411 | 0.0908 | λ1L | 0.0056 | 0.1263 | 0.0138 | 0.0090 |

| λ0U | 0.1584 | 0.9480 | 0.8680 | 0.0781 | λ1U | 0.0413 | 0.2446 | 0.1224 | 0.0457 | ||

| (uWTI, vBDTI) | η0L | 0.0000 | 0.9825 | 0.7749 | 0.3115 | η1L | 0.0000 | 0.6826 | 0.0723 | 0.1341 | |

| (uBrent, vBCTI) | η0L | 0.0000 | 0.3480 | 0.0369 | 0.0723 | η1L | 0.0000 | 0.6146 | 0.1171 | 0.1677 | |

| (uWTI, vBCTI) | λ0L | 0.0001 | 0.8732 | 0.1863 | 0.2294 | λ1L | 0.0001 | 0.0010 | 0.0010 | 0.0001 | |

| λ0U | 0.0000 | 0.0010 | 0.0010 | 0.0001 | λ1U | 0.0000 | 0.0010 | 0.0010 | 0.0001 |

表7

不同时间尺度下Brent原油市场与油轮细分市场间的时变尾部风险依赖结果"

| 时间尺度 | 收益对 | 尾部风险(S0) | 最小值 | 最大值 | 均值 | 标准差 | 尾部风险(S1) | 最小值 | 最大值 | 均值 | 标准差 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| d1时间尺度(短期) | (uBrent,vAframax) | η0L | 0.0000 | 0.8930 | 0.6300 | 0.1968 | η1L | 0.0000 | 0.3329 | 0.0139 | 0.0438 |

| (uBrent,vPanamax) | η0L | 0.0000 | 0.9814 | 0.7837 | 0.3026 | η1L | 0.0000 | 0.5334 | 0.0521 | 0.1136 | |

| (uBrent,vSuezmax) | η0L | 0.0000 | 0.9331 | 0.4635 | 0.4646 | η1L | 0.0000 | 0.0000 | 0.0000 | 0.0000 | |

| (uBrent, vVLCC) | η0L | 0.0000 | 0.9815 | 0.7968 | 0.2789 | η1L | 0.0000 | 0.7505 | 0.4915 | 0.1708 | |

| d2时间尺度(中期) | (uBrent,vAframax) | λ0L | 0.0000 | 0.8781 | 0.2572 | 0.2356 | λ1L | 0.0000 | 0.0010 | 0.0010 | 0.0001 |

| λ0U | 0.0000 | 0.9858 | 0.6024 | 0.3275 | λ1U | 0.0000 | 0.0010 | 0.0010 | 0.0001 | ||

| (uBrent,vPanamax) | λ0L | 0.0000 | 0.9493 | 0.7944 | 0.1079 | λ1L | 0.0000 | 0.0010 | 0.0010 | 0.0001 | |

| λ0U | 0.0002 | 0.0012 | 0.0010 | 0.0001 | λ1U | 0.0002 | 0.0010 | 0.0010 | 0.0001 | ||

| (uBrent,vSuezmax) | η0L | 0.0000 | 0.9877 | 0.7398 | 0.3546 | η1L | 0.0000 | 0.6920 | 0.0301 | 0.0870 | |

| (uBrent, vVLCC) | η0L | 0.0000 | 0.9848 | 0.7836 | 0.3055 | η1L | 0.0000 | 0.7413 | 0.1160 | 0.1844 | |

| d4时间尺度(长期) | (uBrent,vAframax) | λ0L | 0.0005 | 0.9867 | 0.6066 | 0.3562 | λ1L | 0.0005 | 0.0011 | 0.0010 | 0.0000 |

| λ0U | 0.0000 | 0.2897 | 0.1186 | 0.0640 | λ1U | 0.0000 | 0.0010 | 0.0010 | 0.0001 | ||

| (uBrent,vPanamax) | η0L | 0.0000 | 0.9861 | 0.7447 | 0.3255 | η1L | 0.0000 | 0.8495 | 0.5345 | 0.2274 | |

