主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2025, Vol. 33 ›› Issue (8): 14-25.doi: 10.16381/j.cnki.issn1003-207x.2023.1408

吴伟平1,2,3, 林雨4, 金成能5,6,7, 唐振鹏8( )

)

收稿日期:2023-08-23

修回日期:2024-03-20

出版日期:2025-08-25

发布日期:2025-09-10

通讯作者:

唐振鹏

E-mail:zhenpt@126.com

基金资助:

Weiping Wu1,2,3, Yu Lin4, Chengneng Jin5,6,7, Zhenpeng Tang8()

Received:2023-08-23

Revised:2024-03-20

Online:2025-08-25

Published:2025-09-10

Contact:

Zhenpeng Tang

E-mail:zhenpt@126.com

摘要:

最优执行问题作为一类投资决策问题,是金融学术界和实务界都广泛关注的热点话题之一。同时,随机市场流动性、投资者厌恶执行风险以及交易行为受监管限制这三个现实因素显著影响了交易执行策略。故本文基于随机市场深度假设,探究具有常数绝对风险厌恶(CARA)投资者在交易约束制约下的最优执行问题,依据限价订单簿(LOB)市场动态构建随机市场深度下基于风险管理和交易约束的最优执行模型,并利用动态规划方法给出最优执行策略的解析表达式。结果表明,理性投资者不会同时下达相反方向的订单,且最优策略是关于剩余订单量的分段线性函数。数值算例显示,较之风险中性投资者,风险厌恶型投资者为规避风险,倾向于在交易初期执行大规模订单。此外,本文模型在有效管理资产价格变动风险和流动性随机波动风险的同时,还提升了执行策略的有效性。且市场深度和交易约束显著影响了交易执行风险和策略的有效性。研究结果凸显了在解决风险厌恶型投资者的最优执行问题时,同时考虑随机市场流动性和交易约束的重要性。

中图分类号:

吴伟平, 林雨, 金成能, 唐振鹏. 随机市场深度下基于风险管理和交易约束的最优执行问题[J]. 中国管理科学, 2025, 33(8): 14-25.

Weiping Wu, Yu Lin, Chengneng Jin, Zhenpeng Tang. Constrained Optimal Risk Sensitive Execution Problem with Stochastic Market Depth[J]. Chinese Journal of Management Science, 2025, 33(8): 14-25.

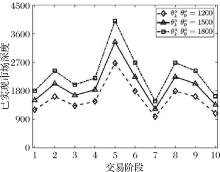

图1

不同初始市场深度情形下的已实现市场深度"

