主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2025, Vol. 33 ›› Issue (11): 1-13.doi: 10.16381/j.cnki.issn1003-207x.2021.2663cstr: 32146.14.j.cnki.issn1003-207x.2021.2663

• • 下一篇

王超1( ), 何建敏2, 刘晓星2

), 何建敏2, 刘晓星2

收稿日期:2021-12-23

修回日期:2022-11-04

出版日期:2025-11-25

发布日期:2025-11-28

通讯作者:

王超

E-mail:wangchaoedu@njau.edu.cn

基金资助:

Chao Wang1(), Jianmin He2, Xiaoxing Liu2

Received:2021-12-23

Revised:2022-11-04

Online:2025-11-25

Published:2025-11-28

Contact:

Chao Wang

E-mail:wangchaoedu@njau.edu.cn

摘要:

通过银行系统性损失模型度量我国银行市场面临压力测试时的系统性风险状况,探究多元化经营与业务相似性之间的关系,进而以业务相似性作为中介变量分析多元化经营对银行系统性风险的影响,揭示银行系统性风险的传染过程,明确银行系统性风险的形成机制。结果表明大型银行通常能够通过多元化经营降低其业务相似性,对于部分中小银行来说多元化经营对业务相似性的促进作用更加明显,而业务过度相似引起的风险传染是目前影响我国银行市场稳定性的关键因素。尽管业务相似性会促进银行系统性风险传染,但是对于大型国有商业银行来说却具有双重效应,在不发生严重系统性风险的情况下能够通过其稳定性的优势分散其他银行的资产冲击。上述研究结果为我国商业银行的业务转型以及系统性风险防范化解等问题提供了监管参考。

中图分类号:

王超,何建敏,刘晓星. 多元化经营、业务相似性与银行系统性风险[J]. 中国管理科学, 2025, 33(11): 1-13.

Chao Wang,Jianmin He,Xiaoxing Liu. Investment Diversification, Business Similarity and Systemic Risk[J]. Chinese Journal of Management Science, 2025, 33(11): 1-13.

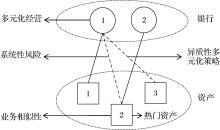

图1

多元化经营的银行系统性风险形成机制示意图"

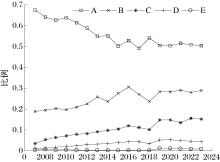

图2

各类银行的资产规模占比"

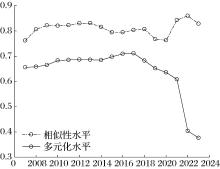

图3

银行多元化经营水平和业务相似性水平"

