主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2026, Vol. 34 ›› Issue (2): 67-78.doi: 10.16381/j.cnki.issn1003-207x.2023.1719

Previous Articles Next Articles

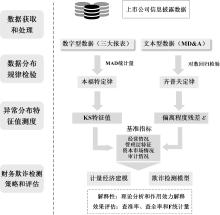

Guowen Li1, Yuhao Gong2, Jingyu Li3( ), Shuai Wang1

), Shuai Wang1

Received:2023-10-25

Revised:2024-09-16

Online:2026-02-25

Published:2026-02-04

Contact:

Jingyu Li

E-mail:lijy@bjut.edu.cn

CLC Number:

Guowen Li,Yuhao Gong,Jingyu Li, et al. Test for Anomalous Distribution of Information Disclosure: A New Strategy for Financial Fraud Detection[J]. Chinese Journal of Management Science, 2026, 34(2): 67-78.

"

"

| 行业 | 样本数 | 行业 | 样本数 | ||

|---|---|---|---|---|---|

| 交通运输 | 1226 | 0.00081 | 煤炭 | 431 | 0.00239 |

| 传媒 | 1390 | 0.00130 | 环保 | 782 | 0.00184 |

| 公用事业 | 1143 | 0.00110 | 电力设备 | 2111 | 0.00095 |

| 农林牧渔 | 904 | 0.00160 | 电子 | 2224 | 0.00078 |

| 医药生物 | 3110 | 0.00039 | 石油石化 | 483 | 0.00168 |

| 商贸零售 | 1018 | 0.00083 | 社会服务 | 650 | 0.00181 |

| 国防军工 | 901 | 0.00164 | 纺织服饰 | 918 | 0.00216 |

| 基础化工 | 2546 | 0.00082 | 综合 | 327 | 0.00155 |

| 家用电器 | 669 | 0.00143 | 美容护理 | 152 | 0.00420 |

| 建筑材料 | 760 | 0.00097 | 计算机 | 2115 | 0.00160 |

| 建筑装饰 | 1096 | 0.00079 | 轻工制造 | 919 | 0.00233 |

| 房地产 | 1454 | 0.00099 | 通信 | 837 | 0.00100 |

| 有色金属 | 1157 | 0.00155 | 钢铁 | 453 | 0.00208 |

| 机械设备 | 3045 | 0.00095 | 食品饮料 | 934 | 0.00140 |

| 汽车 | 1741 | 0.00061 | 所有公司 | 35496 | 0.00052 |

"

| 行业 | 样本数 | 百分比 | 行业 | 样本数 | 百分比 |

|---|---|---|---|---|---|

| 交通运输 | 1226 | 89.89 | 煤炭 | 431 | 90.49 |

| 传媒 | 1390 | 84.89 | 环保 | 782 | 86.32 |

| 公用事业 | 1143 | 86.35 | 电力设备 | 2111 | 87.87 |

| 农林牧渔 | 904 | 86.95 | 电子 | 2224 | 87.1 |

| 医药生物 | 3110 | 86.4 | 石油石化 | 483 | 87.78 |

| 商贸零售 | 1018 | 88.51 | 社会服务 | 650 | 87.85 |

| 国防军工 | 901 | 86.68 | 纺织服饰 | 918 | 84.10 |

| 基础化工 | 2546 | 84.17 | 综合 | 327 | 89.30 |

| 家用电器 | 669 | 82.36 | 美容护理 | 152 | 80.92 |

| 建筑材料 | 760 | 87.11 | 计算机 | 2115 | 86.05 |

| 建筑装饰 | 1096 | 86.95 | 轻工制造 | 919 | 82.48 |

| 房地产 | 1454 | 90.10 | 通信 | 837 | 86.02 |

| 有色金属 | 1157 | 85.57 | 钢铁 | 453 | 85.21 |

| 机械设备 | 3045 | 85.52 | 食品饮料 | 934 | 84.15 |

| 汽车 | 1741 | 86.73 | 所有公司 | 35496 | 86.36 |

"

