主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2026, Vol. 34 ›› Issue (4): 47-62.doi: 10.16381/j.cnki.issn1003-207x.2024.0896cstr: 32146.14.j.cnki.issn1003-207x.2024.0896

王泽舟1, 许启发1,2( ), 蒋翠侠1

), 蒋翠侠1

收稿日期:2024-06-04

修回日期:2024-10-19

出版日期:2026-04-25

发布日期:2026-03-27

通讯作者:

许启发

E-mail:xuqifa1975@163.com

基金资助:

Zezhou Wang1, Qifa Xu1,2(), Cuixia Jiang1

Received:2024-06-04

Revised:2024-10-19

Online:2026-04-25

Published:2026-03-27

Contact:

Qifa Xu

E-mail:xuqifa1975@163.com

摘要:

本文建立上市公司间供应链、股权和行业网络,融合低频公司特征和宏观经济信息以及高频市场、交易和情绪信息等作为网络节点特征,构建混频跨期注意力多层图卷积(MF-IAMGCN)模型,检验混频(MF)定价信息在上市公司多层关系网络中的同期交互和跨期传播对资产价格的预测能力。空间维度上,MF-IAMGCN模型基于注意力多层图卷积网络框架,引入混频数据抽样方法,刻画混频定价信息在多层网络中的同期交互,包括节点间的高阶依赖和非线性关系;时间维度上,借助门控机制,刻画连续时间步骤中节点之间的跨期信息传播和层间交互。选取2003年1月—2022年12月期间中国A股市场为研究样本,从个股定价、测试资产定价和投资组合绩效三个方面,实证检验模型性能。研究结果表明:(1)MF-IAMGCN模型在个股和测试资产层面的定价表现均优于四个竞争性模型,具备较强的综合定价性能。(2)MF-IAMGCN模型构造的投资组合取得了最优的风险调整绩效,兼顾高回报和低波动。(3)MF-IAMGCN模型刻画定价信息的动态传播模式,充分挖掘高频定价信号,显著提升了定价性能。(4)股权网络隐含金融市场资本活动信息,能够显著降低ST股票预测误差。

中图分类号:

王泽舟,许启发,蒋翠侠. 上市公司多层关系网络中混频信息交互与传播能够提升资产定价性能吗?——基于图神经网络的资产定价研究[J]. 中国管理科学, 2026, 34(4): 47-62.

Zezhou Wang,Qifa Xu,Cuixia Jiang. Can Interaction and Dissemination of Mixed-Frequency Information in Companies' Multi-Layer Relationship Networks Improve Asset Pricing? Asset Pricing Study Based on Graph Neural Networks[J]. Chinese Journal of Management Science, 2026, 34(4): 47-62.

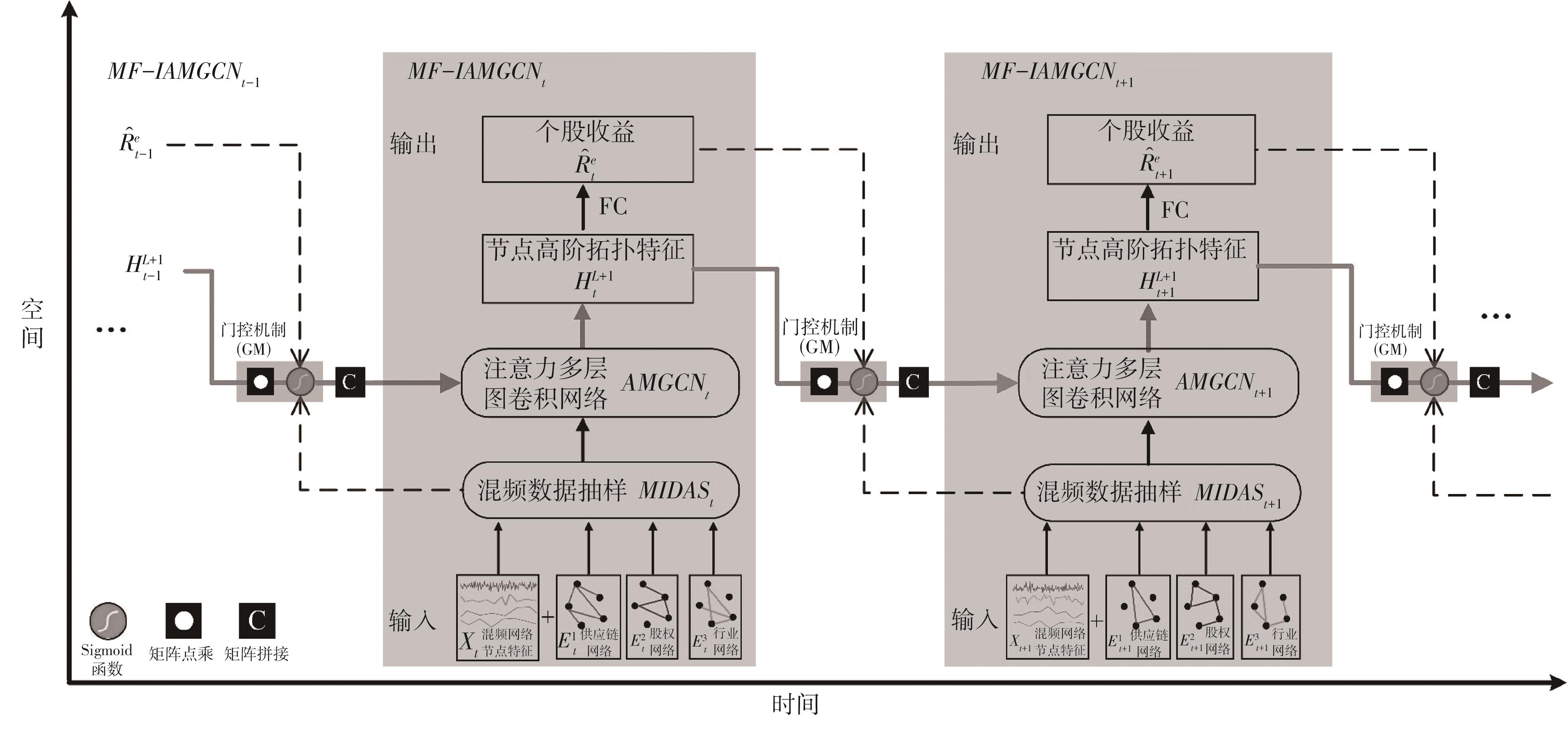

图1

MF-IAMGCN模型整体架构"