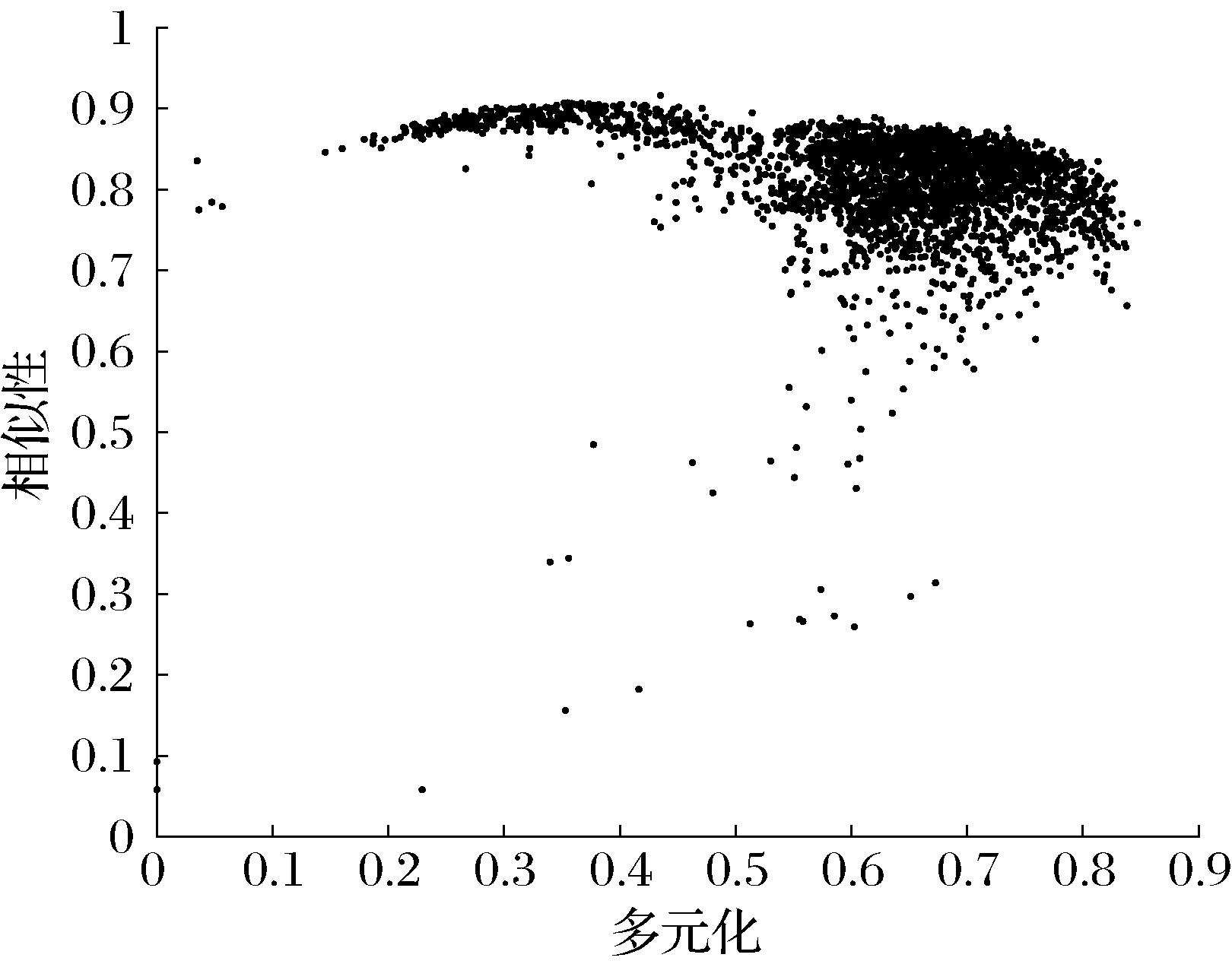

图4

银行多元化经营与业务相似性的关系"

表1

银行多元化经营与业务相似性的关系检验"

| (1) | (2) | (3) | |

|---|---|---|---|

| 门限值 | 0.55 | 0.41 | 0.51 |

0.12*** (0.03) | 0.49*** (0.06) | 0.25*** (0.04) | |

-0.17*** (0.02) | -0.12*** (0.02) | -0.16*** (0.02) | |

| 时间固定 | 是 | 否 | 是 |

| 类别固定 | 否 | 是 | 是 |

| 观测数量 | 2730 | 2730 | 2730 |

表2

不同类别银行多元化经营水平的统计特征"

| 银行类别 | <门限值 | >门限值 | 平均值 | 数量 |

|---|---|---|---|---|

| A | 1.25% | 98.75% | 0.66 | 81 |

| B | 10.34% | 89.66% | 0.65 | 203 |

| C | 12.69% | 87.31% | 0.66 | 1032 |

| D | 20.41% | 79.59% | 0.58 | 1132 |

| E | 14.18% | 85.82% | 0.59 | 282 |

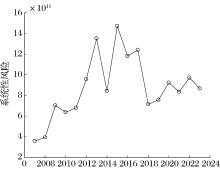

图5

银行市场的系统性风险水平"

