主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2026, Vol. 34 ›› Issue (1): 60-71.doi: 10.16381/j.cnki.issn1003-207x.2024.0361cstr: 32146.14.j.cnki.issn1003-207x.2024.0361

马勇1, 陈犁1, 陈炜2( )

)

收稿日期:2024-03-13

修回日期:2024-10-23

出版日期:2026-01-25

发布日期:2026-01-29

通讯作者:

陈炜

E-mail:chenwei@cueb.edu.cn

基金资助:

Yong Ma1, Li Chen1, Wei Chen2()

Received:2024-03-13

Revised:2024-10-23

Online:2026-01-25

Published:2026-01-29

Contact:

Wei Chen

E-mail:chenwei@cueb.edu.cn

摘要:

在我国央行不断加强政策沟通的背景下,探讨货币政策相关信息的发布如何影响资本市场,对于防范信息冲击导致的系统性风险具有重要意义。本文研究了货币政策公告发布前的股价漂移现象的形成机理及其影响因素。理论上,在连续时间理性预期模型框架中,引入了代表央行沟通的公共信息以及股价对货币政策冲击的敏感性,进而分析私有信息、公共信息与股价敏感程度对公告前股价漂移幅度的影响。实证上,采用2010-2022年的A股非金融行业数据进行经验分析,以验证理论模型的含义。研究发现,当私有信息精度越高或公共信息精度越低时,信息不对称越严重,股价漂移幅度越大。机制分析表明,信息不对称会影响投资者的信息获取行为,进而导致股价漂移。调节效应分析表明,股价对货币政策冲击越敏感,信息不对称导致的股价漂移越大。

中图分类号:

马勇,陈犁,陈炜. 货币政策公告前的股价漂移:形成机理与影响因素[J]. 中国管理科学, 2026, 34(1): 60-71.

Yong Ma,Li Chen,Wei Chen. Pre-Monetary Policy Announcement Drift of Stock Price: Formation Mechanism and Determinants[J]. Chinese Journal of Management Science, 2026, 34(1): 60-71.

表1

模型参数设定"

| 参数 | 值 | 含义 | 参数 | 值 | 含义 | 参数 | 值 | 含义 |

|---|---|---|---|---|---|---|---|---|

| 0.03 | 无风险利率 | 1 | 公开信息精度倒数 | 3 | 风险厌恶系数 | |||

| 0.01 | 时间贴现因子 | 0.85 | 股利长期均值波动率 | 35 | 资产供应量无条件均值 | |||

| 80 | 股利无条件均值 | 0.75 | 资产供应量波动率 | 0.6 | 不知情投资者比例 | |||

| 0.15 | 股利均值回复系数 | 0.7 | 私有信息精度倒数 | 10 | 单位时间购买信息成本 | |||

| 0.1 | 资产供应量回复系数 | 0.002 | 私有信息精度倒数 | — | — | — | ||

| 1 | 股利波动率 | 300 | 模糊厌恶系数 | — | — | — |

图1

无信息获取时不知情投资者的信息劣势注:横坐标为相对于公告日的天数,下同"

图2

信息获取存在情形下的价格漂移"

图3

信息精度对信息不对称程度的影响"

图4

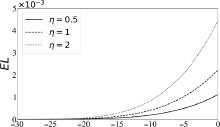

股利与货币政策的相关性对不知情投资者期望损失的影响"

表2

变量描述性统计量"

