主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2026, Vol. 34 ›› Issue (3): 1-14.doi: 10.16381/j.cnki.issn1003-207x.2024.0826cstr: 32146.14.j.cnki.issn1003-207x.2024.0826

• • 下一篇

俞乃畅, 程康, 李心丹, 杨学伟( )

)

收稿日期:2024-05-24

修回日期:2024-09-12

出版日期:2026-03-25

发布日期:2026-03-06

通讯作者:

杨学伟

E-mail:xwyang@nju.edu.cn

基金资助:

Naichang Yu, Kang Cheng, Xindan Li, Xuewei Yang()

Received:2024-05-24

Revised:2024-09-12

Online:2026-03-25

Published:2026-03-06

Contact:

Xuewei Yang

E-mail:xwyang@nju.edu.cn

摘要:

现有关于中国权证市场的研究主要关注二级市场价格泡沫及其形成机制,忽视了关于“权证作为股权分置改革对价支付工具”的探讨:权证是否实现了补偿流通股股东潜在损失的功能?本文使用公开市场数据和私有脱敏账户数据,分析流通股股东的财富在股权分置改革前后的变化。基于公开市场数据的研究结果表明,股权分置改革后,28家公司的个股复权价格较股权分置改革公告前平均增长超过10%。基于账户数据的分析表明,获得权证对价的流通股股东,特别是在股权分置改革首次公告日之前持有股票的流通股股东,绝大多数(约90%)收益为正。总体来看,权证一级市场实现了保护流通股股东利益的功能。但由于不完备的二级市场交易机制和投资者适当性管理制度,权证上市交易后被投资者炒作并出现了投机泡沫,对投资者财富和市场稳定性造成了不利影响。本研究证实了金融衍生品在公司治理中可能产生的积极作用,有助于正确、全面地认识金融衍生品市场,助力其更好地服务实体经济高质量发展。

中图分类号:

俞乃畅,程康,李心丹, 等. 权证实现了股权分置改革对价支付功能吗?[J]. 中国管理科学, 2026, 34(3): 1-14.

Naichang Yu,Kang Cheng,Xindan Li, et al. Do Warrants Fulfill the Role of Consideration Payment in China's Split-Share Structure Reform? Analysis Based on Proprietary Brokerage Data[J]. Chinese Journal of Management Science, 2026, 34(3): 1-14.