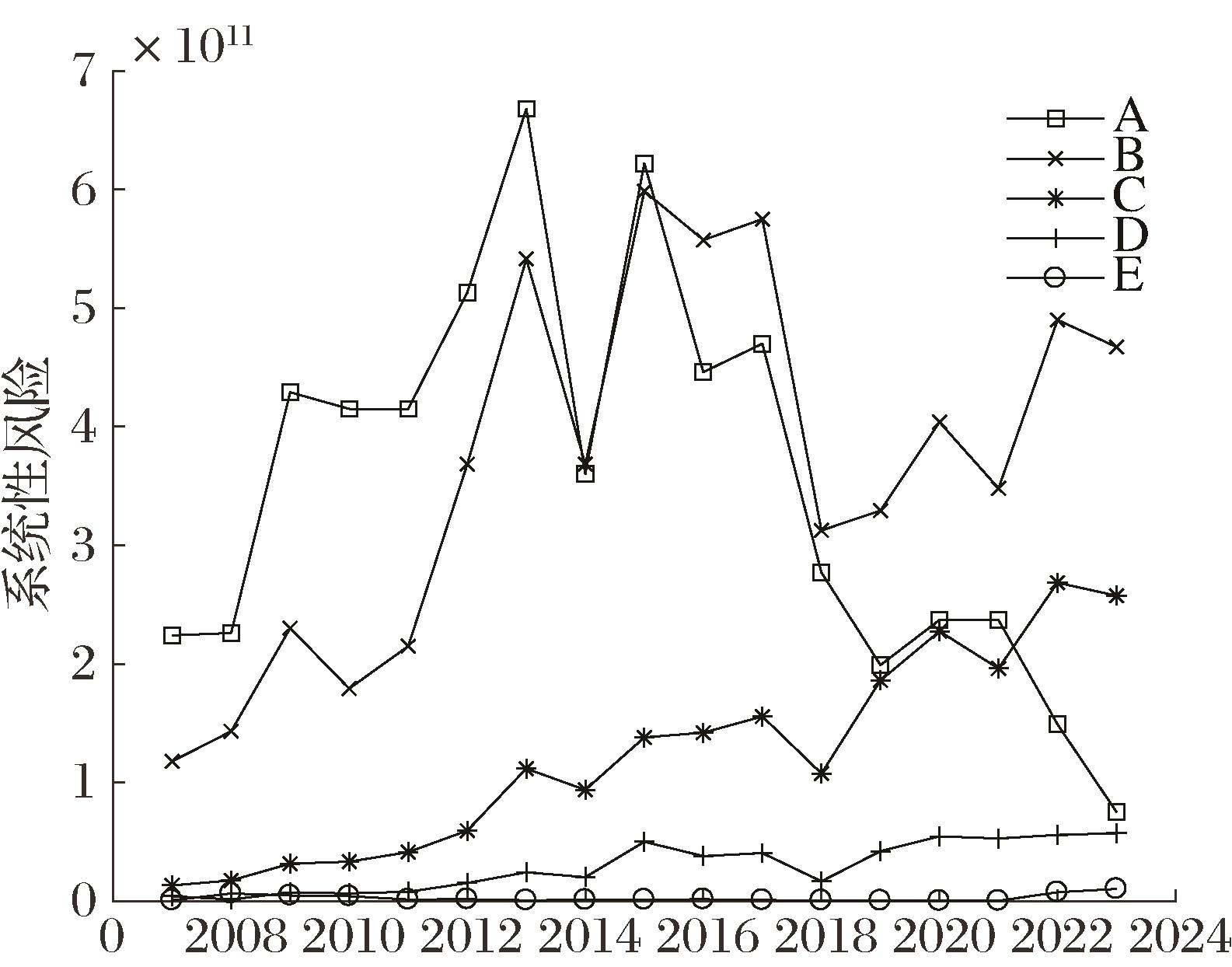

图6

不同类别银行的系统性风险水平"

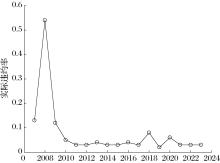

图7

个体银行的实际违约概率"

