主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2024, Vol. 32 ›› Issue (8): 50-60.doi: 10.16381/j.cnki.issn1003-207x.2022.1429cstr: 32146.14.j.cnki.issn1003-207x.2022.1429

倪宣明1,郑田田1,赵慧敏2( ),武康平3

),武康平3

收稿日期:2022-06-30

修回日期:2022-12-18

出版日期:2024-08-25

发布日期:2024-08-29

通讯作者:

赵慧敏

E-mail:zhaohuim@mail.sysu.edu.cn

基金资助:

Xuanming Ni1,Tiantian Zheng1,Huimin Zhao2(),Kangping Wu3

Received:2022-06-30

Revised:2022-12-18

Online:2024-08-25

Published:2024-08-29

Contact:

Huimin Zhao

E-mail:zhaohuim@mail.sysu.edu.cn

摘要:

本文从经典因子模型的异质收益率出发,通过在残差空间中进行投资组合优化构造异质收益率因子来识别基准因子模型中的遗漏信息,从而对基准模型下的基于异质收益率的资产进行定价,提升基准模型的定价能力,并进一步证明了该拓展因子对异质收益率的资产定价能力。之后,本文基于A股1995年1月—2022年11月的6个因子数据集和美股1963年7月至2022年10月的4个因子数据集,在三因子、四因子、五因子模型的基础上加入异质收益率因子,并将拓展后的模型分别与原模型、均值方差有效单因子模型、主成分分析因子模型的定价效果进行对比。结果显示,在加入异质收益率因子之后,测试资产的

中图分类号:

倪宣明,郑田田,赵慧敏, 等. 基于最优异质收益率因子的资产定价研究[J]. 中国管理科学, 2024, 32(8): 50-60.

Xuanming Ni,Tiantian Zheng,Huimin Zhao, et al. Asset Pricing Based on the Optimal Idiosyncratic Return Factor[J]. Chinese Journal of Management Science, 2024, 32(8): 50-60.

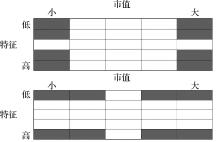

图1

规模、价值、动量、投资、盈利因子的基础资产"

表1

数据说明"

| 数据集名 | 资产数 | 时间跨度 | 来源 |

|---|---|---|---|

| ME5-BEME5-CN | 25 | 1995/01-2022/11 | CSMAR(基于个股信息构造) |

| ME5-INV5-CN | 25 | 1995/01-2022/11 | CSMAR(基于个股信息构造) |

| ME5-OP5-CN | 25 | 1995/01-2022/11 | CSMAR(基于个股信息构造) |

| ME5-MOM5-CN | 25 | 1995/01-2022/11 | CSMAR(基于个股信息构造) |

| ME5-PE5-CN | 25 | 1995/01-2022/11 | CSMAR(基于个股信息构造) |

| ME5-ROE5-CN | 25 | 1995/01-2022/11 | CSMAR(基于个股信息构造) |

| ME5-BEME5-US | 25 | 1963/07-2022/10 | Kenneth R. French Data Library |

| ME5-INV5-US | 25 | 1963/07-2022/10 | Kenneth R. French Data Library |

| ME5-OP5-US | 25 | 1963/07-2022/10 | Kenneth R. French Data Library |

| ME5-MOM5-US | 25 | 1963/07-2022/10 | Kenneth R. French Data Library |

表2

各因子模型在A股6个因子数据集上的样本内GRS统计量"

| 模型 | BEME (1) | INV (2) | OP (3) | MOM (4) | PE (5) | ROE (6) |

|---|---|---|---|---|---|---|

| Base:FF3 | ||||||

| FF3 | 13.1445 | 19.9210 | 16.5175 | 15.0180 | 14.3725 | 17.1991 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| FF3-MV | 1.0940 | 2.4821 | 1.8546 | 1.9885 | 1.8909 | 1.7332 |