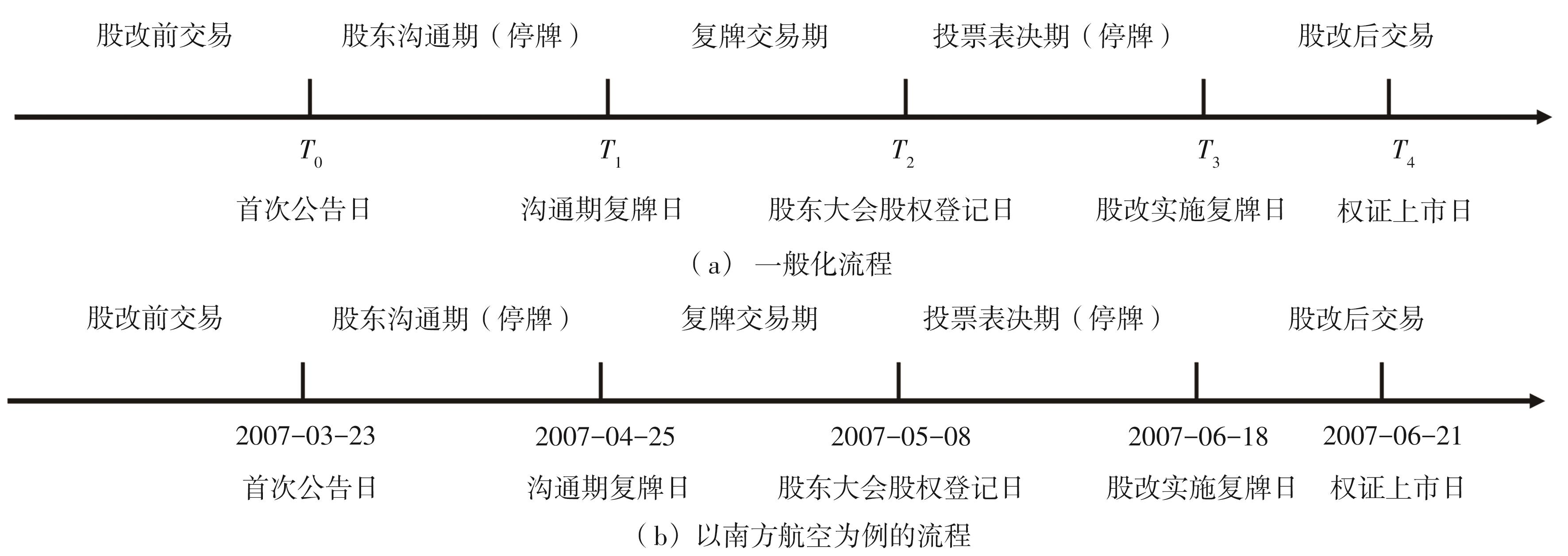

图1

上市公司股权分置改革流程"

图2

南方航空股改事件前后的价格走势"

表1

以权证为对价工具的28家上市公司的股改关键时点信息与价格变化情况"

股票 代码 | 股票 简称 | 差值 | t值 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 000001 | 深发展 | 070511 | 070525 | 070531 | 070620 | 070629 | 5 | 23.00 | 34.89 | 11.89 | 13.91 |

| 000002 | 万科 | 051010 | 051020 | 051104 | 051202 | 051205 | 12 | 3.71 | 4.72 | 1.01 | 16.84 |

| 000027 | 深能源 | 060220 | 060403 | 060407 | 060426 | 060427 | 5 | 7.29 | 9.50 | 2.21 | 16.84 |

| 000039 | 中集集团 | 060313 | 060413 | 060421 | 060524 | 060525 | 7 | 9.33 | 15.56 | 6.23 | 35.34 |

| 000069 | 华侨城 | 051121 | 051205 | 051216 | 060106 | 061124 | 10 | 10.48 | 17.29 | 6.81 | 55.65 |

| 000423 | 东阿阿胶 | 061204 | 070509 | 070515 | 070601 | 080718 | 5 | 11.75 | 45.81 | 34.07 | 68.04 |

| 000629 | 新钢钒 | 050926 | 051012 | 051018 | 051107 | 051205 | 5 | 5.27 | 5.34 | 0.08 | 1.50 |

| 000792 | 盐湖钾肥 | 060410 | 060515 | 060522 | 060629 | 060630 | 6 | 14.95 | 23.74 | 8.80 | 24.57 |

| 000858 | 五粮液 | 060213 | 060302 | 060314 | 060331 | 060403 | 9 | 7.76 | 11.05 | 3.29 | 10.29 |

| 000898 | 鞍钢 | 051017 | 051031 | 051111 | 051202 | 051205 | 10 | 4.29 | 5.28 | 1.00 | 18.01 |

| 000932 | 华菱管线 | 051205 | 051215 | 060120 | 060301 | 060302 | 25 | 4.58 | 4.66 | 0.08 | 3.25 |

| 600001 | 邯郸钢铁 | 060123 | 060210 | 060317 | 060405 | 060407 | 26 | 3.32 | 3.92 | 0.60 | 9.26 |

| 600004 | 白云机场 | 051024 | 051104 | 051111 | 051220 | 051223 | 6 | 7.68 | 9.19 | 1.51 | 16.94 |

| 600005 | 武钢 | 050926 | 051018 | 051028 | 051121 | 051123 | 9 | 3.64 | 4.00 | 0.36 | 6.97 |

| 600008 | 首创 | 060227 | 060330 | 060331 | 060419 | 060424 | 2 | 6.08 | 6.65 | 0.57 | 3.51 |

| 600009 | 上海机场 | 060109 | 060124 | 060207 | 060302 | 060307 | 4 | 14.11 | 15.58 | 1.47 | 7.43 |

| 600010 | 包钢 | 060123 | 060213 | 060309 | 060328 | 060331 | 19 | 2.36 | 2.88 | 0.52 | 11.14 |

| 600019 | 宝钢 | 050620 | 050629 | 050722 | 050818 | 050822 | 18 | 4.77 | 5.64 | 0.86 | 21.29 |