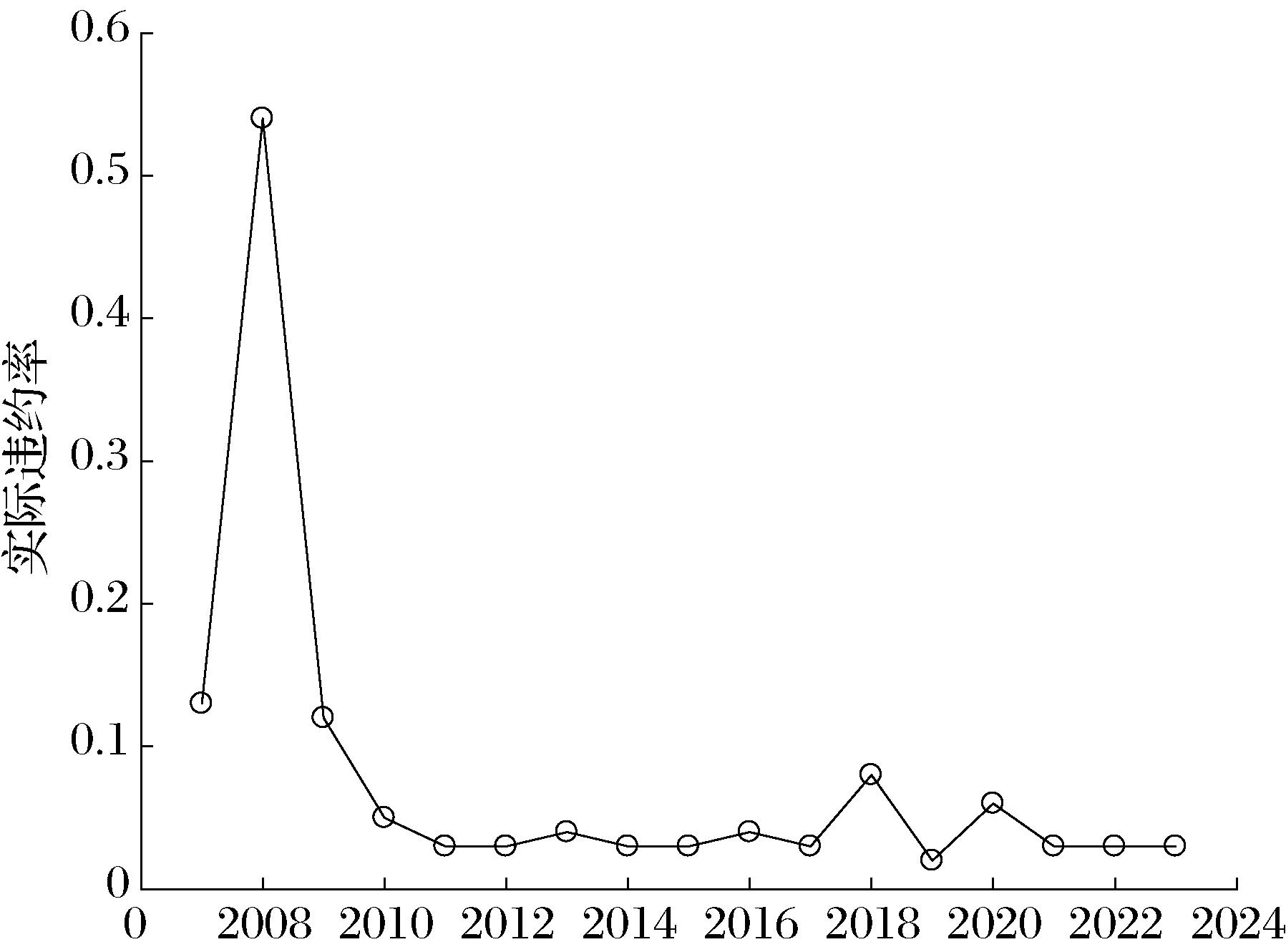

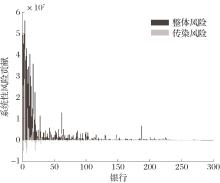

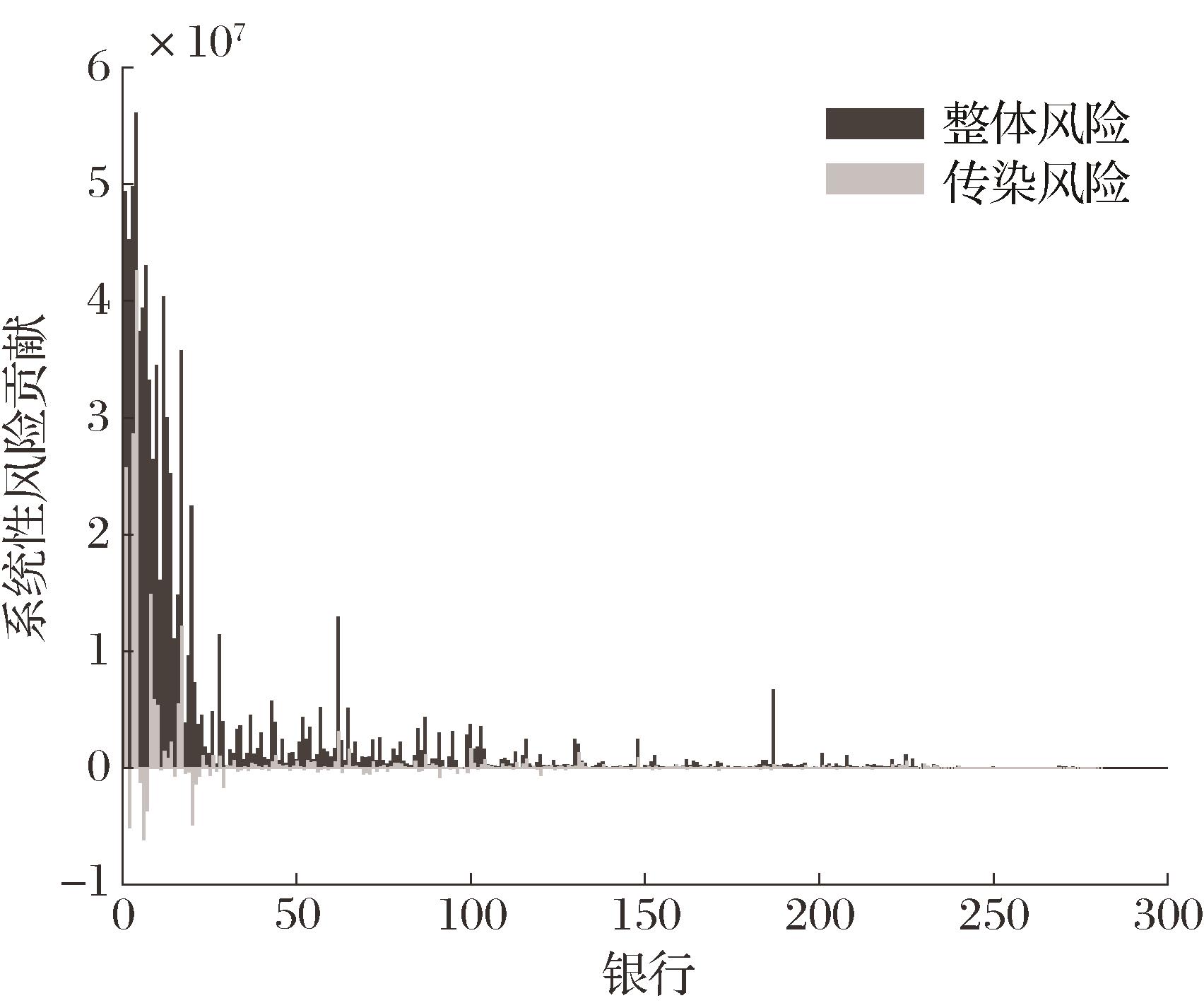

图8

银行系统性风险贡献"

图9

不考虑尾部风险的银行系统性风险贡献"

表3

银行系统性风险的形成机制检验"

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| DIV | 0.97** (0.45) | 0.20*** (0.06) | 0.47 (0.41) | 0.97** (0.47) | 0.20*** (0.06) | 0.43 (0.43) |

| DIV2 | -1.56*** (0.40) | -0.58*** (0.06) | -0.69* (0.37) | -1.45*** (0.42) | -0.58*** (0.06) | -0.57 (0.39) |

| SIM | 3.12*** (0.14) | 3.14*** (0.15) | ||||

| CAP | -0.41*** (0.00) | -0.00 (0.00) | -0.41*** (0.00) | -0.41*** (0.00) | -0.00 (0.00) | -0.42*** (0.00) |

| ASS | 1.02*** (0.01) | -0.00*** (0.00) | 1.04*** (0.01) | 1.01*** (0.01) | -0.00*** (0.00) | 1.03*** (0.01) |

| 时间固定 | -0.41 (0.30) | 0.86*** (0.04) | -3.10*** (0.30) | -0.72** (0.31) | 0.86*** (0.04) | -3.41*** (0.32) |

| 类别固定 | 是 | 是 | 是 | 是 | 是 | 是 |

| 观测数量 | 是 | 是 | 是 | 是 | 是 | 是 |

| Adj. R2 | 2662 | 2729 | 2662 | 2658 | 2729 | 2658 |

| [1] | Roncoroni A, Battiston S, D’Errico M, et al. Interconnected banks and systemically important exposures[J]. Journal of Economic Dynamics and Control, 2021, 133: 104266. |

| [2] | 周爱民, 赵业翔. 价格冲击、资产抛售与银行网络系统性金融风险[J]. 财贸经济, 2023, 44(10): 40-56. |

| Zhou A M, Zhao Y X. Price shocks, fire sale and systemic financial risk in the banking network[J]. Finance & Trade Economics, 2023, 44(10): 40-56. | |