| 行业 | 词语数 | 系数 | 行业 | 词语数 | 系数 | ||

|---|---|---|---|---|---|---|---|

| 交通运输 | 191 | -0.82*** | 0.973 | 煤炭 | 284 | -0.75*** | 0.979 |

| 传媒 | 206 | -0.82*** | 0.973 | 环保 | 196 | -0.77*** | 0.974 |

| 公用事业 | 173 | -0.84*** | 0.969 | 电力设备 | 265 | -0.86*** | 0.974 |

| 农林牧渔 | 150 | -0.78*** | 0.977 | 电子 | 231 | -0.86*** | 0.975 |

| 医药生物 | 551 | -0.96*** | 0.971 | 石油石化 | 661 | -0.72*** | 0.969 |

| 商贸零售 | 149 | -0.78*** | 0.972 | 社会服务 | 101 | -0.74*** | 0.976 |

| 国防军工 | 89 | -0.76*** | 0.977 | 纺织服饰 | 141 | -0.80*** | 0.976 |

| 基础化工 | 413 | -0.89*** | 0.976 | 综合 | 254 | -0.69*** | 0.988 |

| 家用电器 | 172 | -0.70*** | 0.979 | 计算机 | 218 | -0.88*** | 0.970 |

| 建筑材料 | 104 | -0.77** | 0.975 | 轻工制造 | 159 | -0.81*** | 0.974 |

| 建筑装饰 | 220 | -0.84*** | 0.978 | 通信 | 101 | -0.79*** | 0.974 |

| 房地产 | 268 | -0.85*** | 0.979 | 钢铁 | 243 | -0.68*** | 0.975 |

| 有色金属 | 176 | -0.83*** | 0.968 | 食品饮料 | 138 | -0.78*** | 0.977 |

| 机械设备 | 297 | -0.88*** | 0.973 | 所有公司 | 4910 | -1.122*** | 0.975 |

| 汽车 | 152 | -0.81*** | 0.976 |

"

| 申万行业 | 非欺诈组 | 欺诈组 | 申万行业 | 非欺诈组 | 欺诈组 |

|---|---|---|---|---|---|

| 交通运输 | 86.27 | 76.92 | 煤炭 | 90.16 | 81.82 |

| 传媒 | 88.72 | 88.33 | 环保 | 92.41 | 84.62 |

| 公用事业 | 87.41 | 83.33 | 电力设备 | 91.62 | 82.56 |

| 农林牧渔 | 88.46 | 89.19 | 电子 | 90.12 | 82.22 |

| 医药生物 | 88.92 | 87.93 | 石油石化 | 85.37 | 85.00 |

| 商贸零售 | 91.45 | 85.19 | 社会服务 | 91.80 | 78.57 |

| 国防军工 | 92.96 | 80.00 | 纺织服饰 | 93.20 | 77.42 |

| 基础化工 | 88.34 | 86.89 | 综合 | 86.21 | 76.47 |

| 家用电器 | 94.00 | 80.00 | 计算机 | 95.63 | 86.05 |

| 建筑材料 | 86.84 | 90.91 | 轻工制造 | 89.84 | 96.00 |

| 建筑装饰 | 92.94 | 85.71 | 通信 | 98.36 | 72.41 |

| 房地产 | 92.99 | 84.09 | 钢铁 | 91.11 | 87.50 |

| 有色金属 | 88.24 | 87.50 | 食品饮料 | 91.30 | 83.87 |

| 机械设备 | 87.78 | 82.26 | 所有公司 | 89.94 | 84.49 |

| 汽车 | 79.78 | 84.62 |

"

