主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2025, Vol. 33 ›› Issue (8): 61-74.doi: 10.16381/j.cnki.issn1003-207x.2024.0109

景鹏1( ), 任成一1, 寇纲2

), 任成一1, 寇纲2

收稿日期:2024-01-23

修回日期:2024-07-19

出版日期:2025-08-25

发布日期:2025-09-10

通讯作者:

景鹏

E-mail:jingpeng@swufe.edu.cn

基金资助:

Peng Jing1(), Chengyi Ren1, Gang Kou2

Received:2024-01-23

Revised:2024-07-19

Online:2025-08-25

Published:2025-09-10

Contact:

Peng Jing

E-mail:jingpeng@swufe.edu.cn

摘要:

社会保险降费对减轻企业负担和激发企业活力发挥了积极作用。基于上市公司网络招聘数据,本文采用双重差分方法考察了社会保险降费对企业劳动力需求结构的影响。研究结果显示,社会保险降费显著促进了企业劳动力需求结构升级,该效应在非国有企业和高融资约束企业以及政府设定较低就业目标和人才落户门槛的地区企业更明显。机制检验表明,社会保险降费主要通过资本—技能互补效应和流动性约束缓解效应扩大了企业对高技能劳动力的相对需求。进一步研究发现,社会保险降费不仅提高了企业招聘学历门槛,还提升了高技能劳动力实际雇佣比例,证实企业不存在策略性招聘行为。本文结论对于完善社会保险缴费制度和推动企业高质量发展具有重要启示意义。

中图分类号:

景鹏, 任成一, 寇纲. 社会保险降费与企业劳动力需求结构升级[J]. 中国管理科学, 2025, 33(8): 61-74.

Peng Jing, Chengyi Ren, Gang Kou. Reduction in Social Insurance Contributions and the Upgrade of Corporate Labor Demand Structure: Evidence from Internet Recruitment of Listed Companies[J]. Chinese Journal of Management Science, 2025, 33(8): 61-74.

表1

变量描述性统计结果"

| 变量 | 样本量 | 均值 | 标准差 | 最小值 | 最大值 |

|---|---|---|---|---|---|

| Lds | 14591 | 3.6366 | 1.2878 | 0 | 11.1125 |

| HL | 14591 | 0.9553 | 7.6108 | 0 | 670 |

| Treat×Post | 14591 | 0.3072 | 0.4613 | 0 | 1 |

| Brir | 14591 | 0.1737 | 0.3464 | -0.5023 | 1.7667 |

| ROE | 14591 | 0.0603 | 0.1417 | -0.6940 | 0.3407 |

| Age | 14591 | 2.9870 | 0.2852 | 2.1972 | 3.5264 |

| Top10 | 14591 | 0.5834 | 0.1484 | 0.2497 | 0.9018 |

| Dual | 14591 | 0.3149 | 0.4645 | 0 | 1 |

| Cfo | 14591 | 0.0486 | 0.0649 | -0.1367 | 0.2305 |

| Lev | 14591 | 0.4249 | 0.1954 | 0.0675 | 0.8838 |

表2

基准回归结果"

| 变量 | (1) | (2) | (3) |

|---|---|---|---|

| Treat×Post | 0.0985*** | 0.1022*** | 0.1009*** |

| (0.0326) | (0.0328) | (0.0294) | |

| Brir | 0.0198 | 0.0077 | |

| (0.0318) | (0.0322) | ||

| ROE | 0.0838 | 0.0773 | |

| (0.0776) | (0.0847) | ||

| Age | -0.0475 | -0.1424 | |

| (0.2436) | (0.2780) | ||

| Top10 | 0.0721 | 0.1345 | |

| (0.2063) | (0.2078) | ||

| Dual | -0.0163 | -0.0283 | |

| (0.0384) | (0.0369) | ||

| Cfo | 0.0239 | -0.0187 | |

| (0.1244) | (0.1367) | ||

| Lev | -0.2214** | -0.1862* | |

| (0.1079) | (0.1059) | ||

| 常数项 | 3.6204*** | 3.8092*** | 4.0499*** |

| (0.0053) | (0.7666) | (0.8735) | |

| 企业固定效应 | Yes | Yes | Yes |

| 年份固定效应 | Yes | Yes | Yes |

| 行业—年份固定效应 | No | No | Yes |

| 省份—年份固定效应 | No | No | Yes |

| N | 14591 | 14591 | 14591 |

| Adj. R2 | 0.5035 | 0.5036 | 0.5081 |

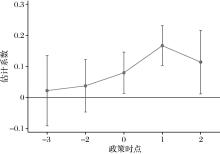

图1

平行趋势检验"