| [3] | Caccioli F, Farmer J D, Foti N, et al. Overlapping portfolios, contagion, and financial stability[J]. Journal of Economic Dynamics and Control, 2015, 51: 50-63. |

| [4] | Silva T C, da Silva Alexandre M, Tabak B M. Bank lending and systemic risk: A financial-real sector network approach with feedback[J]. Journal of Financial Stability, 2018, 38: 98-118. |

| [5] | 张天顶, 张宇. 模型不确定下我国商业银行系统性风险影响因素分析[J]. 国际金融研究, 2017(3): 45-54. |

| Zhang T D, Zhang Y. Analysis of systemic risk determinants of China’s commercial banks—Based on the model uncertainty[J]. Studies of International Finance, 2017(3): 45-54. | |

| [6] | Shim J. Loan portfolio diversification, market structure and bank stability[J]. Journal of Banking & Finance, 2019, 104: 103-115. |

| [7] | Cai J, Eidam F, Saunders A, et al. Syndication, interconnectedness, and systemic risk[J]. Journal of Financial Stability, 2018, 34: 105-120. |

| [8] | Wang C, Liu X, He J. Does diversification promote systemic risk?[J]. The North American Journal of Economics and Finance, 2022, 61: 101680. |

| [9] | 钱崇秀, 宋光辉, 许林. 信贷扩张、资产多元化与商业银行流动性风险[J].管理评论,2018, 30(12): 13-22. |

| Qian C X, Song G H, Xu L. Credit expansion, asset diversification and liquidity risk of commercial banks[J]. Management Review, 2018, 30(12): 13-22. | |