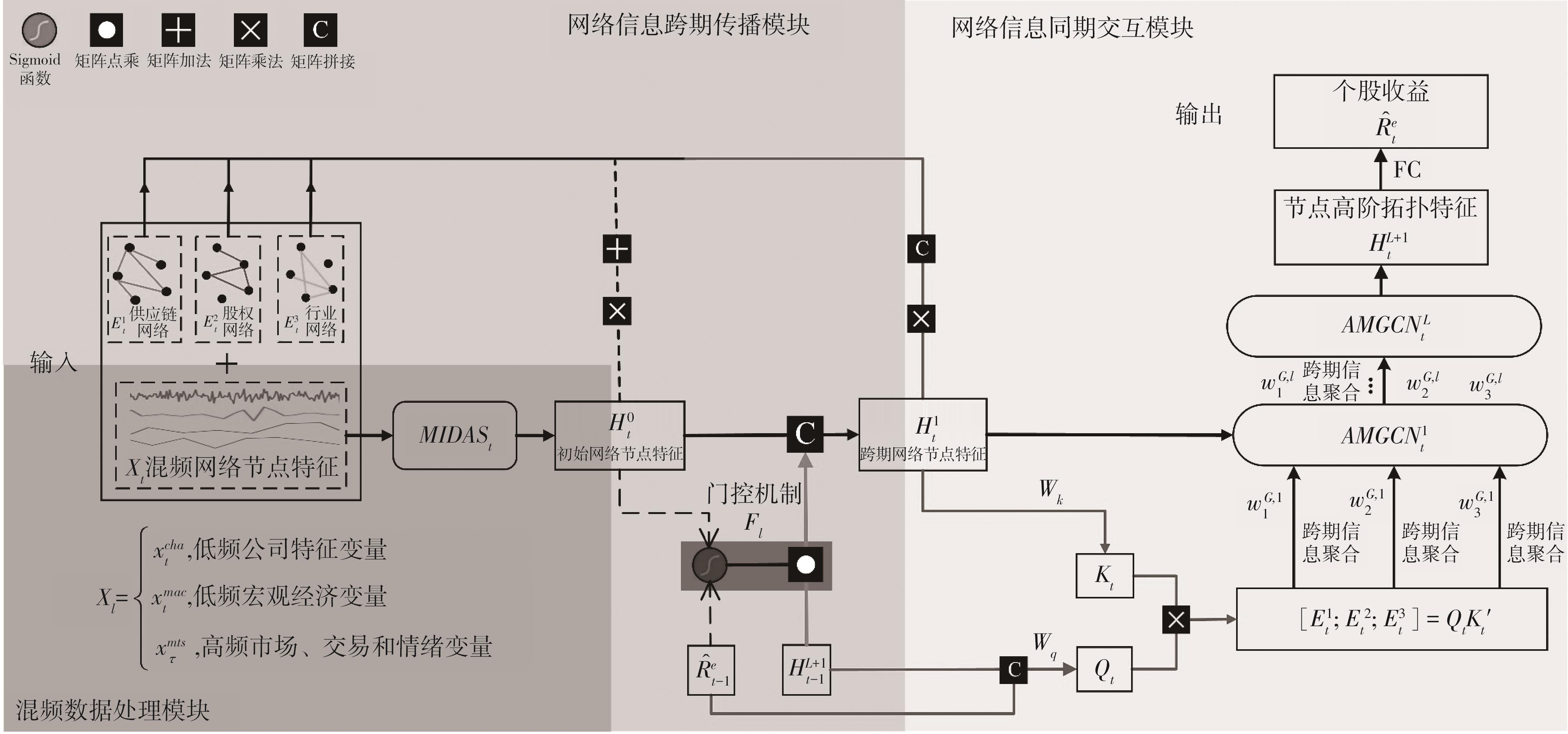

图2

MF-IAMGCN模型模块化展开"

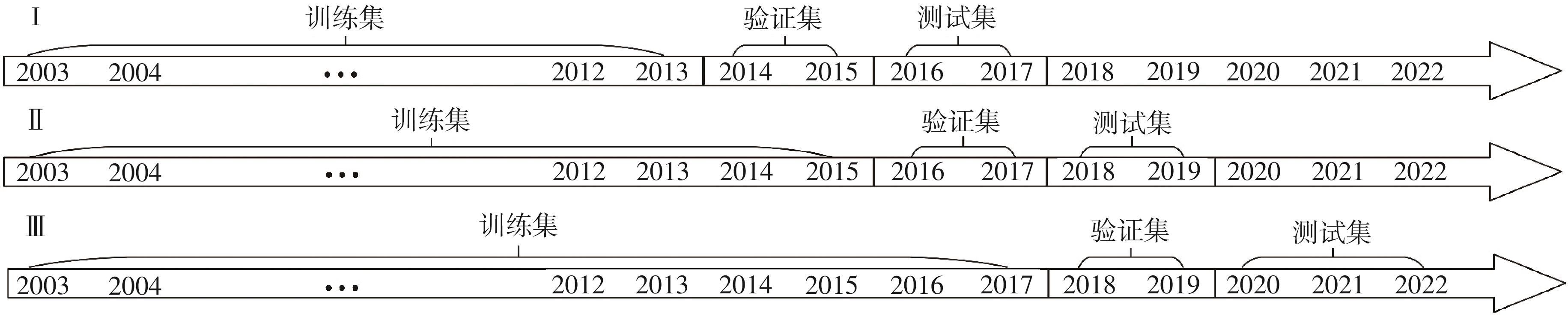

图3

扩展窗口预测"

表1

低频公司特征变量和低频宏观经济变量"

| 变量名称 | 构建方法 | 频率 | 变量名称 | 构建方法 | 频率 | 变量名称 | 构建方法 | 频率 |

|---|---|---|---|---|---|---|---|---|

| acc(应计) | 收入减经营现金除以资产 | 半年 | gma(毛利润) | 收入减去销售成本除以总资产 | 季 | roeq(净资产收益率) | 净利润除以股东权益平均余额 | 季 |

| agr(资产增长) | 总资产的年度变化率 | 年 | grCAPX(资本支出变化率) | 资本支出的年度变化率 | 年 | roic(投入资本回报率) | 税后净营业利润除以总投资额 | 季 |

| bm(账面市值比) | 账面价值除以市值 | 季 | hire(员工数目变化率) | 员工数目的年度变化率 | 年 | rsup(营业收入变化率市值比) | 营业收入的季度变化率除以总市值 | 季 |

| bm_ia(行业调整bm) | 个股账面市值比 减行业平均账面市值比 | 季 | invest(资本支出和存货) | 固定资产年变化率除以总资产 | 年 | tang(债务能力) | 现金及等价物加0.715倍应收账款加0.547 倍存货加0.535倍固定资产除以总资产 | 季 |

| cash(现金持有量) | 现金及等价物除以总资产 | 季 | lev(杠杆率) | 总负债除以市值 | 季 | sp(营业收入市值比) | 营业收入除以总市值 | 季 |

| cashdebt(现金债务比) | 现金及等价物除以总负债 | 季 | lgr(总负债变化率) | 总负债的季度变化率 | 季 | sgr(营业收入变化率) | 营业收入的季度变化率 | 季 |

| cfp(现金流价格比) | 经营现金流除以市值 | 季 | mve(规模) | 总市值的自然对数 | 季 | tb(税费收入比) | 4倍应交税费除以总收入 | 季 |

| maxret(最大日收益) | 过去一个月最大日收益 | 月 | mve_ia(行业调整规模) | 个股对数市值减行业平均市值 | 季 | zerotrade(零交易日) | 上月期交易量为0天数 | 月 |

| mom1 m(一个月动量) | 过去一个月累计收益 | 月 | operprof(经营获利能力) | 营业利润除以股东权益 | 季 | top1(最大股东持股) | 第1大股东占股比列 | 年 |

| mom6 m(6个月动量) | t-6月至t-1月的累积收益 | 月 | orgcap(组织资本) | 管理费用除以净资产总额 | 季 | top10(前10大股东持股) | 前10大股东占股比列 | 年 |

