主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2023, Vol. 31 ›› Issue (8): 61-70.doi: 10.16381/j.cnki.issn1003-207x.2021.2382

马勇,刘晓君,胡荣才( )

)

收稿日期:2021-11-16

修回日期:2022-01-21

出版日期:2023-08-15

发布日期:2023-08-24

通讯作者:

胡荣才

E-mail:Rongcaihu@hnu.edu.cn

基金资助:

Yong MA,Xiao-jun LIU,Rong-cai HU()

Received:2021-11-16

Revised:2022-01-21

Online:2023-08-15

Published:2023-08-24

Contact:

Rong-cai HU

E-mail:Rongcaihu@hnu.edu.cn

摘要:

本文首先在单一商品经济体框架下阐述通胀预期和通胀预测误差影响股票收益的微观机理。然后,基于长短期非对称视角,运用非线性自回归分布滞后(NARDL)模型对我国通胀预期和股票收益之间的非线性累积动态效应进行实证研究。研究发现,通胀预期和通胀预测误差对股票收益的影响均是非对称的,且长短期影响具有异质性。具体而言,通胀预期和通胀预测误差的弱化对股票收益的影响更为显著;通胀预期、通胀预测误差对股票收益的正向影响主要表现在短期,长期内它们对股票收益具有抑制作用,说明股票投资仅能在短期内抵御通胀风险。机制检验表明,利率和投资者情绪是预期通胀与通胀预测误差影响股票收益的两条重要渠道。

中图分类号:

马勇,刘晓君,胡荣才. 通胀预期、通胀预测误差与股票收益的非线性动态效应[J]. 中国管理科学, 2023, 31(8): 61-70.

Yong MA,Xiao-jun LIU,Rong-cai HU. The Nonlinear Dynamics Assessment of Inflation Expectations, Inflation Surprise and Stock: ReturnsTheoretical Analysis and Empirical Research[J]. Chinese Journal of Management Science, 2023, 31(8): 61-70.

表1

变量说明"

| 变量类型 | 变量名称 | 度量方法 |

|---|---|---|

| 被解释变量 | 股票收益率 | 上证综指收益率月度数据转化 |

| 解释变量 | 通胀预期 | 央行问卷调查的通胀预期指数计算 |

| 通胀预测误差 | 通货膨胀率-通胀预期率 | |

| 通货膨胀率 | 月度消费者物价指数转化得来 | |

| 控制变量 | 经济增长率 | 季度GDP增长率 |

| 货币供应量 | 同比增长率 | |

| 中介变量 | 利率 | 月度同业拆借利率按时间加权平均 |

| 投资者情绪 | 月度投资者情绪取均值得到 |

表2

描述性统计"

| 变量 | 均值 | 中位数 | 最大值 | 最小值 | 标准差 |

|---|---|---|---|---|---|

| R | 0.008 | 0.002 | 0.135 | -0.120 | 0.056 |

| EI | 0.025 | 0.031 | 0.035 | -0.011 | 1.056 |

| UI | -0.007 | -1.991 | 1.383 | -0.428 | 17.504 |

| CPI | 0.023 | 0.008 | 1.413 | -0.430 | 16.878 |

| GDP | 0.037 | 0.083 | 0.210 | -0.257 | 0.113 |

| M2 | 0.012 | 0.012 | 0.038 | -0.002 | 0.006 |

| IR | 0.028 | 0.028 | 0.047 | 0.010 | 0.846 |

| ISI | -0.020 | -0.148 | 4.870 | -2.203 | 1.412 |

表3

单位根检验结果"

| 变量 | ADF检验 | PP检验 | 结果 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| t 值 | 临界值 | t 值 | 临界值 | ||||||

| 1% | 5% | 10% | 1% | 5% | 10% | ||||

| R | -7.078 | -3.517 | -2.899 | -2.587 | -7.170 | -3.517 | -2.899 | -2.587 | 平稳 |

| EI | -2.376 | -3.520 | -2.901 | -2.588 | -1.991 | -3.517 | -2.899 | -2.587 | 不平稳 |

| -7.181 | -3.520 | -2.901 | -2.588 | -7.452 | -3.518 | -2.900 | -2.587 | 平稳 | |

| UI | -8.879 | -3.517 | -2.899 | -2.587 | -8.879 | -3.517 | -2.899 | -2.587 | 平稳 |

| CPI | -8.868 | -3.517 | -2.899 | -2.587 | -8.868 | -3.517 | -2.899 | -2.587 | 平稳 |