| [10] | 张琳, 廉永辉. 债券投资如何影响商业银行系统性风险?——基于系统性风险分解的视角[J]. 国际金融研究, 2020(2): 66-76. |

| Zhang L, Lian Y H. How does bond investment affect the systemic risk of commercial banks?——From the perspective of systemic risk decomposition[J]. Studies of International Finance, 2020(2): 66-76. | |

| [11] | 翟永会. 系统性风险管理视角下实体行业与银行业间风险溢出效应研究[J]. 国际金融研究, 2019(12): 74-84. |

| Zhai Y H. Research on the risk spillover effect between entity industry and banking industry from the perspective of systemic risk management[J]. Studies of International Finance, 2019(12): 74-84. | |

| [12] | De Jonghe O, Diepstraten M, Schepens G. Banks’ size, scope and systemic risk: What role for conflicts of interest?[J]. Journal of Banking & Finance, 2015, 61: S3-S13. |

| [13] | 朱波, 杨文华, 邓叶峰. 非利息收入降低了银行的系统性风险吗?——基于规模异质的视角[J]. 国际金融研究, 2016(4): 62-73. |

| Zhu B, Yang W H, Deng Y F. Does the non-interest income of China’s listed banks reduce the systemic risk?——An analysis from the perspective of size heterogeneity[J]. Studies of International Finance, 2016(4): 62-73. | |

| [14] | 马传慧, 方军雄. 贷款跨行业多元化是否降低了银行系统性风险?——基于中国上市银行的证据[J]. 会计研究, 2024(5): 143-155. |

| Ma C H, Fang J X. Does cross-industry loan diversification reduce bank systemic risk? evidence from listed banks in China[J]. Accounting Research, 2024(5): 143-155. | |

| [15] | Glasserman P, Young H P. How likely is contagion in financial networks?[J]. Journal of Banking & Finance, 2015, 50: 383-399. |

| [16] | 黄玮强, 范铭杰, 庄新田. 基于借贷关联网络的我国银行间市场风险传染[J]. 系统管理学报, 2019, 28(5): 899-906. |

| Huang W Q, Fan M J, Zhuang X T. Risk contagion in China’s interbank based on interbank lending network[J]. Journal of Systems & Management, 2019, 28(5): 899-906. | |

| [17] | 姚鸿, 王超, 何建敏, 等. 银行投资组合多元化与系统性风险的关系研究[J]. 中国管理科学, 2019, 27(2): 9-18. |

| Yao H, Wang C, He J M, et al. Study on the relationship between investment portfolios diversification and systemic risk[J]. Chinese Journal of Management Science, 2019, 27(2): 9-18. | |

| [18] | Šeho M, Bacha O I, Smolo E. Bank financing diversification, market structure, and stability in a dual-banking system[J]. Pacific-Basin Finance Journal, 2024, 86: 102461. |

| [19] | Shabir M, Jiang P, Shahab Y, et al. Diversification and bank stability: Role of political instability and climate risk[J]. International Review of Economics & Finance, 2024, 89: 63-92. |

| [20] | 李政, 朱明皓, 范颖岚. 我国金融机构的传染性风险与系统性风险贡献——基于极端风险网络视角的研究[J]. 南开经济研究, 2019(6): 132-157. |

| Li Z, Zhu M H, Fan Y L. The contagious risk and systemic risk contribution of Chinese financial institutions: A study based on the perspective of extreme risk network[J].Nankai Economic Studies,2019(6): 132-157. | |

| [21] | Acharya V V, Pedersen L H, Philippon T, et al. Measuring systemic risk[J]. The Review of Financial Studies, 2017, 30(1): 2-47. |

| [22] | Brownlees C, Engle R F. SRISK: A conditional capital shortfall measure of systemic risk[J]. The Review of Financial Studies, 2017, 30(1): 48-79. |

| [23] | 陈湘鹏, 周皓, 金涛, 等. 微观层面系统性金融风险指标的比较与适用性分析——基于中国金融系统的研究[J]. 金融研究, 2019(5): 17-36. |

| Chen X P, Zhou H, Jin T, et al. Comparison and applicability analysis of micro-level systemic risk measures: A study based on China’s financial system[J]. Journal of Financial Research, 2019(5): 17-36. | |

| [24] | 杨子晖, 陈里璇, 陈雨恬. 经济政策不确定性与系统性金融风险的跨市场传染——基于非线性网络关联的研究[J]. 经济研究, 2020, 55(1): 65-81. |