| 变量 | 样本数 | 均值 | 标准差 | 最小值 | 中位数 | 最大值 |

|---|---|---|---|---|---|---|

| 3159 | 0.063 | 1.734 | -9.703 | 0.190 | 9.689 | |

| 3159 | 0.015 | 1.399 | -9.373 | 0.062 | 7.443 | |

| 3013 | 128.895 | 56.639 | 35.713 | 117.766 | 357.999 | |

| 319605 | 0.396 | 4.786 | -13.269 | 0.299 | 16.414 | |

| 319605 | 0.306 | 4.137 | -11.790 | 0.061 | 14.441 | |

| 296345 | 0.150 | 0.043 | 0.065 | 0.146 | 0.272 | |

| 318473 | 0.091 | 0.144 | 0.001 | 0.047 | 0.969 | |

| 298261 | 0.002 | 0.884 | -2.214 | 0.013 | 2.030 | |

| 298284 | -1.061 | 12.120 | -47.182 | -0.796 | 33.185 | |

| 298284 | 2.625 | 1.332 | 0.746 | 2.323 | 7.994 | |

| 286016 | 1.346 | 0.958 | 0.301 | 1.075 | 7.675 | |

| 318305 | 0.623 | 0.251 | 0.129 | 0.616 | 1.191 | |

| 319599 | 0.028 | 0.036 | -0.080 | 0.020 | 0.156 | |

| 319602 | 22.366 | 1.090 | 20.181 | 22.235 | 25.628 | |

| 294752 | -0.002 | 0.329 | -0.608 | -0.029 | 1.173 | |

| 316123 | -0.008 | 0.512 | -0.719 | -0.100 | 2.586 |

表3

央行沟通不确定性对市场收益率的影响"

| 变量 | EW | VW | ||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| 0.2619*** | 0.2787*** | 0.1207* | 0.1289* | |

| (0.0826) | (0.0859) | (0.0664) | (0.1610) | |

| -0.0045*** | -0.0033*** | |||

| (0.0014) | (0.0011) | |||

| 0.0049*** | 0.0037*** | |||

| (0.0017) | (0.0013) | |||

| 常数项 | -0.1177 | 0.1506 | -0.1447 | 0.0580 |

| (0.1824) | (0.2005) | (0.1554) | (0.1689) | |

| 年份效应 | Yes | Yes | Yes | Yes |

| 月份效应 | Yes | Yes | Yes | Yes |

| 星期效应 | Yes | Yes | Yes | Yes |

| 观测值 | 3159 | 3013 | 3159 | 3013 |

| 0.017 | 0.025 | 0.010 | 0.017 | |

表4

信息不对称影响公告漂移的回归结果"

| 变量 | ||||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| 4.3940*** | 3.8849*** | 4.7430*** | 4.1506*** | |

| (0.2093) | (0.2490) | (0.2062) | (0.2450) | |

| -0.0975*** | -0.1070*** | |||

| (0.0261) | (0.0256) | |||

| -1.9594*** | -1.7116*** | |||

| (0.4093) | (0.4001) | |||

| -0.0141 | -0.0126 | |||

| (0.0097) | (0.0098) | |||

| -0.0299*** | -0.0306*** | |||

| (0.0011) | (0.0011) | |||

| -0.0658*** | -0.0727*** | |||

| (0.0174) | (0.0172) | |||

| -0.1576*** | -0.1642*** | |||

| (0.0104) | (0.0101) | |||

| -0.2211*** | -0.2575*** | |||

| (0.0751) | (0.0740) | |||

| -0.7210*** | -0.7590*** | |||

| (0.0909) | (0.0892) | |||

| 常数项 | 0.6000** | 3.7950*** | 2.1684*** | 5.6107*** |

| (0.2434) | (0.6534) | (0.2376) | (0.6405) | |

| 个体固定效应 | Yes | Yes | Yes | Yes |

| 时间固定效应 | Yes | Yes | Yes | Yes |

| 观测值 | 296345 | 263480 | 296345 | 263480 |

| 0.312 | 0.317 | 0.118 | 0.123 | |

表 5

改变样本区间"

| 变量 | ||||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| 1.9422*** | 3.4465*** | 2.1459*** | 3.6802*** | |

| (0.2860) | (0.3005) | (0.2819) | (0.2959) | |

| 常数项 | 2.3101*** | 4.0123*** | 3.8263*** | 3.0529*** |

| (0.8086) | (0.7783) | (0.7866) | (0.7561) | |

| 控制变量 | Yes | Yes | Yes | Yes |

| 个体固定效应 | Yes | Yes | Yes | Yes |

| 时间固定效应 | Yes | Yes | Yes | Yes |

| 观测值 | 161635 | 180257 | 161635 | 180257 |

| 0.321 | 0.328 | 0.117 | 0.130 | |

表6

替换指标检验"

| 变量 | ||||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| 4.7147*** | 5.1039*** | |||