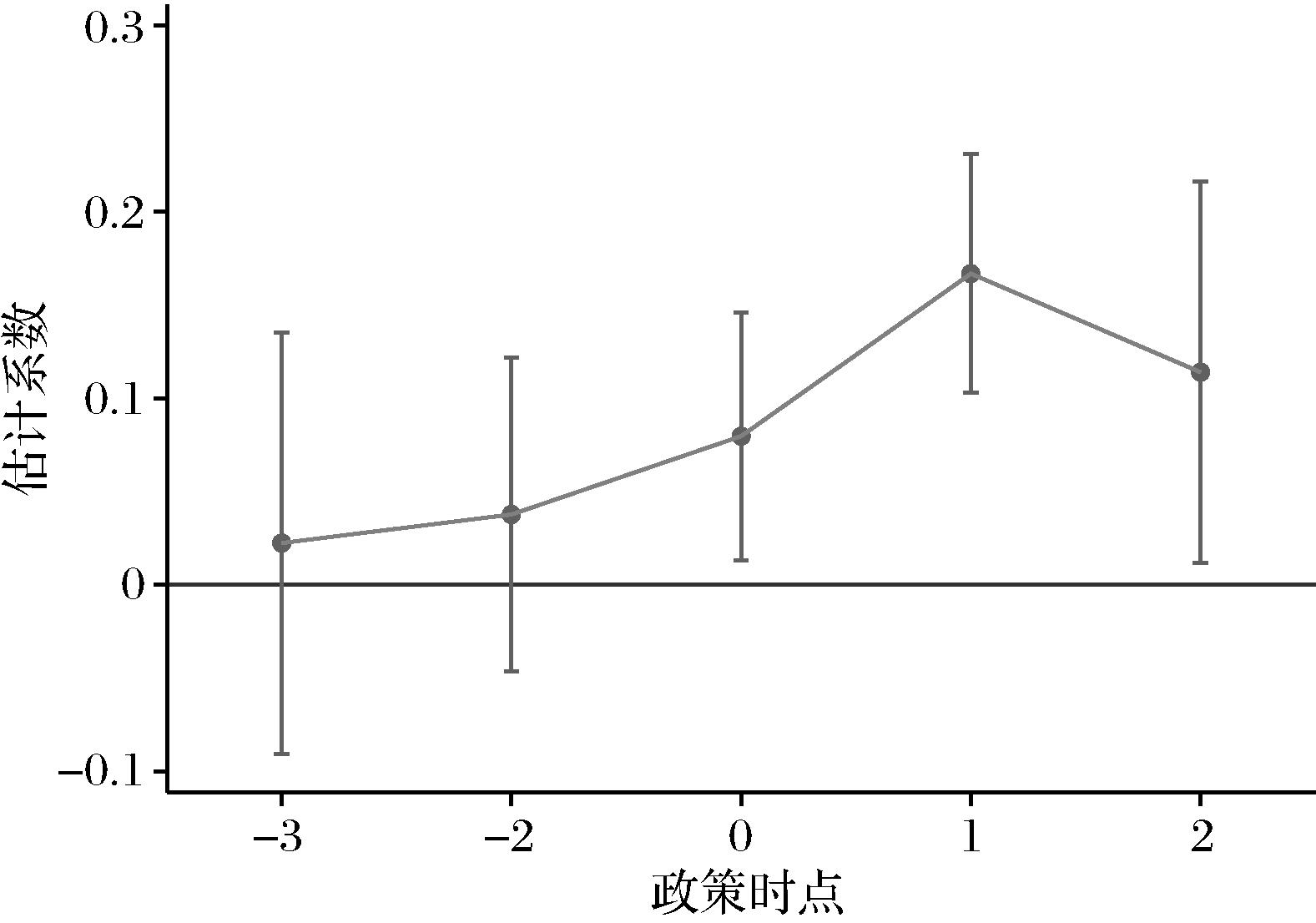

图2

安慰剂检验的估计系数分布"