| 600029 | 南方航空 | 070323 | 070425 | 070508 | 070618 | 070621 | 5 | 6.09 | 10.92 | 4.83 | 23.83 |

| 600036 | 招商银行 | 051219 | 060104 | 060111 | 060227 | 060302 | 6 | 6.46 | 8.24 | 1.78 | 29.29 |

| 600177 | 雅戈尔 | 060220 | 060306 | 060310 | 060516 | 060522 | 5 | 3.86 | 7.62 | 3.76 | 23.82 |

| 600309 | 烟台万华 | 060227 | 060329 | 060331 | 060424 | 060427 | 3 | 14.19 | 26.05 | 11.86 | 15.04 |

| 600519 | 贵州茅台 | 060308 | 060417 | 060425 | 060525 | 060530 | 7 | 52.00 | 111.48 | 59.48 | 26.13 |

| 600649 | 原水 | 060213 | 060223 | 060301 | 060414 | 060419 | 5 | 5.67 | 6.50 | 0.82 | 5.34 |

| 600690 | 青岛海尔 | 060227 | 060309 | 060331 | 060517 | 060522 | 17 | 4.36 | 6.11 | 1.75 | 21.27 |

| 600795 | 国电电力 | 060717 | 060731 | 060803 | 060831 | 060905 | 4 | 7.84 | 6.82 | -1.02 | -20.91 |

| 600887 | 伊利 | 060220 | 060309 | 060310 | 060424 | 061115 | 2 | 16.99 | 25.65 | 8.67 | 20.96 |

| 600900 | 长江电力 | 050620 | 050705 | 050721 | 050815 | 060525 | 13 | 7.82 | 10.27 | 2.45 | 34.00 |

表2

财富增值指标的描述性统计"

| 事件日 | 股改实施复牌日 | 权证上市日 | 股改实施复牌日 | 权证上市日 | ||||

|---|---|---|---|---|---|---|---|---|

| 平均值 | 13.97** | 10.29** | 16.65*** | 14.75*** | 19.57*** | 15.07*** | 22.38*** | 20.05*** |

| 中位数 | 11.54*** | 10.28** | 12.28*** | 12.28*** | 15.90*** | 15.09*** | 16.46*** | 16.46*** |

| 最大值 | 113.34 | 58.34 | 86.17 | 63.91 | 141.06 | 60.79 | 107.34 | 95.23 |

| 最小值 | -24.91 | -24.91 | -28.87 | -21.13 | -23.31 | -23.31 | -25.83 | -19.40 |

| 标准差 | 27.17 | 19.31 | 27.97 | 22.74 | 31.78 | 21.45 | 32.34 | 26.81 |

| 大于0比重 | 64.3 | 63.0 | 67.9 | 70.8 | 71.4 | 70.4 | 75.0 | 75.0 |

| 观测数目 | 28 | 27 | 28 | 24 | 28 | 27 | 28 | 24 |

表3

超额收益和累计超额收益的描述性统计 (%)"