| 变量 | 样本数 | 欺诈公司 | 非欺诈公司 | 均值差异 | ||

|---|---|---|---|---|---|---|

| 均值 | 标准差 | 均值 | 标准差 | |||

| 4627 | 0.84 | 0.36 | 0.90 | 0.30 | -0.06*** | |

| 4627 | 0.31 | 0.05 | 0.24 | 0.04 | 0.07*** | |

| 公司规模 | 4627 | 9.73 | 0.50 | 9.98 | 0.62 | -0.25*** |

| 资产负债率 | 4627 | 0.50 | 0.21 | 0.47 | 0.20 | 0.03*** |

| 总应计项 | 4627 | -0.02 | 0.29 | -0.02 | 0.10 | 0.00 |

| 其他应收款比率 | 4627 | 0.03 | 0.05 | 0.02 | 0.03 | 0.01*** |

| 是否亏损 | 4627 | 0.24 | 0.43 | 0.10 | 0.30 | 0.14*** |

| 应收账款周转率 | 4627 | 0.60 | 0.52 | 0.66 | 0.52 | -0.06*** |

| 折旧率指数 | 4627 | 0.90 | 4.79 | 0.90 | 7.27 | 0.00 |

| ROA | 4627 | 0.01 | 0.18 | 0.04 | 0.07 | -0.03*** |

| ROA增长率 | 4627 | -1.98 | 13.48 | -0.28 | 31.49 | -1.70* |

| 股权集中度 | 4627 | 0.13 | 0.10 | 0.17 | 0.12 | -0.03*** |

| 机构投资者持股比例 | 4627 | 0.37 | 0.23 | 0.45 | 0.23 | -0.07*** |

| 独立董事比例 | 4627 | 0.37 | 0.05 | 0.38 | 0.06 | 0.01** |

| Z指数 | 4627 | 7.37 | 12.19 | 7.64 | 14.74 | -0.26 |

| 董事长与总经理兼任 | 4627 | 0.28 | 0.45 | 0.27 | 0.44 | 0.01 |

| 股票月换手波动率 | 4627 | -0.02 | 0.43 | -0.06 | 0.47 | 0.04** |

| 账面市值比 | 4627 | 0.69 | 0.24 | 0.75 | 0.25 | -0.06*** |

| 股市周期 | 4627 | 0.31 | 0.46 | 0.29 | 0.45 | 0.03* |

| 特别处理ST | 4627 | 0.11 | 0.43 | 0.03 | 0.25 | 0.08*** |

| 审计意见 | 4627 | 0.84 | 0.37 | 0.97 | 0.17 | -0.13*** |

| 审计公司资质 | 4627 | 0.04 | 0.19 | 0.09 | 0.29 | -0.05*** |

"

"

| 变量 | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| 常数项 | 0.508 | 1.170 | 2.501 | -0.019 |

| -0.512** | -0.498*** | -0.732* | -0.467*** | |

| 104.021*** | 36.131*** | 53.948*** | 39.413*** | |

| 公司规模 | 0.444*** | -0.772*** | -2.559* | -0.887*** |

| 资产负债率 | 3.935*** | 1.081*** | 2.187 | 0.483 |

| 总应计项 | 2.083* | 0.823* | 0.217 | 0.337* |

| 其他应收款比率 | 51.152*** | 3.903*** | 12.374*** | 3.898*** |

| 是否亏损 | 1.041* | 0.0528 | -0.058* | 0.321** |

| 应收账款周转率 | 0.875 | -0.235** | -0.858 | -0.326*** |

| 折旧率指数 | 0.999 | -0.004 | -0.749** | -0.008 |

| ROA | 0.460 | -0.594 | -2.398 | -0.346 |

| ROA增长率 | 1.000 | 0.001 | -0.013 | 0.001 |

| 股权集中度 | 0.660 | -1.008* | 2.421 | -1.917*** |

| 机构投资者持股比例 | 0.948 | -0.036 | 0.145 | 0.430 |

| 独立董事比例 | 0.604 | -0.512 | -1.658 | 0.887 |

| Z指数 | 1.009*** | 0.009*** | 0.012* | 0.009** |

| 董事长与总经理兼任 | 0.814** | -0.168 | 0.381 | -0.084 |

| 股票月换手波动率 | 0.995 | -0.031 | 0.672* | 0.127 |

| 账面市值比 | 0.752 | -0.662*** | 0.514 | 0.132 |

| 股市周期 | 0.980 | -0.041 | - | - |

| 特别处理ST | 0.869 | -0.170 | -0.186 | 0.033 |

| 审计意见 | 0.324*** | -1.125*** | 1.125* | -1.289*** |

| 审计公司资质 | 0.881 | -0.166 | 1.436 | -0.554** |

| 固定年份 | 否 | 否 | 是 | 是 |

| 固定行业 | 否 | 是 | 否 | 是 |

| Pseudo | 0.3520 | 0.3886 | 0.4775 | 0.5133 |

| 1717.40*** | 1886.26*** | 1724.24*** | 2504.12*** |

"