| (0.2113) | (0.2060) | |||

| 1.8079*** | 1.9953*** | |||

| (0.4146) | (0.4050) | |||

| 常数项 | 2.1391*** | 4.7394*** | 3.7841*** | 6.5645*** |

| (0.6621) | (0.6356) | (0.6495) | (0.6220) | |

| 控制变量 | Yes | Yes | Yes | Yes |

| 个体固定效应 | Yes | Yes | Yes | Yes |

| 时间固定效应 | Yes | Yes | Yes | Yes |

| 观测值 | 263449 | 262705 | 263449 | 262705 |

| 0.318 | 0.296 | 0.124 | 0.108 | |

表 7

工具变量检验"

| 变量 | |||

|---|---|---|---|

| (1) | (2) | (3) | |

| -0.0045*** | |||

| (0.0006) | |||

| 15.7464** | 19.7034*** | ||

| (7.2429) | (7.2279) | ||

| 常数项 | 0.4247*** | -1.9219 | -1.7790 |

| (0.0132) | (3.2331) | (3.2297) | |

| 控制变量 | Yes | Yes | Yes |

| 个体固定效应 | Yes | Yes | Yes |

| 时间固定效应 | Yes | Yes | Yes |

| 观测值 | 263503 | 263503 | 263503 |

| 0.249 | 0.310 | 0.106 |

表 8

信息获取机制分析"

| 变量 | ||

|---|---|---|

| (1) | (2) | |

| 0.1505*** | 0.1553*** | |

| (0.0129) | (0.0248) | |

| 常数项 | 0.4530*** | 0.0585*** |

| (0.0296) | (0.00166) | |

| 控制变量 | Yes | Yes |

| 个体固定效应 | Yes | Yes |

| 时间固定效应 | Yes | Yes |

| 观测值 | 258760 | 316123 |

| 0.613 | 0.073 |

表 9

市场不确定性变化分析"

| 变量 | 高不确定性时期 | 低不确定性时期 | ||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| -0.0570 | 0.0365 | -0.0576** | -0.0274 | |

| (0.0522) | (0.0497) | (0.0251) | (0.0247) | |

| 0.1307* | 0.0299 | 0.0010 | -0.0040 | |

| (0.0684) | (0.0633) | (0.0195) | (0.0265) | |

| -0.0554 | 0.0823* | -0.0063 | 0.0492* | |

| (0.0640) | (0.0469) | (0.0197) | (0.0290) | |

| 0.0240 | 0.0733 | -0.0194 | 0.0484** | |

| (0.0526) | (0.0720) | (0.1797) | (0.0243) | |

| -0.0608*** | -0.0840** | 0.0137 | 0.0852*** | |

| (0.0223) | (0.0358) | (0.0105) | (0.0204) | |

| 0.0047 | -0.0900** | 0.0274 | 0.0334 | |

| (0.0366) | (0.0420) | (0.0278) | (0.0254) | |

| 常数项 | 0.0075* | 0.0020 | 0.0045 | -0.0097 |

| (0.0045) | (0.0075) | (0.0050) | (0.0137) | |

| 观测值 | 3010 | 1946 | 3010 | 1946 |

| 0.0061 | 0.0103 | 0.0009 | 0.0060 | |

表 10

股价的货币政策敏感性的调节效应"

| 变量 | ||||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| 0.1693 | -1.7726** | 0.9878 | -0.6755 | |

| (0.6811) | (0.7379) | (0.8879) | (0.7378) | |

| 0.2270** | 0.2114** | |||

| (0.0632) | (0.0870) | |||

| -2.0845** | -1.7560** | |||

| (0.5882) | (0.8198) | |||

| -0.8099*** | -0.8512*** | |||

| (0.1066) | (0.1073) | |||

| 5.1473*** | 4.2650*** | |||

| (0.6385) | (0.6375) | |||

| 常数项 | 3.8194*** | 4.5381*** | 3.9242*** | 6.3104*** |

| (0.6639) | (0.6627) | (0.6434) | (0.6527) | |

| 控制变量 | Yes | Yes | Yes | Yes |

| 个体固定效应 | Yes | Yes | Yes | Yes |

| 时间固定效应 | Yes | Yes | Yes | Yes |

| 观测值 | 229506 | 263480 | 229506 | 263480 |

| 0.323 | 0.317 | 0.118 | 12.31 | |

| [1] | Lin J, Mei Z, Chen L, et al. Is the People’s Bank of China consistent in words and deeds?[J]. China Economic Review, 2023, 78: 101919. |