表4

长期协整关系检验结果"

| 变量 | 模型(16) |

|---|---|

| -10.068 *** | |

| 4.770*** |

表5

长、短期非对称性检验结果"

| 短期非对称性 | 长期非对称性 | ||

|---|---|---|---|

| 2.939* (0.092) | 7.848***(0.007) | ||

| 2.082* (0.094) | 12.006**(0.001) | ||

表6

模型(21)的长、短期估计系数"

| 变量 | 短期估计系数 | 变量 | 长期估计系数 |

|---|---|---|---|

| 3.911***(0.002) | -4.193***(0.005) | ||

| 2.850**(0.020) | -4.800***(0.000) | ||

| 5.617***(0.000) | -1.733***(0.005) | ||

| 3.266***(0.005) | -0.706***(0.000) | ||

| 1.187*(0.012) | — | — | |

| 1.160**(0.023) | — | — | |

| 1.506**(0.033) | — | — | |

| 1.991***(0.000) | — | — | |

| 长期传递系数 | |||

| -5.938***(0.001) | 0.157(0.487) | ||

| -6.796***(0.001) | -2.454***(0.002) | ||

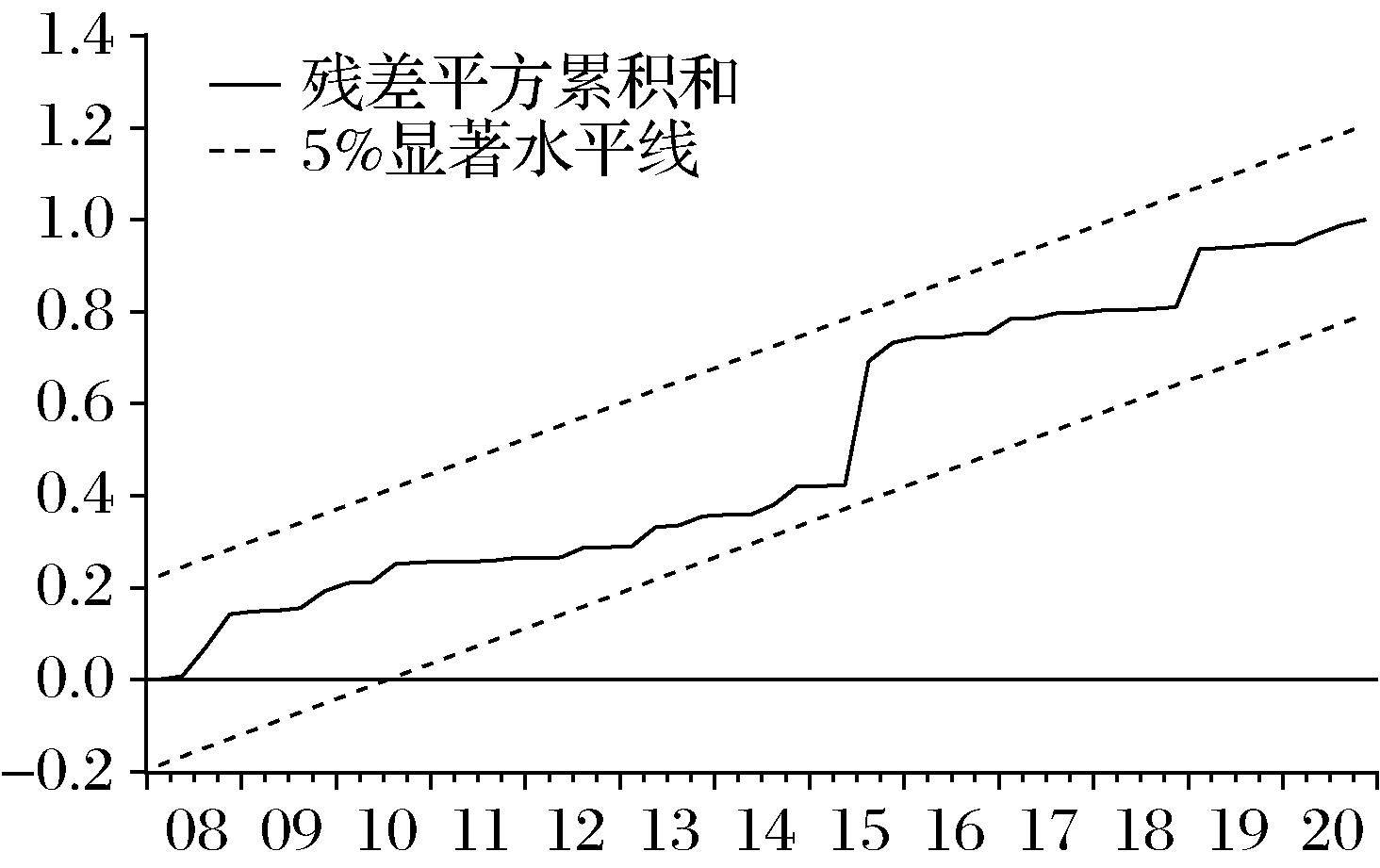

图1

模型稳定性检验"

表7

影响渠道:利率的影响"

| 模型(22)的长、短期估计系数 | 模型(24)的长、短期估计系数 | ||||||

|---|---|---|---|---|---|---|---|

| 变量 | 短期估计系数 | 变量 | 长期估计系数 | 变量 | 短期估计系数 | 变量 | 长期估计系数 |

| -1.950*(0.052) | 1.318*(0.071) | 2.983**(0.001) | -1.908**(0.016) | ||||

| -7.102***(0.001) | 6.476***(0.001) | 0.267*(0.074) | -1.924**(0.028) | ||||

| -3.447**(0.025) | 6.922***(0.001) | -0.441**(0.005) | -0.708**(0.046) | ||||

| -4.193***(0.003) | — | — | — | — | 0.283**(0.043) | ||

| -6.483***(0.002) | — | — | — | — | -0.786***(0.001) | ||

| -7.048***(0.001) | — | — | — | — | — | — | |

| -2.854*(0.078) | — | — | — | — | — | — | |

| -3.797*(0.007) | — | — | — | — | — | — | |

表8

影响渠道:投资者情绪的影响"

| 模型(23)的长、短期估计系数 | 模型(25)的长、短期估计系数 | ||||||

|---|---|---|---|---|---|---|---|

| 变量 | 短期估计系数 | 变量 | 长期估计系数 | 变量 | 短期估计系数 | 变量 | 长期估计系数 |

| 7.176**(0.000) | -10.204***(0.000) | 1.193(0.108) | -2.594***(0.000) | ||||