| 股改宣告 | -5 | -4 | -3 | -2 | -1 | 0 | +1 |

|---|---|---|---|---|---|---|---|

| -0.57 | 0.04 | 1.17*** | 1.00** | 1.56*** | 4.00*** | 0.92 | |

| (-1.54) | (0.09) | (3.75) | (2.13) | (3.06) | (4.91) | (1.23) | |

| -0.57 | -0.53 | 0.65 | 1.65* | 3.21*** | 7.21*** | 8.12*** | |

| (-1.54) | (-0.87) | (1.01) | (1.85) | (3.36) | (6.46) | (5.54) | |

| — | — | — | — | — | 4.47*** | 5.39*** | |

| — | — | — | — | — | (3.43) | (3.82) | |

| 股改实施 | -2 | -1 | 0 | +1 | +2 | +3 | +4 |

| 0.39 | 0.95** | 15.87*** | 2.15** | 0.22 | 2.22** | 1.80 | |

| (1.00) | (2.65) | (2.95) | (2.21) | (0.33) | (2.28) | (1.61) | |

| 0.39 | 1.35*** | 17.21*** | 19.37*** | 19.59*** | 21.81*** | 23.60*** | |

| (1.00) | (3.08) | (3.14) | (3.64) | (3.46) | (3.63) | (3.67) | |

| — | — | 10.65** | 12.80** | 13.02** | 15.15** | 16.87*** | |

| — | — | (2.11) | (2.59) | (2.46) | (2.72) | (2.90) | |

| 权证上市 | -2 | -1 | 0 | +1 | +2 | +3 | +4 |

| 0.69 | 1.86 | 4.69*** | 1.20 | 0.09 | -0.39 | -0.56 | |

| (0.56) | (1.60) | (3.81) | (1.35) | (0.14) | (-0.56) | (-1.31) | |

| 0.69 | 2.55 | 7.23*** | 8.44*** | 8.53*** | 8.14*** | 7.58*** | |

| (0.56) | (1.56) | (3.36) | (3.31) | (3.37) | (3.27) | (3.29) |

表4

权证相关的描述性统计"

| 权证代码 | 031003 | 031004 | 031007 | 580989 |

|---|---|---|---|---|

| 权证简称 | 深发SFC1 | 深发 SFC2 | 阿胶 EJC1 | 南航JTP1 |

| 标的简称 | 深发展 | 深发展 | 东阿阿胶 | 南方航空 |

| 上市日期 | 2007-06-29 | 2007-06-29 | 2008-07-18 | 2007-06-21 |

| 权证类型 | 认购权证 | 认购权证 | 认购权证 | 认沽权证 |

| 观测数目 | 3144 | 3144 | 1110 | 2232 |

| 单次交易清仓比例 | 76.8 | 82.7 | 62.6 | 57.2 |

| 平均持仓天数 | 50 | 76 | 85 | 63 |

| 中位数持仓天数 | 20 | 11 | 7 | 7 |

表5

流通股股东的毛利润率(%)情况"

| 股票代码 | 000001 | 000423 | 600029 | 000001 | 000423 | 600029 |

|---|---|---|---|---|---|---|

| 股票简称 | 深发展 | 东阿阿胶 | 南方航空 | 深发展 | 东阿阿胶 | 南方航空 |

| 股票参考买入价格 | 首次公告日收盘价 | 区间加权平均收盘价 | ||||

| 股票利润率大于0比重 | 60.4 | 96.0 | 98.1 | 55.3 | 4.8 | 94.7 |

| 股票利润率均值 | 11.8*** | 40.9*** | 41.1*** | 10.3*** | -28.6*** | 37.3*** |

| 股票利润率中位数 | 7.4*** | 49.6*** | 23.1*** | 3.5*** | -28.2*** | 21.0*** |

| 权证利润率大于0比重 | 99.6 | 98.9 | 98.5 | 98.5 | 96.5 | 98.2 |

| 权证利润率均值 | 10.2*** | 25.6*** | 29.8*** | 10.1*** | 13.0*** | 28.5*** |

| 权证利润率中位数 | 10.3*** | 27.4*** | 39.3*** | 9.5*** | 13.3*** | 36.7*** |

| 总体利润率大于0比重 | 89.3 | 98.5 | 98.2 | 68.1 | 5.2 | 97.9 |

| 总体利润率均值 | 22.0*** | 66.5*** | 70.9*** | 20.3*** | -15.7*** | 65.7*** |

| 总体利润率中位数 | 17.2*** | 77.3*** | 64.3*** | 14.2*** | -14.7*** | 58.0*** |

| 调整利润率大于0比重 | 89.1 | 99.1 | 97.8 | 65.7 | 8.2 | 97.1 |

| 调整利润率均值 | 16.7*** | 73.8*** | 71.1*** | 15.1*** | -8.4** | 65.9*** |

| 调整利润率中位数 | 13.6*** | 82.1*** | 67.6*** | 16.1*** | -9.4*** | 61.4*** |

表6

不同类型流通股股东的数目"

| 股票代码 | 000001 | 000423 | 600029 |

|---|---|---|---|

| 股票简称 | 深发展 | 东阿阿胶 | 南方航空 |

| 流通股股东数目 | 3144 | 1110 | 2232 |

| 第一类原有股东数目 | 1483 | 92 | 1712 |

| 第二类原有股东数目 | 1085 | 34 | 1544 |

| 第一类新进股东数目 | 1386 | 450 | 482 |

| 第二类新进股东数目 | 472 | 213 | 266 |

表7

不同类型流通股股东的毛利润率(%)情况"