表3

稳健性检验结果"

| 变量 | (1) | (2) | (3) | (4) | (5) | (6) | (7) |

|---|---|---|---|---|---|---|---|

| 按中位数确定处理组 | 按三分位数确定处理组 | 保留制造业企业样本 | 剔除广东和浙江企业 | 增加控制变量 | 排除增值税留抵退税政策 | PSM-DID | |

| Treat×Post | 0.0578* | 0.1009*** | 0.1610*** | 0.1282*** | 0.0978** | 0.1174*** | 0.1045** |

| (0.0304) | (0.0294) | (0.0452) | (0.0348) | (0.0421) | (0.0307) | (0.0414) | |

| Brir | 0.0060 | 0.0077 | 0.0158 | -0.0122 | 0.0090 | 0.0181 | 0.0120 |

| (0.0325) | (0.0322) | (0.0449) | (0.0400) | (0.0307) | (0.0306) | (0.0301) | |

| ROE | 0.0781 | 0.0773 | 0.0491 | 0.1320 | 0.0752 | 0.0869 | 0.0681 |

| (0.0861) | (0.0847) | (0.1126) | (0.1291) | (0.0815) | (0.0713) | (0.0815) | |

| Age | -0.1362 | -0.1424 | -0.2783 | -0.4209 | -0.1957 | -0.1114 | -0.1678 |

| (0.2784) | (0.2780) | (0.2765) | (0.3078) | (0.3064) | (0.2479) | (0.3033) | |

| Top10 | 0.1365 | 0.1345 | 0.2874 | 0.1194 | 0.1224 | 0.1092 | 0.1269 |

| (0.2061) | (0.2078) | (0.2243) | (0.2878) | (0.2182) | (0.1971) | (0.2189) | |

| Dual | -0.0294 | -0.0283 | -0.0564 | -0.0600 | -0.0315 | -0.0239 | -0.0251 |

| (0.0373) | (0.0369) | (0.0397) | (0.0423) | (0.0378) | (0.0389) | (0.0394) | |

| Cfo | -0.0209 | -0.0187 | -0.0131 | 0.0334 | -0.0192 | -0.0228 | -0.0123 |

| (0.1375) | (0.1367) | (0.2633) | (0.1980) | (0.1731) | (0.1276) | (0.1732) | |

| Lev | -0.1801* | -0.1862* | -0.1275 | -0.3132** | -0.1962 | -0.1837 | -0.2060* |

| (0.1019) | (0.1059) | (0.1389) | (0.1474) | (0.1184) | (0.1109) | (0.1202) | |

| GDPr | 0.0018*** | 0.0018*** | |||||

| (0.0002) | (0.0002) | ||||||

| Fin | -0.0436 | -0.0319 | |||||

| (0.1353) | (0.1372) | ||||||

| Rob | 0.0021 | 0.0021 | |||||

| (0.0014) | (0.0015) | ||||||

| Dig | 0.1165 | 0.1008 | |||||

| (0.2227) | (0.2171) | ||||||

| Pol | 0.0889*** | ||||||

| (0.0291) | |||||||

| 常数项 | 4.0300*** | 4.0499*** | 4.4299*** | 4.9375*** | 4.2359*** | 3.9260*** | 4.1329*** |

| (0.8773) | (0.8735) | (0.8509) | (0.9665) | (0.9371) | (0.7853) | (0.9218) | |

| 企业固定效应 | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| 年份固定效应 | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| 行业—年份固定效应 | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| 省份—年份固定效应 | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 14591 | 14591 | 9362 | 9865 | 14036 | 14591 | 13976 |

| Adj. R2 | 0.5079 | 0.5081 | 0.4738 | 0.5093 | 0.5114 | 0.5041 | 0.5134 |

表4

劳动力需求结构分解检验"

| 变量 | (1) | (2) |

|---|---|---|

| 高技能劳动力招聘数量的自然对数 | 低技能劳动力招聘数量的自然对数 | |

| Treat×Post | 0.1219*** | 0.0169 |

| (0.0408) | (0.0424) | |

| Brir | 0.0624** | 0.0499* |

| (0.0274) | (0.0252) | |

| ROE | 0.6426*** | 0.5383*** |

| (0.1084) | (0.0757) | |

| Age | 0.6271 | 0.5768 |

| (0.5364) | (0.4522) | |

| Top10 | 0.6157* | 0.5181* |

| (0.3233) | (0.3009) | |

| Dual | 0.0065 | 0.0245 |

| (0.0291) | (0.0291) | |

| Cfo | -0.1684 | -0.1290 |

| (0.1244) | (0.1366) | |

| Lev | 0.1708 | 0.3840*** |

| (0.1457) | (0.1122) | |

| 常数项 | 1.3726 | 2.4433 |

| (1.7126) | (1.4629) | |

| 企业固定效应 | Yes | Yes |

| 年份固定效应 | Yes | Yes |

| 行业—年份固定效应 | Yes | Yes |

| 省份—年份固定效应 | Yes | Yes |

| N | 14591 | 14591 |

| Adj. R2 | 0.7268 | 0.7180 |

表5

作用机制检验"