| Yang Z H, Chen L X, Chen Y T. Cross-market contagion of economic policy uncertainty and systemic financial risk: A nonlinear network connectedness analysis[J].Economic Research Journal, 2020,55(1): 65-81. | |

| [25] | 欧阳资生, 周学伟. 中国金融机构系统性风险回测与关联研究——基于MES和ΔCoVaR的实证分析[J]. 中国管理科学, 2025, 33(6): 14-26. |

| Ouyang Z S, Zhou X W. Systemic risk backtesting and connectedness of Chinese financial institutions: Evidence from MES and ΔCoVaR[J]. Chinese Journal of Management Science, 2025, 33(6): 14-26. | |

| [26] | 章秀, 周尧婷, 李岳山. 中国系统重要性银行的关联网络与风险贡献研究——基于极端事件冲击视角[J]. 中央财经大学学报, 2025(4): 24-40. |

| Zhang X, Zhou Y T, Li Y S. Research on the network connectivity and risk contributions of China’s systemically important banks: A perspective of extreme event shocks[J]. Journal of Central University of Finance & Economics, 2025(4): 24-40. | |

| [27] | Tasca P, Battiston S, Deghi A. Portfolio diversification and systemic risk in interbank networks[J]. Journal of Economic Dynamics and Control,2017,82: 96-124. |

| [28] | Roukny T, Battiston S, Stiglitz J E. Interconnectedness as a source of uncertainty in systemic risk[J]. Journal of Financial Stability, 2018, 35: 93-106. |

| [29] | 方意, 刘江龙. 银行关联性与系统性金融风险: 传染还是分担?[J]. 金融研究, 2023(6): 57-74. |

| Fang Y, Liu J L. Bank interconnectedness and systemic risk: Contagion or sharing?[J]. Journal of Financial Research, 2023(6): 57-74. | |

| [30] | 黄岩渠, 何阳, 喻采平. 资产异质视角下我国的系统性金融风险研究[J].中国软科学,2024(4): 176-188. |

| Huang Y Q, He Y, Yu C P. Research on systemic financial risk in China from the perspective of asset heterogeneity[J].China Soft Science,2024(4): 176-188. | |

| [31] | 隋聪, 王宪峰, 王宗尧. 银行间债务网络流动性差异对风险传染的影响[J]. 管理科学学报, 2020, 23(3): 65-72. |

| Sui C, Wang X F, Wang Z Y. The impacts of interbank debt network liquidity differences on risk contagion[J]. Journal of Management Sciences in China, 2020, 23(3): 65-72. | |

| [32] | 王辉, 朱家雲, 陈旭. 银行间市场网络稳定性与系统性金融风险最优应对策略: 政府控股视角[J]. 经济研究, 2021, 56(11): 100-118. |

| Wang H, Zhu J Y, Chen X. Interbank network stability and optimal strategies to deal with systemic financial risk: Based on the perspective of government shareholding[J]. Economic Research Journal, 2021, 56(11): 100-118. | |

| [33] | Eboli M. A flow network analysis of direct balance-sheet contagion in financial networks[J]. Journal of Economic Dynamics and Control, 2019, 103: 205-233. |

| [34] | 范小云, 荣宇浩, 王博. 我国系统重要性银行评估: 网络层次结构视角[J]. 管理科学学报, 2021, 24(2): 48-74. |

| Fan X Y, Rong Y H, Wang B. Identifying systemically important banks in China: A network hierarchy structure perspective[J]. Journal of Management Sciences in China, 2021, 24(2): 48-74. | |

| [35] | 沈虹, 张晨曜, 刘晓星. 基于多层网络结构的行业间风险联动机制研究[J].中国管理科学, 2024, 32(12): 173-182. |

| Shen H, Zhang C Y, Liu X X. Analysis of risk spillover characteristics and mechanism among industries: Evidence from multilayer network[J]. Chinese Journal of Management Science, 2024, 32(12): 173-182. | |

| [36] | 徐国祥, 吴婷, 王莹. 基于共同冲击和异质风险叠加传导的风险传染研究——来自中国上市银行网络的传染模拟[J]. 金融研究, 2021(4): 38-54. |

| Xu G X, Wu T, Wang Y. A study of risk contagion based on the interaction between common shocks and idiosyncratic risks: Evidence from the simulation of listed banks in China[J]. Journal of Financial Research, 2021(4): 38-54. | |

| [37] | Bardoscia M, Barucca P, Codd A B, et al. Forward-looking solvency contagion[J]. Journal of Economic Dynamics and Control, 2019, 108: 103755. |

| [38] | Peltonen T A, Rancan M, Sarlin P. Interconnectedness of the banking sector as a vulnerability to crises[J]. International Journal of Finance & Economics, 2019, 24(2): 963-990. |