| 5.385***(0.002) | -9.814***(0.000) | 1.237(0.168) | -3.447***(0.000) | ||||

| 3.727*(0.060) | -12.628**(0.020) | 3.264***(0.000) | -1.451***(0.002) | ||||

| 10.190***(0.000) | -19.505***(0.000) | 1.419*(0.065) | 0.352***(0.002) | ||||

| 10.131***(0.000) | — | — | 0.941*(0.064) | 0.944***(0.000) | |||

| 1.160**(0.023) | — | — | 1.546***(0.000) | — | — | ||

| 1.506**(0.033) | — | — | — | — | — | — | |

| 13.560***(0.010) | — | — | — | — | — | — | |

| 9.581**(0.014) | — | — | — | — | — | — | |

| 17.112***(0.001) | — | — | — | — | — | — | |

| 10.783**(0.022) | — | — | — | — | — | — | |

表9

模型(21)的长、短期估计系数"

| 变量 | 短期估计系数 | 变量 | 长期估计系数 |

|---|---|---|---|

| 2.951*(0.082) | -1.930***(0.000) | ||

| 3.751**(0.035) | 2.410***(0.002) | ||

| 0.711**(0.015) | -1.091**(0.019) | ||

| 0.396*(0.079) | -2.049***(0.000) | ||

| 0.536**(0.018) | — | — | |

| 0.437**(0.013) | — | — | |

| 0.329*(0.055) | — | — |

表10

模型(21)的长、短期估计系数"

| 变量 | 短期估计系数 | 变量 | 长期估计系数 |

|---|---|---|---|

| 5.749**(0.014) | -6.173***(0.001) | ||

| 4.934**(0.019) | -6.748***(0.001) | ||

| 3.744**(0.047) | -1.862(0.543) | ||

| 4.187**(0.021) | — | — | |

| 6.723***(0.001) | — | — | |

| 3.802*(0.098) | — | — | |

| 5.464**(0.016) | — | — | |

| 5.196***(0.010) | — | — | |

| 3.855*(0.056) | — | — | |

| -1.285***(0.010) | — | — | |

| -0.845*(0.083) | — | — |

| 1 | Duca-Radu I, Kenny G, Reuter A. Inflation expectations, consumption and the lower bound: micro evidence from a large multi-country survey[J]. Journal of Monetary Economics, 2021,(118): 120-134. |