| 变量 | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| 资本投入 | 资本劳动比 | 现金持有 | 债务规模 | |

| Treat×Post | 0.1480*** | -8.4443 | -0.0117* | 0.1206*** |

| (0.0414) | (6.5588) | (0.0065) | (0.0222) | |

| Brir | 0.1263*** | -7.9033 | -0.0013 | 0.1371*** |

| (0.0309) | (5.4847) | (0.0027) | (0.0165) | |

| ROE | 0.9334*** | 5.6492 | 0.0085 | 0.7470*** |

| (0.0849) | (11.9432) | (0.0056) | (0.0399) | |

| Age | 1.1425*** | 9.8282 | 0.0202 | 0.9670*** |

| (0.3913) | (45.9419) | (0.0403) | (0.2450) | |

| Top10 | 1.1012*** | -30.2766* | 0.0919*** | 0.5620*** |

| (0.2097) | (16.3962) | (0.0185) | (0.1683) | |

| Dual | 0.0013 | -7.4838 | 0.0028 | 0.0177 |

| (0.0276) | (4.8397) | (0.0038) | (0.0120) | |

| Cfo | -0.2972 | 8.1359 | 0.2267*** | -0.1818* |

| (0.1875) | (23.9201) | (0.0207) | (0.0932) | |

| Lev | 1.3223*** | 26.4282* | -0.1571*** | 3.7447*** |

| (0.1955) | (14.8574) | (0.0128) | (0.1099) | |

| 常数项 | 13.9897*** | 44.4307 | 0.1384 | 16.5010*** |

| (1.2337) | (138.3892) | (0.1164) | (0.8067) | |

| 企业固定效应 | Yes | Yes | Yes | Yes |

| 年份固定效应 | Yes | Yes | Yes | Yes |

| 行业—年份固定效应 | Yes | Yes | Yes | Yes |

| 省份—年份固定效应 | Yes | Yes | Yes | Yes |

| N | 14591 | 14591 | 14591 | 14591 |

| Adj. R2 | 0.8146 | 0.9618 | 0.6700 | 0.9740 |

表6

基于企业内部特征的异质性分析结果"

| 变量 | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| 国有企业 | 非国有 企业 | 低融资约束企业 | 高融资约束企业 | |

| Treat×Post | 0.0576 | 0.1310*** | 0.1022 | 0.1197*** |

| (0.0596) | (0.0453) | (0.0760) | (0.0403) | |

| Brir | 0.0261 | 0.0186 | 0.0053 | 0.0203 |

| (0.0861) | (0.0322) | (0.0389) | (0.0467) | |

| ROE | 0.1278 | 0.0503 | 0.0128 | 0.1474 |

| (0.2594) | (0.0811) | (0.0931) | (0.1301) | |

| Age | 0.9260 | -0.4072 | 0.6125 | -0.4663 |

| (0.7700) | (0.3103) | (0.3770) | (0.5362) | |

| Top10 | -0.3425 | 0.2309 | 0.1566 | 0.3347 |

| (0.4932) | (0.2568) | (0.2281) | (0.2786) | |

| Dual | -0.0285 | -0.0400 | -0.0533 | 0.0193 |

| (0.0885) | (0.0378) | (0.0362) | (0.0793) | |

| Cfo | -0.1589 | -0.0163 | 0.0889 | -0.0621 |

| (0.3875) | (0.1818) | (0.2083) | (0.2591) | |

| Lev | -0.7368* | -0.0963 | -0.2156 | -0.1967 |

| (0.4112) | (0.1067) | (0.1799) | (0.1161) | |

| 常数项 | 1.2171 | 4.7796*** | 1.7288 | 4.9161*** |

| (2.3860) | (0.9530) | (1.1583) | (1.6036) | |

| 企业固定效应 | Yes | Yes | Yes | Yes |

| 年份固定效应 | Yes | Yes | Yes | Yes |

| 行业—年份固定效应 | Yes | Yes | Yes | Yes |

| 省份—年份固定效应 | Yes | Yes | Yes | Yes |

| N | 4066 | 10525 | 7288 | 7303 |

| Adj. R2 | 0.4549 | 0.5255 | 0.5099 | 0.5084 |

表7

基于企业外部环境的异质性分析结果"