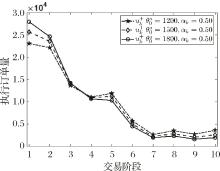

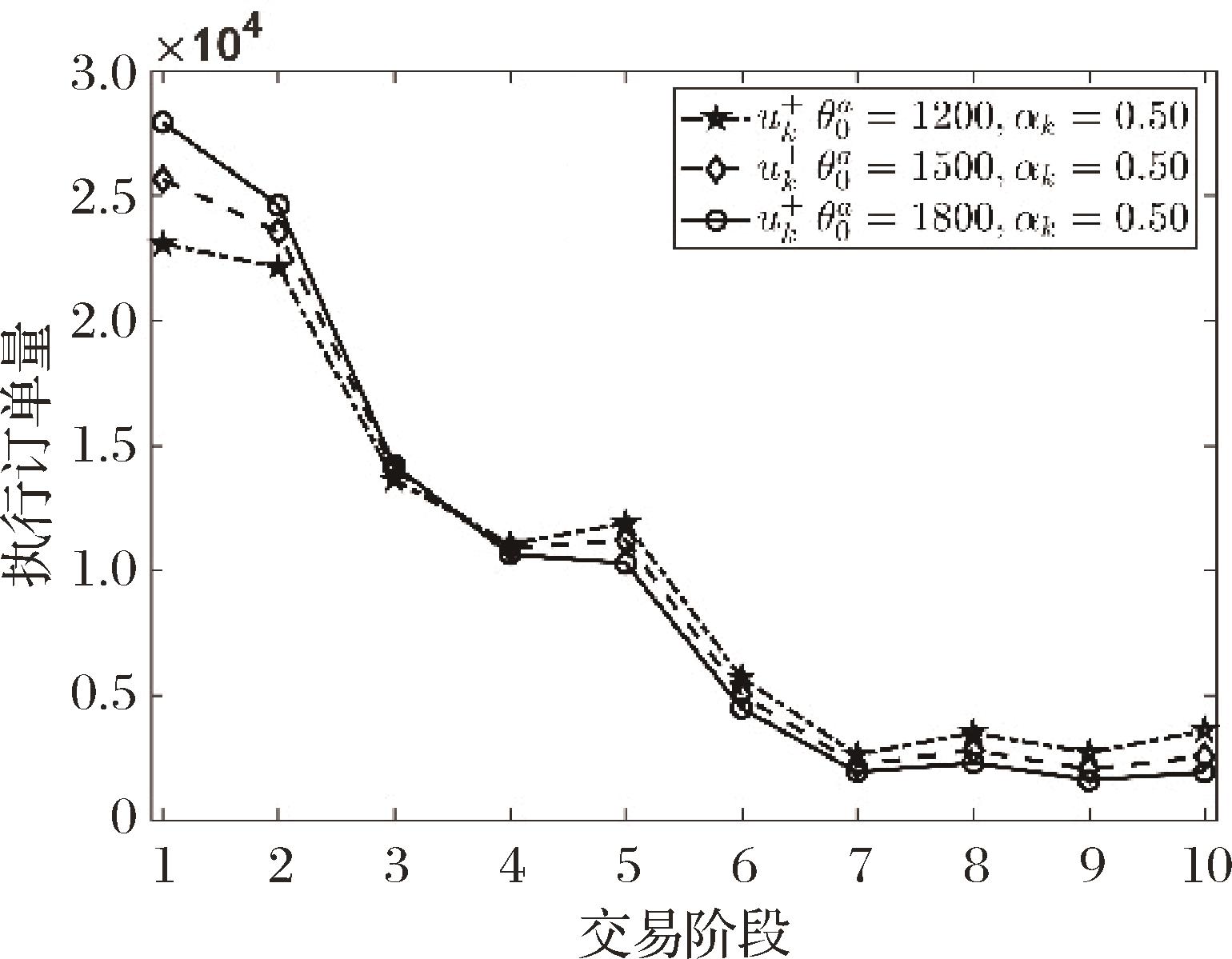

图2

当交易约束上限阈值αk=0.50时,不同初始市场深度情形下𝒫1模型的最优执行策略"