| (0.3476) | (0.0002) | (0.0089) | (0.0040) | (0.0072) | (0.0179) | |

| MVE | 1.1936 | 1.6755 | 1.6119 | 2.7056 | 1.0238 | 1.5562 |

| (0.2770) | (0.0482) | (0.0619) | (0.0006) | (0.4512) | (0.0769) | |

| MVE-MV | 1.2363 | 1.6886 | 1.5791 | 2.6570 | 1.1149 | 1.5245 |

| (0.2424) | (0.0461) | (0.0709) | (0.0008) | (0.3517) | (0.0874) | |

| PCA | 70.8700 | 3.3591 | 4.8543 | 7.0512 | 2.8394 | 5.3881 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| PCA-MV | 36.7027 | 1.9102 | 2.7191 | 3.0232 | 1.9557 | 2.5225 |

| (0.0000) | (0.0192) | (0.0006) | (0.0002) | (0.0159) | (0.0015) | |

| Base:C4 | ||||||

| C4 | 13.1858 | 19.9417 | 17.7860 | 15.6457 | 14.4048 | 17.7537 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| C4-MV | 1.5014 | 2.5055 | 1.9206 | 1.6961 | 1.8865 | 1.7416 |

| (0.0615) | (0.0001) | (0.0060) | (0.0220) | (0.0074) | (0.0171) | |

| MVE | 0.9425 | 1.8707 | 1.7414 | 1.7378 | 0.9287 | 1.8171 |

| (0.5500) | (0.0217) | (0.0369) | (0.0375) | (0.5674) | (0.0271) | |

| MVE-MV | 1.0259 | 2.0083 | 1.7728 | 1.6430 | 0.9712 | 1.8196 |

| (0.4490) | (0.0124) | (0.0329) | (0.0553) | (0.5145) | (0.0271) | |

| PCA | 2.5416 | 2.4555 | 3.2339 | 6.2533 | 1.2769 | 3.3114 |

| (0.0001) | (0.0002) | (0.0000) | (0.0000) | (0.1733) | (0.0000) | |

| PCA-MV | 1.5867 | 1.9160 | 2.2437 | 2.3251 | 1.1922 | 1.9420 |

| (0.0700) | (0.0188) | (0.0048) | (0.0034) | (0.2799) | (0.0169) | |

| Base:FF5 | ||||||

| FF5 | 12.2916 | 18.2013 | 14.5138 | 13.8382 | 12.8829 | 15.3652 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| FF5-MV | 1.2171 | 1.8741 | 1.4984 | 2.0453 | 1.7119 | 1.4176 |

| (0.2213) | (0.0080) | (0.0624) | (0.0028) | (0.0202) | (0.0925) | |

| MVE | 1.3119 | 1.1819 | 1.0459 | 2.4659 | 0.9739 | 1.0127 |

| (0.1879) | (0.2873) | (0.4257) | (0.0017) | (0.5111) | (0.4642) | |

| MVE-MV | 1.2985 | 1.1894 | 1.0537 | 2.4592 | 1.0417 | 1.0062 |

| (0.1973) | (0.2812) | (0.4172) | (0.0018) | (0.4308) | (0.4721) | |

| PCA | 5.0999 | 4.8512 | 6.0405 | 9.0142 | 4.6782 | 5.8977 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| PCA-MV | 3.4042 | 1.5849 | 2.3086 | 2.8972 | 1.9755 | 2.4746 |

| (0.0000) | (0.0705) | (0.0036) | (0.0003) | (0.0147) | (0.0018) | |

表3

各因子模型在A股6个因子数据集上的样本外GRS统计量"

| 模型 | BEME | INV | OP | MOM | PE | ROE |

|---|---|---|---|---|---|---|

| Base:FF3 | ||||||

| FF3 | 13.1445 | 19.9210 | 16.5175 | 15.0180 | 14.3725 | 17.1991 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| FF3-MV | 3.4874 | 2.9205 | 2.6322 | 3.5418 | 2.7474 | 2.5147 |

