主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2026, Vol. 34 ›› Issue (2): 56-66.doi: 10.16381/j.cnki.issn1003-207x.2023.0501

Previous Articles Next Articles

Yong Zhang, Qingmei Huang, Xiaoteng Zheng, Fuding Wang, Xingyu Yang( )

)

Received:2023-03-29

Revised:2024-01-15

Online:2026-02-25

Published:2026-02-04

Contact:

Xingyu Yang

E-mail:yangxy@gdut.edu.cn

CLC Number:

Yong Zhang,Qingmei Huang,Xiaoteng Zheng, et al. Reversal Online Portfolio Strategy with Investors' Attention[J]. Chinese Journal of Management Science, 2026, 34(2): 56-66.

"

"

| 数据集 | 时间区间 | 交易天数 | 数据来源 | 股票数量 |

|---|---|---|---|---|

| Dataset A | 2020.1.2-2023.12.29 | 969 | 医药行业 | 13 |

| Dataset B | 2020.1.2-2023.12.29 | 969 | 中证科创创业50指数 | 10 |

| Dataset C | 2020.1.2-2023.12.29 | 969 | 文化传媒 | 54 |

| Dataset D | 2020.1.2-2023.12.29 | 969 | 计算机设备 | 24 |

| Dataset E | 2011.1.4-2023.12.29 | 3158 | 上证50指数 | 10 |

| Dataset F | 2011.1.4-2023.12.29 | 3158 | 旅游酒店 | 10 |

"

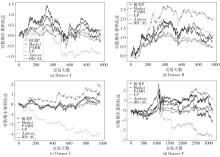

| 策略 | BCRP | Market | PAMR | OLMAR | EG | UP | Anticor | BD-AC |

|---|---|---|---|---|---|---|---|---|

| Dataset A | 1.32 | 0.78 | 0.42 | 0.92 | 0.91 | 0.92 | 0.81 | 1.10 |

| Dataset B | 7.84 | 1.75 | 3.89 | 1.63 | 1.63 | 1.63 | 2.40 | 3.00 |

| Dataset C | 6.23 | 1.04 | 0.05 | 1.20 | 1.19 | 1.20 | 1.36 | 2.58 |

| Dataset D | 2.63 | 0.98 | 0.32 | 1.24 | 1.22 | 1.24 | 1.37 | 1.36 |

| Dataset E | 9.30 | 1.84 | 0.37 | 1.77 | 1.76 | 1.78 | 1.11 | 2.57 |

| Dataset F | 3.12 | 0.81 | 0.06 | 1.16 | 1.14 | 1.16 | 0.32 | 1.04 |

"

"

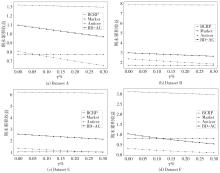

| 数据集 | 指标 | BCRP | Market | PAMR | OLMAR | EG | UP | Anticor | BD-AC |

|---|---|---|---|---|---|---|---|---|---|

| Dataset A | APY | 0.0710 | -0.0615 | -0.1961 | -0.0218 | -0.0238 | -0.0225 | -0.0514 | 0.0230 |

| IR | 0.0376 | — | -0.0176 | 0.0502 | 0.0500 | 0.0492 | 0.0259 | 0.0370 | |

| SR | 0.0249 | -0.3344 | -0.0153 | 0.0039 | 0.0035 | -0.2191 | 0.0147 | -0.0265 | |

| MDD | 0.4291 | 0.5805 | 0.7758 | 0.5059 | 0.5071 | 0.5069 | 0.7933 | 0.8206 | |

| CR | 0.1655 | -0.1059 | -0.2528 | -0.0430 | -0.0469 | -0.0444 | -0.0648 | 0.0280 | |

| Dataset B | APY | 0.6734 | 0.1494 | 0.4041 | 0.1300 | 0.1300 | 0.1306 | 0.2443 | 0.3165 |

| IR | 0.0862 | — | 0.0405 | -0.0165 | -0.0169 | -0.0163 | 0.0332 | 0.0383 | |

| SR | 0.0722 | 0.2936 | 0.0632 | 0.0357 | 0.0356 | 0.2937 | 0.0425 | 0.3757 | |

| MDD | 0.6662 | 0.5573 | 0.6102 | 0.5232 | 0.5254 | 0.5227 | 0.7083 | 0.7397 | |

| CR | 1.0109 | 0.2680 | 0.6622 | 0.2484 | 0.2475 | 0.5227 | 0.3449 | 0.4279 | |

| Dataset C | APY | 0.5796 | 0.0106 | -0.5371 | 0.0467 | 0.0449 | 0.0469 | 0.0802 | 0.2679 |