| 变量 | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

低就业 目标 | 高就业 目标 | 低人才落户门槛 | 高人才落户门槛 | |

| Treat×Post | 0.1473** | 0.0179 | 0.1226** | 0.0905** |

| (0.0682) | (0.0567) | (0.0537) | (0.0409) | |

| Brir | 0.0983** | -0.0419 | 0.0495 | -0.0422 |

| (0.0451) | (0.0507) | (0.0402) | (0.0306) | |

| ROE | -0.1336 | 0.2984* | 0.1129 | 0.1445 |

| (0.1967) | (0.1446) | (0.1033) | (0.0901) | |

| Age | -0.5436 | 0.0215 | -0.6089 | 0.3524 |

| (0.6391) | (0.7104) | (0.8832) | (0.3230) | |

| Top10 | -0.1139 | 0.1250 | 0.3455 | 0.0094 |

| (0.2956) | (0.4596) | (0.3072) | (0.4192) | |

| Dual | -0.0575 | -0.0465 | -0.0658 | 0.0116 |

| (0.0520) | (0.0457) | (0.0435) | (0.0580) | |

| Cfo | -0.0925 | 0.1299 | -0.3939* | 0.2433* |

| (0.3296) | (0.1991) | (0.2137) | (0.1276) | |

| Lev | -0.3270 | -0.3679** | -0.0078 | -0.2794 |

| (0.2309) | (0.1324) | (0.1840) | (0.2017) | |

| 常数项 | 5.3591*** | 3.6827 | 5.2479* | 2.7513** |

| (1.8965) | (2.2317) | (2.6044) | (1.0416) | |

| 企业固定效应 | Yes | Yes | Yes | Yes |

| 年份固定效应 | Yes | Yes | Yes | Yes |

| 行业—年份固定效应 | Yes | Yes | Yes | Yes |

| 省份—年份固定效应 | Yes | Yes | Yes | Yes |

| N | 5963 | 5625 | 6350 | 6241 |

| Adj. R2 | 0.4213 | 0.5807 | 0.4889 | 0.5748 |

表8

进一步讨论结果"

| 变量 | (1) | (2) |

|---|---|---|

| 招聘岗位学历要求 | 实际雇佣结构 | |

| Treat×Post | 0.0690*** | 0.0128* |

| (0.0173) | (0.0069) | |

| Brir | -0.0283 | -0.0240** |

| (0.0221) | (0.0099) | |

| ROE | -0.0039 | -0.0144 |

| (0.0665) | (0.0130) | |

| Age | 0.2768 | -0.0350 |

| (0.2354) | (0.2112) | |

| Top10 | 0.0362 | -0.0292 |

| (0.1156) | (0.0784) | |

| Dual | -0.0060 | 0.0140* |

| (0.0226) | (0.0072) | |

| Cfo | 0.0205 | 0.0284 |

| (0.1230) | (0.0517) | |

| Lev | 0.0755 | -0.0074 |

| (0.0755) | (0.0274) | |

| 常数项 | 2.7911*** | 1.0669 |

| (0.7261) | (0.6500) | |

| 企业固定效应 | Yes | Yes |

| 年份固定效应 | Yes | Yes |

| 行业—年份固定效应 | Yes | Yes |

| 省份—年份固定效应 | Yes | Yes |

| N | 14591 | 14591 |

| Adj. R2 | 0.5173 | 0.8198 |

| [1] | 刘贯春, 叶永卫, 张军. 社会保险缴费、企业流动性约束与稳就业——基于《社会保险法》实施的准自然实验[J]. 中国工业经济, 2021(5): 152-169. |

| Liu G C, Ye Y W, Zhang J. Social security contributions, liquidity constraint and employment stabilization: A quasi-natural experiment from the enactment of social insurance law[J]. China Industrial Economics, 2021(5): 152-169. | |

| [2] | 林灵, 曾海舰. 社会保险成本过高是否抑制企业投资?[J]. 管理科学学报, 2020, 23(7): 57-75. |

| Lin L, Zeng H J. Does high social insurance cost discourage firm investment?[J]. Journal of Management Sciences in China, 2020, 23(7): 57-75. | |

| [3] | 崔小勇, 卢国军, 翟颖佳. 促就业与稳增长: 养老保险缴费率的视角[J]. 经济研究, 2024, 59(1): 148-167. |

| Cui X Y, Lu G J, Zhai Y J. Promoting employment and stabilizing growth: A perspective of pension insurance contribution rates in China[J]. Economic Research Journal, 2024, 59(1): 148-167. | |

| [4] | 赵健宇, 陆正飞. 养老保险缴费比例会影响企业生产效率吗?[J]. 经济研究, 2018, 53(10): 97-112. |

| Zhao J Y, Lu Z F. Does pension contribution rate affect firm productivity?[J]. Economic Research Journal, 2018, 53(10): 97-112. | |