| 检测模型 | 比较基准 | 最大提升 | |||

|---|---|---|---|---|---|

| 面板A:准确率比较结果 | |||||

| 逻辑回归 | 0.6177 | 0.6274*** | 0.7934*** | +0.1784 | |

| 支持向量机 | 0.7437 | 0.7463** | 0.8260*** | +0.0863 | |

| 随机森林 | 0.7431 | 0.7442 | 0.8564*** | +0.1140 | |

| 长短期记忆网络 | 0.6882 | 0.6946*** | 0.6904*** | +0.1383 | |

| 循环神经网络 | 0.6298 | 0.6396* | 0.8103*** | +0.1849 | |

| RUSBoost | 0.6548 | 0.6545 | 0.7702*** | +0.1233 | |

| 面板B:查准率比较结果 | |||||

| 逻辑回归 | 0.6396 | 0.6522*** | 0.8071*** | +0.1728 | |

| 支持向量机 | 0.6919 | 0.6903 | 0.8162*** | +0.1316 | |

| 随机森林 | 0.7553 | 0.7538 | 0.8648*** | +0.1117 | |

| 长短期记忆网络 | 0.7154 | 0.7189* | 0.7134 | +0.1154 | |

| 循环神经网络 | 0.6644 | 0.6682 | 0.8287*** | +0.1695 | |

| RUSBoost | 0.6686 | 0.6675 | 0.7888*** | +0.1240 | |

| 面板C:查全率比较结果 | |||||

| 逻辑回归 | 0.5480 | 0.5546*** | 0.7714*** | +0.2242 | |

| 支持向量机 | 0.8836 | 0.8429*** | 0.8416*** | +0.0136 | |

| 随机森林 | 0.7222 | 0.7280** | 0.8427*** | +0.1251 | |

| 长短期记忆网络 | 0.6277 | 0.6416*** | 0.6398*** | +0.1935 | |

| 循环神经网络 | 0.5323 | 0.5563* | 0.7838*** | +0.2551 | |

| RUSBoost | 0.6139 | 0.6156 | 0.7377*** | +0.1390 | |

| 面板D:F1度量比较 | |||||

| 逻辑回归 | 0.5887 | 0.5979*** | 0.7889*** | +0.2023 | |

| 支持向量机 | 0.7747 | 0.7792** | 0.8289*** | +0.0572 | |

| 随机森林 | 0.7376 | 0.7399* | 0.8544** | +0.1181 | |

| 长短期记忆网络 | 0.6679 | 0.6772*** | 0.6736*** | +0.1577 | |

| 循环神经网络 | 0.5818 | 0.6034** | 0.8052*** | +0.2278 | |

| RUSBoost | 0.6393 | 0.6394* | 0.7617*** | +0.1322 | |

"

| [1] | Li G, Wang S, Feng Y. Making differences work: Financial fraud detection based on multi-subject perceptions[J]. Emerging Markets Review,2024, 60: 101134. |

| [2] | Beasley M S, Hermanson D R, Carcello J V, et al. Fraudulent financial reporting: 1998-2007: An analysis of US public companies[R].Working Paper,Committee of Sponsoring Organizations of the Treadway Commission, 2010. |

| [3] | ACFE. Report to the nation: 2020 global study on occupation fraud and abuse[R].Working Paper, ACFE Global Headquarters, 2020. |

| [4] | Zhu X, Ao X, Qin Z, et al. Intelligent financial fraud detection practices in post-pandemic era[J]. The Innovation, 2021, 2(4): 100176. |

| [5] | Beneish M D. The detection of earnings manipulation[J]. Financial Analysts Journal, 1999, 55(5): 24-36. |