| [2] | 张一帆, 林建浩, 杨扬, 等. 央行沟通、信息冲击与国债市场波动[J]. 系统工程理论与实践, 2022, 42(3): 575-590. |

| Zhang Y F, Lin J H, Yang Y, et al. Central bank communication, information shock and Treasury market volatility[J]. Systems Engineering-Theory & Practice, 2022, 42(3): 575-590. | |

| [3] | 郭豫媚, 王航, 郭俊杰. 货币政策预期测度与央行预期管理效果评估[J].金融评论,2023,15(6):47-71+123. |

| Guo Y M, Wang H, Guo J J. Monetary policy expectation measurement and evaluation of the expected management effect of the central bank[J]. Chinese Review of Financial Studies, 2023, 15(6): 47-71+123. | |

| [4] | 陈其安, 雷小燕. 货币政策、投资者情绪与中国股票市场波动性: 理论与实证[J]. 中国管理科学, 2017, 25(11): 1-11. |

| Chen Q A, Lei X Y. Monetary policy, investor sentiment and volatility of Chinese stock market: Theory and evidence[J]. Chinese Journal of Management Science, 2017, 25(11): 1-11. | |

| [5] | 刘晓君, 姜伟, 胡劲松. 基于TVP-VAR模型的信心、货币政策与中国经济波动研究[J]. 中国管理科学, 2019, 27(8): 37-46. |

| Liu X J, Jiang W, Hu J S. A study on confidence, monetary policy and China’s economic fluctuation based on TVP-VAR model[J]. Chinese Journal of Management Science, 2019, 27(8): 37-46. | |

| [6] | 肖争艳, 黄源, 王兆瑞. 央行沟通的股票市场稳定效应研究——基于事件研究法的分析[J]. 经济学动态, 2019(7): 80-93. |

| Xiao Z Y, Huang Y, Wang Z R. The effects of China’s central bank communication on stock market volatility[J]. Economic Perspectives, 2019(7): 80-93. | |

| [7] | 林建浩, 陈良源, 罗子豪, 等. 央行沟通有助于改善宏观经济预测吗?——基于文本数据的高维稀疏建模[J]. 经济研究, 2021, 56(3): 48-64. |

| Lin J H, Chen L Y, Luo Z H, et al. Does central bank communication improve macroeconomic forecasting?High-dimensional sparse modeling based on text data[J]. Economic Research Journal, 2021, 56(3): 48-64. | |

| [8] | Bernanke B S, Kuttner K N. What explains the stock market’s reaction to federal reserve policy?[J]. The Journal of Finance, 2005, 60(3): 1221-1257. |

| [9] | Swanson E T. Measuring the effects of federal reserve forward guidance and asset purchases on financial markets[J].Journal of Monetary Economics,2021,118: 32-53. |

| [10] | Schmeling M, Schrimpf A, Steffensen S A M. Monetary policy expectation errors[J]. Journal of Financial Economics, 2022, 146(3): 841-858. |

| [11] | 郭晔, 黄振, 王蕴. 未预期货币政策与企业债券信用利差——基于固浮利差分解的研究[J]. 金融研究, 2016(6): 67-80. |

| Guo Y, Huang Z, Wang Y. Unexpected monetary policy and credit spreads of corporate bonds in China: An empirical analysis using spreads of fixed and floating rate bonds[J]. Journal of Financial Research, 2016(6): 67-80. | |

| [12] | 朱小能, 周磊. 未预期货币政策与股票市场——基于媒体数据的实证研究[J].金融研究,2018(1): 102-120. |

| Zhu X N, Zhou L. Monetary policy surprises and stock returns: Evidence from media forecasts[J]. Journal of Financial Research, 2018(1): 102-120. | |

| [13] | Savor P, Wilson M. How much do investors care about macroeconomic risk? Evidence from scheduled economic announcements[J]. The Journal of Financial and Quantitative Analysis, 2013, 48(2): 343-375. |

| [14] | Lucca D O, Moench E. The pre-FOMC announcement drift[J]. The Journal of Finance, 2015, 70(1): 329-371. |

| [15] | Cieslak A, Morse A, Vissing-Jorgensen A. Stock returns over the FOMC cycle[J]. The Journal of Finance, 2019, 74(5): 2201-2248. |