| [5] | 赵绍阳, 杨豪. 我国企业社会保险逃费现象的实证检验[J]. 统计研究, 2016, 33(1): 78-86. |

| Zhao S Y, Yang H. An empirical research on social insurance evasion of enterprises in China[J]. Statistical Research, 2016, 33(1): 78-86. | |

| [6] | 李逸飞, 李金, 肖人瑞. 社会保险缴费征管与企业人力资本结构升级[J]. 经济研究, 2023, 58(1): 158-174. |

| Li Y F, Li J, Xiao R R. Collection and management of social security contributions and upgrading of firms' human capital structure[J]. Economic Research Journal, 2023, 58(1): 158-174. | |

| [7] | 刘毓芸, 程宇玮. 重点产业政策与人才需求——来自企业招聘面试的微观证据[J]. 管理世界, 2020, 36(6): 65-79+245. |

| Liu Y Y, Cheng Y W. Key industrial policy and talent demand: Microscopic evidence from enterprise recruitment interview[J]. Journal of Management World, 2020, 36(6): 65-79+245. | |

| [8] | Jung B, Lee W J, Weber D P. Financial reporting quality and labor investment efficiency[J]. Contemporary Accounting Research, 2014, 31(4): 1047-1076. |

| [9] | 孙鲲鹏, 罗婷, 肖星. 人才政策、研发人员招聘与企业创新[J]. 经济研究, 2021, 56(8): 143-159. |

| Sun K P, Luo T, Xiao X. Talent policy, R & D recruitment and corporate innovation[J]. Economic Research Journal, 2021, 56(8): 143-159. | |

| [10] | 陈琳, 高悦蓬, 余林徽. 人工智能如何改变企业对劳动力的需求?——来自招聘平台大数据的分析[J]. 管理世界, 2024, 40(6): 74-93. |

| Chen L, Gao Y P, Yu L H. How is AI shaping the labor demands of Enterprises? Evidence from big data analysis of recruitment platforms[J]. Journal of Management World, 2024, 40(6): 74-93. | |

| [11] | Nielsen I, Smyth R. Who bears the burden of employer compliance with social security contributions? Evidence from Chinese firm level data[J]. China Economic Review, 2008, 19(2): 230-244. |

| [12] | 封进. 社会保险对工资的影响——基于人力资本差异的视角[J]. 金融研究, 2014(7): 109-123. |

| Feng J. The effect of social insurance on wages: Difference by human capital[J].Journal of Financial Research, 2014(7): 109-123. | |

| [13] | Angelopoulos K, Asimakopoulos S, Malley J. Tax smoothing in a business cycle model with capital-skill complementarity[J]. Journal of Economic Dynamics and Control, 2015, 51: 420-444. |

| [14] | 刘啟仁, 赵灿. 税收政策激励与企业人力资本升级[J]. 经济研究, 2020, 55(4): 70-85. |

| Liu Q R, Zhao C. Tax incentives and upgrading firms' human capital[J]. Economic Research Journal, 2020, 55(4): 70-85. | |

| [15] | Benmelech E, Frydman C, Papanikolaou D. Financial frictions and employment during the great depression[J]. Journal of Financial Economics, 2019, 133(3): 541-563. |

| [16] | 宋弘, 封进, 杨婉彧. 社保缴费率下降对企业社保缴费与劳动力雇佣的影响[J]. 经济研究, 2021, 56(1): 90-104. |

| Song H, Feng J, Yang W Y. The effect of a reduction of the social security contribution rate on enterprise social security participation and labor employment[J]. Economic Research Journal, 2021, 56(1): 90-104. | |

| [17] | 袁璐璐, 罗楚亮. 养老保险费率对小微企业用工形式的影响[J]. 中国人口科学, 2023(1): 70-85. |

| Yuan L L, Luo C L. The effect of pension contribution rate on the employment pattern of small and micro enterprises[J]. Chinese Journal of Population Science, 2023(1): 70-85. | |

| [18] | 孙楚仁, 马艳君, 陈瑾. 最低工资对企业内部雇佣技能结构的影响[J]. 经济科学, 2020(4): 97-110. |

| Sun C R, Ma Y J, Chen J. The effect of minimum wage on the structure of internal employment skills in enterprises[J]. Economic Science, 2020(4): 97-110. | |

| [19] | 马慧, 陈胜蓝, 刘晓玲. 担保物权制度改革与企业劳动力结构[J]. 金融研究, 2022(10): 153-169. |

| Ma H, Chen S L, Liu X L. Reform of the security system and enterprise labor structure[J]. Journal of Financial Research, 2022(10): 153-169. | |