| (uBrent,vSuezmax) | λ0L | 0.0000 | 0.9758 | 0.9090 | 0.0735 | λ1L | 0.0000 | 0.0010 | 0.0010 | 0.0001 | |

| λ0U | 0.0009 | 0.0010 | 0.0010 | 0.0000 | λ1U | 0.0009 | 0.0010 | 0.0010 | 0.0000 | ||

| (uBrent, vVLCC) | λ0L | 0.0010 | 0.9047 | 0.1204 | 0.2116 | λ1L | 0.0010 | 0.0654 | 0.0013 | 0.0045 | |

| λ0U | 0.0032 | 0.3824 | 0.1296 | 0.0967 | λ1U | 0.0010 | 0.0912 | 0.0014 | 0.0063 |

图5

不同尺度下(uBrent,vAframax)间的时变尾部风险"

| [1] | Choi K H, Yoon S M. Asymmetric dependence between oil prices and maritime freight rates: A time-varying Copula approach[J].Sustainability,2020,12(24): 10687. |

| [2] | Eslami P, Jung K, Lee D, et al. Predicting tanker freight rates using parsimonious variables and a hybrid artificial neural network with an adaptive genetic algorithm[J]. Maritime Economics & Logistics, 2017, 19(3): 538-550. |

| [3] | Shi W M, Yang Z Z, Li K X. The impact of crude oil price on the tanker market[J]. Maritime Policy & Management, 2013, 40(4): 309-322. |

| [4] | Abouarghoub W, Mariscal I B F, Howells P. A two-state Markov-switching distinctive conditional variance application for tanker freight returns[J]. International Journal of Financial Engineering and Risk Management, 2014, 1(3): 239-263. |

| [5] | Alizadeh A H, Huang C Y, van Dellen S. A regime switching approach for hedging tanker shipping freight rates[J]. Energy Economics, 2015, 49: 44-59. |

| [6] | Yang Y Y, Liu C, Sun X L, et al. Spillover effect of international crude oil market on tanker market[J]. International Journal of Global Energy Issues, 2015, 38(41516): 257-277. |

| [7] | Gavriilidis K, Kambouroudis D S, Tsakou K, et al. Volatility forecasting across tanker freight rates: The role of oil price shocks[J]. Transportation Research Part E: Logistics and Transportation Review, 2018, 118: 376-391. |

| [8] | Gong X, Lin B Q. Time-varying effects of oil supply and demand shocks on China's macro-economy[J]. Energy, 2018, 149: 424-437. |

| [9] | Maitra D, Chandra S, Dash S R. Liner shipping industry and oil price volatility: Dynamic connectedness and portfolio diversification[J]. Transportation Research Part E: Logistics and Transportation Review, 2020, 138: 101962. |

| [10] | Chen F E, Miao Y Q, Tian K, et al. Multifractal cross-correlations between crude oil and tanker freight rate[J]. Physica A: Statistical Mechanics and Its Applications, 2017, 474: 344-354. |

| [11] | 冯钰瑶, 刘畅, 孙晓蕾. 不确定性与原油市场的交互影响测度:基于综合集成的多尺度方法论[J]. 管理评论, 2020, 32(7): 29-40. |

| Feng Y Y, Liu C, Sun X L. Measuring the interaction between uncertainty and crude oil market: A multiscale methodology based on synthetic integration[J]. Management Review, 2020, 32(7): 29-40. | |

| [12] | 杨坤, 于文华, 魏宇. 基于R-vine copula的原油市场极端风险动态测度研究[J]. 中国管理科学, 2017, 25(8): 19-29. |

| Yang K, Yu W H, Wei Y. Dynamic measurement of extreme risk among various crude oil markets based on R-vine copula[J]. Chinese Journal of Management Science, 2017, 25(8): 19-29. | |

| [13] | 余乐安, 查锐, 贺凯健,等. 国际油价与中美股价的相依关系研究——基于不同行业数据的分析[J]. 中国管理科学, 2018, 26(11): 74-82. |