| (0.0000) | (0.0002) | (0.0009) | (0.0000) | (0.0006) | (0.0015) | |

| MVE | 1.1936 | 1.6755 | 1.6119 | 2.7056 | 1.0238 | 1.5562 |

| (0.2770) | (0.0482) | (0.0619) | (0.0006) | (0.4512) | (0.0769) | |

| MVE-MV | 0.6125 | 1.8356 | 2.0824 | 5.9804 | 1.5512 | 2.3772 |

| (0.9290) | (0.0099) | (0.0022) | (0.0000) | (0.0477) | (0.0003) | |

| PCA | 70.8700 | 3.3591 | 4.8543 | 7.0512 | 2.8394 | 5.3881 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| PCA-MV | 65.1869 | 3.0563 | 4.4415 | 6.7906 | 2.4868 | 4.9631 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0002) | (0.0000) | |

| Base:C4 | ||||||

| C4 | 13.1858 | 19.9417 | 17.7860 | 15.6457 | 14.4048 | 17.7537 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| C4-MV | 1.5985 | 4.0996 | 2.1118 | 1.9392 | 2.1105 | 1.9459 |

| (0.0675) | (0.0000) | (0.0085) | (0.0174) | (0.0085) | (0.0169) | |

| MVE | 0.9425 | 1.8707 | 1.7414 | 1.7378 | 0.9287 | 1.8171 |

| (0.5500) | (0.0217) | (0.0369) | (0.0375) | (0.5674) | (0.0271) | |

| MVE-MV | 0.6349 | 2.1381 | 2.7254 | 2.1344 | 0.9488 | 2.701 |

| (0.9134) | (0.0016) | (0.0000) | (0.0016) | (0.5372) | (0.0000) | |

| PCA | 2.5416 | 2.4555 | 3.2339 | 6.2533 | 1.2769 | 3.3114 |

| (0.0001) | (0.0002) | (0.0000) | (0.0000) | (0.1733) | (0.0000) | |

| PCA-MV | 4.1944 | 2.4587 | 3.6146 | 3.1235 | 1.1356 | 3.8824 |

| (0.0000) | (0.0002) | (0.0000) | (0.0000) | (0.3007) | (0.0000) | |

| Base:FF5 | ||||||

| FF5 | 12.2916 | 18.2013 | 14.5138 | 13.8382 | 12.8829 | 15.3652 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| FF5-MV | 3.5243 | 2.3147 | 1.8735 | 3.2986 | 2.5161 | 1.7374 |

| (0.0000) | (0.0037) | (0.0227) | (0.0001) | (0.0016) | (0.0397) | |

| MVE | 1.3119 | 1.1819 | 1.0459 | 2.4659 | 0.9739 | 1.0127 |

| (0.1879) | (0.2873) | (0.4257) | (0.0017) | (0.5111) | (0.4642) | |

| MVE-MV | 0.4119 | 0.8239 | 0.6615 | 5.459 | 1.415 | 0.8911 |

| (0.9951) | (0.7107) | (0.8923) | (0.0000) | (0.0935) | (0.6182) | |

| PCA | 5.0999 | 4.8512 | 6.0405 | 9.0142 | 4.6782 | 5.8977 |

| (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

| PCA-MV | 3.1081 | 2.1424 | 4.6007 | 7.0399 | 2.8333 | 3.8119 |

| (0.0000) | (0.0015) | (0.0000) | (0.0000) | (0.0000) | (0.0000) | |

表4

各因子模型在A股6个因子数据集上的MAA"