| 股票代码 | 000001 | 000423 | 600029 | 000001 | 000423 | 600029 |

|---|---|---|---|---|---|---|

| 股票简称 | 深发展 | 东阿阿胶 | 南方航空 | 深发展 | 东阿阿胶 | 南方航空 |

| 股票参考买入价格 | 第二类原有股东 | 第二类新进股东 | ||||

| 股票利润率大于0比重 | 82.5 | 90.0 | 98.5 | 19.7 | 0.0 | 51.7 |

| 股票利润率均值 | 28.0*** | 74.4*** | 47.6*** | -8.4*** | -24.5*** | 1.1** |

| 股票利润率中位数 | 25.1*** | 86.5*** | 23.3*** | -9.4*** | -24.8*** | 0.8** |

| 权证利润率大于0比重 | 99.5 | 100.0 | 98.5 | 98.9 | 98.6 | 98.1 |

| 权证利润率均值 | 11.1*** | 30.0*** | 27.3*** | 8.6*** | 13.7*** | 27.4*** |

| 权证利润率中位数 | 11.3*** | 33.1*** | 37.8*** | 8.3*** | 14.5*** | 32.3*** |

| 总体利润率大于0比重 | 88.5 | 90.0 | 98.4 | 43.4 | 0.5 | 97.0 |

| 总体利润率均值 | 39.0*** | 104.4*** | 74.8*** | 0.2 | -10.8*** | 28.5*** |

| 总体利润率中位数 | 36.2*** | 120.6*** | 63.9*** | -1.6* | -10.4*** | 32.0*** |

| 调整利润率大于0比重 | 89.5 | 90.0 | 91.2 | 50.8 | 10.3 | 94.7 |

| 调整利润率均值 | 17.1*** | 39.6*** | 40.9*** | -1.0 | -5.7*** | 29.6*** |

| 调整利润率中位数 | 12.3*** | 53.4*** | 35.0*** | 0.1 | -6.3*** | 35.3*** |

| [1] | 李佳岚, 万迪昉, 陈楠. 交易所治理结构、所有者背景和衍生品创新[J]. 中国管理科学, 2022, 30(11): 31-41. |

| Li J L, Wan D F, Chen N. Governance structure, ownership background and derivatives innovation of exchanges[J]. Chinese Journal of Management Science, 2022, 30(11): 31-41. | |

| [2] | Hu G X, Wang J. A review of China’s financial markets[J]. Annual Review of Financial Economics, 2022, 14: 465-507. |

| [3] | Xiong W, Yu J. The Chinese warrants bubble[J]. American Economic Review, 2011, 101(6): 2723-2753. |

| [4] | Jiang F, Kim K A. Corporate governance in China: A survey[J]. Review of Finance, 2020, 24(4): 733-772. |

| [5] | 攀登, 施东晖, 宋铮. 证券市场泡沫的生成机理分析——基于宝钢权证自然实验的实证研究[J]. 管理世界, 2008, 24(4): 15-23+186. |

| Pan D, Shi D H, Song Z. An analysis—Based on the case study on the “natural experiment” on the warrant of Shanghai Baoshan steel group—of the generative mechanism of the foam of securities markets[J]. Journal of Management World, 2008, 24(4): 15-23+186. | |

| [6] | 边江泽, 宿铁. “T+1”交易制度和中国权证市场溢价[J]. 金融研究, 2010(6): 143-161. |

| Bian J Z, Su T. The “T+1” trading rule and the Chinese warrant market overprice[J]. Journal of Financial Research, 2010(6): 143-161. | |

| [7] | 王茵田, 朱英姿, 章真. 投资者是非理性的吗——卖空限制下我国权证价格偏离探析[J]. 金融研究, 2012(1): 194-206. |

| Wang Y T, Zhu Y Z, Zhang Z. Are investors rational or irrational?—Warrant pricing and bubbles under short-sale constraints in China[J]. Journal of Financial Research, 2012(1): 194-206. | |