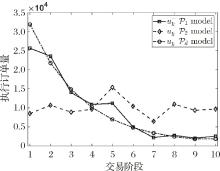

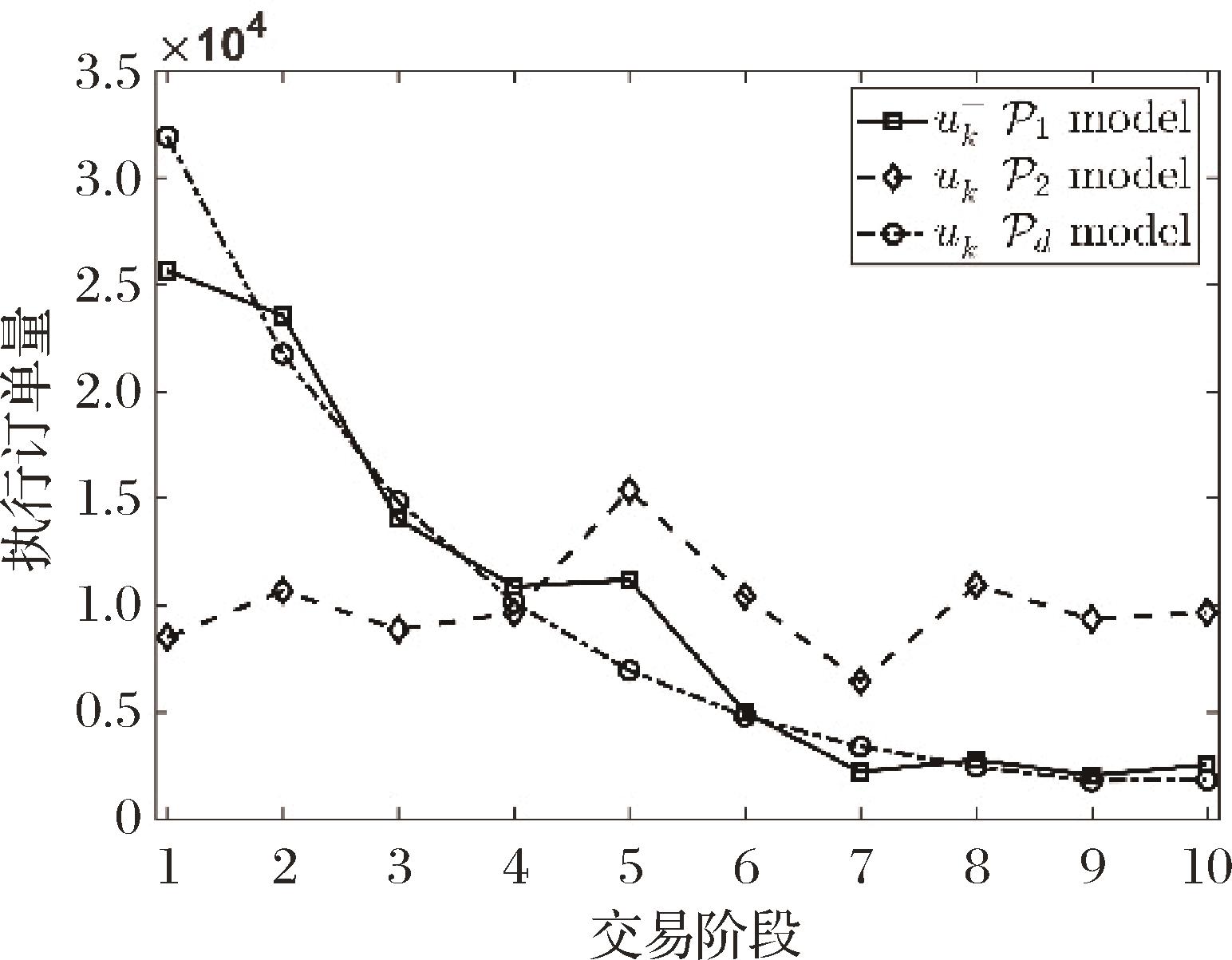

图3

当θ0a=1500,αk=0.50时𝒫1,𝒫2和𝒫d模型的最优执行策略"

图4

当θ0a=1500时不同交易约束情形下𝒫1模型的最优执行策略及可行策略集"

表1

当交易约束上限阈值αk=0.50时,不同初始市场深度θ0a下𝒫1、𝒫2和𝒫d模型价格冲击成本的部分统计量"

| 模型 | 标准差( | 偏度 | 峰度 | 极差( | 执行夏普比率( | |

|---|---|---|---|---|---|---|

| 1200 | 1.19 | -0.11 | 2.96 | 0.92 | 3.06 | |

| 3.08 | 0.72 | 3.76 | 2.58 | 1.25 | ||

| 4.93 | 0.13 | 2.35 | 2.72 | 0.71 | ||

| 1500 | 1.04 | -0.30 | 2.66 | 0.67 | 2.73 | |

| 2.43 | 0.71 | 3.77 | 2.23 | 1.27 | ||

| 4.23 | 0.14 | 2.30 | 2.24 | 0.65 | ||

| 1800 | 0.98 | -0.35 | 2.52 | 0.60 | 2.39 | |

| 2.00 | 0.70 | 3.74 | 1.79 | 1.28 | ||

| 3.69 | 0.14 | 2.24 | 1.89 | 0.61 | ||

| 2100 | 0.95 | -0.40 | 2.65 | 0.57 | 2.07 | |

| 1.75 | 0.69 | 3.71 | 1.59 | 1.26 | ||

| 3.27 | 0.16 | 2.23 | 1.65 | 0.58 |

表2

当初始市场深度θ0a=1500时,不同交易约束上限阈值αk下𝒫1、𝒫2和𝒫d模型价格冲击成本的部分统计量"