| Yu L A, Zha R, He K J, et al. The analysis of dependence relationship between oil and stock prices: Evidence from China and American industrial sector indices[J]. Chinese Journal of Management Science, 2018, 26(11): 74-82. | |

| [14] | Aloui R, Hammoudeh S, Nguyen D K. A time-varying copula approach to oil and stock market dependence: The case of transition economies[J]. Energy Economics, 2013, 39: 208-221. |

| [15] | Liu B Y, Ji Q, Fan Y. Dynamic return-volatility dependence and risk measure of CoVaR in the oil market: A time-varying Mixed-Clayton copula model[J]. Energy Economics, 2017, 68: 53-65. |

| [16] | 赵林海, 陈名智. 金融机构系统性风险溢出和系统性风险贡献——基于滚动窗口动态Copula模型双时变相依视角[J]. 中国管理科学, 2021, 29(7): 71-83. |

| Zhao L H, Chen M Z. Systemic risk spillovers and systemic risk contributions of financial institutions in China: A perspective of dual time-varying dependence of rolling window dynamic copula model[J]. Chinese Journal of Management Science, 2021, 29(7): 71-83. | |

| [17] | 林娟, 吴春晓, 张明. 上海黄金是人民币汇率风险的对冲工具和安全港吗?——基于常量和动态Copula模型[J]. 中国管理科学, 2023, 31(5): 104-115. |

| Lin J, Wu C X, Zhang M. Is Shanghai gold a hedge and a safe haven for the RMB?Based on the constant and time-varying copula models[J]. Chinese Journal of Management Science,2023,31(5): 104-115. | |

| [18] | Alizadeh A H, Nomikos N K. Cost of carry, causality and arbitrage between oil futures and tanker freight markets[J]. Transportation Research Part E: Logistics and Transportation Review, 2004, 40(4): 297-316. |

| [19] | Zhang Y. Investigating dependencies among oil price and tanker market variables by copula-based multivariate models[J]. Energy, 2018, 161: 435-446. |

| [20] | Bai X W, Lam J S L. A Copula-GARCH approach for analyzing dynamic conditional dependency structure between liquefied petroleum gas freight rate, product price arbitrage and crude oil price[J]. Energy Economics, 2019, 78: 412-427. |

| [21] | Sun X L, Liu C, Wang J, et al. Assessing the extreme risk spillovers of international commodities on maritime markets: A GARCH-Copula-CoVaR approach[J]. International Review of Financial Analysis, 2020, 68: 101453. |

| [22] | Fei F, Fuertes A, Kalotychou E. Dependence in credit default swap and equity markets: Dynamic copula with Markov-switching[J]. International Journal of Forecasting, 2017, 33(3): 662-678. |

| [23] | BenSaïda A. The contagion effect in European sovereign debt markets: A regime-switching vine copula approach[J]. International Review of Financial Analysis, 2018, 58: 153-165. |

| [24] | Garcia R, Tsafack G. Dependence structure and extreme comovements in international equity and bond markets[J]. Journal of Banking & Finance, 2011, 35(8): 1954-1970. |

| [25] | Wang Y C, Wu J L, Lai Y H. A revisit to the dependence structure between the stock and foreign exchange markets: A dependence-switching copula approach[J].Journal of Banking & Finance,2013,37(5): 1706-1719. |

| [26] | Ji Q, Bouri E, Roubaud D, et al. Risk spillover between energy and agricultural commodity markets: A dependence-switching CoVaR-copula model[J]. Energy Economics, 2018, 75: 14-27. |

| [27] | 王未卿, 刘祥东, 李慧忠. 房地产股票投资能对冲通货膨胀吗?——基于Markov转换GRG copula的相关性测度研究[J]. 中国管理科学,2020,28(12): 23-34. |

| Wang W Q, Liu X D, Li H Z. Does real estate stock investment hedge inflation?Research on correlation measurement based on Markov-switching GRG copula[J]. Chinese Journal of Management Science, 2020, 28(12): 23-34. | |

| [28] | Ding X X, Dai S Y, Chen F E, et al. Long memory and scaling behavior study of bulk freight rate volatility with structural breaks[J]. Transportation Letters, 2018, 10(6): 343-353. |