| [8] | 张伟强, 廖理, 沈红波. 中国认购权证市场泡沫形成机制研究[J]. 中国工业经济, 2013(1): 90-102. |

| Zhang W Q, Liao L, Shen H B. An empirical research on the formation mechanism of China’s call warrants bubble[J]. China Industrial Economics, 2013(1): 90-102. | |

| [9] | 马文杰, 路磊. 认沽权证系统性高估机理: 投机还是创设机制?[J]. 管理科学学报, 2016, 19(5): 68-86. |

| Ma W J, Lu L. Systematic overvaluation mechanism of put warrants: Speculation or issuing mechanism?[J]. Journal of Management Sciences in China, 2016, 19(5): 68-86. | |

| [10] | Gong B, Pan D, Shi D. New investors and bubbles: An analysis of the baosteel call warrant bubble[J]. Management Science, 2017, 63(8): 2493-2508. |

| [11] | Cai J, He J, Jiang W, et al. The whack-a-mole game: Tobin taxes and trading frenzy[J]. The Review of Financial Studies, 2021, 34(12): 5723-5755. |

| [12] | Pearson N D, Yang Z, Zhang Q. The Chinese warrants bubble: Evidence from brokerage account records[J]. The Review of Financial Studies, 2021, 34(1): 264-312. |

| [13] | Wang Y, Zhou G, Zhu Y. The Chinese warrant bubble: A fundamental analysis[J]. Journal of Futures Markets, 2021, 41(1): 3-26. |

| [14] | Bian J, Su T, Wang J. Non-marketability and one-day selling lockup[J]. Journal of Empirical Finance, 2022, 65: 1-23. |

| [15] | Li X, Subrahmanyam A, Yang X. Winners, losers, and regulators in a derivatives market bubble[J]. The Review of Financial Studies, 2021, 34(1): 313-350. |

| [16] | 曹沅岚, 朱鹏, 杨学伟. 中国资本市场机制设计与评估[J]. 中国科学基金, 2023, 37(6): 933-943. |

| Cao Y L, Zhu P, Yang X W. Design and evaluation of China’s capital market mechanisms[J]. Bulletin of National Natural Science Foundation of China, 2023, 37(6): 933-943. | |

| [17] | 张爱玲, 吴冲锋. 权证发行对标的资产交易行为的影响研究[J]. 管理工程学报, 2008, 22(4): 137-139+145. |

| Zhang A L, Wu C F. Impact of warrant introduction on trade behavior of underlying stocks[J]. Journal of Industrial Engineering and Engineering Management, 2008, 22(4): 137-139+145. | |

| [18] | 胡志鹏. 权证上市对标的股票的影响——基于中国股市的分析与实证[J]. 金融研究, 2008(1): 100-118. |

| Hu Z P. The effectiveness of warrant issuance on the underlying stock[J]. Journal of Financial Research, 2008(1): 100-118. | |

| [19] | 鲁炜, 卢宝. 权证发行上市与到期效应实证研究[J]. 管理学报, 2009, 6(7): 978-980+987. |

| Lu W, Lu B. An empirical analysis of the impact of warrants introduction and expiration[J]. Chinese Journal of Management, 2009, 6(7): 978-980+987. | |

| [20] | 周海林, 吴鑫育, 丁忠明, 等. 权证是冗余证券吗? 基于沪深交易所的经验证据[J]. 系统工程理论与实践, 2013, 33(7): 1699-1708. |

| Zhou H L, Wu X Y, Ding Z M, et al. Are warrants redundant securities? An empirical evidence from Shanghai and Shenzhen stock exchanges[J]. Systems Engineering-Theory & Practice, 2013, 33(7): 1699-1708. | |

| [21] | 张伟强, 王珺, 廖理. 中国个人权证投资者处置效应研究[J]. 清华大学学报(哲学社会科学版), 2011, 26(4): 112-122+160. |

| Zhang W Q, Wang J, Liao L. The dispersion effect in Chinese individual investors’ option trading[J]. Journal of Tsinghua University (Philosophy and Social Sciences), 2011, 26(4): 112-122+160. | |

| [22] | Liu Y J, Zhang Z, Zhao L. Speculation spillovers[J]. Management Science, 2015, 61(3): 649-664. |