| [16] | Hu G X, Pan J, Wang J, et al. Premium for heightened uncertainty: Explaining pre-announcement market returns[J]. Journal of Financial Economics, 2022, 145(3): 909-936. |

| [17] | Fisher A, Martineau C, Sheng J. Macroeconomic attention and announcement risk premia[J]. The Review of Financial Studies, 2022, 35(11): 5057-5093. |

| [18] | Guo R, Jia D, Sun X. Information acquisition, uncertainty reduction, and pre-announcement premium in China[J]. Review of Finance, 2023, 27(3): 1077-1118. |

| [19] | Ai H, Han L J, Pan X N, et al. The cross section of the monetary policy announcement premium[J]. Journal of Financial Economics, 2022, 143(1): 247-276. |

| [20] | Wachter J A, Zhu Y. A model of two days: Discrete news and asset prices[J]. The Review of Financial Studies, 2022, 35(5): 2246-2307. |

| [21] | Han L J. Announcements, expectations, and stock returns with asymmetric information[J]. Journal of Monetary Economics, 2025, 151: 103751. |

| [22] | Wang J. A model of intertemporal asset prices under asymmetric information[J]. The Review of Economic Studies, 1993, 60(2): 249-282. |

| [23] | 赵向琴, 袁靖. 罕见灾难风险与中国股权溢价[J]. 系统工程理论与实践, 2016, 36(11): 2764-2777. |

| Zhao X Q, Yuan J. Disaster risk and equity premium in China[J]. Systems Engineering —Theory & Practice, 2016, 36(11): 2764-2777. | |

| [24] | 陈彦斌, 林晨, 陈小亮. 人工智能、老龄化与经济增长[J]. 经济研究, 2019, 54(7): 47-63. |

| Chen Y B, Lin C, Chen X L. Artificial intelligence, aging and economic growth[J]. Economic Research Journal, 2019, 54(7): 47-63. | |

| [25] | 贾盾, 孙溪, 郭瑞. 货币政策公告、政策不确定性及股票市场的预公告溢价效应——来自中国市场的证据[J]. 金融研究, 2019(7): 76-95. |

| Jia D, Sun X, Guo R. Monetary announcements, policy uncertainty, and equity premium in China[J]. Journal of Financial Research, 2019(7): 76-95. | |

| [26] | Huang Y, Luk P. Measuring economic policy uncertainty in China[J]. China Economic Review, 2020, 59: 101367. |

| [27] | MacKinlay A C. Event studies in economics and finance[J]. Journal of Economic Literature, 1997, 35(1): 13-39. |

| [28] | Chordia T, Hu J, Subrahmanyam A, et al. Order flow volatility and equity costs of capital[J]. Management Science, 2019, 65(4): 1520-1551. |

| [29] | Huang H G, Tsai W C, Weng P S, et al. Volatility of order imbalance of institutional traders and expected asset returns: Evidence from Taiwan [J]. Journal of Financial Markets, 2021, 52: 100546. |

| [30] | Bollerslev T, Li J, Xue Y. Volume, volatility, and public news announcements[J]. The Review of Economic Studies, 2018, 85(4): 2005-2041. |

| [31] | 毛杰, 刘红忠. 股市信息不对称对股价暴跌的影响——基于不确定性的新视角[J]. 管理科学学报, 2023, 26(8): 117-132. |

| Mao J, Liu H Z. The impact of stock market information asymmetry on stock price crash: A new perspective of uncertainty[J]. Journal of Management Sciences in China, 2023, 26(8): 117-132. | |

| [32] | Lee C M C, Qu Y, Shen T. Gate fees: The pervasive effect of IPO restrictions on Chinese equity markets[J]. Review of Finance, 2023, 27(3): 809-849. |

| [33] | Chae J. Trading volume, information asymmetry, and timing information[J]. The Journal of Finance, 2005, 60(1): 413-442. |

| [34] | 陈国进, 张润泽, 谢沛霖, 等. 知情交易、信息不确定性与股票风险溢价[J]. 管理科学学报, 2019, 22(4): 53-74. |

| Chen G J, Zhang R Z, Xie P L, et al. Informed trading, information uncertainty and stock risk premium[J]. Journal of Management Sciences in China, 2019, 22(4): 53-74. | |