| 2 | 洪智武, 牛霖琳. 中国通胀预期及其影响因素分析——基于混频无套利Nelson-Siegel利率期限结构扩展模型[J].金融研究, 2020(12): 95-113. |

| Hong Zhiwu, Niu Linlin. Analysis of inflation expectations in China and their determinants:based on a mixed frequency no-arbitrage Nelson-Siegel extended model[J]. Journal of Financial Research, 2020(12): 95-113. | |

| 3 | Fisher I. The Theory of Interest[M]. New York: McMillan, 1930. |

| 4 | Zhao Liuyan. Stock returns under hyperinflation: evidence from China 1945-48[J]. China Economic Review, 2017, 45(155): 155-167. |

| 5 | Arjoon R, Botes M, Chesang L K, et al. The long-run relationship between inflation and real stock prices: empirical evidence from South Africa[J]. Journal of Business Economics and Management,2012,13(4): 600-613. |

| 6 | Bekaert G, Engstrom E. Inflation and the stock market: understanding the“Fed Model”[J]. Journal of Monetary Economics, 2010, 57(3): 278-294. |

| 7 | 赵留彦.股票收益与通货膨胀: 中国恶性通胀时期的实证研究[J]. 经济学(季刊), 2016, 15(2): 479-498. |

| Zhao Liuyan. Stock return and inflation: a short-horizon perspective in the Chinese hyperinflation[J]. China Economic Quarterly, 2016, 15(2): 479-498. | |

| 8 | Modigliani F, Cohn R A. Inflation, rational valuation and the market[J]. Financial Analysts Journal, 1979, 35(2): 24-44. |

| 9 | Campbell J Y, Vuolteenaho T. Inflation illusion and stock prices[J]. The American Economic Review, 2004, 94(2): 19-23. |

| 10 | Lee B S. Stock returns and inflation revisited: an evaluation of the inflation illusion hypothesis[J]. Journal of Banking & Finance, 2010, 34: 1257-1273. |

| 11 | 张宗新, 朱伟骅. 通胀幻觉、预期偏差和股市估值[J]. 金融研究, 2010(5): 116-132. |

| Zhang Zongxin, Zhu Weihua. Inflation illusion,expectation bias and stock market evaluation[J]. Journal of Financial Research, 2010(5): 116-132. | |

| 12 | Brown W O, Huang Dayong, Wang Fang. Inflation illusion and stock returns[J]. Journal of Empirical Finance, 2016, 35(1): 14-24. |

| 13 | Fama E F. Stock returns, real activity, inflation, and money[J]. The American Economic Review, 1981, 71(4): 545-565. |

| 14 | 刘金全, 王风云. 资产收益率与通货膨胀率关联性的实证分析[J]. 财经研究, 2004(1): 123-128. |

| Liu Jinquan, Wang Fengyun. A positive analysis of the dynamic relationship between stock returns and inflation[J]. Journal of Finance and Economics, 2004(1): 123-128. | |

| 15 | Alagidede P, Panagiotidis T. Stock returns and inflation: evidence from quantile regressions[J]. Economic Letters, 2012, 117(1): 283-286. |

| 16 | Madadpour S, Asgari M. The puzzling relationship between stocks return and inflation: a review article[J]. International Review of Economics,2019,66:115-145. |

| 17 | Li Lifang, Narayan P K, Zheng Xinwei. An analysis of inflation and stock returns for the UK[J]. Journal of international Financial Markets,Institutions and Money, 2010, 20(5): 519-532. |

| 18 | Omay T, Yuksel A. An empirical examination of the generalized Fisher effect using cross-sectional correlation robust tests for panel cointegration[J]. Journal of International Financial Markets,Institutions and Money, 2015, 35: 18-29. |

| 19 | Kim J H, Ryoo H H. Common stocks as a hedge against inflation: Evidence from century- long US data[J]. Economic Letters, 2011, 113(2): 168-171. |