| [23] | Tan L, Zhang X, Zhang X. Retail and institutional investor trading behaviors: Evidence from China[J]. Annual Review of Financial Economics, 2024, 16: 459-483. |

| [24] | 刘慕涵, 熊熊. 股指期货交易政策、投资者行为与市场质量[J]. 中国管理科学, 2023, 31(7): 126-139. |

| Liu M H, Xiong X. Stock index futures trading policy, investors’behavior and stock market quality[J]. Chinese Journal of Management Science, 2023, 31(7): 126-139. | |

| [25] | Subrahmanyam A, Tang K, Wang J, et al. Leverage is a double-edged sword[J]. The Journal of Finance, 2024, 79(2): 1579-1634. |

| [26] | Jones C M, Shi D, Zhang X, et al. Retail trading and return predictability in China[J]. Journal of Financial and Quantitative Analysis, 2025, 60(1): 68-104. |

| [27] | 何朝林, 张棋翔, 曹旺栋. 基于异质价格信念的金融资产泡沫形成机制[J]. 中国管理科学, 2022, 30(12): 162-172. |

| He C L, Zhang Q X, Cao W D. The forming mechanism of financial asset bubble based on the heterogeneous price beliefs[J]. Chinese Journal of Management Science, 2022, 30(12): 162-172. | |

| [28] | 朱莉, 刘向丽, 杨晓光. 投资者情绪影响股指期现货市场的价格动态关系吗?[J]. 中国管理科学, 2022, 30(4): 52-62. |

| Zhu L, Liu X L, Yang X G. Does investor sentiment affect the price dynamic relationship of stock index futures-spot market?[J]. Chinese Journal of Management Science, 2022, 30(4): 52-62. | |

| [29] | 寇红红, 柴建, 郑嘉俐, 等. 上海原油期货市场是否具有稳定中国股票市场的作用?[J]. 中国管理科学, 2022, 30(11): 20-30. |

| Kou H H, Chai J, Zheng J L, et al. Does the Shanghai crude oil futures market have a role in stabilizing China’s stock market?[J]. Chinese Journal of Management Science, 2022, 30(11): 20-30. | |

| [30] | Liao L, Liu B, Wang H. China׳s secondary privatization: Perspectives from the split-share structure reform[J]. Journal of Financial Economics, 2014, 113(3): 500-518. |

| [31] | 施新政, 高文静, 陆瑶, 等. 资本市场配置效率与劳动收入份额——来自股权分置改革的证据[J]. 经济研究, 2019, 54(12): 21-37. |

| Shi X Z, Gao W J, Lu Y, et al. Efficient resource allocation and labor income share: Evidence from the split-share structure reform[J]. Economic Research Journal, 2019, 54(12): 21-37. | |

| [32] | Liu J, Wang Z, Zhu W. Does privatization reform alleviate ownership discrimination? Evidence from the Split-share structure reform in China[J]. Journal of Corporate Finance, 2021, 66: 101848. |

| [33] | 吴德胜, 吕斐适, 于善辉. 流通股股东在股权分置改革中是否获得了财富增值?[J]. 南开经济研究, 2008(2): 126-143. |

| Wu D S, Lü F S, Yu S H. Do floating Shareholders have wealth premium in the process of equity separation reform in China?[J]. Nankai Economic Studies, 2008(2): 126-143. | |

| [34] | 张伟强, 王珺, 廖理. 股权分置改革中的“实惠效应”与“未来效应”[J]. 中国工业经济, 2008(11): 98-107. |

| Zhang W Q, Wang J, Liao L. Announcement effects and execution effects in nontradable shares reform[J]. China Industrial Economics, 2008(11): 98-107. | |

| [35] | 廖理, 沈红波. Fama-French三因子模型与股权分置改革效应研究[J]. 数量经济技术经济研究, 2008, 25(9): 117-125. |

| Liao L, Shen H B. Fama-French three factors model and the effect of the split-share structure reform[J]. The Journal of Quantitative & Technical Economics, 2008, 25(9): 117-125. | |