| 模型 | 标准差( | 偏度 | 峰度 | 极差( | 执行夏普比率( | |

|---|---|---|---|---|---|---|

0.30 | 2.71 | -0.33 | 2.49 | 1.59 | 1.06 | |

| 2.79 | 0.63 | 3.44 | 2.30 | 1.10 | ||

| 3.92 | 0.14 | 2.34 | 2.17 | 0.72 | ||

0.40 | 1.33 | -0.72 | 3.47 | 0.91 | 2.16 | |

| 2.56 | 0.68 | 3.64 | 2.14 | 1.20 | ||

| 4.19 | 0.13 | 2.29 | 2.22 | 0.66 | ||

0.50 | 1.04 | -0.30 | 2.66 | 0.67 | 2.73 | |

| 2.43 | 0.71 | 3.77 | 2.23 | 1.27 | ||

| 4.23 | 0.14 | 2.30 | 2.24 | 0.65 | ||

0.60 | 0.98 | -0.29 | 2.75 | 0.69 | 2.92 | |

| 2.42 | 0.74 | 3.86 | 2.12 | 1.27 | ||

| 4.23 | 0.14 | 2.29 | 2.24 | 0.65 |

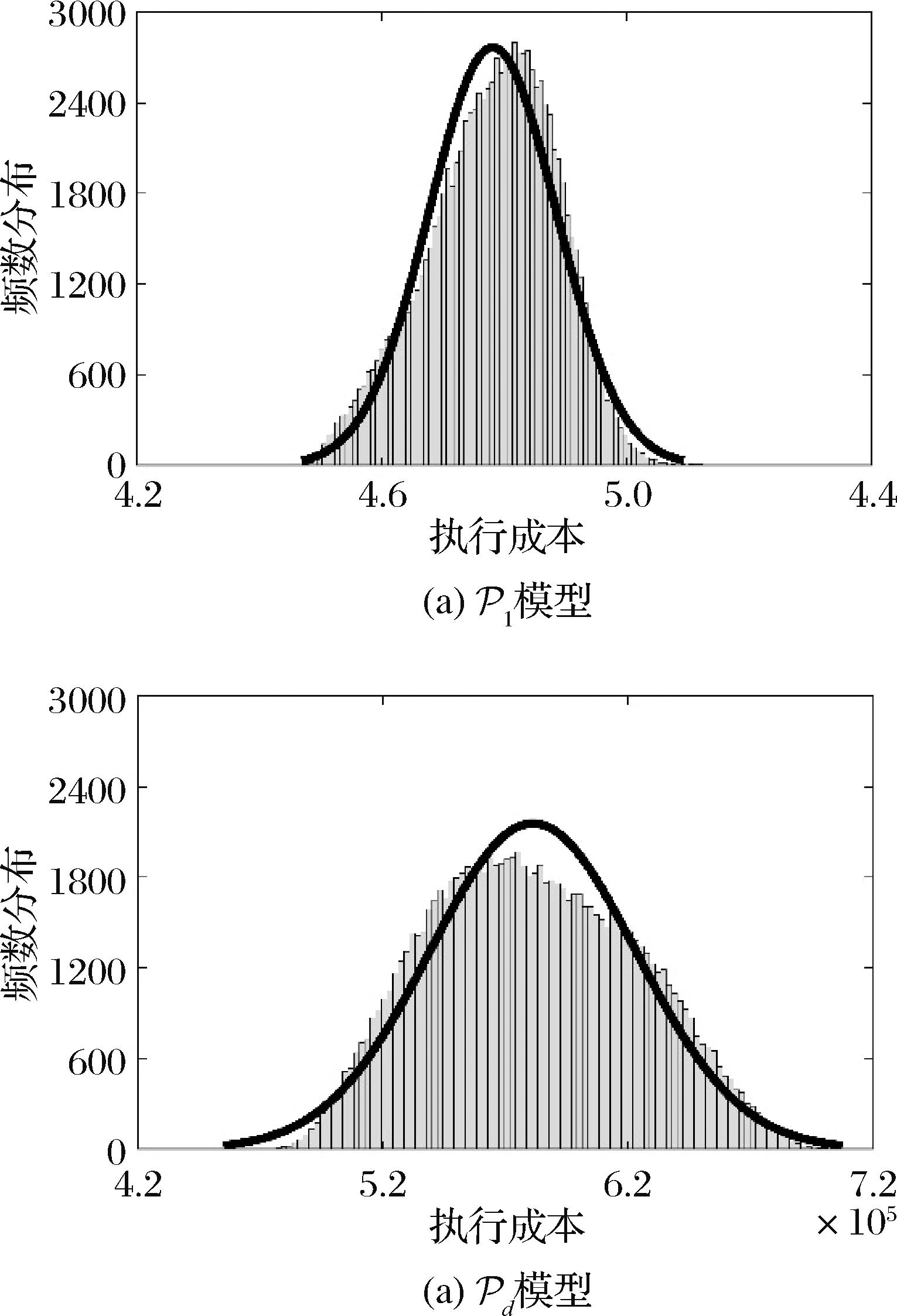

图5

θ0a=1500,αk=0.50时,10万条样本路径下不同模型的价格冲击成本分布"

表3

θ0a=1500,αk=0.50时,不同永久性价格冲击参数ϕ情形下𝒫1模型价格冲击成本的部分统计量"

| ( | 标准差( | 偏度 | 峰度 | 极差( | 执行夏普比率( |

|---|---|---|---|---|---|

| 2 | 1.04 | -0.30 | 2.66 | 0.67 | 2.73 |

| 12 | 1.05 | -0.30 | 2.64 | 0.69 | 2.73 |

| 22 | 1.05 | -0.30 | 2.64 | 0.67 | 2.72 |

| 32 | 1.05 | -0.32 | 2.66 | 0.66 | 2.71 |

表4