| IR | 0.0774 | — | -0.1080 | 0.0447 | 0.0441 | 0.0449 | 0.0348 | 0.0566 | |

| SR | 0.0653 | -0.0975 | -0.0770 | 0.0195 | 0.0191 | 0.0243 | 0.0283 | 0.0441 | |

| MDD | 0.5833 | 0.4208 | 0.9680 | 0.3623 | 0.3652 | 0.3618 | 0.6368 | 0.6833 | |

| CR | 0.9937 | 0.0253 | -0.5549 | 0.1288 | 0.1231 | 0.1297 | 0.1260 | 0.3920 | |

| Dataset D | APY | 0.2733 | -0.0060 | -0.2507 | 0.0544 | 0.0513 | 0.0563 | 0.0814 | 0.0804 |

| IR | 0.0568 | — | -0.0285 | 0.1088 | 0.1077 | 0.1124 | 0.0362 | 0.0354 | |

| SR | 0.0458 | -0.1575 | -0.0184 | 0.0212 | 0.0205 | 0.0564 | 0.0285 | 0.0282 | |

| MDD | 0.5993 | 0.4790 | 0.8361 | 0.4161 | 0.4196 | 0.4135 | 0.7093 | 0.6302 | |

| CR | 0.4560 | -0.0125 | -0.2999 | 0.1307 | 0.1222 | 0.1361 | 0.1148 | 0.1275 | |

| Dataset E | APY | 0.1872 | 0.0478 | -0.0739 | 0.0449 | 0.0447 | 0.0445 | 0.0079 | 0.0753 |

| IR | 0.0383 | — | -0.0255 | -0.0054 | -0.0057 | -0.0057 | 0.0107 | 0.0237 | |

| SR | 0.0458 | 0.0314 | -0.0042 | 0.0197 | 0.0196 | 0.0194 | 0.0168 | 0.0253 | |

| MDD | 0.5479 | 0.5269 | 0.7890 | 0.4948 | 0.4958 | 0.4954 | 0.7776 | 0.7705 | |

| CR | 0.3416 | 0.0907 | -0.0936 | 0.0908 | 0.0901 | 0.0899 | 0.0102 | 0.0977 | |

| Dataset F | APY | 0.0915 | -0.0158 | -0.1897 | 0.0116 | 0.0104 | 0.0117 | -0.0831 | 0.0030 |

| IR | 0.0461 | — | -0.0253 | 0.0122 | 0.0120 | 0.0123 | 0.0192 | 0.0262 | |

| SR | 0.0277 | -0.1907 | -0.0155 | 0.0115 | 0.0112 | -0.1019 | 0.0161 | 0.0208 | |

| MDD | 0.6783 | 0.5794 | 0.9527 | 0.5575 | 0.5576 | 0.5582 | 0.9808 | 0.8732 | |

| CR | 0.1349 | -0.0272 | -0.1991 | 0.0208 | 0.0187 | 0.0210 | -0.0847 | 0.0034 |

"

"

| t检验 | 样本数 | BD-AC策略平均收益 | Market策略平均收益 | 胜率/% | t检验量 | p值 | ||

|---|---|---|---|---|---|---|---|---|

| Dataset A | 969 | 0.0007 | -0.0003 | 46.52 | 0.0013 | 1.7668 | 1.7762 | 0.0760 |

| Dataset B | 969 | 0.0020 | 0.0006 | 48.71 | 0.0025 | 2.5214 | 2.1453 | 0.0322 |

| Dataset C | 969 | 0.0017 | -0.0000 | 48.92 | 0.0018 | 1.9105 | 2.2821 | 0.0227 |

| Dataset D | 969 | 0.0009 | -0.0000 | 48.09 | 0.0014 | 1.8053 | 1.6777 | 0.0937 |

| Dataset E | 3158 | 0.0005 | 0.0001 | 48.23 | 0.0009 | 2.0257 | 2.5243 | 0.0116 |

| Dataset F | 3158 | 0.0005 | -0.0001 | 50.51 | 0.0008 | 1.7436 | 1.9236 | 0.0545 |