| 模型 | BEME | INV | OP | MOM | PE | ROE |

|---|---|---|---|---|---|---|

| Base:FF3 | ||||||

| FF3 | 0.0185 | 0.0197 | 0.0187 | 0.0189 | 0.0184 | 0.0188 |

| FF3-MV | 0.0178 | 0.0190 | 0.0179 | 0.0183 | 0.0177 | 0.0180 |

| 0.0154 | 0.0137 | 0.0154 | 0.0165 | 0.0153 | 0.0153 | |

| MVE | 0.0088 | 0.0086 | 0.0089 | 0.0096 | 0.0085 | 0.0088 |

| MVE-MV | 0.0038 | 0.0058 | 0.0047 | 0.0048 | 0.0041 | 0.0050 |

| 0.0088 | 0.0088 | 0.0089 | 0.0096 | 0.0084 | 0.0087 | |

| PCA | 0.0031 | 0.0052 | 0.0042 | 0.0046 | 0.0038 | 0.0045 |

| PCA-MV | 0.0026 | 0.0049 | 0.0040 | 0.0045 | 0.0032 | 0.0043 |

| 0.0027 | 0.0050 | 0.0045 | 0.0047 | 0.0029 | 0.0045 | |

| Base:C4 | ||||||

| C4 | 0.0184 | 0.0196 | 0.0186 | 0.0187 | 0.0183 | 0.0186 |

| C4-MV | 0.0150 | 0.0157 | 0.0152 | 0.0142 | 0.0147 | 0.0153 |

| 0.0157 | 0.0128 | 0.0155 | 0.0157 | 0.0149 | 0.0155 | |

| MVE | 0.0061 | 0.0060 | 0.0066 | 0.0061 | 0.0063 | 0.0067 |

| MVE-MV | 0.0009 | 0.0036 | 0.0039 | 0.0020 | 0.0019 | 0.0044 |

| 0.0062 | 0.0063 | 0.0068 | 0.0062 | 0.0066 | 0.0069 | |

| PCA | 0.0016 | 0.0039 | 0.0036 | 0.0035 | 0.0017 | 0.0040 |

| PCA-MV | 0.0012 | 0.0039 | 0.0042 | 0.0021 | 0.0019 | 0.0047 |

| 0.0016 | 0.0042 | 0.0040 | 0.0036 | 0.0022 | 0.0043 | |

| Base:FF5 | ||||||

| FF5 | 0.0182 | 0.0198 | 0.0184 | 0.0184 | 0.0179 | 0.0185 |

| FF5-MV | 0.0165 | 0.0177 | 0.0167 | 0.0162 | 0.0162 | 0.0167 |

| 0.0155 | 0.0137 | 0.0155 | 0.0160 | 0.0148 | 0.0155 | |

| MVE | 0.0062 | 0.0056 | 0.0063 | 0.0066 | 0.0058 | 0.0062 |

| MVE-MV | 0.0014 | 0.0037 | 0.0015 | 0.0050 | 0.0028 | 0.0016 |

| 0.0067 | 0.0057 | 0.0067 | 0.0070 | 0.0063 | 0.0066 | |

| PCA | 0.0031 | 0.0051 | 0.0033 | 0.0049 | 0.0039 | 0.0035 |

| PCA-MV | 0.0019 | 0.0042 | 0.0021 | 0.0048 | 0.0031 | 0.0021 |

| 0.0025 | 0.0029 | 0.0021 | 0.0048 | 0.0027 | 0.0021 | |

表5

异质收益率因子在各经典因子模型下的α情况"

| 模型 | 样本内 | 样本外 | ||||

|---|---|---|---|---|---|---|

| FF3 | C4 | FF5 | FF3 | C4 | FF5 | |

| FF3-MV | 0.0222*** | 0.0220*** | 0.0276*** | 0.0307*** | 0.0304*** | 0.0363*** |

| (3.8420) | (3.8090) | (4.7230) | (2.8020) | (2.8540) | (3.5140) | |

| C4-MV | 0.2122*** | 0.2225*** | 0.2209*** | 0.2342*** | 0.2383*** | 0.2260*** |

| (9.1940) | (12.2490) | (9.2880) | (3.8720) | (5.0100) | (3.8930) | |

| FF5-MV | 0.1560*** | 0.1547*** | 0.1462*** | 0.1897*** | 0.1887*** | 0.2002*** |

| (10.8350) | (10.8090) | (9.9790) | (5.3020) | (5.4220) | (5.8600) | |

| 1 | Sharpe W F. Capital asset prices: A theory of market equilibrium under conditions of risk[J]. The Journal of Finance, 1964, 19(3): 425-442. |

| 2 | Lintner J. The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets[J]. The Review of Economics and Statistics, 1965,47(1): 13-37. |