| chmom(6个月惯性) | t-6月至t-1月累积回报减 t-12至t-7的累计回报 | 月 | pchcurrat(流动比率变化率) | 流动比率的季度变化率 | 季 | Ownership(所有权) | 公司所有权性质(国企、私企、外资和其他) | 年 |

| mom12 m(12个月动量) | t-12到t-1月的累积收益 | 月 | pchquick(速动比率变化率) | 速动比率的季度变化率 | 季 | dp(股息价格比) | A股平均股利与平均股价对数之商 | 月 |

| mom36 m(36个月动量) | t-36至t-13月的累积收益 | 月 | pctacc(应计百分比) | 应计项目除以净利润 | 半年 | de(派息率) | A股平均股利与平均收益对数之商 | 月 |

| chpm(营业利润变化) | 营业利润除以收入变化率 | 季 | quick(速动比率) | 流动资产减存货除以流动负债 | 季 | svar(指数波动率) | 上证综合指数收益的平方 | 月 |

| chpm_ia(行业调整chpm) | 行业调整营业利润变化 | 季 | rd(研发费用占比) | 若研发费用占资产总额比例 | 季 | M_ntis(股本扩张) | 中国A股市场的净发行量除以A股总市值 | 月 |

| cinvest(公司投资) | 固定资产除以营业收入 | 季 | rd_mve(研发费用市值比) | 研发费用除以总市值 | 季 | infl(通货膨胀率) | 居民消费价格指数增长率 | 月 |

| currat(流动比率) | 流动资产除以流动负债 | 季 | rd_sale(研发费用营业收入比) | 研发费用除以营业收入 | 季 | m2gr(M2增长率) | 广义货币供应量增长率 | 月 |

| dy(本利比) | 年末总股息除以市值。 | 季 | realestate(房地产投资占比) | 房地产投资除以固定资产总额 | 季 | itgr(国际贸易额增长率) | 进出口总额增长率 | 月 |

| egr(权益增长率) | 账面价值季度变化率 | 季 | roaq(总资产收益率) | 净利润除以平均资产总额 | 季 | PPI(生产价格指数) | 工业生产者出厂价格增长率 | 月 |

表2

高频市场、交易和情绪变量"

| 变量名称 | 构建方法 | 频率 | 变量名称 | 构建方法 | 频率 | 变量名称 | 构建方法 | 频率 |

|---|---|---|---|---|---|---|---|---|

| beta(beta值) | CAPM模型回归系数 | 日 | BullishSent(看涨情绪指数) | 东方财富论坛个股看涨情绪指数 | 日 | oil(油价) | 西德克萨斯中质原油价格 | 日 |

| dolvol(对数交易额) | 交易额的自然对数 | 日 | PositiveSent(积极情绪指数) | 东方财富论坛个股积极情绪指数 | 日 | exchange(汇率) | 人民币元对美元汇率 | 日 |

| ill(Amihud流动性指标) | Amihud流动性指标 | 日 | news_senti(媒体情绪指数) | 个股新闻媒体情绪指数 | 日 | goldprice(金价) | 伦敦黄金市场价格 | 日 |

| volatility(收益波动率) | 收益率标准差 | 日 | searchindex(网络搜索指数) | 个股网络搜索指数 | 日 | shibor(上海银行间同业拆借利率) | 上海银行间同业拆借利率 | 日 |

| turnover(换手率) | 成交金额除以流通股数 | 日 | voldolvol(对数交易额波动率) | 对数交易额的标准差 | 周 | VIX(恐慌指数) | 芝加哥期权交易所波动率指数 | 日 |

| atr(异常换手率) | 个股换手率减市场换手率 | 日 | volturnover(换手率波动率) | 换手率的标准差 | 周 | ucirs(中美利差) | Shibor与美国联邦基金利率之差 | 日 |

| risk_factor(风险因子) | CAPM模型风险因子 | 日 | volill(ill波动率) | Amihud流动性指标的标准差 | 周 | Mturnover(市场换手率) | A股流通市值加权换手率 | 日 |

| ertrend(趋势因子) | 市场趋势因子 | 日 | volliquid(liquid波动率) | 流动性指标的标准差 | 周 | Mtrade_volume(市场交易量) | A股按流通市值加权交易量 | 日 |

| liquid(流动性) | 收益率除以成交金额 | 日 | volPB(PB波动率) | 市净率的标准差 | 周 | M_BullishSent(市场看涨情绪指数) | 东方财富论坛市场看涨情绪指数 | 日 |

| trade_volume(总交易金额) | 总交易金额 | 日 | volPE(PE波动率) | 市盈率的标准差 | 周 | M_PositiveSent(市场积极情绪指数) | 东方财富论坛市场积极情绪指数 | 日 |

| trade_number(总交易量) | 交易金额除以成交量 | 日 | voltrade_number(交易量波动) | 交易量的标准差 | 周 | M_news_senti(市场媒体情绪指数) | 市场新闻媒体情绪指数 | 日 |

| deltatrade_voulme(滞后交易量) | 总交易量的一阶滞后 | 日 | voltrade_volume(交易额波动) | 交易额的标准差 | 周 | M_searchindex(市场搜索指数) | 市场网络搜索指数 | 日 |

| PB(市净率) | 总市值除以净资产 | 日 | tms(利差) | 10年期国债利率减1年期国债利率 | 日 | SMB(市值因子) | 小盘组合和大盘组合收益率之差 | 日 |

| PE(市盈率) | 总市值除以归属母公司的净利润之和 | 日 | CMA(投资模式因子) | 低投资比例股票组合和高投资比例股票组合收益率差 | 日 | HML(账面市值比因子) | 高账面市值比股票组合和低账面市值比股票组合收益率差 | 日 |

| corrlation(相关系数) | 个股风险收益率与市场风险收益率的相关系数 | 日 | RMW(盈利能力因子) | 高盈利股票组合和 低盈利股票组合的收益率之差。 | 日 | ep(市场市盈率) | A股市场平均每股收益与平均股价对数商 | 日 |

表3

模型功能结构"

| 模型 | 混频数据处理 | 多层关系网络 | 网络信息同期交互 | 网络信息跨期传播 | 注意力机制 |

|---|---|---|---|---|---|

| MF-IAMGCN | √ | √ | √ | √ | √ |

| IAMGCN | × | √ | √ | √ | √ |

| MF-AMGCN | √ | √ | √ | × | √ |

| MGCN | × | √ | √ | × | × |

| LSTM | × | × | × | × | × |

表4

模型个股层面样本外αI和EV"