| [36] | 袁显平, 柯大钢. 事件研究方法及其在金融经济研究中的应用[J]. 统计研究, 2006, 23(10): 31-35. |

| Yuan X P, Ke D G. Event study method and its application to financial economic study[J]. Statistical Research, 2006, 23(10): 31-35. | |

| [37] | 邹文理, 王曦, 谢小平. 中央银行沟通的金融市场响应——基于股票市场的事件研究[J]. 金融研究, 2020(2): 34-50. |

| Zou W L, Wang X, Xie X P. Financial market response to central bank communication: Event study on stock market[J]. Journal of Financial Research, 2020(2): 34-50. | |

| [38] | 余军. 机构投资者的投票权与流通股东的利益实现——来自股改事件的经验证据[J]. 山西财经大学学报, 2010, 32(12): 88-96. |

| Yu J. Vote control of institutional investors and interests realization of tradable-share holders-An empirical evidence from Chinese splitting-share reform[J]. Journal of Shanxi University of Finance and Economics, 2010, 32(12): 88-96. | |

| [39] | 陈其安, 沈猛, 张红真. 股权分置改革过程中非流通股股东对流通股股东的利益侵占行为研究[J]. 中国管理科学, 2016, 24(S1): 461-469. |

| Chen Q A, Shen M, Zhang H Z. Study on behaviors of non-tradable shareholders expropriating tradable shareholders’ interest in the process of split-share structure reform of Chinese stock market[J]. Chinese Journal of Management Science, 2016, 24(S1): 461-469. | |

| [40] | Chan K C, Jiang X, Wu D, et al. When is the client king? evidence from affiliated-analyst recommendations in China’s split-share reform[J]. Contemporary Accounting Research, 2020, 37(2): 1044-1072. |

| [41] | Subrahmanyam M G, Tang D Y, Wang S Q. Does the tail wag the dog? The effect of credit default swaps on credit risk[J]. The Review of Financial Studies, 2014, 27(10): 2927-2960. |

| [42] | Purnanandam A, Weagley D. Can markets discipline government agencies?Evidence from the weather derivatives market[J]. The Journal of Finance, 2016, 71(1): 303-334. |

| [43] | 肖万, 张宇彤, 许林. 期权属性、公司治理与可转债发行[J]. 南开管理评论, 2020, 23(2): 142-154. |

| Xiao W, Zhang Y T, Xu L. Option, corporate governance and convertible bonds issuance[J]. Nankai Business Review, 2020, 23(2): 142-154. |

| [1] | 邹高峰, 李广群, 熊熊, 崔博洋. 中小股东网络表达对企业金融化的影响[J]. 中国管理科学, 2026, 34(3): 15-24. |

| [2] | 吴勇, 李倩, 朱卫东. 董事责任保险能否提升公司价值?——基于公司治理视角的研究[J]. 中国管理科学, 2018, 26(4): 188-196. |

| [3] | 赵国强, 徐晓辉, 蒲勇健. 授权决策的期权特征与模型解析[J]. 中国管理科学, 2015, 23(8): 54-62. |

| [4] | 曾江洪, 崔晓云. 基于演化博弈模型的企业集团母子公司治理研究[J]. 中国管理科学, 2015, 23(2): 148-153. |

| [5] | 孟庆春, 张江华, 赵炳新. 产权结构、公司治理、社会保障与国企改革——基于Cournot竞争的系统分析[J]. 中国管理科学, 2010, 18(6): 138-139. |

| [6] | 余劲松, 陈其安. 立法导向、投资者诉讼与上市公司治理水平改善[J]. 中国管理科学, 2009, 17(2): 176-184. |

| [7] | 王雪荣, 董威. 中国上市公司机构投资者对公司绩效影响的实证分析[J]. 中国管理科学, 2009, 17(2): 15-20. |

| [8] | 党文娟, 张宗益, 吴俊. 基于博弈论的均衡股权结构治理模型研究[J]. 中国管理科学, 2008, 16(3): 164-172. |

| [9] | 周刚, 姜彦福, 雷家骕, 傅家骥. 战略性大股东的公司治理[J]. 中国管理科学, 2002, (2): 76-78. |

| [10] | 向锐, 曹国华, 杨秀苔. 公司治理的政府介入结构分析[J]. 中国管理科学, 2001, (2): 65-70. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||