| 3 | Roll R. A critique of the asset pricing theory's tests part I: On past and potential testability of the theory[J]. Journal of Financial Economics, 1977, 4(2): 129-176. |

| 4 | Banz R W. The relationship between return and market value of common stocks[J]. Journal of Financial Economics, 1981, 9(1): 3-18. |

| 5 | Chan K C, Chen N F. Structural and return characteristics of small and large firms[J]. The Journal of Finance, 1991, 46(4): 1467-1484. |

| 6 | Jegadeesh N, Titman S. Returns to buying winners and selling losers: Implications for stock market efficiency[J]. The Journal of Finance, 1993, 48(1): 65-91. |

| 7 | Ang A, Hodrick R J, Xing Y, et al. The cross-section of volatility and expected returns[J]. The Journal of Finance, 2006, 61(1): 259-299. |

| 8 | 邓晴元, 刘舟, 张顺明. 交易者过度自信与信息相关性暖昧的资产定价[J]. 系统工程理论与实践, 2022, 42(7): 1755-1769. |

| Deng Q Y, Liu Z, Zhang S M. Asset pricing with overconfident traders and information correlation ambiguity[J]. Systems Engineering-Theory & Practice, 2022, 42(7): 1755-1769. | |

| 9 | 陈国进, 刘元月, 陈凌凌, 等. 广义失望厌恶、下行风险与中国股票市场定价[J]. 中国管理科学,2023,31(7):22-37. |

| Chen G J, Liu Y Y, Chen L L, et al. Generalized disappointment aversion, downside risk and asset pricing of Chinese stock market[J]. Chinese Journal of Management Science, 2023,31(7):22-37. | |

| 10 | 万谍, 杨晓光. 中国股市正反馈交易涨强不对称的定价能力[J]. 系统工程理论与实践, 2019, 39(1): 1-18. |

| Wan D, Yang X G. Pricing power of rise-favor asymmetry of positive feedback trading in China's stock market[J]. Systems Engineering-Theory & Practice, 2019, 39(1): 1-18. | |

| 11 | Ross S A. The arbitrage theory of capital asset pricing[J].Journal of Economic Theory,1976,13(3): 341-360. |

| 12 | Tian M. Firm characteristics and empirical factor models: A model mining experiment[J]. The Review of Financial Studies, 2021, 34(12): 6087-6125. |

| 13 | Yara F B, Boyer B H, Davis C. The factor model failure puzzle[R]. Working Paper, Available at SSRN 3967588, 2021. |

| 14 | Fama E F, French K R. Common risk factors in the returns on stocks and bonds[J]. Journal of Financial Economics, 1993, 33(1): 3-56. |

| 15 | Fama E F, French K R. A five-factor asset pricing model[J]. Journal of Financial Economics, 2015, 116(1): 1-22. |

| 16 | Carhart M M. On persistence in mutual fund performance[J]. The Journal of Finance, 1997, 52(1): 57-82. |

| 17 | Hou K, Xue C, Zhang L. Digesting anomalies: An investment approach[J]. The Review of Financial Studies, 2015, 28(3): 650-705. |

| 18 | Stambaugh R F, Yuan Y. Mispricing factors[J]. The Review of Financial Studies, 2017, 30(4): 1270-1315. |

| 19 | Daniel K, Hirshleifer D, Sun L. Short-and long-horizon behavioral factors[J]. The Review of Financial Studies, 2020, 33(4): 1673-1736. |

| 20 | Hou K, Xue C, Zhang L. Replicating anomalies[J]. The Review of Financial Studies, 2020, 33(5): 2019-2133. |

| 21 | Kozak S, Nagel S, Santosh S. Shrinking the cross-section[J]. Journal of Financial Economics, 2020, 135(2): 271-292. |

| 22 | Bryzgalova S, Huang J, Julliard C. Bayesian solutions for the factor zoo: We just ran two quadrillion models[J]. The Journal of Finance, 2023,78(1): 487-557. |

| 23 | Rapach D E, Strauss J K, Zhou G. International stock return predictability: What is the role of the United States?[J]. The Journal of Finance, 2013, 68(4): 1633-1662. |

| 24 | Freyberger J, Neuhierl A, Weber M. Dissecting characteristics nonparametrically[J]. The Review of Financial Studies, 2020, 33(5): 2326-2377. |

| 25 | Feng G, Giglio S, Xiu D. Taming the factor zoo: A test of new factors[J]. The Journal of Finance, 2020, 75(3): 1327-1370. |

| 26 | Kelly B T, Pruitt S, Su Y. Characteristics are covariances: A unified model of risk and return[J]. Journal of Financial Economics, 2019, 134(3): 501-524. |

| 27 | Fan J, Liao Y, Wang W. Projected principal component analysis in factor models[J]. Annals of Statistics, 2016, 44(1): 219-254. |

| 28 | Kozak S, Nagel S, Santosh S. Interpreting factor models[J]. The Journal of Finance, 2018, 73(3): 1183-1223. |

| 29 | MacKinlay A C. Multifactor models do not explain deviations from the CAPM[J]. Journal of Financial Economics, 1995, 38(1): 3-28. |

| 30 | 黄嵩, 倪宣明, 钱龙, 等. 基于集成学习的在线高维投资组合策略[J].系统科学与数学,2020,40(1): 29-40. |

| Huang S, Ni X M, Qian L, et al. Large-dimensional online portfolio strategy based on ensemble learning[J]. Journal of Systems Science and Mathematical Sciences, 2020, 40(1): 29-40. | |

| 31 | 倪宣明, 沈鑫圆, 赵慧敏, 等. 基于多任务相关学习的投资组合优化[J]. 系统工程理论与实践, 2021, 41(6): 1428-1438. |

| Ni X M, Shen X Y, Zhao H M, et al. Portfolio optimization based on multi-task relationship learning[J]. Systems Engineering-Theory & Practice, 2021, 41(6): 1428-1438. | |

| 32 | 倪宣明, 邱语宁, 赵慧敏. 基于因子特征的高维稀疏投资组合优化[J]. 系统科学与数学, 2021, 41(10): 2716-2729. |

| Ni X M, Qiu Y N, Zhao H M. High-dimensional sparse portfolio optimization based on factor characteristics[J]. Journal of Systems Science and Mathematical Sciences, 2021, 41(10): 2716-2729. | |

| 33 | 倪宣明, 陈檬檬, 钱龙, 等. 基于因子载荷二叉树的高维投资组合优化[J]. 系统科学与数学, 2022, 42(9): 2312-2326. |

| Ni X M, Chen M M, Qian L, et al. High-dimensional portfolio optimization based on binary tree of factor loadings[J]. Journal of Systems Science and Mathematical Sciences, 2022, 42(9): 2312-2326. | |

| 34 | 钱龙, 韦江, 赵慧敏, 等. 基于AdaBoost的投资组合优化[J]. 系统科学与数学, 2022, 42(2): 271-286. |

| Qian L, Wei J, Zhao H M, et al. Portfolio optimization based on AdaBoost[J]. Journal of Systems Science and Mathematical Sciences, 2022, 42(2): 271-286. | |

| 35 | 钱龙,彭方平,沈鑫圆,等.基于已实现半协方差的投资组合优化[J].系统工程理论与实践,2021,41(1): 34-44. |

| Qian L, Peng F P, Shen X Y, et al. Portfolio optimization based on realized semi-covariance[J]. Systems Engineering-Theory & Practice, 2021,41(1): 34-44. | |

| 36 | Wei K C J. An asset-pricing theory unifying the CAPM and APT[J]. The Journal of Finance, 1988, 43(4): 881-892. |

| 37 | Huberman G, Kandel S. Mean-variance spanning[J]. The Journal of Finance, 1987, 42(4): 873-888. |

| 38 | Welch I. The link between Fama-French time-series tests and Fama-Macbeth cross-sectional tests[R]. Working Paper, Available at SSRN 1271935, 2008. |

| 39 | Grinblatt M, Saxena K. When factors do not span their basis portfolios[J]. Journal of Financial and Quantitative Analysis, 2018, 53(6): 2335-2354. |

| 40 | Daniel K, Mota L, Rottke S, et al. The cross-section of risk and returns[J]. The Review of Financial Studies, 2020, 33(5): 1927-1979. |

| 41 | Fama E F, French K R. Comparing cross-section and time-series factor models[J]. The Review of Financial Studies, 2020, 33(5): 1891-1926. |

| 42 | Lettau M, Pelger M. Factors that fit the time series and cross-section of stock returns[J]. The Review of Financial Studies, 2020, 33(5): 2274-2325. |

| 43 | Connor G, Korajczyk R A. Risk and return in an equilibrium APT: Application of a new test methodology[J]. Journal of Financial Economics, 1988, 21(2): 255-289. |

| 44 | Liu J, Stambaugh R F, Yuan Y. Size and value in China[J]. Journal of Financial Economics, 2019, 134(1): 48-69. |

| 45 | Newey W K, West K D. A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix[J]. Econometrica, 1987, 55(3): 703-708. |

| 46 | Gibbons M R, Ross S A, Shanken J. A test of the efficiency of a given portfolio[J]. Econometrica, 1989, 57(5): 1121-1152. |

| [1] | 刘超, 许澜涛. 多层时序网络视角下的最优投资组合策略研究[J]. 中国管理科学, 2025, 33(9): 46-56. |

| [2] | 林娟娟, 黄志刚, 唐勇. 数据质量、数量与数据资产定价:基于消费者异质性视角[J]. 中国管理科学, 2025, 33(5): 88-98. |

| [3] | 李星毅, 李仲飞, 李其谦, 刘昱君, 唐文金. 基于机器学习的资产收益率预测研究综述[J]. 中国管理科学, 2025, 33(1): 311-322. |

| [4] | 许启发, 王泽舟, 蒋翠侠. 基于生成对抗网络的混频资产定价研究[J]. 中国管理科学, 2024, 32(11): 53-64. |

| [5] | 张鹏, 崔淑琳, 李璟欣. 一致性均值-CVaR可信性投资组合优化[J]. 中国管理科学, 2023, 31(6): 111-121. |

| [6] | 陈淼鑫, 黄振伟. 股价波动的长记忆性与横截面股票收益——基于中国市场的实证研究[J]. 中国管理科学, 2023, 31(4): 1-10. |

| [7] | 黄光麟,鲁万波. 基于变系数多因子半参数分布的高维动态高阶矩投资组合研究[J]. 中国管理科学, 2023, 31(12): 272-280. |

| [8] | 陆静, 张银盈. “特质波动率之谜”与估计模型有关吗?[J]. 中国管理科学, 2022, 30(9): 36-48. |

| [9] | 杨瑞成, 邢伟泽. CRMW风险缓释效用目标跟踪的债券投资组合优化策略研究[J]. 中国管理科学, 2022, 30(7): 150-163. |

| [10] | 刘志东, 郑雪飞. 基于Hawkes因子模型的股价共同跳跃研究[J]. 中国管理科学, 2018, 26(7): 18-31. |

| [11] | 刘燕, 朱宏泉. 个体与机构投资者,谁左右A股股价变化?——基于投资者异质信念的视角[J]. 中国管理科学, 2018, 26(4): 120-130. |

| [12] | 徐元栋. BSV、DHS等模型中资产定价与模糊不确定性下资产定价在逻辑结构上的一致性[J]. 中国管理科学, 2017, 25(6): 22-31. |

| [13] | 龚旭, 文凤华, 黄创霞, 杨晓光. 下行风险、符号跳跃风险与行业组合资产定价[J]. 中国管理科学, 2017, 25(10): 1-10. |

| [14] | 葛静, 田新时. 中国利率期限结构的理论与实证研究——基于无套利DNS模型和DNS模型[J]. 中国管理科学, 2015, 23(2): 29-38. |

| [15] | 刘维奇, 邢红卫, 张信东. 投资偏好与“特质波动率之谜”——以中国股票市场A股为研究对象[J]. 中国管理科学, 2014, 22(8): 10-20. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||