| [6] | Jones J J. Earnings management during import relief investigations[J].Journal of Accounting Research, 1991, 29(2): 193-228. |

| [7] | Dechow P M, Ge W, Larson C R, et al. Predicting material accounting misstatements[J]. Contemporary Accounting Research, 2011, 28(1): 17-82. |

| [8] | Chen G, Firth M, Gao D N, et al. Ownership structure, corporate governance, and fraud: Evidence from China[J]. Journal of Corporate Finance, 2006, 12(3): 424-448. |

| [9] | 温石刚, 朱晓谦, 李建平. 公司财务欺诈行为的同群效应: 基于连锁董事网络社团的研究[J]. 工程管理科技前沿, 2023, 42(3): 20-28. |

| Wen S G, Zhu X Q, Li J P. A study on the peer effect of financial statement fraud based on the communities of interlocking director networks[J]. Frontiers of Science and Technology of Engineering Management, 2023, 42(3): 20-28. | |

| [10] | DeFond M L, Subramanyam K R. Auditor changes and discretionary accruals[J]. Journal of Accounting and Economics, 1998, 25(1): 35-67. |

| [11] | Erickson M, Hanlon M, Maydew E L. Is there a link between executive equity incentives and accounting fraud?[J]. Journal of Accounting Research, 2006, 44(1): 113-143. |

| [12] | Li J, Chang Y, Wang Y, et al. Tracking down financial statement fraud by analyzing the supplier-customer relationship network[J]. Computers & Industrial Engineering, 2023, 178: 109118. |

| [13] | Dechow P M, Sloan R G, Sweeney A P. Detecting earnings management[J]. The Accounting Review, 1995, 70(2): 193-225. |

| [14] | Liu R, Huang J, Zhang Z. Tracking disclosure change trajectories for financial fraud detection[J]. Production and Operations Management, 2023, 32(2): 584-602. |

| [15] | Amiram D, Bozanic Z, Rouen E. Financial statement errors: Evidence from the distributional properties of financial statement numbers[J]. Review of Accounting Studies, 2015, 20(4): 1540-1593. |

| [16] | Dechow P, Ge W, Schrand C. Understanding earnings quality: A review of the proxies, their determinants and their consequences[J]. Journal of Accounting and Economics, 2010, 50(2-3): 344-401. |

| [17] | 钱苹, 罗玫. 中国上市公司财务造假预测模型[J]. 会计研究, 2015(7): 18-25+96. |

| Qian P, Luo M. Predicting accounting fraud in China[J]. Accounting Research, 2015(7): 18-25+96. | |

| [18] | Dong W, Liao S, Zhang Z. Leveraging financial social media data for corporate fraud detection[J]. Journal of Management Information Systems, 2018, 35(2): 461-487. |

| [19] | Hill T P. A statistical derivation of the significant-digit law[J]. Statistical Science, 1995, 10(4): 354-363. |

| [20] | Michalski T, Stoltz G. Do countries falsify economic data strategically? some evidence that they might[J]. The Review of Economics and Statistics, 2013, 95(2): 591-616. |

| [21] | Nigrini M J, Mittermaier L J. The use of Benford's law as an aid in analytical procedures[J]. Auditing, 1997, 16(2): 52-67. |

| [22] | Zipf B G K. Human Behavior and the principle of least effort: An introduction to human ecology[M]. Mansfield Centre, Conn.: Martino Pub, 2012. |

| [23] | Huang S M, Yen D C, Yang L W, et al. An investigation of Zipf’s law for fraud detection[J]. Decision Support Systems, 2008, 46(1): 70-83. |

| [24] | Iorliam A, Ho A T S, Poh N, et al. Data forensic techniques using Benford’s law and Zipf’s law for keystroke dynamics[C]//Processdings of the 3rd International Workshop on Biometrics and Forensics (IWBF 2015),Gjovik, Norway, March 3-4, IEEE, 2015: 1-6. |

| [25] | Chakravarthy J, DeHaan E, Rajgopal S. Reputation repair after a serious restatement[J]. The Accounting Review, 2014, 89(4): 1329-1363. |