| 模型 | EV | |

|---|---|---|

| MF-IAMGCN | 0.0446 | 0.6664 |

| IAMGCN | 0.0522 | 0.6044 |

| MF-AMGCN | 0.0497 | 0.6131 |

| MGCN | 0.0558 | 0.5724 |

| LSTM | 0.0583 | 0.5204 |

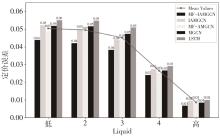

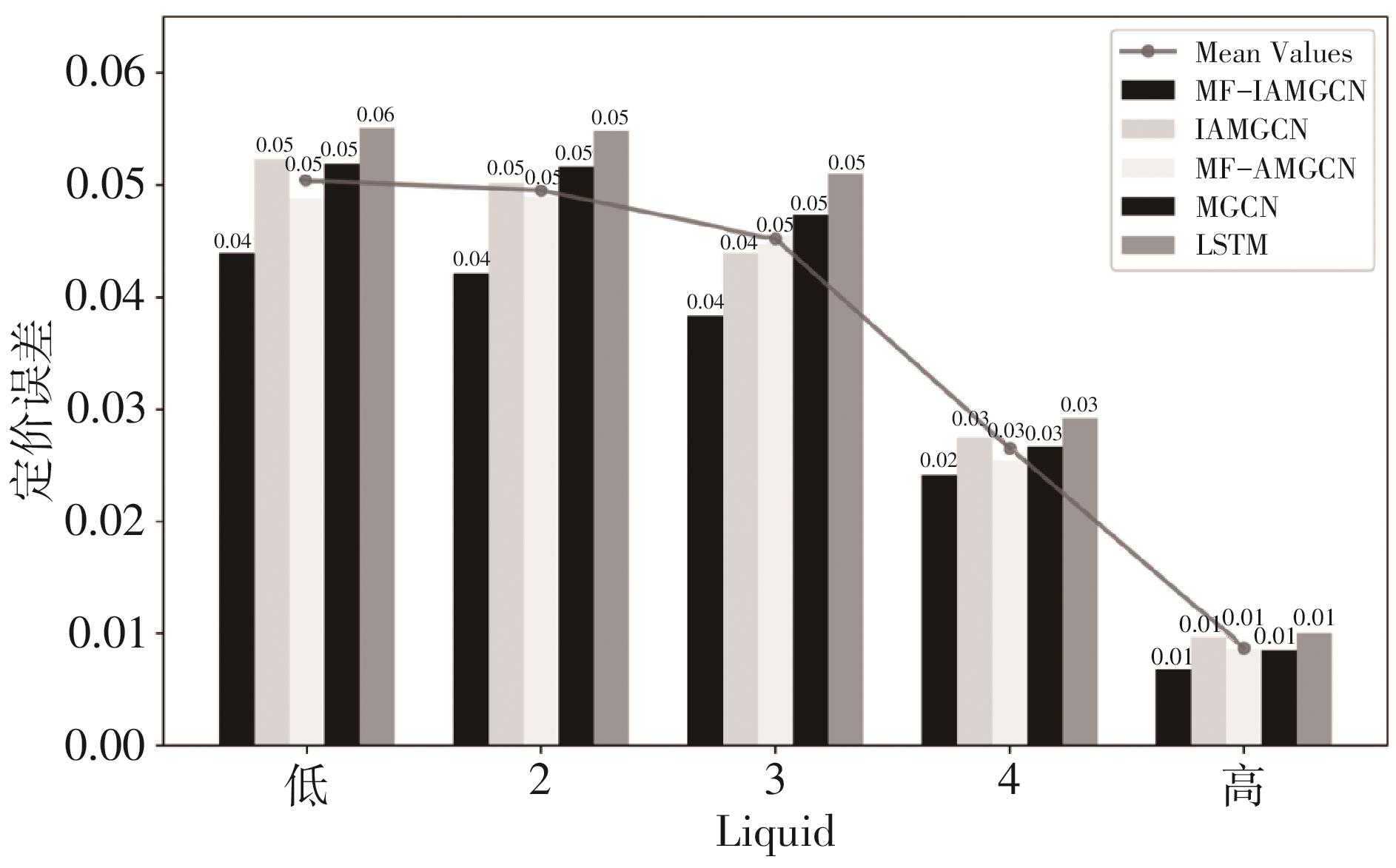

图4

Liquid单特征排序组合样本外αP"

表5

模型单特征排序组合样本外平均αP和GF"

| 模型 | GF | |

|---|---|---|

| MF-IAMGCN | 0.0305 | 0.9563 |

| IAMGCN | 0.0366 | 0.8527 |

| MF-AMGCN | 0.0349 | 0.9237 |

| MGCN | 0.0389 | 0.7584 |

| LSTM | 0.0400 | 0.6743 |

表6

模型投资组合样本外月度绩效"

| 模型 | SR | AR | MaxLoss | MD |

|---|---|---|---|---|

| MF-IAMGCN | 0.5740 | 0.0730 | 0.1555 | 0.1166 |

| IAMGCN | 0.5237 | 0.0640 | 0.2086 | 0.1221 |

| MF-AMGCN | 0.5191 | 0.0660 | 0.2268 | 0.2853 |

| MGCN | 0.4036 | 0.0564 | 0.2111 | 0.1449 |

| LSTM | 0.4276 | 0.0491 | 0.2129 | 0.0844 |

表7

模型单特征排序组合样本外GF"

| 特征 | MF- IAMGCN | IAM-GCN | MF-AMGCN | MGCN | LSTM | 特征 | MF-IAMGCN | IAM-GCN | MF-AMGCN | MGCN | LSTM |

|---|---|---|---|---|---|---|---|---|---|---|---|

| acc | 0.9621 | 0.8679 | 0.9326 | 0.7610 | 0.6774 | quick | 0.9337 | 0.8455 | 0.9356 | 0.7549 | 0.6727 |

| agr | 0.9667 | 0.8663 | 0.9317 | 0.7576 | 0.6750 | rd | 0.9558 | 0.8351 | 0.9182 | 0.7542 | 0.6678 |

| bm | 0.9519 | 0.8667 | 0.9199 | 0.7652 | 0.6844 | rd_sale | 0.9539 | 0.8405 | 0.9211 | 0.7516 | 0.6665 |

| bm_ia | 0.9420 | 0.8266 | 0.9084 | 0.7423 | 0.6570 | realestate | 0.9600 | 0.8616 | 0.9317 | 0.7629 | 0.6795 |

| cash | 0.9579 | 0.8547 | 0.9273 | 0.7587 | 0.6734 | roaq | 0.9648 | 0.8676 | 0.9321 | 0.7666 | 0.6809 |

| cashdebt | 0.9629 | 0.8598 | 0.9279 | 0.7601 | 0.6726 | roeq | 0.9621 | 0.8676 | 0.9284 | 0.7635 | 0.6778 |

| cfp | 0.9501 | 0.8095 | 0.9010 | 0.7418 | 0.6597 | roic | 0.9534 | 0.8571 | 0.9238 | 0.7513 | 0.6692 |

| chmom | 0.9546 | 0.8215 | 0.9076 | 0.7473 | 0.6620 | rsup | 0.9549 | 0.8452 | 0.9110 | 0.7541 | 0.6690 |

| chpm | 0.9521 | 0.8494 | 0.9241 | 0.7532 | 0.6685 | sgr | 0.9370 | 0.8306 | 0.9466 | 0.7489 | 0.6595 |

| chpm_ia | 0.9491 | 0.8375 | 0.9201 | 0.7502 | 0.6667 | sp | 0.9647 | 0.8753 | 0.9259 | 0.7562 | 0.6760 |

| cinvest | 0.9623 | 0.8554 | 0.9227 | 0.7507 | 0.6646 | tang | 0.9659 | 0.8668 | 0.9332 | 0.7666 | 0.6885 |

| currat | 0.9534 | 0.8477 | 0.9268 | 0.7566 | 0.6738 | tb | 0.9611 | 0.8609 | 0.9229 | 0.7559 | 0.6732 |

| dy | 0.9489 | 0.8468 | 0.9247 | 0.7515 | 0.6676 | zerotrade | 0.9605 | 0.8654 | 0.9281 | 0.7758 | 0.6916 |