"

| [1] | Markowitz H. Portfolio selection[J]. The Journal of Finance, 1952, 7(1): 77-91. |

| [2] | Cover T M. Universal portfolios[J]. Mathematical Finance, 1991, 1(1): 1-29. |

| [3] | Borodin A, El-Yaniv R, Gogan V. Can we learn to beat the best stock[J]. Journal of Artificial Intelligence Research, 2004, 21: 579-594. |

| [4] | Crammer K, Dekel O, Keshet J, et al. Online passive-aggressive algorithms[J]. Journal of Machine Learning Research, 2006, 7: 551-585. |

| [5] | Li B, Zhao P, Hoi S C H, et al. PAMR: Passive aggressive mean reversion strategy for portfolio selection[J]. Machine Learning, 2012, 87(2): 221-258. |

| [6] | Li B, Hoi S C H, Zhao P, et al. Confidence weighted mean reversion strategy for online portfolio selection[J]. ACM Transactions on Knowledge Discovery from Data, 2013, 7(1): 1-38. |

| [7] | Li B, Hoi S C H, Sahoo D, et al. Moving average reversion strategy for on-line portfolio selection[J]. Artificial Intelligence, 2015, 222: 104-123. |

| [8] | Li B, Hoi S C H. Online portfolio selection: A survey[J]. ACM Computing Surveys, 2014, 46(3): 1-36. |

| [9] | Huang D, Zhou J, Li B, et al. Robust Median reversion strategy for online portfolio selection[J]. IEEE Transactions on Knowledge and Data Engineering, 2016, 28(9): 2480-2493. |

| [10] | Yang X Y, Li H, Zhang Y, et al. Reversion strategy for online portfolio selection with transaction costs[J]. International Journal of Applied Decision Sciences, 2018, 11(1): 79-99. |

| [11] | Cai X, Ye Z. Gaussian weighting reversion strategy for accurate online portfolio selection[J]. IEEE Transactions on Signal Processing, 2019, 67(21): 5558-5570. |

| [12] | Peng Z, Xu W, Li H. A novel online portfolio selection strategy with multiperiodical asymmetric mean reversion[J]. Discrete Dynamics in Nature and Society, 2020, 2020(1): 5956146. |

| [13] | Moon S H, Yoon Y. Genetic mean reversion strategy for online portfolio selection with transaction costs[J]. Mathematics, 2022, 10(7): 1073-1092. |

| [14] | Guo S, Gu J W, Fok C H, et al. Online portfolio selection with state-dependent price estimators and transaction costs[J]. European Journal of Operational Research, 2023, 311(1): 333-353. |

| [15] | He H, Li H. A new boosting algorithm for online portfolio selection based on dynamic time warping and anti-correlation[J]. Computational Economics, 2024, 63(5): 1777-1803. |

| [16] | 曹敏, 吴冲锋. 中国证券市场反向策略研究及其短周期性[J]. 系统工程理论与实践, 2004, 24(1): 30-34. |

| Cao M, Wu C F. Tests of the contrarian strategy evidence from the Chinese stock market[J]. Systems Engineering——Theory & Practice, 2004, 24(1): 30-34. | |

| [17] | 鲁臻, 邹恒甫. 中国股市的惯性与反转效应研究[J]. 经济研究, 2007, 42(9): 145-155. |

| Lu Z, Zou H F. Momentum and reversal in China stock market[J]. Economic Research Journal, 2007, 42(9): 145-155. | |

| [18] | 游家兴. 谁反应过度,谁反应不足——投资者异质性与收益时间可预测性分析[J]. 金融研究, 2008(4): 161-173. |

| You J X. Who overreacts and who underreacts? analysis on the relationship between the investor’s heterogeneity and return time-series predictability[J]. Journal of Financial Research, 2008(4): 161-173. | |

| [19] | 何诚颖, 陈锐, 蓝海平, 等. 投资者非持续性过度自信与股市反转效应[J]. 管理世界, 2014(8): 44-54. |

| He C Y, Chen R, Lan H P, et al. Investors’ unsustainable overconfidence and stock market reversal effect[J]. Journal of Management World, 2014(8): 44-54. | |