| [35] | Drake M S, Jennings J, Roulstone D T, et al. The comovement of investor attention[J]. Management Science, 2017, 63(9): 2847-2867. |

| [36] | 王春岚, 施文, 孙芳芳, 等. 金融市场中的信息传递机制——投资者关注转移视角下基于中国A股市场的实证研究[J]. 中国管理科学, 2024, 32(12): 15-24. |

| Wang C L, Shi W, Sun F F, et al. Information transfer in financial market: Evidence based on investor attention transfer in Chinese A-share market[J]. Chinese Journal of Management Science, 2024, 32(12): 15-24. | |

| [37] | Ozdagli A K. Financial frictions and the stock price reaction to monetary policy[J]. The Review of Financial Studies, 2018, 31(10): 3895-3936. |

| [38] | Ozdagli A, Velikov M. Show me the money: The monetary policy risk premium[J]. Journal of Financial Economics, 2020, 135(2): 320-339. |

| [39] | Chava S, Hsu A. Financial constraints, monetary policy shocks, and the cross-section of equity returns[J]. The Review of Financial Studies, 2020, 33(9): 4367-4402. |

| [40] | Whited T M, Wu G. Financial constraints risk[J]. The Review of Financial Studies,2006,19(2): 531-559. |

| [41] | Savor P, Wilson M. Asset pricing: A tale of two days[J]. Journal of Financial Economics, 2014, 113(2): 171-201. |

| [1] | 胡强, 谢吉青, 张广思, 梁玲, 谢家平. 政府激励科创平台协同创新的契约设计——基于双重信息不对称视角[J]. 中国管理科学, 2026, 34(1): 153-166. |

| [2] | 甘柳, 蔡颖俐, 徐明玉, 谭英贤. 二级债券市场信息获取与可转债融资[J]. 中国管理科学, 2025, 33(9): 22-32. |

| [3] | 周驰, 李赫, 于静. 委托代理关系下品牌商网络直播营销激励机制设计[J]. 中国管理科学, 2025, 33(4): 265-274. |

| [4] | 许明辉, 袁睢秋, 秦颖, 张佳. 基于委托代理理论的逆向供应链激励机制设计与回收模式选择[J]. 中国管理科学, 2025, 33(3): 297-313. |

| [5] | 李新军, 王利. 双重供需关系下基于信息禀赋差异的均衡采购战略[J]. 中国管理科学, 2025, 33(12): 285-293. |

| [6] | 李晓娜,马卫民. 需求不确定下高耗水企业节水服务外包决策研究[J]. 中国管理科学, 2024, 32(8): 230-240. |

| [7] | 刘祥,杨招军,刘苏华. 信息不对称与信用担保贝叶斯均衡分析[J]. 中国管理科学, 2024, 32(7): 1-10. |

| [8] | 冯颖,魏敏,何文豪,张炎治. 质量信息不对称下考虑参考价格效应的灰市供应链定价决策[J]. 中国管理科学, 2024, 32(6): 207-218. |

| [9] | 金亮,卢海涛. 技术授权与新产品引入:基于跨国竞合视角[J]. 中国管理科学, 2024, 32(6): 98-108. |

| [10] | 王军进, 许淞俊, 刘家国. 面对不确定性供应中断风险的制造商采购策略研究[J]. 中国管理科学, 2024, 32(12): 269-277. |

| [11] | 金亮,朱颖. 信息不对称下技术供应链专利许可合同设计[J]. 中国管理科学, 2024, 32(1): 211-219. |

| [12] | 林强, 马嘉昕, 陈亮君, 林晓刚, 周永务. 考虑成本信息不对称的生鲜电商销售模式选择研究[J]. 中国管理科学, 2023, 31(6): 153-163. |

| [13] | 牛腾,赵息. 信息不对称下业绩补偿承诺对企业并购时机的影响研究[J]. 中国管理科学, 2023, 31(12): 46-56. |

| [14] | 王明涛,李茜. 融资融券降低了交易中的信息不对称程度吗?[J]. 中国管理科学, 2023, 31(10): 1-11. |

| [15] | 刘浪, 汪惠, 黄冬宏. 销售成本信息不对称下供应商风险规避的回购契约[J]. 中国管理科学, 2023, 31(1): 158-167. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||