| 20 | 王未卿, 刘祥东, 李慧忠. 房地产股票投资能对冲通货膨胀吗?——基于Markov转换GRG copula的相关性测度研究[J]. 中国管理科学, 2020, 28(12): 23-34. |

| Wang Weiqing, Liu Xiangdong, Li Huizhong. Does real estate stock investment hedge inflation? Research on correlation measurement based on Markov-switching GRG Copula[J]. Chinese Journal of Management Science, 2020, 28(12): 23-34. | |

| 21 | Knif J, Kolari J, Pynnonen S. Stock market reaction to good and bad inflation news[J]. Journal of Financial Research, 2008, 31(2): 141-166. |

| 22 | Salisu A, Ndako U. Modelling stock price- exchange rate nexus in OECD countries: a new perspective[J]. Economic Modelling, 2018, 74: 105-123. |

| 23 | Zhou John C. The Good, the bad, and the ambiguous: the aggregate stock market dynamics around macroeconomic news[B]. Social Science Electronic Publishing, 2015. |

| 24 | Nusair S A, Al-Khasawneh J A. On the relationship between Asian exchange rates and stock prices: a nonlinear analysis[J]. Economic Change and Restructuring, 2021,55(1):361-400. |

| 25 | 汪红驹, 张慧莲. 资产选择、风险偏好与储蓄存款需求[J]. 经济研究, 2006(6): 48-58. |

| Wang Hongju, Zhang Huilian. Portfolio choice, risk preference and the demand for savings deposit[J]. Economic Research Journal, 2006(6): 48-58. | |

| 26 | 唐振鹏, 吴俊传, 冉梦, 等.考虑投资者情绪的中国股市自激发效应研究[J]. 中国管理科学, 2020, 28(7): 1-12. |

| Tang Zhenpeng, Wu Junchuan, Ran Meng, et al. Research on the self-exciting effect of Chinese stock market considering investor sentiment[J]. Chinese Journal of Management Science, 2020, 28(7): 1-12. | |

| 27 | 饶品贵, 张会丽. 通货膨胀预期与企业现金持有行为[J]. 金融研究, 2015(1): 101-116. |

| Rao Pingui, Zhang Huili. Expected inflation and firms’ behavior of cash holdings[J].Journal of Financial Rese-arch, 2015(1): 101-116. | |

| 28 | 黎文靖, 郑曼妮.通货膨胀预期、企业成长性与企业投资[J].统计研究, 2016, 33(5): 34-42. |

| Li Wenjing, Zheng Manni. Inflation expectation, growth and firm investment[J]. Statistical Research, 2016, 33(5): 34-42. | |

| 29 | 林建浩, 王美今. 通货膨胀与股票收益的关系研究——基于具有财务杠杆与货币效用的资产定价模型[J]. 金融研究, 2011(9): 93-106. |

| Lin Jianhao, Wang Meijin. A study on the relationship between inflation and stock returns:based on asset pricing model with financial leverage and monetary utility[J]. Journal of Financial Research, 2011(9): 93-106. | |

| 30 | Baker M, Wurgler J. Investor sentiment and the cross-section of stock returns[J]. The Journal of Finance, 2006(4): 1645-1680. |

| 31 | 陈文博, 陈浪南, 王升泉. 投资者的博彩行为研究——基于盈亏状态和投资者情绪的视角[J]. 中国管理科学, 2019, 27(2): 19-30. |

| Chen Wenbo, Chen Langnan, Wang Shengquan. Investors’ gambling behavior:a perspective from profit/loss condition and investor sentiment[J]. Chinese Journal of Management Science, 2019, 27(2): 19-30. | |

| 32 | 武佳薇, 汪昌云, 陈紫琳, 等.中国个人投资者处置效应研究——一个非理性信念的视角[J]. 金融研究, 2020(2): 147-166. |

| Wu Jiawei, Wang Changyun, Chen Zilin, et al. A study of disposition effect among China’s individual investors: the perspective of irrational beliefs[J]. Journal of Financial Research, 2020(2): 147-166. | |

| 33 | 张凌翔, 张晓峒. 通货膨胀率周期波动与非线性动态调整[J]. 经济研究, 2011, 46(5): 17-31. |

| Zhang Lingxiang, Zhang Xiaotong. Cyclical fluctuations and nonlinear dynamics of inflation rate[J]. Economic Research Journal, 2011, 46(5): 17-31. | |

| 34 |

Shin Y, Yu B, GreenwoodNimmo M. Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework[J]. SSRN Electronic Journal,2014,DOI:10.1007/978-1-4899-8008-3_9.

