主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2023, Vol. 31 ›› Issue (8): 1-8.doi: 10.16381/j.cnki.issn1003-207x.2020.0981

王江涛( ),蔡雅,郑承利

),蔡雅,郑承利

Jiang-tao WANG(),Ya CAI,Cheng-li ZHENG

摘要:

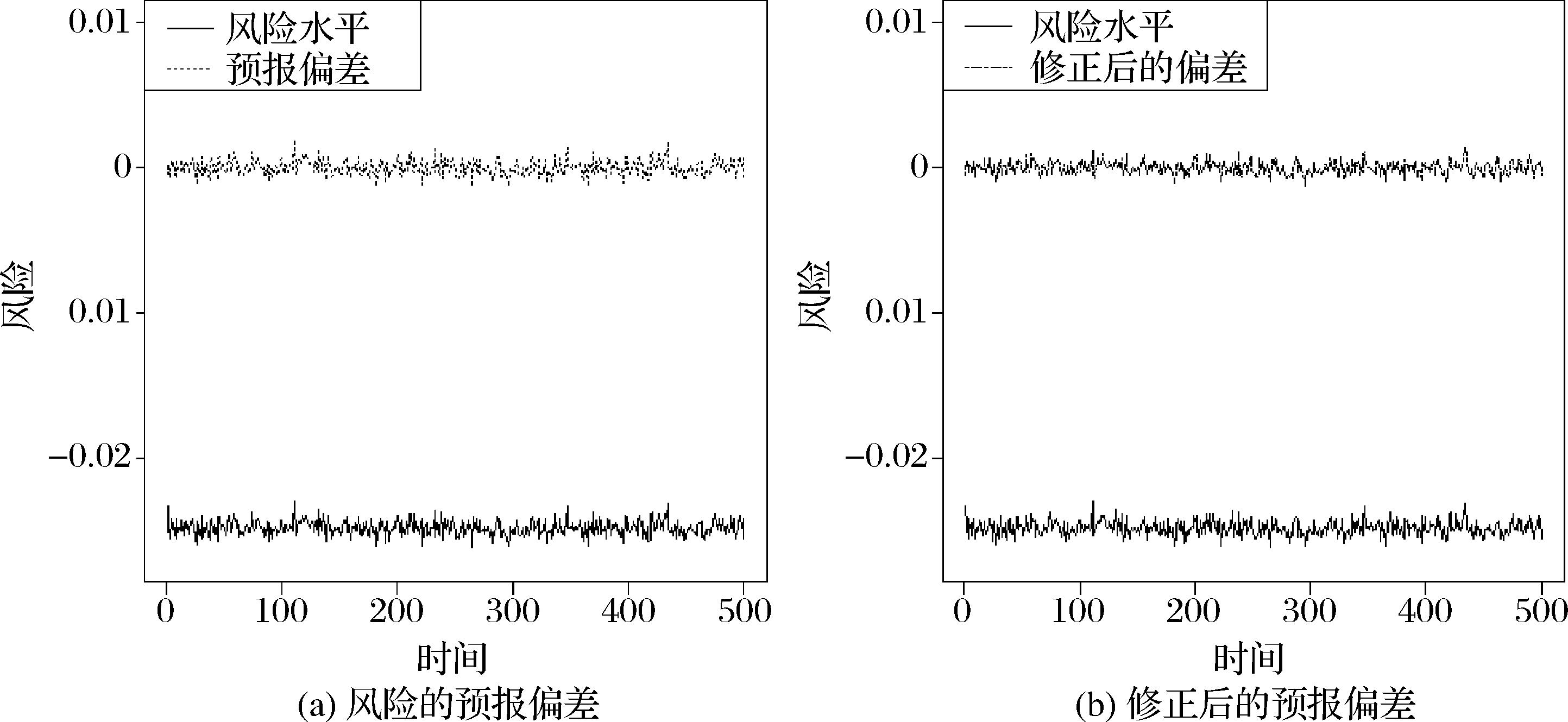

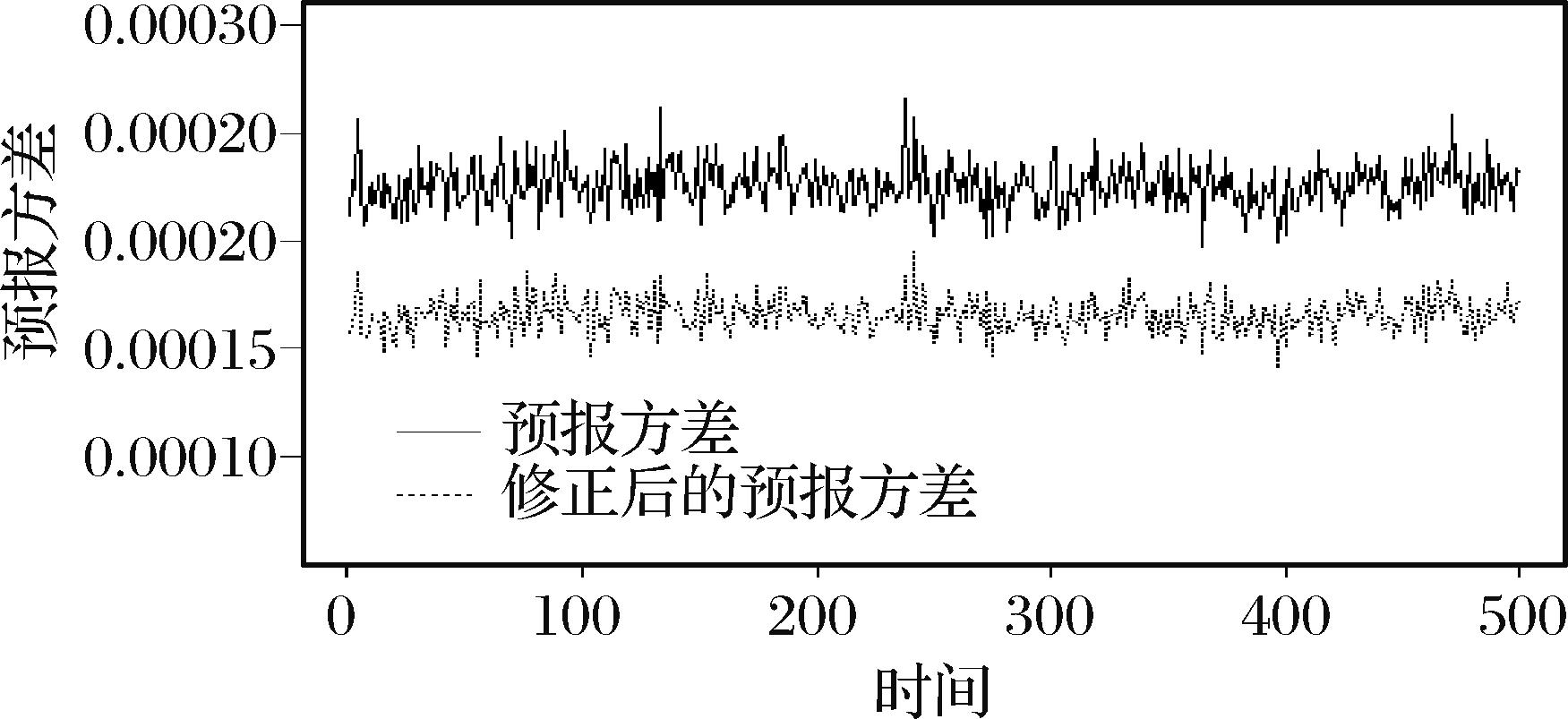