| [39] | De Lisa R, Zedda S, Vallascas F, et al. Modelling deposit insurance scheme losses in a Basel 2 framework[J]. Journal of Financial Services Research, 2011, 40(3): 123-141. |

| [40] | Benczur P, Cannas G, Cariboni J, et al. Evaluating the effectiveness of the new EU bank regulatory framework: A farewell to bail-out?[J]. Journal of Financial Stability, 2017, 33: 207-223. |

| [41] | 杨子晖, 李东承. 我国银行系统性金融风险研究——基于“去一法”的应用分析[J].经济研究,2018, 53(8): 36-51. |

| Yang Z H, Li D C. An investigation of the systemic risk of Chinese banks: An application based on leave-one-out[J]. Economic Research Journal, 2018, 53(8): 36-51. | |

| [42] | 宋清华, 宋一程, 刘金玉, 等. 多元化能降低银行风险吗?——来自中国上市银行的经验证据[J]. 财经理论与实践, 2016, 37(5): 9-15. |

| Song Q H, Song Y C, Liu J Y, et al. Can diversification reduce the risk of banks? -empirical evidence from listed banks in China[J]. The Theory and Practice of Finance and Economics, 2016, 37(5): 9-15. | |

| [43] | Sironi A, Zazzara C. Applying credit risk models to deposit insurance pricing: Empirical evidence from the Italian banking system[J]. Journal of International Banking Regulations, 2004, 6(1): 10-32. |

| [44] | Zedda S, Cannas G. Analysis of banks’ systemic risk contribution and contagion determinants through the leave-one-out approach[J]. Journal of Banking & Finance, 2020, 112: 105160. |

| [1] | 刘高峰, 李佳静, 王慧敏, 龚艳冰, 陶飞飞. 城市暴雨洪涝灾害链辨识及系统性风险评估[J]. 中国管理科学, 2025, 33(7): 222-231. |

| [2] | 欧阳资生, 周学伟. 中国金融机构系统性风险回测与关联研究[J]. 中国管理科学, 2025, 33(6): 14-26. |

| [3] | 姚海祥, 刘秋瑜, 杨晓光. 增强还是减弱:新型金融与传统金融行业之间系统性风险溢出[J]. 中国管理科学, 2025, 33(3): 1-12. |

| [4] | 沈嘉贤, 陈浩智, 张卫国. 基于知识图谱网络特征的中国外汇市场系统性风险测度研究[J]. 中国管理科学, 2025, 33(3): 45-61. |

| [5] | 吴文洋,蒋海,唐绅峰. 数字化转型、网络关联性与银行系统性风险[J]. 中国管理科学, 2024, 32(3): 9-19. |

| [6] | 沈虹, 张晨曜, 刘晓星. 基于多层网络结构的行业间风险联动机制研究[J]. 中国管理科学, 2024, 32(12): 173-182. |

| [7] | 赵静, 郭晔. 金融强监管、影子银行与银行系统性风险[J]. 中国管理科学, 2023, 31(7): 50-59. |

| [8] | 王虎, 李守伟, 马瑜寅, 刘晓星. 基于共同持股网络的基金系统性风险研究[J]. 中国管理科学, 2023, 31(6): 82-90. |

| [9] | 欧阳资生, 杨希特, 黄颖. 嵌入网络舆情指数的中国金融机构系统性风险传染效应研究[J]. 中国管理科学, 2022, 30(4): 1-12. |

| [10] | 刘志东, 张培元, 荆中博. 跨行业风险溢出冲击下我国银行业系统性风险研究[J]. 中国管理科学, 2022, 30(12): 1-12. |

| [11] | 张飞鹏, 徐一雄, 邹胜轩, 陈艳. 基于LGCNET多层网络的中国A股上市公司系统性风险度量[J]. 中国管理科学, 2022, 30(12): 13-25. |

| [12] | 赵林海, 陈名智. 金融机构系统性风险溢出和系统性风险贡献——基于滚动窗口动态Copula模型双时变相依视角[J]. 中国管理科学, 2021, 29(7): 71-83. |

| [13] | 高倩倩, 范宏. 基于银行-资产双边网络模型的系统性风险及投资策略研究[J]. 中国管理科学, 2021, 29(7): 1-12. |

| [14] | 王耀东, 冯燕, 周桦. 保险业在金融系统性风险传染路径中起到“媒介”作用吗?——基于金融市场尾部风险传染路径的实证分析[J]. 中国管理科学, 2021, 29(5): 14-24. |

| [15] | 马钱挺, 杨文珂, 何建敏. 基于多层网络的银企系统性风险研究[J]. 中国管理科学, 2021, 29(12): 1-14. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||