θ0a=1500,αk=0.50时,不同证券基础价值白噪声方差σ2情形下𝒫1模型价格冲击成本的部分统计量"

| ( | 标准差( | 偏度 | 峰度 | 极差( | 执行夏普比率( |

|---|---|---|---|---|---|

| 1 | 1.04 | -0.30 | 2.66 | 0.67 | 2.73 |

| 2 | 1.98 | -0.88 | 3.66 | 1.15 | 1.33 |

| 3 | 3.31 | -0.71 | 2.60 | 1.55 | 0.75 |

| 4 | 4.07 | 0.31 | 2.00 | 1.72 | 0.57 |

| [1] | 陈收, 李双飞, 黎传国. 订单差、交易量变化对股票价格的冲击[J].管理科学学报,2010,13(9): 68-75+97. |

| Chen S, Li S F, Li C G. Stock price response to order imbalance and change of volume[J]. Journal of Management Sciences in China, 2010, 13(9): 68-75+97. | |

| [2] | 刘志东, 王超. 多层级指令流不平衡的价格冲击效应研究[J]. 中国管理科学, 2023, 31(12): 11-22. |

| Liu Z D, Wang C. Multi-level order flow imbalance and price impact[J]. Chinese Journal of Management Science, 2023, 31(12): 11-22. | |

| [3] | Bertsimas D, Lo A W. Optimal control of execution costs[J]. Journal of Financial Markets, 1998, 1(1): 1-50. |

| [4] | Obizhaeva A A, Wang J. Optimal trading strategy and supply/demand dynamics[J]. Journal of Financial Markets, 2013, 16(1): 1-32. |