doi: 10.1007/978-1-4899-8008-3_9. |

| 35 | 李胜旗, 毛其淋. 制造业上游垄断与企业出口国内附加值——来自中国的经验证据[J].中国工业经济, 2017(3): 101-119. |

| Li Shengqi, Mao Qilin. Upstream monopoly and domestic value added of manufacturing firms’ exports:empirical evidence from China[J]. China’s Industrial Economics, 2017(3): 101-119. | |

| 36 | 强静, 侯鑫, 范龙振. 基准利率、预期通胀率和市场利率期限结构的形成机制[J]. 经济研究, 2018, 53(4): 92-107. |

| Qiang Jing, Hou Xin, Fan Longzhen. Base interest rate,expected inflation and the mechanism for determining the term structure of market interest rates in China[J]. Economic Research Journal, 2018, 53(4): 92-107. | |

| 37 | 陈坚, 张轶凡.中国股票市场的已实现偏度与收益率预测[J].金融研究, 2018(9): 107-125. |

| Chen Jian, Zhang Yifan. Realized skewness of Chinese stock market and the predictability of stock return[J]. Journal of Financial Research, 2018(9): 107-125. |

| [1] | 张莉莉, 杨文文, 罗冠聪. 面向时间优化的“任务-人员”匹配逆最优值方法:以石化设备抢修为例[J]. 中国管理科学, 2023, 31(6): 276-286. |

| [2] | 李德昌, 杨华龙, 宋巍, 郑建风. 考虑船舶速度偏差的集装箱班轮运输货运收益鲁棒优化[J]. 中国管理科学, 2023, 31(4): 151-160. |

| [3] | 戢守峰, 刘红玉, 赵鹏云, 戢婷婷. 基于PI的企业动态库存补货模型与算法[J]. 中国管理科学, 2023, 31(2): 205-214. |

| [4] | 张鹏,党世力,黄梅雨,李璟欣. 基于机器学习预测股票收益率的两步骤M-SV投资组合优化[J]. 中国管理科学, 2023, 31(12): 96-106. |

| [5] | 贺俊, 韩汶衍, 毕功兵. 直接融资结构对经济发展的非线性影响[J]. 中国管理科学, 2023, 31(1): 47-55. |

| [6] | 董乾东, 李敏. 考虑不同碳排放处理模式的动态供应商选择及采购批量问题研究[J]. 中国管理科学, 2022, 30(8): 106-116. |

| [7] | 赵泉午, 姚珍珍, 林娅. 面向新零售的生鲜连锁企业城市配送网络优化研究[J]. 中国管理科学, 2021, 29(9): 168-179. |

| [8] | 李爱忠, 任若恩, 董纪昌. 金融网络风险下多因子矩阵回归的资产组合与定价[J]. 中国管理科学, 2021, 29(6): 1-9. |

| [9] | 翟东升, 李梦洋, 何喜军, 徐硕. 非线性技术演化条件下的专利研发投资决策研究[J]. 中国管理科学, 2021, 29(12): 168-178. |

| [10] | 邓春生. 基于非线性系统稳定性理论的P2P网络借贷三方演化博弈分析[J]. 中国管理科学, 2021, 29(11): 134-145. |

| [11] | 陆晓琴, 冯玲, 丁剑平. 汇率货币模型的非线性协整关系检验——基于深度GRU神经网络[J]. 中国管理科学, 2020, 28(5): 1-13. |

| [12] | 刘维奇, 张燕. 资产定价与劳动成本占比[J]. 中国管理科学, 2020, 28(12): 1-11. |

| [13] | 胡鸿韬, 边迎迎, 郭书源, 王帅安, 严伟. 考虑定价和需求关系的供应链网络优化研究[J]. 中国管理科学, 2020, 28(10): 165-171. |

| [14] | 张敏, 余乐安, 刘凤根. 生猪产业链价格的区制转移与非线性动态调整行为研究[J]. 中国管理科学, 2020, 28(1): 45-56. |

| [15] | 马超群, 徐光鲁, 刘伟, 贾钰, 赵新伟. 询价制度改革、知情交易者概率与IPO溢价[J]. 中国管理科学, 2018, 26(8): 1-12. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||