| [26] | 王鲁平, 陈羿. 管理舞弊的形成机理及治理对策研究[J]. 管理工程学报, 2018, 32(1): 107-116. |

| Wang L P, Chen Y. Research of formation mechanism and countermeasure of management fraud[J]. Journal of Industrial Engineering and Engineering Management, 2018, 32(1): 107-116. | |

| [27] | Dyck A, Morse A, Zingales L. How pervasive is corporate fraud?[J]. Review of Accounting Studies, 2024, 29(1): 736-769. |

| [28] | Brazel J F, Jones K L, Zimbelman M F. Using nonfinancial measures to assess fraud risk[J]. Journal of Accounting Research, 2009, 47(5): 1135-1166. |

| [29] | Lin C C, Chiu A A, Huang S Y, et al. Detecting the financial statement fraud: The analysis of the differences between data mining techniques and experts’ judgments[J].Knowledge-Based Systems,2015, 89: 459-470. |

| [30] | 李建平, 孙灏, 常闫芃, 等. 考虑审计要素多重语义关联的财务欺诈识别[J]. 管理科学学报, 2024, 27(3): 58-70. |

| Li J P, Sun H, Chang Y P, et al. Financial statement fraud identification considering the multiple-dimensional semantic associations of auditing elements[J]. Journal of Management Sciences in China, 2024, 27(3): 58-70. | |

| [31] | Goel S, Gangolly J. Beyond the numbers: Mining the annual reports for hidden cues indicative of financial statement fraud[J]. Intelligent Systems in Accounting, Finance and Management, 2012, 19(2): 75-89. |

| [32] | Purda L, Skillicorn D. Accounting variables, deception, and a bag of words: Assessing the tools of fraud detection[J]. Contemporary Accounting Research, 2015, 32(3): 1193-1223. |

| [33] | Hajek P, Henriques R. Mining corporate annual reports for intelligent detection of financial statement fraud–A comparative study of machine learning methods[J]. Knowledge-Based Systems, 2017, 128: 139-152. |

| [34] | Larcker D F, Zakolyukina A A. Detecting deceptive discussions in conference calls[J]. Journal of Accounting Research, 2012, 50(2): 495-540. |

| [35] | Xu X, Xiong F, An Z. Using machine learning to predict corporate fraud: Evidence based on the GONE framework[J]. Journal of Business Ethics, 2023, 186(1): 137-158. |

| [36] | Li J, Li N, Xia T, et al. Textual analysis and detection of financial fraud: Evidence from Chinese manufacturing firms[J]. Economic Modelling, 2023, 126: 106428. |

| [37] | Cecchini M, Aytug H, Koehler G J, et al. Detecting management fraud in public companies[J]. Management Science, 2010, 56(7): 1146-1160. |

| [38] | Bertomeu J, Cheynel E, Floyd E, et al. Using machine learning to detect misstatements[J]. Review of Accounting Studies, 2021, 26(2): 468-519. |

| [39] | 袁先智, 周云鹏, 严诚幸, 等. 财务欺诈风险特征筛选框架的建立和应用[J]. 中国管理科学, 2022, 30(3): 43-54. |

| Yuan X Z, Zhou Y P, Yan C X, et al. The framework for the risk feature extraction method on corporate financial fraud George[J]. Chinese Journal of Management Science, 2022, 30(3): 43-54. | |

| [40] | Achakzai M A K, Peng J. Detecting financial statement fraud using dynamic ensemble machine learning[J]. International Review of Financial Analysis, 2023, 89: 102827. |

| [41] | Hoberg G, Lewis C. Do fraudulent firms produce abnormal disclosure?[J]. Journal of Corporate Finance, 2017, 43: 58-85. |

| [42] | 杨贵军, 孙玲莉, 周亚梦, 等. 基于修正Benford律的财务危机预警Logistic模型及其应用[J]. 数理统计与管理, 2021, 40(4): 585-595. |

| Yang G J, Sun L L, Zhou Y M, et al. Financial early warning logistic model based on corrected benford’s law and its application[J]. Journal of Applied Statistics and Management, 2021, 40(4): 585-595. | |