| [20] | Phan H V, Hegde S P. Pension contributions and firm performance: Evidence from frozen defined benefit plans[J]. Financial Management, 2013, 42(2): 373-411. |

| [21] | 唐珏, 封进. 社会保险缴费对企业资本劳动比的影响——以21世纪初省级养老保险征收机构变更为例[J]. 经济研究, 2019, 54(11): 87-101. |

| Tang J, Feng J. Do social security contributions affect the capital-labor ratio: Evidence from China[J]. Economic Research Journal, 2019, 54(11): 87-101. | |

| [22] | 汪佩洁, 蒙克, 黄海, 等. 社会保险缴费率与企业全要素生产率和创新[J].经济研究,2022, 57(10): 69-85. |

| Wang P J, Meng K, Huang H, et al. The effect of social insurance contribution rate on firms' TFP and innovation[J]. Economic Research Journal, 2022, 57(10): 69-85. | |

| [23] | Kugler A, Kugler M. Labor market effects of payroll taxes in developing countries: Evidence from Colombia[J]. Economic Development and Cultural Change, 2009, 57(2): 335-358. |

| [24] | Iturbe-Ormaetxe I. Salience of social security contributions and employment[J]. International Tax and Public Finance, 2015, 22(5): 741-759.. |

| [25] | 钱雪亚, 蒋卓余, 胡琼.社会保险缴费对企业雇佣工资和规模的影响研究[J].统计研究,2018,35(12): 68-79. |

| Qian X Y, Jiang Z Y, Hu Q. A study on the impacts of social insurance contributions on employment decisions by firms[J]. Statistical Research, 2018, 35(12): 68-79. | |

| [26] | 马双, 孟宪芮, 甘犁. 养老保险企业缴费对员工工资、就业的影响分析[J]. 经济学(季刊), 2014, 14(3): 969-1000. |

| Ma S, Meng X R, Gan L. Effect of pension on employment and firm average wage[J]. China Economic Quarterly, 2014, 14(3): 969-1000. | |

| [27] | 尹恒, 张子尧, 曹斯蔚. 社会保险降费的就业促进效应——基于服务业的政策模拟[J]. 中国工业经济, 2021(5): 57-75. |

| Yin H, Zhang Z Y, Cao S W. The effect of social security fee reduction on the labor demand—Policy simulation based on service sector[J]. China Industrial Economics, 2021(5): 57-75. | |

| [28] | Acemoglu D, Restrepo P. Robots and jobs: Evidence from US labor markets[J].Journal of Political Economy, 2020, 128(6): 2188-2244. |

| [29] | 王永钦, 董雯. 机器人的兴起如何影响中国劳动力市场?——来自制造业上市公司的证据[J]. 经济研究, 2020, 55(10): 159-175. |

| Wang Y Q, Dong W. How the rise of robots has affected China’s labor market: Evidence from China’s listed manufacturing firms[J]. Economic Research Journal, 2020, 55(10): 159-175. | |

| [30] | 叶永卫, 李鑫, 刘贯春. 数字化转型与企业人力资本升级[J]. 金融研究, 2022(12): 74-92. |

| Ye Y W, Li X, Liu G C. Digital transformation and corporate human capital upgrade[J]. Journal of Financial Research, 2022(12): 74-92. | |

| [31] | 肖土盛, 孙瑞琦, 袁淳, 等. 企业数字化转型、人力资本结构调整与劳动收入份额[J]. 管理世界, 2022, 38(12): 220-237. |

| Xiao T S, Sun R Q, Yuan C, et al. Digital transformation, human capital structure adjustment and labor income share[J].Journal of Management World, 2022, 38(12): 220-237. | |

| [32] | 宋晓梧. 企业社会保险缴费成本与政策调整取向[J]. 社会保障评论, 2017, 1(1): 63-82. |

| Song X W. Social insurance contribution as enterprises' cost and policy adjustments[J]. Chinese Social Security Review, 2017, 1(1): 63-82. | |

| [33] | 景鹏. 社会保险缴费与企业杠杆率——“降成本”有利于“去杠杆”吗?[J]. 社会保障评论,2024,8(1): 74-87. |

| Jing P. Social insurance contributions and firm leverage: Can cost reduction help de-leverage?[J]. Chinese Social Security Review, 2024, 8(1): 74-87. | |