| [29] | Leonov Y, Nikolov V. A wavelet and neural network model for the prediction of dry bulk shipping indices[J]. Maritime Economics & Logistics,2012,14(3): 319-333. |

| [30] | Pal D, Mitra S K. Time-frequency contained co-movement of crude oil and world food prices: A wavelet-based analysis[J]. Energy Economics, 2017, 62: 230-239. |

| [31] | He K J, Yu L, Lai K K. Crude oil price analysis and forecasting using wavelet decomposed ensemble model[J]. Energy, 2012, 46(1): 564-574. |

| [32] | Nelson D B. Conditional heteroskedasticity in asset returns: A new approach[J]. Econometrica, 1991, 59(2): 347-370. |

| [33] | Percival D B, Walden A T. Wavelet methods for time series analysis[M]. Cambridge: Cambridge University Press, 2000. |

| [34] | Sklar A. Fonctions de repartition à n dimensions et leurs marges[J]. Publication de l’Institut de Statistique de l’ Université de Paris, 1959(8): 229-231. |

| [35] | Joe H. Multivariate models and dependence concepts[M]. London: Chapman & Hall, 1997. |

| [1] | 文璐, 冯玲. 动态政府干预下银行风险传染与最优救助决策研究[J]. 中国管理科学, 2025, 33(6): 37-48. |

| [2] | 罗长青,刘澜,朱慧明,张敏. 基于多尺度信息份额模型的原油市场定价能力动态演变研究[J]. 中国管理科学, 2024, 32(6): 1-12. |

| [3] | 何汉,李思呈. 基于有向复杂网络的担保圈违约风险传染建模研究[J]. 中国管理科学, 2024, 32(6): 22-33. |

| [4] | 张雪彤,张卫国,王超. 发达市场与新兴市场的尾部风险[J]. 中国管理科学, 2024, 32(4): 14-25. |

| [5] | 黄云洲,黄炯豪,夏晓华. 比特币价格风险、宏观经济波动与股市风险传染[J]. 中国管理科学, 2024, 32(4): 26-37. |

| [6] | 刘映琳, 方艳, 杨金强. 我国粮食与能源的跨市场风险传染及外部冲击[J]. 中国管理科学, 2024, 32(11): 103-114. |

| [7] | 李冰清, 张潇元. 基于网络结构的企业集团内部风险传染机制研究[J]. 中国管理科学, 2023, 31(5): 20-28. |

| [8] | 吴金宴, 王鹏. 基于协高阶矩检验体系的中国资本市场开放与风险传染效应研究[J]. 中国管理科学, 2023, 31(1): 37-46. |

| [9] | 吴金宴, 王鹏. 哪些因素影响了股市风险传染?——来自行业数据的证据[J]. 中国管理科学, 2022, 30(8): 57-68. |

| [10] | 王磊, 李守伟, 陈庭强, 何建敏. 基于企业行为偏好的企业间信用担保网络与风险传染研究[J]. 中国管理科学, 2022, 30(2): 80-93. |

| [11] | 张跃军, 张晗, 王金丽. 考虑结构变化和长记忆性的国际原油价格波动率预测研究[J]. 中国管理科学, 2021, 29(9): 54-64. |

| [12] | 朱小能, 吴杰楠. 股市联动中的“涟漪效应”[J]. 中国管理科学, 2021, 29(8): 1-12. |

| [13] | 陈粘, 黄迅, 严晓凤. 结构突变下的高维汇率资产时变投资组合预测研究[J]. 中国管理科学, 2021, 29(11): 13-22. |

| [14] | 陈庭强, 周文静, 童毛弟, 刘海飞. 融合CDS网络的银行间信用风险传染模型研究[J]. 中国管理科学, 2020, 28(6): 24-37. |

| [15] | 朱鹏飞, 唐勇, 钟莉. 基于小波-高阶矩模型的投资组合策略——以国际原油市场为例[J]. 中国管理科学, 2020, 28(10): 24-35. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||