| egr | 0.9605 | 0.8625 | 0.9268 | 0.7537 | 0.6690 | top1 | 0.9606 | 0.8667 | 0.9266 | 0.7597 | 0.6792 |

| gma | 0.9601 | 0.8650 | 0.9288 | 0.7570 | 0.6700 | top10 | 0.9619 | 0.9147 | 0.9284 | 0.7598 | 0.6765 |

| grCAPX | 0.9386 | 0.8646 | 0.9408 | 0.7685 | 0.6838 | beta | 0.9573 | 0.8271 | 0.9273 | 0.7567 | 0.6653 |

| hire | 0.9604 | 0.8679 | 0.9314 | 0.7660 | 0.6818 | ill | 0.9576 | 0.8727 | 0.9293 | 0.7887 | 0.7066 |

| invest | 0.9595 | 0.8648 | 0.9254 | 0.7625 | 0.6776 | volatility | 0.9557 | 0.8592 | 0.9301 | 0.7649 | 0.6786 |

| lev | 0.9509 | 0.8673 | 0.9204 | 0.7650 | 0.6869 | turnover | 0.9652 | 0.8726 | 0.9359 | 0.7884 | 0.7006 |

| lgr | 0.9708 | 0.8698 | 0.9346 | 0.7605 | 0.6748 | atr | 0.9513 | 0.8580 | 0.9230 | 0.7585 | 0.6737 |

| maxret | 0.9667 | 0.8629 | 0.9312 | 0.7727 | 0.6900 | ertrend | 0.9647 | 0.8367 | 0.9064 | 0.7542 | 0.6702 |

| mom1m | 0.9481 | 0.8320 | 0.9077 | 0.7247 | 0.6343 | risk_factor | 0.9600 | 0.8554 | 0.9332 | 0.7694 | 0.6823 |

| mom6m | 0.9375 | 0.8110 | 0.9016 | 0.7375 | 0.6477 | corrlation | 0.9610 | 0.8633 | 0.9260 | 0.7637 | 0.6802 |

| mom12m | 0.9533 | 0.8204 | 0.9027 | 0.7537 | 0.6669 | PE | 0.9557 | 0.8539 | 0.9214 | 0.7591 | 0.6725 |

| mom36m | 0.9522 | 0.8135 | 0.9132 | 0.7421 | 0.6545 | PB | 0.9484 | 0.8598 | 0.9172 | 0.7698 | 0.6862 |

| mve | 0.9527 | 0.8543 | 0.9174 | 0.7526 | 0.6709 | trade_volume | 0.9519 | 0.8647 | 0.9218 | 0.7819 | 0.6996 |

| mve_ia | 0.9661 | 0.8686 | 0.9316 | 0.7726 | 0.6924 | trade_number | 0.9638 | 0.8622 | 0.9302 | 0.7826 | 0.6971 |

| operprof | 0.9525 | 0.8112 | 0.9089 | 0.7275 | 0.6443 | BullishSent | 0.9554 | 0.8347 | 0.9135 | 0.7542 | 0.6696 |

| orgcap | 0.9622 | 0.8578 | 0.9363 | 0.7345 | 0.6557 | news_senti | 0.9623 | 0.8609 | 0.9238 | 0.7668 | 0.6855 |

| pchcurrat | 0.9635 | 0.8535 | 0.9253 | 0.7505 | 0.6701 | PositiveSent | 0.9546 | 0.8381 | 0.9177 | 0.7543 | 0.6697 |

| pchquick | 0.9651 | 0.8581 | 0.9264 | 0.7559 | 0.6762 | searchindex | 0.9563 | 0.8617 | 0.9219 | 0.7662 | 0.6859 |

| pctacc | 0.9380 | 0.8064 | 0.9114 | 0.7331 | 0.6496 |

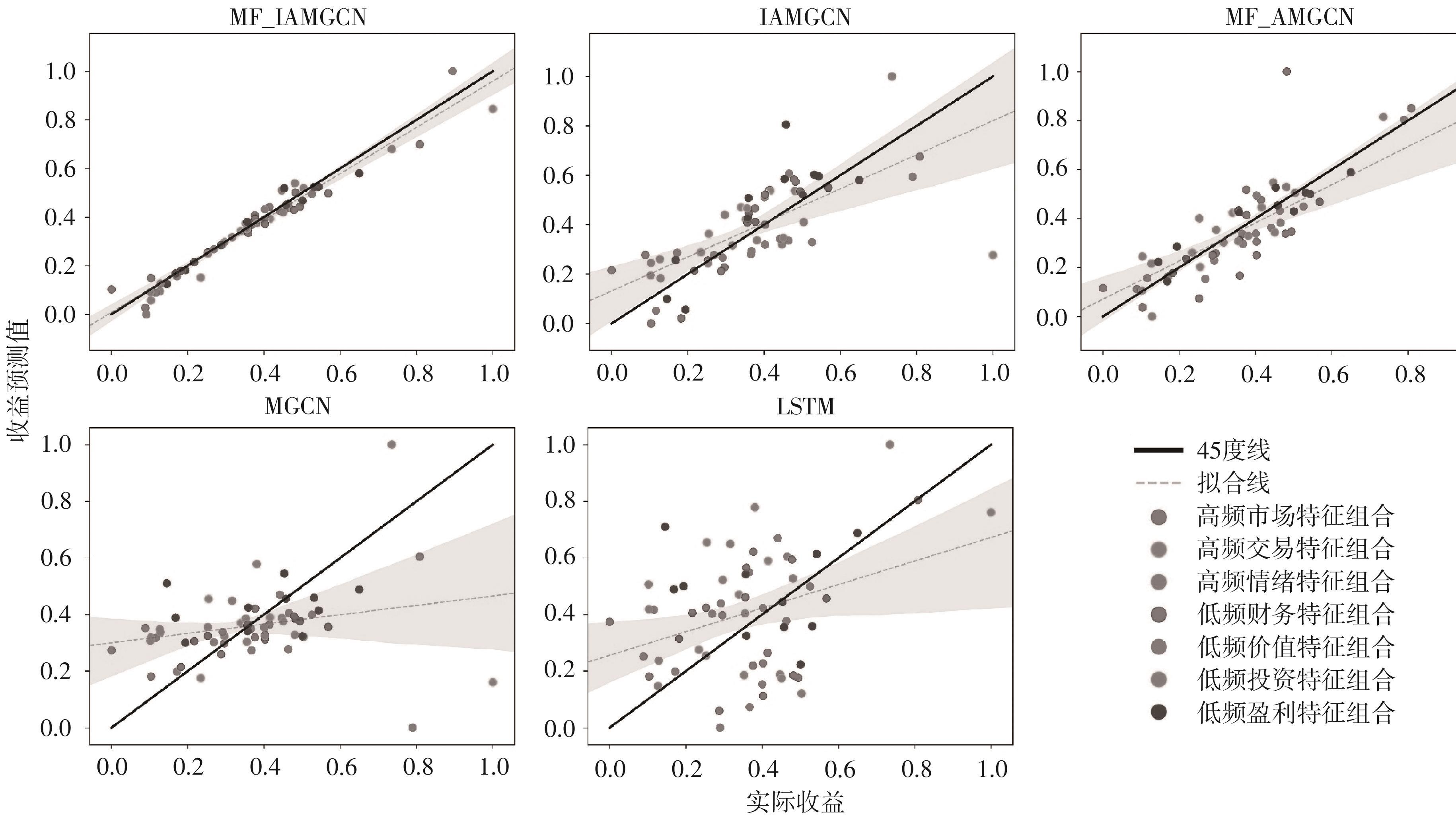

图5

单排序组合超额收益样本外预测散点图"