| [5] | Moallemi C C, Wang M. A reinforcement learning approach to optimal execution[J]. Quantitative Finance, 2022, 22(6): 1051-1069. |

| [6] | Neuman E, Voß M. Optimal signal-adaptive trading with temporary and transient price impact[J].SIAM Journal on Financial Mathematics,2022,13(2): 551-575. |

| [7] | 王宇超, 李心丹, 刘海飞. 算法交易的市场影响研究[J]. 管理科学学报, 2014, 17(1): 57-71. |

| Wang Y C, Li X D, Liu H F. Market impact of algorithmic trading[J]. Journal of Management Sciences in China, 2014, 17(1): 57-71. | |

| [8] | Chen N, Kou S, Wang C. A partitioning algorithm for Markov decision processes with applications to market microstructure[J]. Management Science, 2017, 64(2): 784-803. |

| [9] | Siu C C, Guo I, Zhu S P, et al. Optimal execution with regime-switching market resilience[J]. Journal of Economic Dynamics and Control, 2019, 101: 17-40. |

| [10] | 林辉, 杨念, 吴广谋. 证券买卖速度受制约下的最优交易策略[J]. 管理科学学报, 2020, 23(1): 65-76. |

| Lin H, Yang N, Wu G M. Optimal trading strategies with restricted securities buying and selling speeds[J]. Journal of Management Sciences in China, 2020, 23(1): 65-76. | |

| [11] | Cheridito P, Sepin T. Optimal trade execution under stochastic volatility and liquidity[J]. Applied Mathematical Finance, 2014, 21(4): 342-362. |

| [12] | 林辉, 张涤新, 杨浩, 等. 流动性调整的最优交易策略模型研究[J]. 管理科学学报, 2011, 14(5): 65-76. |

| Lin H, Zhang D X, Yang H, et al. Study on liquidity-adjusted optimal trading strategy model[J]. Journal of Management Sciences in China, 2011, 14(5): 65-76. | |

| [13] | Bergault P, Drissi F, Guéant O. Multi-asset optimal execution and statistical arbitrage strategies under Ornstein—Uhlenbeck dynamics[J]. SIAM Journal on Financial Mathematics, 2022, 13(1): 353-390. |

| [14] | Tsoukalas G, Wang J, Giesecke K. Dynamic portfolio execution[J]. Management Science, 2017, 65(5): 2015-2040. |

| [15] | Jin Y. Optimal execution strategy and liquidity adjusted value-at-risk[J]. Quantitative Finance,2017,17(8): 1147-1157. |

| [16] | 刘慕涵, 熊熊. 股指期货交易政策、投资者行为与市场质量[J]. 中国管理科学, 2023, 31(7): 126-139. |

| Liu M H, Xiong X. Stock index futures trading policy, investors’ behavior and stock market quality[J]. Chinese Journal of Management Science, 2023, 31(7): 126-139. | |

| [17] | 尹海员, 吴兴颖. 投资者日度情绪、订单流不均衡与股票流动性[J]. 中国管理科学, 2023, 31(5): 60-70. |

| Yin H Y, Wu X Y. Investor sentiment, order flow imbalance and stock liquidity[J]. Chinese Journal of Management Science, 2023, 31(5): 60-70. | |

| [18] | 储小俊, 刘思峰. 在随机非线性价格冲击下的最优变现策略研究[J].中国管理科学,2007,15(5): 137-142. |

| Chu X J, Liu S F. The investigation of optimal liquidation under stochastic and nonlinear price impact[J]. Chinese Journal of Management Science, 2007, 15(5): 137-142. | |

| [19] | Cartea Á, Sánchez-Betancourt L. Optimal execution with stochastic delay[J]. Finance and Stochastics, 2023, 27(1): 1-47. |

| [20] | Almgren R. Optimal trading with stochastic liquidity and volatility[J]. SIAM Journal on Financial Mathematics, 2012, 3(1): 163-181. |