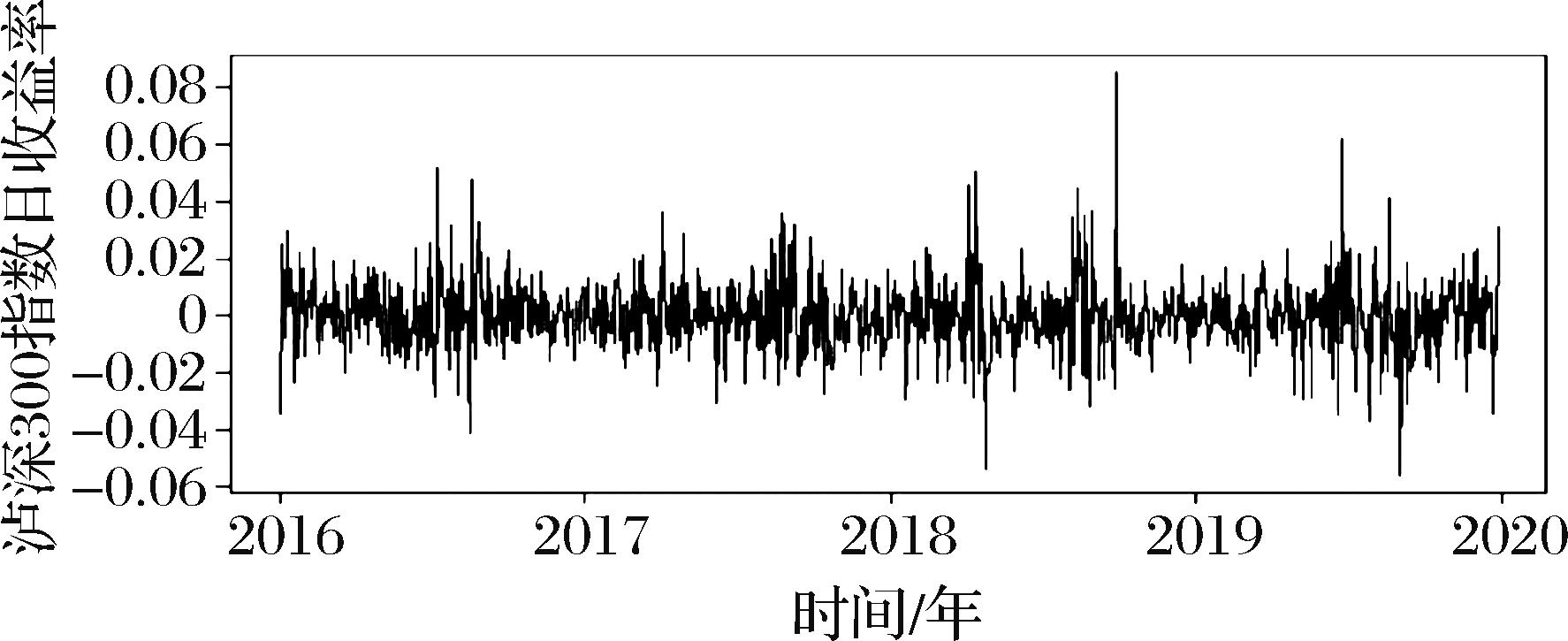

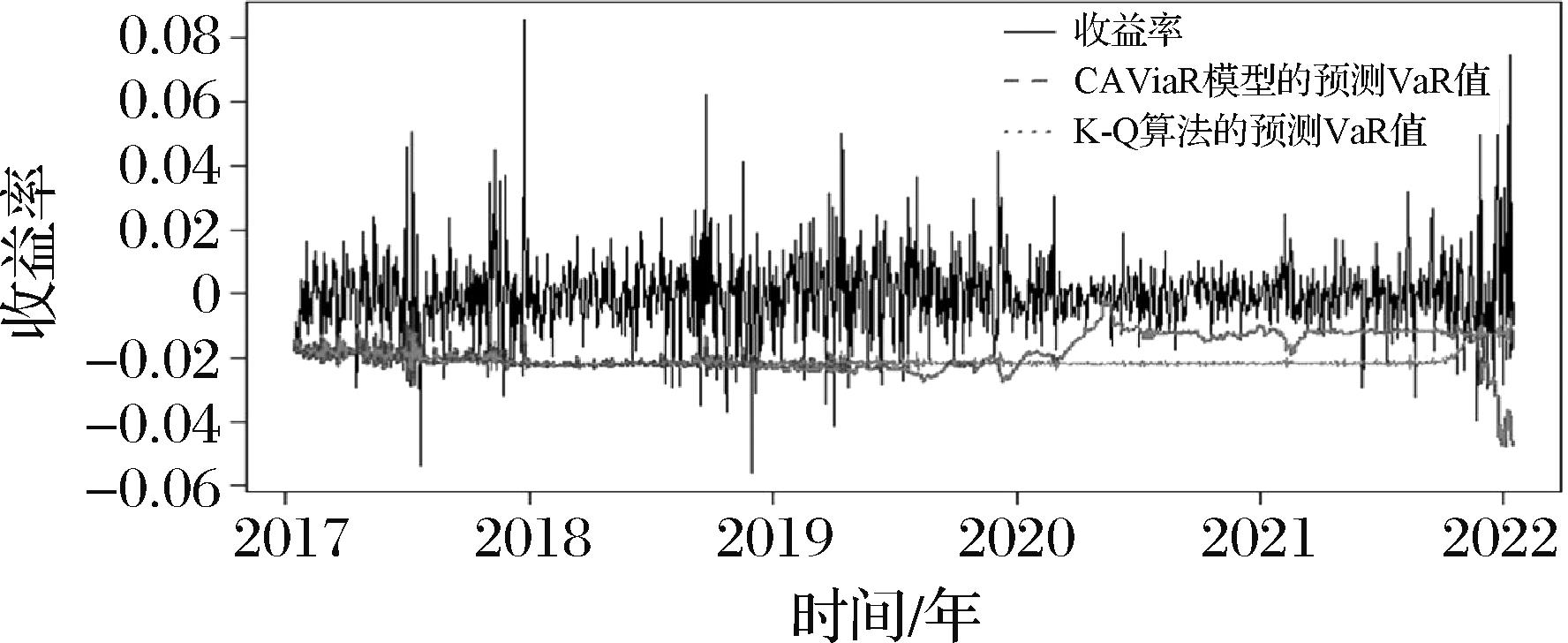

本文在充分利用交易信息的基础上,用离散随机过程刻画风险的演变,构建了一类分位数框架下的状态-空间模型来度量和预报风险。为了克服参数估计的困难,使模型具有实用价值,仿照传统卡尔曼滤波的思想,依据模型的设定,本文重构了分位数框架下的增益系数和修正过程,设计了一类新的风险预测算法。该算法的主要优势是,能依据观测数据的更新,自适应地修正已有的预测结果,并利用修正后的结果进行预测分析,从而降低连续预测过程中的误差积累,提高风险预测的准确性。文中理论结果和实证结论都证实了这一点。算法的理论分析及其模拟检验表明,修正之后的结果仍然具有无偏性,但方差却显著降低了。因此基于修正后的数值,再做下一步预测,必将减少整个风险预测过程中的误差积累。实际数据的应用结果显示,相比现有的风险预测方法,文中提出的算法能更加准确地预测出风险大小,而且这种预测优势在极端水平下更加明显。算法的提出既丰富了风险预测的手段,又为恰当规避风险,特别是极端风险,提供技术参考。

中图分类号: