主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2026, Vol. 34 ›› Issue (4): 47-62.doi: 10.16381/j.cnki.issn1003-207x.2024.0896

Previous Articles Next Articles

Zezhou Wang1, Qifa Xu1,2( ), Cuixia Jiang1

), Cuixia Jiang1

Received:2024-06-04

Revised:2024-10-19

Online:2026-04-25

Published:2026-03-27

Contact:

Qifa Xu

E-mail:xuqifa1975@163.com

CLC Number:

Zezhou Wang,Qifa Xu,Cuixia Jiang. Can Interaction and Dissemination of Mixed-Frequency Information in Companies' Multi-Layer Relationship Networks Improve Asset Pricing? Asset Pricing Study Based on Graph Neural Networks[J]. Chinese Journal of Management Science, 2026, 34(4): 47-62.

"

"

"

"

| 变量名称 | 构建方法 | 频率 | 变量名称 | 构建方法 | 频率 | 变量名称 | 构建方法 | 频率 |

|---|---|---|---|---|---|---|---|---|

| acc(应计) | 收入减经营现金除以资产 | 半年 | gma(毛利润) | 收入减去销售成本除以总资产 | 季 | roeq(净资产收益率) | 净利润除以股东权益平均余额 | 季 |

| agr(资产增长) | 总资产的年度变化率 | 年 | grCAPX(资本支出变化率) | 资本支出的年度变化率 | 年 | roic(投入资本回报率) | 税后净营业利润除以总投资额 | 季 |

| bm(账面市值比) | 账面价值除以市值 | 季 | hire(员工数目变化率) | 员工数目的年度变化率 | 年 | rsup(营业收入变化率市值比) | 营业收入的季度变化率除以总市值 | 季 |

| bm_ia(行业调整bm) | 个股账面市值比 减行业平均账面市值比 | 季 | invest(资本支出和存货) | 固定资产年变化率除以总资产 | 年 | tang(债务能力) | 现金及等价物加0.715倍应收账款加0.547 倍存货加0.535倍固定资产除以总资产 | 季 |

| cash(现金持有量) | 现金及等价物除以总资产 | 季 | lev(杠杆率) | 总负债除以市值 | 季 | sp(营业收入市值比) | 营业收入除以总市值 | 季 |

| cashdebt(现金债务比) | 现金及等价物除以总负债 | 季 | lgr(总负债变化率) | 总负债的季度变化率 | 季 | sgr(营业收入变化率) | 营业收入的季度变化率 | 季 |

| cfp(现金流价格比) | 经营现金流除以市值 | 季 | mve(规模) | 总市值的自然对数 | 季 | tb(税费收入比) | 4倍应交税费除以总收入 | 季 |

| maxret(最大日收益) | 过去一个月最大日收益 | 月 | mve_ia(行业调整规模) | 个股对数市值减行业平均市值 | 季 | zerotrade(零交易日) | 上月期交易量为0天数 | 月 |

| mom1 m(一个月动量) | 过去一个月累计收益 | 月 | operprof(经营获利能力) | 营业利润除以股东权益 | 季 | top1(最大股东持股) | 第1大股东占股比列 | 年 |

| mom6 m(6个月动量) | t-6月至t-1月的累积收益 | 月 | orgcap(组织资本) | 管理费用除以净资产总额 | 季 | top10(前10大股东持股) | 前10大股东占股比列 | 年 |

| chmom(6个月惯性) | t-6月至t-1月累积回报减 t-12至t-7的累计回报 | 月 | pchcurrat(流动比率变化率) | 流动比率的季度变化率 | 季 | Ownership(所有权) | 公司所有权性质(国企、私企、外资和其他) | 年 |

| mom12 m(12个月动量) | t-12到t-1月的累积收益 | 月 | pchquick(速动比率变化率) | 速动比率的季度变化率 | 季 | dp(股息价格比) | A股平均股利与平均股价对数之商 | 月 |

| mom36 m(36个月动量) | t-36至t-13月的累积收益 | 月 | pctacc(应计百分比) | 应计项目除以净利润 | 半年 | de(派息率) | A股平均股利与平均收益对数之商 | 月 |

| chpm(营业利润变化) | 营业利润除以收入变化率 | 季 | quick(速动比率) | 流动资产减存货除以流动负债 | 季 | svar(指数波动率) | 上证综合指数收益的平方 | 月 |

| chpm_ia(行业调整chpm) | 行业调整营业利润变化 | 季 | rd(研发费用占比) | 若研发费用占资产总额比例 | 季 | M_ntis(股本扩张) | 中国A股市场的净发行量除以A股总市值 | 月 |

| cinvest(公司投资) | 固定资产除以营业收入 | 季 | rd_mve(研发费用市值比) | 研发费用除以总市值 | 季 | infl(通货膨胀率) | 居民消费价格指数增长率 | 月 |

| currat(流动比率) | 流动资产除以流动负债 | 季 | rd_sale(研发费用营业收入比) | 研发费用除以营业收入 | 季 | m2gr(M2增长率) | 广义货币供应量增长率 | 月 |

| dy(本利比) | 年末总股息除以市值。 | 季 | realestate(房地产投资占比) | 房地产投资除以固定资产总额 | 季 | itgr(国际贸易额增长率) | 进出口总额增长率 | 月 |

| egr(权益增长率) | 账面价值季度变化率 | 季 | roaq(总资产收益率) | 净利润除以平均资产总额 | 季 | PPI(生产价格指数) | 工业生产者出厂价格增长率 | 月 |

"

| 变量名称 | 构建方法 | 频率 | 变量名称 | 构建方法 | 频率 | 变量名称 | 构建方法 | 频率 |

|---|---|---|---|---|---|---|---|---|

| beta(beta值) | CAPM模型回归系数 | 日 | BullishSent(看涨情绪指数) | 东方财富论坛个股看涨情绪指数 | 日 | oil(油价) | 西德克萨斯中质原油价格 | 日 |

| dolvol(对数交易额) | 交易额的自然对数 | 日 | PositiveSent(积极情绪指数) | 东方财富论坛个股积极情绪指数 | 日 | exchange(汇率) | 人民币元对美元汇率 | 日 |

| ill(Amihud流动性指标) | Amihud流动性指标 | 日 | news_senti(媒体情绪指数) | 个股新闻媒体情绪指数 | 日 | goldprice(金价) | 伦敦黄金市场价格 | 日 |

| volatility(收益波动率) | 收益率标准差 | 日 | searchindex(网络搜索指数) | 个股网络搜索指数 | 日 | shibor(上海银行间同业拆借利率) | 上海银行间同业拆借利率 | 日 |

| turnover(换手率) | 成交金额除以流通股数 | 日 | voldolvol(对数交易额波动率) | 对数交易额的标准差 | 周 | VIX(恐慌指数) | 芝加哥期权交易所波动率指数 | 日 |

| atr(异常换手率) | 个股换手率减市场换手率 | 日 | volturnover(换手率波动率) | 换手率的标准差 | 周 | ucirs(中美利差) | Shibor与美国联邦基金利率之差 | 日 |

| risk_factor(风险因子) | CAPM模型风险因子 | 日 | volill(ill波动率) | Amihud流动性指标的标准差 | 周 | Mturnover(市场换手率) | A股流通市值加权换手率 | 日 |

| ertrend(趋势因子) | 市场趋势因子 | 日 | volliquid(liquid波动率) | 流动性指标的标准差 | 周 | Mtrade_volume(市场交易量) | A股按流通市值加权交易量 | 日 |

| liquid(流动性) | 收益率除以成交金额 | 日 | volPB(PB波动率) | 市净率的标准差 | 周 | M_BullishSent(市场看涨情绪指数) | 东方财富论坛市场看涨情绪指数 | 日 |

| trade_volume(总交易金额) | 总交易金额 | 日 | volPE(PE波动率) | 市盈率的标准差 | 周 | M_PositiveSent(市场积极情绪指数) | 东方财富论坛市场积极情绪指数 | 日 |

| trade_number(总交易量) | 交易金额除以成交量 | 日 | voltrade_number(交易量波动) | 交易量的标准差 | 周 | M_news_senti(市场媒体情绪指数) | 市场新闻媒体情绪指数 | 日 |

| deltatrade_voulme(滞后交易量) | 总交易量的一阶滞后 | 日 | voltrade_volume(交易额波动) | 交易额的标准差 | 周 | M_searchindex(市场搜索指数) | 市场网络搜索指数 | 日 |

| PB(市净率) | 总市值除以净资产 | 日 | tms(利差) | 10年期国债利率减1年期国债利率 | 日 | SMB(市值因子) | 小盘组合和大盘组合收益率之差 | 日 |

| PE(市盈率) | 总市值除以归属母公司的净利润之和 | 日 | CMA(投资模式因子) | 低投资比例股票组合和高投资比例股票组合收益率差 | 日 | HML(账面市值比因子) | 高账面市值比股票组合和低账面市值比股票组合收益率差 | 日 |

| corrlation(相关系数) | 个股风险收益率与市场风险收益率的相关系数 | 日 | RMW(盈利能力因子) | 高盈利股票组合和 低盈利股票组合的收益率之差。 | 日 | ep(市场市盈率) | A股市场平均每股收益与平均股价对数商 | 日 |

"

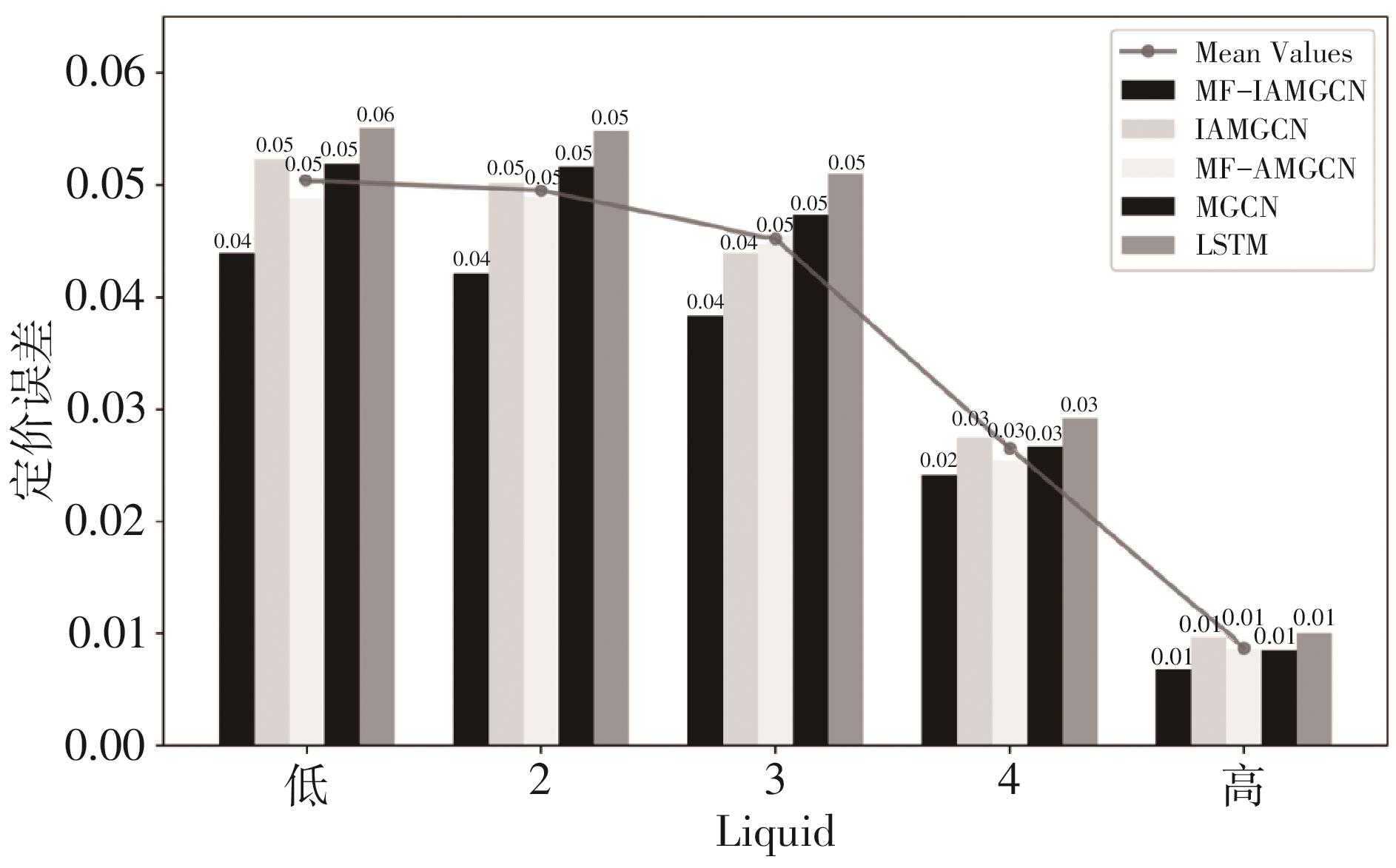

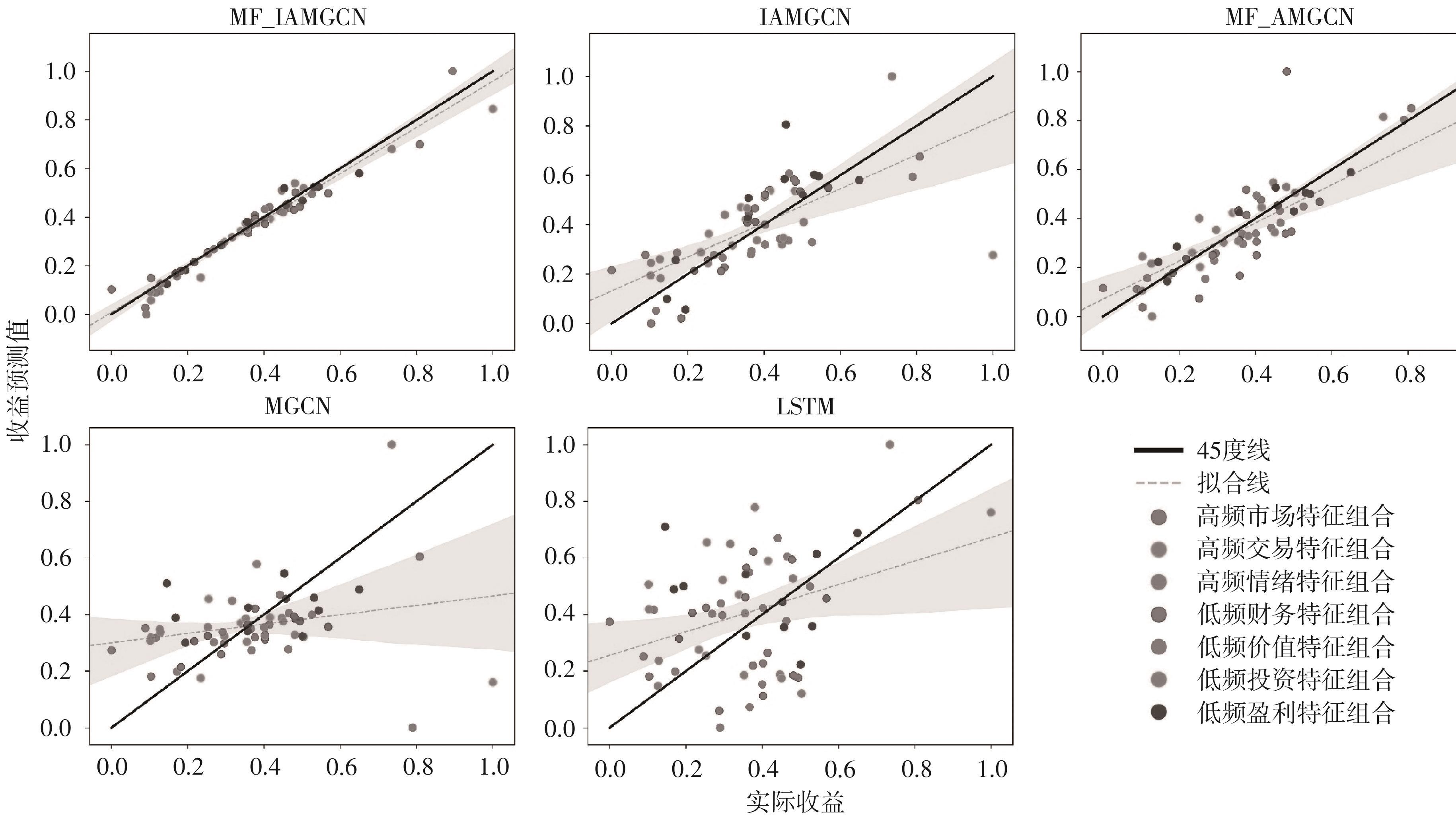

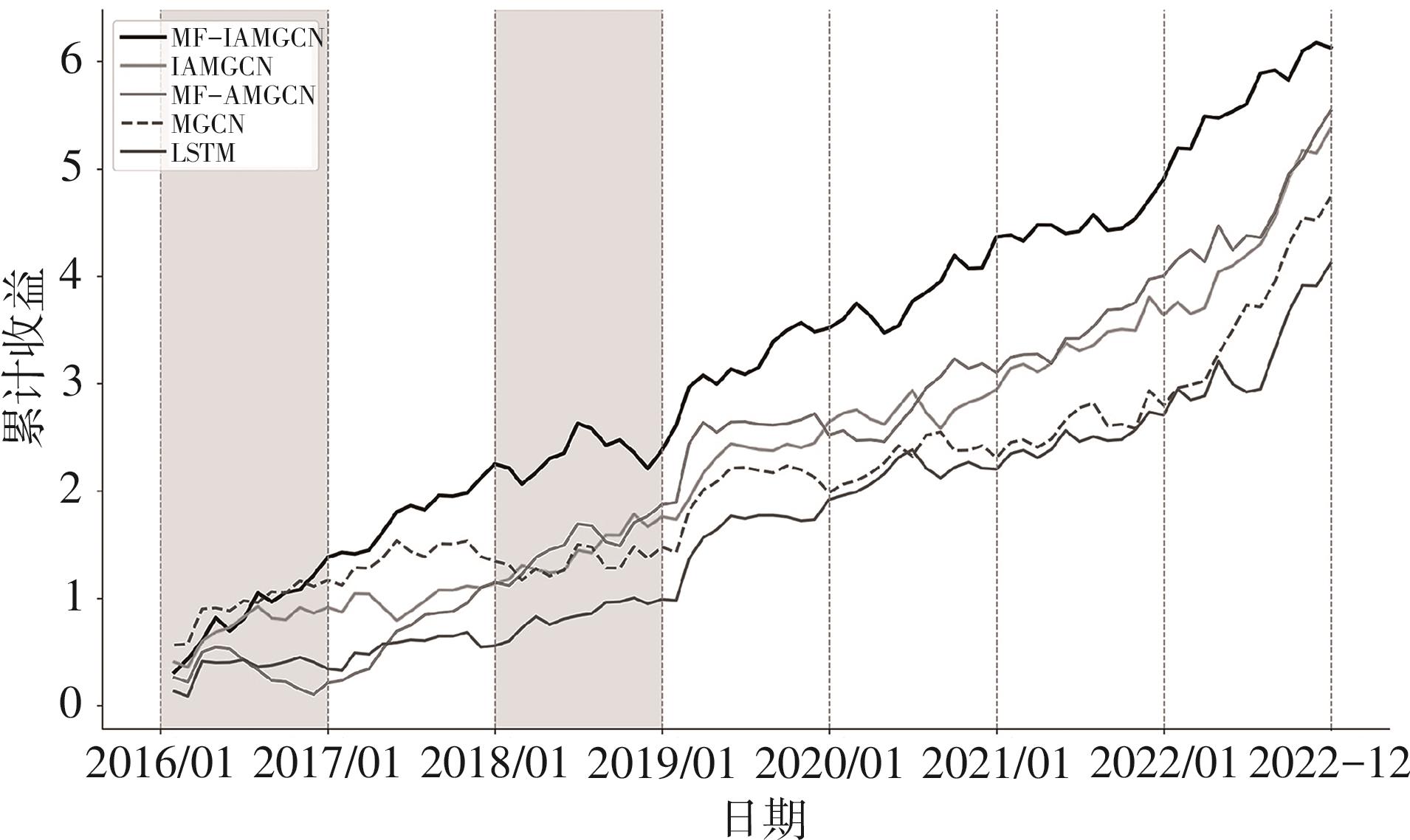

| 模型 | 混频数据处理 | 多层关系网络 | 网络信息同期交互 | 网络信息跨期传播 | 注意力机制 |

|---|---|---|---|---|---|

| MF-IAMGCN | √ | √ | √ | √ | √ |

| IAMGCN | × | √ | √ | √ | √ |

| MF-AMGCN | √ | √ | √ | × | √ |

| MGCN | × | √ | √ | × | × |

| LSTM | × | × | × | × | × |

"

| 模型 | EV | |

|---|---|---|

| MF-IAMGCN | 0.0446 | 0.6664 |

| IAMGCN | 0.0522 | 0.6044 |

| MF-AMGCN | 0.0497 | 0.6131 |

| MGCN | 0.0558 | 0.5724 |

| LSTM | 0.0583 | 0.5204 |

"

"

| 模型 | GF | |

|---|---|---|

| MF-IAMGCN | 0.0305 | 0.9563 |

| IAMGCN | 0.0366 | 0.8527 |

| MF-AMGCN | 0.0349 | 0.9237 |

| MGCN | 0.0389 | 0.7584 |

| LSTM | 0.0400 | 0.6743 |

"

| 模型 | SR | AR | MaxLoss | MD |

|---|---|---|---|---|

| MF-IAMGCN | 0.5740 | 0.0730 | 0.1555 | 0.1166 |

| IAMGCN | 0.5237 | 0.0640 | 0.2086 | 0.1221 |

| MF-AMGCN | 0.5191 | 0.0660 | 0.2268 | 0.2853 |

| MGCN | 0.4036 | 0.0564 | 0.2111 | 0.1449 |

| LSTM | 0.4276 | 0.0491 | 0.2129 | 0.0844 |

"

| 特征 | MF- IAMGCN | IAM-GCN | MF-AMGCN | MGCN | LSTM | 特征 | MF-IAMGCN | IAM-GCN | MF-AMGCN | MGCN | LSTM |

|---|---|---|---|---|---|---|---|---|---|---|---|

| acc | 0.9621 | 0.8679 | 0.9326 | 0.7610 | 0.6774 | quick | 0.9337 | 0.8455 | 0.9356 | 0.7549 | 0.6727 |

| agr | 0.9667 | 0.8663 | 0.9317 | 0.7576 | 0.6750 | rd | 0.9558 | 0.8351 | 0.9182 | 0.7542 | 0.6678 |

| bm | 0.9519 | 0.8667 | 0.9199 | 0.7652 | 0.6844 | rd_sale | 0.9539 | 0.8405 | 0.9211 | 0.7516 | 0.6665 |

| bm_ia | 0.9420 | 0.8266 | 0.9084 | 0.7423 | 0.6570 | realestate | 0.9600 | 0.8616 | 0.9317 | 0.7629 | 0.6795 |

| cash | 0.9579 | 0.8547 | 0.9273 | 0.7587 | 0.6734 | roaq | 0.9648 | 0.8676 | 0.9321 | 0.7666 | 0.6809 |

| cashdebt | 0.9629 | 0.8598 | 0.9279 | 0.7601 | 0.6726 | roeq | 0.9621 | 0.8676 | 0.9284 | 0.7635 | 0.6778 |

| cfp | 0.9501 | 0.8095 | 0.9010 | 0.7418 | 0.6597 | roic | 0.9534 | 0.8571 | 0.9238 | 0.7513 | 0.6692 |

| chmom | 0.9546 | 0.8215 | 0.9076 | 0.7473 | 0.6620 | rsup | 0.9549 | 0.8452 | 0.9110 | 0.7541 | 0.6690 |

| chpm | 0.9521 | 0.8494 | 0.9241 | 0.7532 | 0.6685 | sgr | 0.9370 | 0.8306 | 0.9466 | 0.7489 | 0.6595 |

| chpm_ia | 0.9491 | 0.8375 | 0.9201 | 0.7502 | 0.6667 | sp | 0.9647 | 0.8753 | 0.9259 | 0.7562 | 0.6760 |

| cinvest | 0.9623 | 0.8554 | 0.9227 | 0.7507 | 0.6646 | tang | 0.9659 | 0.8668 | 0.9332 | 0.7666 | 0.6885 |

| currat | 0.9534 | 0.8477 | 0.9268 | 0.7566 | 0.6738 | tb | 0.9611 | 0.8609 | 0.9229 | 0.7559 | 0.6732 |

| dy | 0.9489 | 0.8468 | 0.9247 | 0.7515 | 0.6676 | zerotrade | 0.9605 | 0.8654 | 0.9281 | 0.7758 | 0.6916 |

| egr | 0.9605 | 0.8625 | 0.9268 | 0.7537 | 0.6690 | top1 | 0.9606 | 0.8667 | 0.9266 | 0.7597 | 0.6792 |

| gma | 0.9601 | 0.8650 | 0.9288 | 0.7570 | 0.6700 | top10 | 0.9619 | 0.9147 | 0.9284 | 0.7598 | 0.6765 |

| grCAPX | 0.9386 | 0.8646 | 0.9408 | 0.7685 | 0.6838 | beta | 0.9573 | 0.8271 | 0.9273 | 0.7567 | 0.6653 |

| hire | 0.9604 | 0.8679 | 0.9314 | 0.7660 | 0.6818 | ill | 0.9576 | 0.8727 | 0.9293 | 0.7887 | 0.7066 |

| invest | 0.9595 | 0.8648 | 0.9254 | 0.7625 | 0.6776 | volatility | 0.9557 | 0.8592 | 0.9301 | 0.7649 | 0.6786 |

| lev | 0.9509 | 0.8673 | 0.9204 | 0.7650 | 0.6869 | turnover | 0.9652 | 0.8726 | 0.9359 | 0.7884 | 0.7006 |

| lgr | 0.9708 | 0.8698 | 0.9346 | 0.7605 | 0.6748 | atr | 0.9513 | 0.8580 | 0.9230 | 0.7585 | 0.6737 |

| maxret | 0.9667 | 0.8629 | 0.9312 | 0.7727 | 0.6900 | ertrend | 0.9647 | 0.8367 | 0.9064 | 0.7542 | 0.6702 |

| mom1m | 0.9481 | 0.8320 | 0.9077 | 0.7247 | 0.6343 | risk_factor | 0.9600 | 0.8554 | 0.9332 | 0.7694 | 0.6823 |

| mom6m | 0.9375 | 0.8110 | 0.9016 | 0.7375 | 0.6477 | corrlation | 0.9610 | 0.8633 | 0.9260 | 0.7637 | 0.6802 |

| mom12m | 0.9533 | 0.8204 | 0.9027 | 0.7537 | 0.6669 | PE | 0.9557 | 0.8539 | 0.9214 | 0.7591 | 0.6725 |

| mom36m | 0.9522 | 0.8135 | 0.9132 | 0.7421 | 0.6545 | PB | 0.9484 | 0.8598 | 0.9172 | 0.7698 | 0.6862 |

| mve | 0.9527 | 0.8543 | 0.9174 | 0.7526 | 0.6709 | trade_volume | 0.9519 | 0.8647 | 0.9218 | 0.7819 | 0.6996 |

| mve_ia | 0.9661 | 0.8686 | 0.9316 | 0.7726 | 0.6924 | trade_number | 0.9638 | 0.8622 | 0.9302 | 0.7826 | 0.6971 |

| operprof | 0.9525 | 0.8112 | 0.9089 | 0.7275 | 0.6443 | BullishSent | 0.9554 | 0.8347 | 0.9135 | 0.7542 | 0.6696 |

| orgcap | 0.9622 | 0.8578 | 0.9363 | 0.7345 | 0.6557 | news_senti | 0.9623 | 0.8609 | 0.9238 | 0.7668 | 0.6855 |

| pchcurrat | 0.9635 | 0.8535 | 0.9253 | 0.7505 | 0.6701 | PositiveSent | 0.9546 | 0.8381 | 0.9177 | 0.7543 | 0.6697 |

| pchquick | 0.9651 | 0.8581 | 0.9264 | 0.7559 | 0.6762 | searchindex | 0.9563 | 0.8617 | 0.9219 | 0.7662 | 0.6859 |

| pctacc | 0.9380 | 0.8064 | 0.9114 | 0.7331 | 0.6496 |

"

"

| mve/bm | MF-IAMGCN / IAMGCN / MF-AMGCN //MGCN / LSTM / 最小Odds ratio | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 市值↓ 账面市值比→ 低 | 2 | 3 | 4 | 高 | |||||||||||||||

| 低 | 0.9257 | 0.7997 | 0.8148 | 0.9009 | 0.7521 | 0.7448 | 0.8254 | 0.7416 | 0.7799 | 0.8118 | 0.7293 | 0.8058 | 0.7978 | 0.7206 | 0.7787 | ||||

| 0.8288 | 0.8388 | 1.1036 | 0.7080 | 0.7180 | 1.1979 | 0.5678 | 0.5778 | 1.0582 | 0.5491 | 0.5591 | 1.0074 | 0.4625 | 0.4725 | 1.0245 | |||||

| 2 | 0.9213 | 0.8371 | 0.8251 | 0.8923 | 0.8339 | 0.8785 | 0.8824 | 0.8168 | 0.8833 | 0.8082 | 0.7001 | 0.7808 | 0.8435 | 0.7235 | 0.7451 | ||||

| 0.8362 | 0.8462 | 1.0887 | 0.6325 | 0.6425 | 1.0158 | 0.6385 | 0.6485 | 0.9990 | 0.5338 | 0.5438 | 1.0351 | 0.5781 | 0.5881 | 1.1321 | |||||

| 3 | 0.9393 | 0.8023 | 0.8374 | 0.8928 | 0.8290 | 0.8763 | 0.8583 | 0.7919 | 0.8565 | 0.7718 | 0.6564 | 0.7699 | 0.8480 | 0.7506 | 0.7760 | ||||

| 0.8315 | 0.8415 | 1.1163 | 0.6028 | 0.6128 | 1.0189 | 0.6000 | 0.6100 | 1.0020 | 0.4208 | 0.4308 | 1.0025 | 0.5614 | 0.5714 | 1.0928 | |||||

| 4 | 0.9625 | 0.8522 | 0.8617 | 0.9105 | 0.7991 | 0.8285 | 0.9052 | 0.8122 | 0.8603 | 0.8119 | 0.7924 | 0.8029 | 0.8697 | 0.7923 | 0.8263 | ||||

| 0.8580 | 0.8680 | 1.1090 | 0.7421 | 0.7521 | 1.0990 | 0.7137 | 0.7237 | 1.0522 | 0.5796 | 0.5896 | 1.0112 | 0.7015 | 0.7115 | 1.0524 | |||||

| 高 | 0.9550 | 0.7969 | 0.9102 | 0.9866 | 0.8801 | 0.9053 | 0.9763 | 0.8849 | 0.9199 | 0.9446 | 0.8493 | 0.8939 | 0.9015 | 0.7994 | 0.8663 | ||||

| 0.9017 | 0.9117 | 1.0475 | 0.8928 | 0.9028 | 1.0898 | 0.8730 | 0.8830 | 1.0613 | 0.8705 | 0.8805 | 1.0567 | 0.8500 | 0.8600 | 1.0406 | |||||

"

"

"

| 模型 | 非ST | ST | 误差增幅 |

|---|---|---|---|

| MF-IAMGCN | 0.0533 | 0.0621 | 16.51% |

| MF-IAMGCN-E | 0.0601 | 0.0814 | 35.44% |

| GCN+E | 0.0686 | 0.0779 | 13.56% |

"

| [1] | Cochrane J H. Presidential address: Discount rates[J]. The Journal of Finance, 2011, 66(4): 1047-1108. |

| [2] | Sharpe W F. Capital asset prices: A theory of market equilibrium under conditions of risk[J]. The Journal of Finance, 1964, 19(3): 425-442. |

| [3] | Fama E F, French K R. The cross-section of expected stock returns[J]. The Journal of Finance, 1992, 47(2): 427. |

| [4] | Carhart M M. On persistence in mutual fund performance[J]. The Journal of Finance, 1997, 52(1): 57-82. |

| [5] | De Bondt W F M, Thaler R. Does the stock market overreact?[J]. The Journal of Finance, 1985, 40(3): 793-805. |

| [6] | Black F. Capital market equilibrium with restricted borrowing[J]. The Journal of Business, 1972, 45(3): 444-455. |

| [7] | Shi J, Liu X, Li Y, et al. Does supply chain network centrality affect stock price crash risk? Evidence from Chinese listed manufacturing companies[J]. International Review of Financial Analysis, 2022, 80: 102040. |

| [8] | Wen F, Yuan Y, Zhou W X. Cross-shareholding networks and stock price synchronicity: Evidence from China[J]. International Journal of Finance & Economics, 2021, 26(1): 914-948. |

| [9] | Chen W, Qu S, Jiang M, et al. The construction of multilayer stock network model[J]. Physica A: Statistical Mechanics and Its Applications, 2021, 565: 125608. |

| [10] | 王纲金, 吴昊钰, 谢赤. 基于多层关联网络的投资组合优化研究[J]. 系统工程理论与实践, 2022, 42(4): 937-957. |

| Wang G J, Wu H Y, Xie C. Portfolio optimization based on multilayer connectedness networks[J]. Systems Engineering-Theory & Practice, 2022, 42(4): 937-957. | |

| [11] | 刘超, 许澜涛. 多层时序网络视角下的最优投资组合策略研究[J]. 中国管理科学, 2025, 33(9): 46-56. |

| Liu C, Xu L T. Study on optimal portfolio strategy from the perspective of multilayer temporal network[J]. Chinese Journal of Management Science, 2025, 33(9): 46-56. | |

| [12] | Manessi F, Rozza A, Manzo M. Dynamic graph convolutional networks[J]. Pattern Recognition, 2020, 97: 107000. |

| [13] | Wu Z, Pan S, Chen F, et al. A comprehensive survey on graph neural networks[J]. IEEE Transactions on Neural Networks and Learning Systems, 2021, 32(1): 4-24. |

| [14] | Chen W, Jiang M, Zhang W G, et al. A novel graph convolutional feature based convolutional neural network for stock trend prediction[J]. Information Sciences, 2021, 556: 67-94. |

| [15] | Song G, Zhao T, Wang S, et al. Stock ranking prediction using a graph aggregation network based on stock price and stock relationship information[J]. Information Sciences, 2023, 643: 119236. |

| [16] | 卜湛, 张善凡, 李雪延, 等. 基于深度强化学习的自适应股指预测研究[J]. 管理科学学报, 2023, 26(4): 148-174. |

| Bu Z, Zhang S F, Li X Y, et al. Adaptive stock index prediction based on deep reinforcement learning[J]. Journal of Management Sciences in China, 2023, 26(4): 148-174. | |

| [17] | Tan J, Li Q, Wang J, et al. FinHGNN: A conditional heterogeneous graph learning to address relational attributes for stock predictions[J]. Information Sciences, 2022, 618: 317-335. |

| [18] | Brunnermeier M, Farhi E, Koijen R S J, et al. Review article: Perspectives on the future of asset pricing[J]. The Review of Financial Studies, 2021, 34(4): 2126-2160. |

| [19] | Ghysels E, Santa-Clara P, Valkanov R. Predicting volatility: Getting the most out of return data sampled at different frequencies[J]. Journal of Econometrics, 2006, 131(1-2): 59-95. |

| [20] | 谭德凯, 田利辉. 黄金是股票市场的“避险天堂”吗?——基于动态条件相关混频数据抽样模型[J]. 中国管理科学, 2022, 30(10): 14-24. |

| Tan D K, Tian L H. Is gold a safe haven of the stock market? —Based on dynamic conditional correlation mixed data sampling model[J]. Chinese Journal of Management Science, 2022, 30(10): 14-24. | |

| [21] | 刘凤根, 吴军传, 杨希特, 等. 基于混频数据模型的宏观经济对股票市场波动的长期动态影响研究[J]. 中国管理科学, 2020, 28(10): 65-76. |

| Liu F G, Wu J C, Yang X T, et al. Long-Run dynamic effect of macro-economy on stock market volatility based on mixed frequency data model[J]. Chinese Journal of Management Science, 2020, 28(10): 65-76. | |

| [22] | Yang C, Zhang R. Does mixed-frequency investor sentiment impact stock returns? Based on the empirical study of MIDAS regression model[J]. Applied Economics, 2014, 46(9): 966-972. |

| [23] | Xu M, Fu P, Liu B, et al. Multi-stream attention-aware graph convolution network for video salient object detection[J]. IEEE Transactions on Image Processing, 2021, 30: 4183-4197. |

| [24] | Shi J, Zhang W, Bao Y, et al. Load forecasting of electric vehicle charging stations: Attention based spatiotemporal multi-graph convolutional networks[J]. IEEE Transactions on Smart Grid, 2024, 15(3): 3016-3027. |

| [25] | 胡春华, 邓奥, 童小芹, 等. 社交电商中融合信任和声誉的图神经网络推荐研究[J]. 中国管理科学, 2021, 29(10): 202-212. |

| Hu C H, Deng A, Tong X Q, et al. A graph neural network recommendation study combining trust and reputation in social E-commerce[J]. Chinese Journal of Management Science, 2021, 29(10): 202-212. | |

| [26] | 陈妍, 张小威, 金赞, 等. 基于加权GraphSAGE和生成对抗网络的医保欺诈识别方法[J]. 系统工程理论与实践, 2024, 44(2): 732-751. |

| Chen Y, Zhang X W, Jin Z, et al. Medical fraud detection method based on weighted GraphSAGE and generative adversarial network[J]. Systems Engineering-Theory & Practice, 2024, 44(2): 732-751. | |

| [27] | Lin Y, Yan Y, Xu J, et al. Forecasting stock index price using the CEEMDAN-LSTM model[J]. The North American Journal of Economics and Finance, 2021, 57: 101421. |

| [28] | Ghysels E, Kvedaras V, Zemlys V. Mixed frequency data sampling regression models: The R package midasr[J]. Journal of Statistical Software, 2016, 72(4): 1-35. |

| [29] | Leippold M, Wang Q, Zhou W. Machine learning in the Chinese stock market[J]. Journal of Financial Economics, 2022, 145(2): 64-82. |

| [30] | 邵新建, 贾中正, 赵映雪, 等. 借壳上市、内幕交易与股价异动——基于ST类公司的研究[J]. 金融研究, 2014(5): 126-142. |

| Shao X J, Jia Z Z, Zhao Y X, et al. Reverse merger, insider trading and abnormal market reaction: Evidence from ST listed companies in China[J]. Journal of Financial Research, 2014(5): 126-142. |

| [1] | Juanjuan Lin, Zhigang Huang, Yong Tang. Data Quality, Quantity and Data Asset Pricing: Based on the Perspective of Consumer Heterogeneity [J]. Chinese Journal of Management Science, 2025, 33(5): 88-98. |

| [2] | Xingyi Li, Zhongfei Li, Qiqian Li, Yujun Liu, Wenjin Tang. A Review of Research on Asset Return Prediction Based on Machine Learning [J]. Chinese Journal of Management Science, 2025, 33(1): 311-322. |

| [3] | Xuanming Ni,Tiantian Zheng,Huimin Zhao,Kangping Wu. Asset Pricing Based on the Optimal Idiosyncratic Return Factor [J]. Chinese Journal of Management Science, 2024, 32(8): 50-60. |

| [4] | Qifa Xu, Zezhou Wang, Cuixia Jiang. Research on Mixed Frequency Asset Pricing Based on Generative Adversarial Network [J]. Chinese Journal of Management Science, 2024, 32(11): 53-64. |

| [5] | Dawen Yan,Cun Li,Guotai Chi. Dynamic Financial Distress Prediction for Chinese Listed Companies Based on the Mixed Frequency Data [J]. Chinese Journal of Management Science, 2024, 32(1): 1-12. |

| [6] | CHEN Miao-xin, HUANG Zhen-wei. Long Memory Volatility and Cross-section Stock Returns: Empirical Research in Chinese Stock Market [J]. Chinese Journal of Management Science, 2023, 31(4): 1-10. |

| [7] | LU Jing, ZHANG Yin-ying. Idiosyncratic Volatility Puzzle and Its Estimation Model [J]. Chinese Journal of Management Science, 2022, 30(9): 36-48. |

| [8] | LIU Yan, ZHU Hong-quan. Individual Investor or Institutional Investor, Who Dominates Asset Pricing in Chinese A-share Stock Market? [J]. Chinese Journal of Management Science, 2018, 26(4): 120-130. |

| [9] | XU Yuan-dong. The Consistency of Logical Structure about Asset Pricing in BSV, DHS model and Asset Pricing under Ambiguity [J]. Chinese Journal of Management Science, 2017, 25(6): 22-31. |

| [10] | GONG Xu, WEN Feng-hua, HUANG Chuang-xia, YANG Xiao-guang. Downside Risk, Signed Jump Risk and Asset Pricing of Industry Portfolios [J]. Chinese Journal of Management Science, 2017, 25(10): 1-10. |

| [11] | LIU Wei-qi, XING Hong-wei, ZHANG Xin-dong. Investment Preference and the Idiosyncratic Volatility Puzzle——Evidence from China Stock Market [J]. Chinese Journal of Management Science, 2014, 22(8): 10-20. |

| [12] | ZHOU Fang, ZHANG Wei, ZHOU Bing. Capital Asset Pricing Model Based on Liquidity Risk [J]. Chinese Journal of Management Science, 2013, 21(5): 1-7. |

| [13] | ZHU Hong-quan, CHEN Lin, PAN Ning-ning. Industry, Local and Market Information, Who Dominates Price Movement in Chinese Stock Market? [J]. Chinese Journal of Management Science, 2011, 19(4): 1-8. |

| [14] | LUO Deng-yue, WANG Chun-feng, FANG Zhen-ming. An Empirical Research on the Relationship between Aggregate Liquidity and Asset Pricing in China Stock Market [J]. Chinese Journal of Management Science, 2007, 15(2): 33-38. |

| [15] | LU Jing, TANG Xiao-wo. The Empirical Study on Multi-Factor Pricing Model Based on Liquidity Risk [J]. Chinese Journal of Management Science, 2006, (5): 45-51. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||