| [43] | 赵子夜, 杨庆, 杨楠. 言多必失? 管理层报告的样板化及其经济后果[J]. 管理科学学报, 2019, 22(3): 53-70. |

| Zhao Z Y, Yang Q, Yang N. The less said the better? Economic consequences of textual similarity in man-agement discussion and analysis[J]. Journal of Management Sciences in China, 2019, 22(3): 53-70. | |

| [44] | Li F. The information content of forward-looking statements in corporate filings—a Naïve Bayesian machine learning approach[J]. Journal of Accounting Research, 2010, 48(5): 1049-1102. |

| [45] | 薛爽, 肖泽忠, 潘妙丽. 管理层讨论与分析是否提供了有用信息?——基于亏损上市公司的实证探索[J]. 管理世界, 2010, 26(5): 130-140. |

| Xue S, Xiao Z Z, Pan M L. Did the management discussion and analysis provide useful information?-Empirical exploration based on loss-making listed companies[J]. Journal of Management World, 2010, 26(5): 130-140. | |

| [46] | Lo K, Ramos F, Rogo R. Earnings management and annual report readability[J]. Journal of Accounting and Economics, 2017, 63(1): 1-25. |

| [47] | Benford F. The law of anomalous numbers[J]. Proceedings of the American Philosophical Society, 1938, 78(4): 551-572. |

| [48] | Joos M, Zipf G K. The psycho-biology of language[J]. Language, 1936, 12(3): 196-210. |

| [49] | Urzúa C M. A simple and efficient test for Zipf’s law[J]. Economics Letters, 2000, 66(3): 257-260. |

| [50] | Pao M L. Automatic text analysis based on transition phenomena of word occurrences[J]. Journal of the American Society for Information Science, 1978, 29(3): 121-124. |

| [51] | Loughran T, McDonald B. Textual analysis in accounting and finance: A survey[J]. Journal of Accounting Research, 2016, 54(4): 1187-1230. |

| [52] | Loughran T, McDonald B. When is a liability not a liability? textual analysis, dictionaries, and 10-ks[J]. The Journal of Finance, 2011, 66(1): 35-65. |

| [53] | Jiang F, Lee J, Martin X, et al. Manager sentiment and stock returns[J]. Journal of Financial Economics, 2019, 132(1): 126-149. |

| [54] | 郝俊, 李建平, 冯倩倩, 等. 基于溢出效应的金融危机早期预警方法研究[J]. 中国管理科学, 2023, 31(4): 35-45. |

| Hao J, Li J P, Feng Q Q, et al. Early warning of financial crisis based on the spillover effects[J]. Chinese Journal of Management Science, 2023, 31(4): 35-45. | |

| [55] | Lundberg S M, Lee S I. A unified approach to interpreting model predictions[C]//Proceedings of the 31st International Conference on Neural Information Processing Systems,Long Beach, California, USA,December 4-9, ACM, 2017: 4768-4777. |

| [1] | Zhongyi Hu, Diancheng Shui, Jiang Wu. Measurement and Evolution of Digitization Level of Chinese Listed Companies: Empirical Evidence from Annual Report Text [J]. Chinese Journal of Management Science, 2025, 33(4): 36-49. |

| [2] | Gang Li, Chaochao Qiu, Zhipeng Zhang, Simeng Qin, Xingnan Xue. Research on Predicting Corporate Fraud of Listed Companies Based on Multi-Source Text Data and Feature-Augmented Tree Models [J]. Chinese Journal of Management Science, 2025, 33(11): 29-40. |

| [3] | Wanhai You, Senjie Chen, Jianyong Chen, Yinghua Ren. The Impact of “More Words Than Deeds” on Environmental Responsibility on Stock Price Crash Risk: The Mediation Effect of Investor Sentiment [J]. Chinese Journal of Management Science, 2025, 33(10): 12-23. |

| [4] | DONG Bing-jie, CHI Guo-tai. Study on Default Prediction Based on Sentiment Data [J]. Chinese Journal of Management Science, 2023, 31(4): 111-120. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||