表8

市值-账面市值比双特征排序组合样本外GF"

| mve/bm | MF-IAMGCN / IAMGCN / MF-AMGCN //MGCN / LSTM / 最小Odds ratio | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 市值↓ 账面市值比→ 低 | 2 | 3 | 4 | 高 | |||||||||||||||

| 低 | 0.9257 | 0.7997 | 0.8148 | 0.9009 | 0.7521 | 0.7448 | 0.8254 | 0.7416 | 0.7799 | 0.8118 | 0.7293 | 0.8058 | 0.7978 | 0.7206 | 0.7787 | ||||

| 0.8288 | 0.8388 | 1.1036 | 0.7080 | 0.7180 | 1.1979 | 0.5678 | 0.5778 | 1.0582 | 0.5491 | 0.5591 | 1.0074 | 0.4625 | 0.4725 | 1.0245 | |||||

| 2 | 0.9213 | 0.8371 | 0.8251 | 0.8923 | 0.8339 | 0.8785 | 0.8824 | 0.8168 | 0.8833 | 0.8082 | 0.7001 | 0.7808 | 0.8435 | 0.7235 | 0.7451 | ||||

| 0.8362 | 0.8462 | 1.0887 | 0.6325 | 0.6425 | 1.0158 | 0.6385 | 0.6485 | 0.9990 | 0.5338 | 0.5438 | 1.0351 | 0.5781 | 0.5881 | 1.1321 | |||||

| 3 | 0.9393 | 0.8023 | 0.8374 | 0.8928 | 0.8290 | 0.8763 | 0.8583 | 0.7919 | 0.8565 | 0.7718 | 0.6564 | 0.7699 | 0.8480 | 0.7506 | 0.7760 | ||||

| 0.8315 | 0.8415 | 1.1163 | 0.6028 | 0.6128 | 1.0189 | 0.6000 | 0.6100 | 1.0020 | 0.4208 | 0.4308 | 1.0025 | 0.5614 | 0.5714 | 1.0928 | |||||

| 4 | 0.9625 | 0.8522 | 0.8617 | 0.9105 | 0.7991 | 0.8285 | 0.9052 | 0.8122 | 0.8603 | 0.8119 | 0.7924 | 0.8029 | 0.8697 | 0.7923 | 0.8263 | ||||

| 0.8580 | 0.8680 | 1.1090 | 0.7421 | 0.7521 | 1.0990 | 0.7137 | 0.7237 | 1.0522 | 0.5796 | 0.5896 | 1.0112 | 0.7015 | 0.7115 | 1.0524 | |||||

| 高 | 0.9550 | 0.7969 | 0.9102 | 0.9866 | 0.8801 | 0.9053 | 0.9763 | 0.8849 | 0.9199 | 0.9446 | 0.8493 | 0.8939 | 0.9015 | 0.7994 | 0.8663 | ||||

| 0.9017 | 0.9117 | 1.0475 | 0.8928 | 0.9028 | 1.0898 | 0.8730 | 0.8830 | 1.0613 | 0.8705 | 0.8805 | 1.0567 | 0.8500 | 0.8600 | 1.0406 | |||||

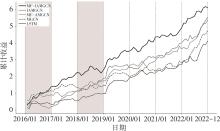

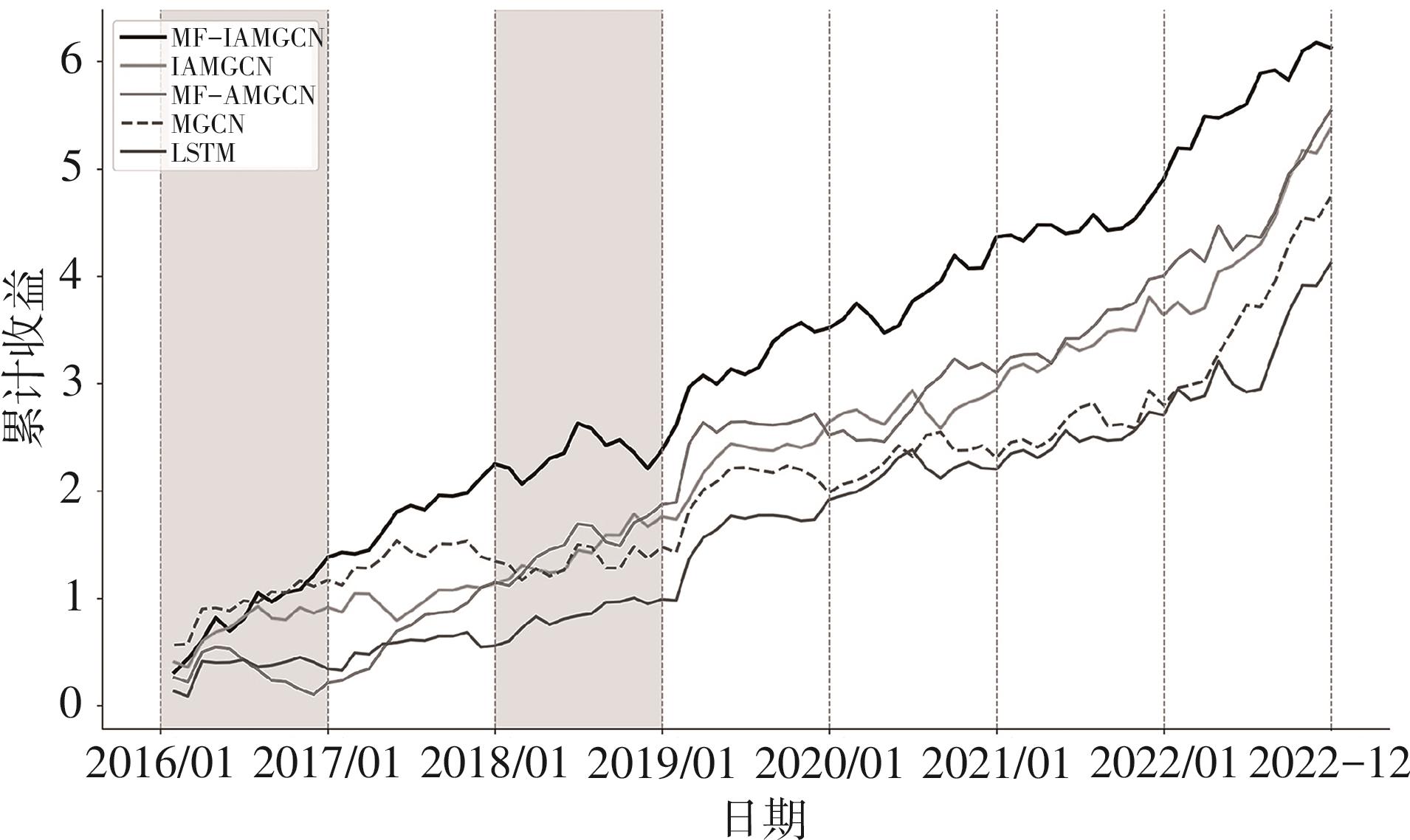

图6

模型投资组合样本外累计收益曲线"