| [21] | Fukasawa M, Ohnishi M, Shimoshimizu M. Discrete–time optimal execution under a generalized price impact model with Markovian exogenous orders[J]. International Journal of Theoretical and Applied Finance, 2021, 24(5): 2150025. |

| [22] | 冯玲, 林雨, 吴伟平, 等. 随机市场深度下多资产的最优执行问题[J]. 系统工程理论与实践, 2022, 42(7): 1811-1825. |

| Feng L, Lin Y, Wu W P, et al. The optimal portfolio execution problem with the stochastic market depth[J]. Systems Engineering-Theory & Practice, 2022, 42(7): 1811-1825. | |

| [23] | Markov V, Mazur S, Saltz D. Design and implementation of schedule-based Trading Strategies based on uncertainty bands[J]. The Journal of Trading, 2011, 6(4): 45-52. |

| [24] | Wu W, Gao J, Li D, et al. Explicit solution for constrained scalar-state stochastic linear-quadratic control with multiplicative noise[J]. IEEE Transactions on Automatic Control, 2019, 64(5): 1999-2012. |

| [1] | 姚银红, 王晓旭, 陈炜, 陈振松. 基于Transformer-LSTM分位数回归的全球股市极端风险溢出研究[J]. 中国管理科学, 2025, 33(8): 1-13. |

| [2] | 田军, 董赞强, 李雅丽. 基于预付账款融资模式的供应链融资策略研究[J]. 中国管理科学, 2025, 33(7): 272-283. |

| [3] | 杨科, 刘鑫, 田凤平. 中国与其他主要新兴市场国家间股市极端风险的跨市场传染[J]. 中国管理科学, 2025, 33(7): 44-53. |

| [4] | 欧阳资生, 周学伟. 中国金融机构系统性风险回测与关联研究[J]. 中国管理科学, 2025, 33(6): 14-26. |

| [5] | 沈根祥, 周泽峰. 拟得分驱动条件异方差自回归极差模型及其实证研究[J]. 中国管理科学, 2025, 33(5): 34-44. |

| [6] | 冯浩原, 吴颉, 于安琪, 郭琨. 杠杆交易会提高股票市场的流动性吗?——基于微观个股层面的实证分析[J]. 中国管理科学, 2025, 33(4): 1-11. |

| [7] | 姚海祥, 刘秋瑜, 杨晓光. 增强还是减弱:新型金融与传统金融行业之间系统性风险溢出[J]. 中国管理科学, 2025, 33(3): 1-12. |

| [8] | 王纲金, 马欣宇, 谢赤. 基于尾部风险溢出网络的全球外汇市场关联性研究[J]. 中国管理科学, 2025, 33(3): 13-23. |

| [9] | 许帅, 邵帅, 何贤杰. 业绩说明会前瞻性信息对分析师盈余预测准确性的影响[J]. 中国管理科学, 2025, 33(3): 34-44. |

| [10] | 孙庆文, 靳玉, 郑立梅, 孙子涵. 企业净资产收益率操纵度量模型与识别方法[J]. 中国管理科学, 2025, 33(2): 1-15. |

| [11] | 胡玉真, 刘建霞. 基于消冗时段网络的集装箱班轮干扰恢复研究[J]. 中国管理科学, 2025, 33(2): 118-130. |

| [12] | 马梦迪, 李烁, 王玉涛. 中国分析师报告有效性研究:特定信息与投资者有限关注[J]. 中国管理科学, 2025, 33(2): 38-49. |

| [13] | 宋诗佳, 田飞, 李汉东. 基于时变极值方法的VaR预测模型以及应用[J]. 中国管理科学, 2025, 33(2): 61-70. |

| [14] | 李星毅, 李仲飞, 李其谦, 刘昱君, 唐文金. 基于机器学习的资产收益率预测研究综述[J]. 中国管理科学, 2025, 33(1): 311-322. |

| [15] | 陈张杭健, 任飞. 交互作用视角下股吧信息扩散与股价联动关系研究[J]. 中国管理科学, 2024, 32(12): 25-36. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||