| [20] | Da Z, Engelberg J, Gao P. The sum of all FEARS investor sentiment and asset prices[J]. The Review of Financial Studies, 2015, 28(1): 1-32. |

| [21] | Guzmán G. Internet search behavior as an economic forecasting tool: The case of inflation expectations[J]. Journal of Economic and Social Measurement, 2011, 36(3): 119-167. |

| [22] | Wang J, Li M, Wang X, et al. Impact of investor attention on mutual funds[J]. Journal of Neuroscience, Psychology, and Economics, 2021, 14(1): 1-19. |

| [23] | 瞿慧, 沈微. 引入投资者关注的中国股市协方差预测——基于多元HAR类模型[J]. 中国管理科学, 2022, 30(7): 9-19. |

| Qu H, Shen W. Investor attention and covariance forecasting in China’s stock markets—a study based on the MHAR type models[J]. Chinese Journal of Management Science, 2022, 30(7): 9-19. | |

| [24] | 林娟娟, 唐勇, 周小亮, 等. 北上资金、百度指数与股市关联性的时频域研究——基于协高阶矩视角[J]. 中国管理科学, 2022, 30(1): 20-31. |

| Lin J J, Tang Y, Zhou X L, et al. Research on the relationship between northward capital, about: Blank index and stock market in time and frequency domain-based on the perspective of higher order co-moments[J]. Chinese Journal of Management Science, 2022, 30(1): 20-31. | |

| [25] | 俞庆进, 张兵. 投资者有限关注与股票收益——以百度指数作为关注度的一项实证研究[J]. 金融研究, 2012(8): 152-165. |

| Yu Q J, Zhang B. Limited attention and stock performance: An empirical study using Baidu index as the proxy for investor attention[J]. Journal of Financial Research, 2012(8): 152-165. | |

| [26] | 陈植元, 米雁翔, 厉洋军, 等. 基于百度指数的投资者关注度与股票市场表现的实证分析[J]. 统计与决策, 2016, 32(23): 155-157. |

| Chen Z Y, Mi Y X, Li Y J, et al. Empirical analysis of investor attention and stock market performance based on Baidu index[J]. Statistics & Decision, 2016, 32(23): 155-157. | |

| [27] | 杨涛, 郭萌萌. 投资者关注度与股票市场——以PM2.5概念股为例[J]. 金融研究, 2019(5): 190-206. |

| Yang T, Guo M M. Investor attention and the stock market: A new perspective on PM2.5 concept stocks[J]. Journal of Financial Research, 2019(5): 190-206. | |

| [28] | 张学勇, 唐国梅. 行业关注度与股票横截面收益率——基于百度行业搜索指数的研究[J]. 经济学(季刊), 2022, 22(3): 773-794. |

| Zhang X Y, Tang G M. Industry-wide attention based on Internet searches and the cross-section of stock returns[J]. China Economic Quarterly, 2022, 22(3): 773-794. | |

| [29] | 樊晓倩, 苑莹. 投资者本地异常关注能预测股票市场吗?[J]. 管理评论, 2021, 33(10): 70-80. |

| Fan X Q, Yuan Y. Can abnormal local investor attention be used to predict stock market?[J]. Management Review, 2021, 33(10): 70-80. | |

| [30] | 张同辉, 苑莹, 曾文. 投资者关注能提高市场波动率预测精度吗?——基于中国股票市场高频数据的实证研究[J]. 中国管理科学, 2020, 28(11): 192-205. |

| Zhang T H, Yuan Y, Zeng W. Can investor attention help to predict stock market volatility? An empirical research based on Chinese stock market high-frequency data[J]. Chinese Journal of Management Science, 2020, 28(11): 192-205. | |

| [31] | Blum A, Kalai A. Universal portfolios with and without transaction costs[J]. Machine Learning, 1999, 35(3): 193-205. |

| [32] | Gao L, Zhang W. Weighted moving average passive aggressive algorithm for online portfolio selection[C]//Proceeding of 2013 5th International Conference on Intelligent Human-Machine Systems and Cybernetics, Hangzhou, China, August 26-27, 2013, IEEE, 2013: 327-330. |

| [33] | Helmbold D P, Schapire R E, Singer Y, et al. On-line portfolio selection using multiplicative updates[J]. Mathematical Finance, 1998, 8(4): 325-347. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||