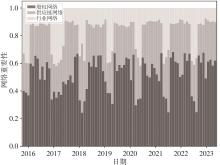

图7

网络重要性"

表9

模型ST分组股票定价误差"

| 模型 | 非ST | ST | 误差增幅 |

|---|---|---|---|

| MF-IAMGCN | 0.0533 | 0.0621 | 16.51% |

| MF-IAMGCN-E | 0.0601 | 0.0814 | 35.44% |

| GCN+E | 0.0686 | 0.0779 | 13.56% |

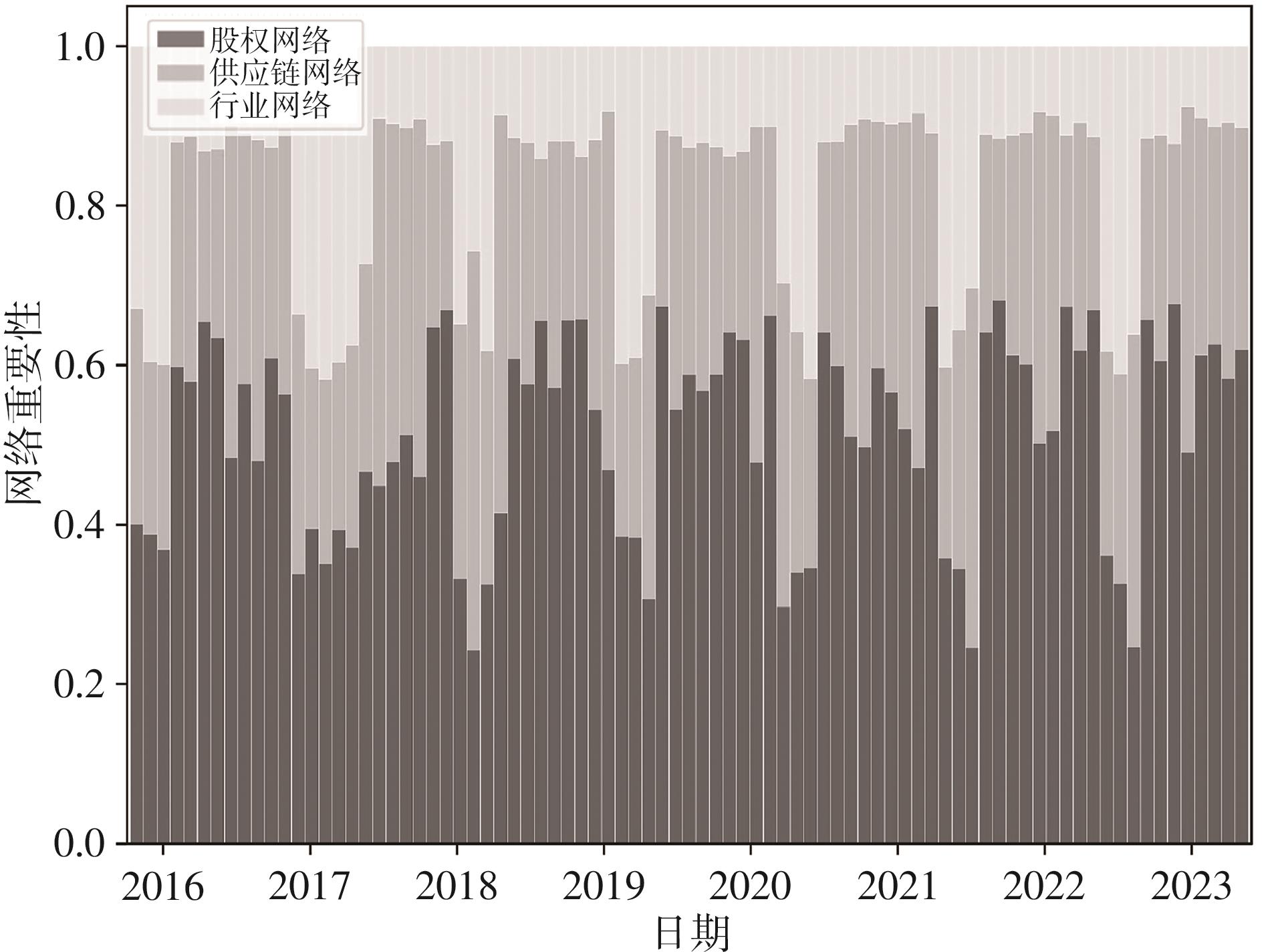

图8

变量重要性"

| [1] | Cochrane J H. Presidential address: Discount rates[J]. The Journal of Finance, 2011, 66(4): 1047-1108. |

| [2] | Sharpe W F. Capital asset prices: A theory of market equilibrium under conditions of risk[J]. The Journal of Finance, 1964, 19(3): 425-442. |

| [3] | Fama E F, French K R. The cross-section of expected stock returns[J]. The Journal of Finance, 1992, 47(2): 427. |

| [4] | Carhart M M. On persistence in mutual fund performance[J]. The Journal of Finance, 1997, 52(1): 57-82. |

| [5] | De Bondt W F M, Thaler R. Does the stock market overreact?[J]. The Journal of Finance, 1985, 40(3): 793-805. |

| [6] | Black F. Capital market equilibrium with restricted borrowing[J]. The Journal of Business, 1972, 45(3): 444-455. |

| [7] | Shi J, Liu X, Li Y, et al. Does supply chain network centrality affect stock price crash risk? Evidence from Chinese listed manufacturing companies[J]. International Review of Financial Analysis, 2022, 80: 102040. |

| [8] | Wen F, Yuan Y, Zhou W X. Cross-shareholding networks and stock price synchronicity: Evidence from China[J]. International Journal of Finance & Economics, 2021, 26(1): 914-948. |

| [9] | Chen W, Qu S, Jiang M, et al. The construction of multilayer stock network model[J]. Physica A: Statistical Mechanics and Its Applications, 2021, 565: 125608. |

| [10] | 王纲金, 吴昊钰, 谢赤. 基于多层关联网络的投资组合优化研究[J]. 系统工程理论与实践, 2022, 42(4): 937-957. |

| Wang G J, Wu H Y, Xie C. Portfolio optimization based on multilayer connectedness networks[J]. Systems Engineering-Theory & Practice, 2022, 42(4): 937-957. | |

| [11] | 刘超, 许澜涛. 多层时序网络视角下的最优投资组合策略研究[J]. 中国管理科学, 2025, 33(9): 46-56. |

| Liu C, Xu L T. Study on optimal portfolio strategy from the perspective of multilayer temporal network[J]. Chinese Journal of Management Science, 2025, 33(9): 46-56. | |

| [12] | Manessi F, Rozza A, Manzo M. Dynamic graph convolutional networks[J]. Pattern Recognition, 2020, 97: 107000. |

| [13] | Wu Z, Pan S, Chen F, et al. A comprehensive survey on graph neural networks[J]. IEEE Transactions on Neural Networks and Learning Systems, 2021, 32(1): 4-24. |

| [14] | Chen W, Jiang M, Zhang W G, et al. A novel graph convolutional feature based convolutional neural network for stock trend prediction[J]. Information Sciences, 2021, 556: 67-94. |