| [34] | 郭凯明, 余靖雯, 龚六堂. 人口政策、劳动力结构与经济增长[J]. 世界经济, 2013, 36(11): 72-92. |

| Guo K M, Yu J W, Gong L T. Population policy, labor structure and economic growth[J]. The Journal of World Economy, 2013, 36(11): 72-92. | |

| [35] | 王明益, 张中意. 进口贸易自由化与企业就业技能结构升级[J]. 经济学动态, 2022(4): 103-122. |

| Wang M Y, Zhang Z Y. Liberalization of import trade and upgrading of employment skill structure of enterprises[J].Economic Perspectives, 2022(4): 103-122. | |

| [36] | 张同斌, 刘文龙, 付婷婷. 《社会保险法》实施与企业劳动收入份额变动[J]. 数量经济技术经济研究, 2023, 40(6): 91-112. |

| Zhang T B, Liu W L, Fu T T. Enforcement of social insurance law and change in corporate labor income share[J]. Journal of Quantitative & Technological Economics, 2023, 40(6): 91-112. | |

| [37] | Li P, Lu Y, Wang J. Does flattening government improve economic performance? Evidence from China[J]. Journal of Development Economics, 2016, 123: 18-37. |

| [38] | 安辉, 何萱, 邹千邈. 中国房地产限售政策对房价的影响研究——兼论限售和限购的政策组合效应[J]. 中国管理科学, 2021, 29(8): 35-43. |

| An H, He X, Zou Q M. The impact of China’s house-sale restrictions and its joint effect with housing-purchase restriction on housing price[J]. Chinese Journal of Management Science, 2021, 29(8): 35-43. | |

| [39] | 钱雪松, 方胜. 《物权法》出台、融资约束与民营企业投资效率——基于双重差分法的经验分析[J]. 经济学(季刊), 2021, 21(2): 713-732. |

| Qian X S, Fang S. Enactment of the property law, financial constraints and investment efficiency of private-owned enterprises—Empirical analysis based on difference-in-differences method[J]. China Economic Quarterly, 2021, 21(2): 713-732. | |

| [40] | 江艇. 因果推断经验研究中的中介效应与调节效应[J]. 中国工业经济, 2022(5): 100-120. |

| Jiang T. Mediating effects and moderating effects in causal inference[J]. China Industrial Economics, 2022(5): 100-120. | |

| [41] | 刘贯春, 吴佳其, 叶永卫, 等. 增值税留抵退税的就业创造效应[J]. 财经研究, 2023, 49(11): 19-33+94. |

| Liu G C, Wu J Q, Ye Y W, et al. The employment creation effect of value-added tax refunds[J]. Journal of Finance and Economics, 2023, 49(11): 19-33+94. | |

| [42] | 谢雁翔, 覃家琦, 金振, 等. 增值税税收中性与企业现金持有[J]. 财贸经济, 2022, 43(12): 80-96. |

| Xie Y X, Qin J Q, Jin Z, et al. VAT neutrality and corporate cash holdings[J]. Finance & Trade Economics, 2022, 43(12): 80-96. | |

| [43] | 曹春方, 邓松林. 政府失业目标调整与就业质量——来自微观企业层面的证据[J]. 金融研究, 2022(6): 115-132. |

| Cao C F, Deng S L. Government unemployment target adjustment and employment quality: Evidence from micro-firms[J]. Journal of Financial Research, 2022(6): 115-132. | |

| [44] | 钟粤俊, 陆铭, 奚锡灿. 集聚与服务业发展——基于人口空间分布的视角[J]. 管理世界, 2020, 36(11): 35-49. |

| Zhong Y J, Lu M, Xi X C. Agglomeration and service industry development: Based on the perspective of population spatial distribution[J].Journal of Management World, 2020, 36(11): 35-49. | |

| [45] | 张吉鹏, 卢冲. 户籍制度改革与城市落户门槛的量化分析[J]. 经济学(季刊), 2019, 19(4): 1509-1530. |

| Zhang J P, Lu C. A quantitative analysis on the reform of household registration in Chinese Cities[J]. China Economic Quarterly, 2019, 19(4): 1509-1530. | |

| [46] | 王兆萍. 数智时代我国面临的主要就业风险及治理路径[J]. 北京社会科学, 2023(3): 88-98. |

| Wang Z P. Main employment risks which China is facing and its governance path in the era of digitalization and intelligence[J]. Social Sciences of Beijing, 2023(3): 88-98. |

| [1] | 屈伸,钱雪松,康瑾. 商业信用和产业政策传导:理论建模分析和来自十大产业振兴规划的证据[J]. 中国管理科学, 2024, 32(5): 38-46. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||