| [15] | Song G, Zhao T, Wang S, et al. Stock ranking prediction using a graph aggregation network based on stock price and stock relationship information[J]. Information Sciences, 2023, 643: 119236. |

| [16] | 卜湛, 张善凡, 李雪延, 等. 基于深度强化学习的自适应股指预测研究[J]. 管理科学学报, 2023, 26(4): 148-174. |

| Bu Z, Zhang S F, Li X Y, et al. Adaptive stock index prediction based on deep reinforcement learning[J]. Journal of Management Sciences in China, 2023, 26(4): 148-174. | |

| [17] | Tan J, Li Q, Wang J, et al. FinHGNN: A conditional heterogeneous graph learning to address relational attributes for stock predictions[J]. Information Sciences, 2022, 618: 317-335. |

| [18] | Brunnermeier M, Farhi E, Koijen R S J, et al. Review article: Perspectives on the future of asset pricing[J]. The Review of Financial Studies, 2021, 34(4): 2126-2160. |

| [19] | Ghysels E, Santa-Clara P, Valkanov R. Predicting volatility: Getting the most out of return data sampled at different frequencies[J]. Journal of Econometrics, 2006, 131(1-2): 59-95. |

| [20] | 谭德凯, 田利辉. 黄金是股票市场的“避险天堂”吗?——基于动态条件相关混频数据抽样模型[J]. 中国管理科学, 2022, 30(10): 14-24. |

| Tan D K, Tian L H. Is gold a safe haven of the stock market? —Based on dynamic conditional correlation mixed data sampling model[J]. Chinese Journal of Management Science, 2022, 30(10): 14-24. | |

| [21] | 刘凤根, 吴军传, 杨希特, 等. 基于混频数据模型的宏观经济对股票市场波动的长期动态影响研究[J]. 中国管理科学, 2020, 28(10): 65-76. |

| Liu F G, Wu J C, Yang X T, et al. Long-Run dynamic effect of macro-economy on stock market volatility based on mixed frequency data model[J]. Chinese Journal of Management Science, 2020, 28(10): 65-76. | |

| [22] | Yang C, Zhang R. Does mixed-frequency investor sentiment impact stock returns? Based on the empirical study of MIDAS regression model[J]. Applied Economics, 2014, 46(9): 966-972. |

| [23] | Xu M, Fu P, Liu B, et al. Multi-stream attention-aware graph convolution network for video salient object detection[J]. IEEE Transactions on Image Processing, 2021, 30: 4183-4197. |

| [24] | Shi J, Zhang W, Bao Y, et al. Load forecasting of electric vehicle charging stations: Attention based spatiotemporal multi-graph convolutional networks[J]. IEEE Transactions on Smart Grid, 2024, 15(3): 3016-3027. |

| [25] | 胡春华, 邓奥, 童小芹, 等. 社交电商中融合信任和声誉的图神经网络推荐研究[J]. 中国管理科学, 2021, 29(10): 202-212. |

| Hu C H, Deng A, Tong X Q, et al. A graph neural network recommendation study combining trust and reputation in social E-commerce[J]. Chinese Journal of Management Science, 2021, 29(10): 202-212. | |

| [26] | 陈妍, 张小威, 金赞, 等. 基于加权GraphSAGE和生成对抗网络的医保欺诈识别方法[J]. 系统工程理论与实践, 2024, 44(2): 732-751. |

| Chen Y, Zhang X W, Jin Z, et al. Medical fraud detection method based on weighted GraphSAGE and generative adversarial network[J]. Systems Engineering-Theory & Practice, 2024, 44(2): 732-751. | |

| [27] | Lin Y, Yan Y, Xu J, et al. Forecasting stock index price using the CEEMDAN-LSTM model[J]. The North American Journal of Economics and Finance, 2021, 57: 101421. |

| [28] | Ghysels E, Kvedaras V, Zemlys V. Mixed frequency data sampling regression models: The R package midasr[J]. Journal of Statistical Software, 2016, 72(4): 1-35. |

| [29] | Leippold M, Wang Q, Zhou W. Machine learning in the Chinese stock market[J]. Journal of Financial Economics, 2022, 145(2): 64-82. |

| [30] | 邵新建, 贾中正, 赵映雪, 等. 借壳上市、内幕交易与股价异动——基于ST类公司的研究[J]. 金融研究, 2014(5): 126-142. |

| Shao X J, Jia Z Z, Zhao Y X, et al. Reverse merger, insider trading and abnormal market reaction: Evidence from ST listed companies in China[J]. Journal of Financial Research, 2014(5): 126-142. |

| [1] | 林娟娟, 黄志刚, 唐勇. 数据质量、数量与数据资产定价:基于消费者异质性视角[J]. 中国管理科学, 2025, 33(5): 88-98. |

| [2] | 李星毅, 李仲飞, 李其谦, 刘昱君, 唐文金. 基于机器学习的资产收益率预测研究综述[J]. 中国管理科学, 2025, 33(1): 311-322. |

| [3] | 倪宣明,郑田田,赵慧敏,武康平. 基于最优异质收益率因子的资产定价研究[J]. 中国管理科学, 2024, 32(8): 50-60. |

| [4] | 许启发, 王泽舟, 蒋翠侠. 基于生成对抗网络的混频资产定价研究[J]. 中国管理科学, 2024, 32(11): 53-64. |

| [5] | 闫达文,李存,迟国泰. 基于混频数据的中国上市公司财务困境动态预测研究[J]. 中国管理科学, 2024, 32(1): 1-12. |

| [6] | 陈淼鑫, 黄振伟. 股价波动的长记忆性与横截面股票收益——基于中国市场的实证研究[J]. 中国管理科学, 2023, 31(4): 1-10. |

| [7] | 陆静, 张银盈. “特质波动率之谜”与估计模型有关吗?[J]. 中国管理科学, 2022, 30(9): 36-48. |

| [8] | 谭德凯, 田利辉. 黄金是股票市场的“避险天堂”吗?——基于动态条件相关混频数据抽样模型[J]. 中国管理科学, 2022, 30(10): 14-24. |

| [9] | 刘燕, 朱宏泉. 个体与机构投资者,谁左右A股股价变化?——基于投资者异质信念的视角[J]. 中国管理科学, 2018, 26(4): 120-130. |

| [10] | 徐元栋. BSV、DHS等模型中资产定价与模糊不确定性下资产定价在逻辑结构上的一致性[J]. 中国管理科学, 2017, 25(6): 22-31. |

| [11] | 龚旭, 文凤华, 黄创霞, 杨晓光. 下行风险、符号跳跃风险与行业组合资产定价[J]. 中国管理科学, 2017, 25(10): 1-10. |

| [12] | 刘维奇, 邢红卫, 张信东. 投资偏好与“特质波动率之谜”——以中国股票市场A股为研究对象[J]. 中国管理科学, 2014, 22(8): 10-20. |

| [13] | 周芳, 张维, 周兵. 基于流动性风险的资本资产定价模型[J]. 中国管理科学, 2013, 21(5): 1-7. |

| [14] | 朱宏泉, 陈林, 潘宁宁. 行业、地区和市场信息,谁主导中国证券市场价格的变化[J]. 中国管理科学, 2011, 19(4): 1-8. |

| [15] | 李勇, 倪中新, 周影辉. 具有结构变化的资产定价模型的贝叶斯自回归条件异方差检验[J]. 中国管理科学, 2010, 18(2): 14-18. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||