主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2024, Vol. 32 ›› Issue (11): 53-64.doi: 10.16381/j.cnki.issn1003-207x.2022.2261

Previous Articles Next Articles

Qifa Xu1,2, Zezhou Wang1, Cuixia Jiang1( )

)

Received:2022-10-16

Revised:2022-12-26

Online:2024-11-25

Published:2024-12-09

Contact:

Cuixia Jiang

CLC Number:

Qifa Xu,Zezhou Wang,Cuixia Jiang. Research on Mixed Frequency Asset Pricing Based on Generative Adversarial Network[J]. Chinese Journal of Management Science, 2024, 32(11): 53-64.

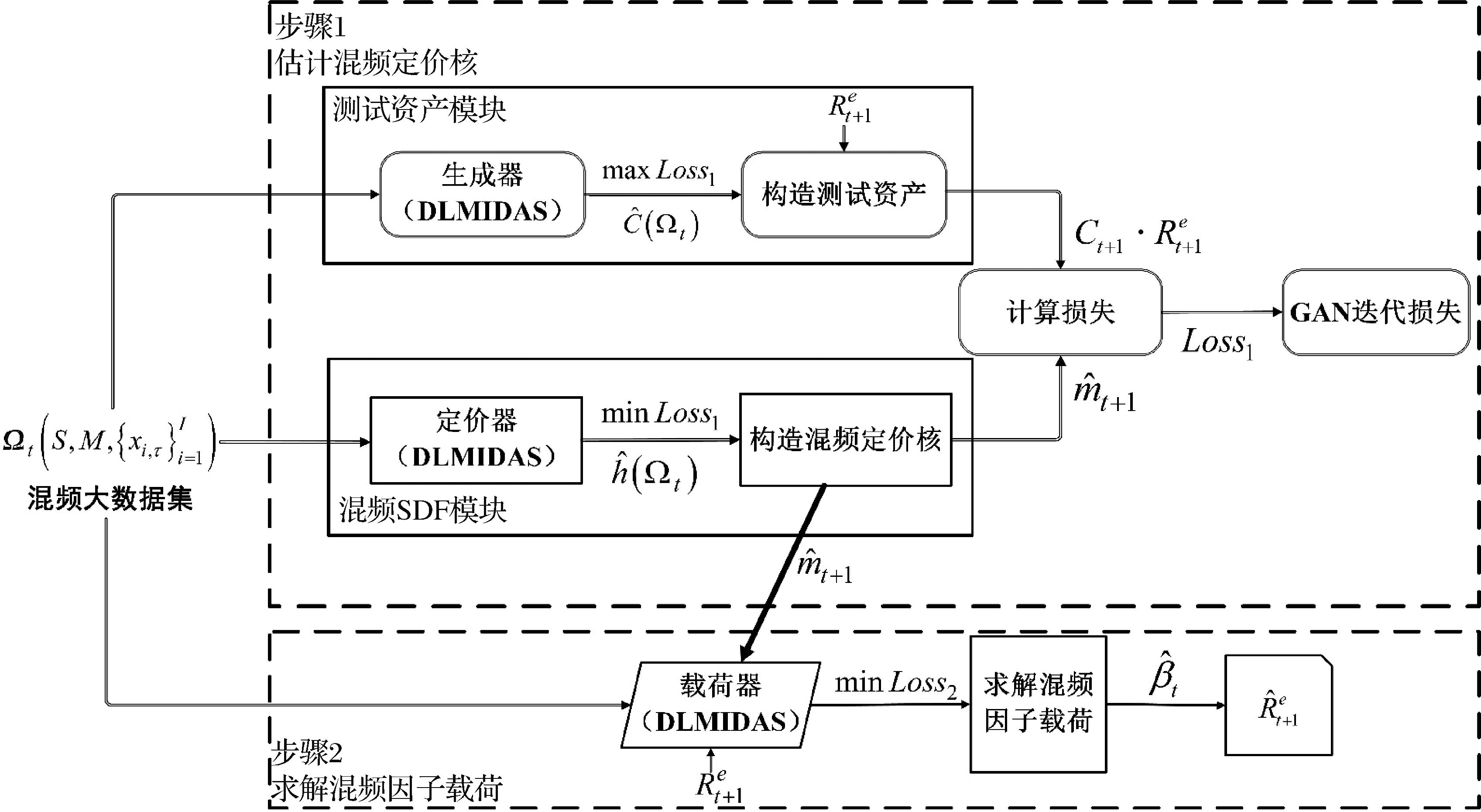

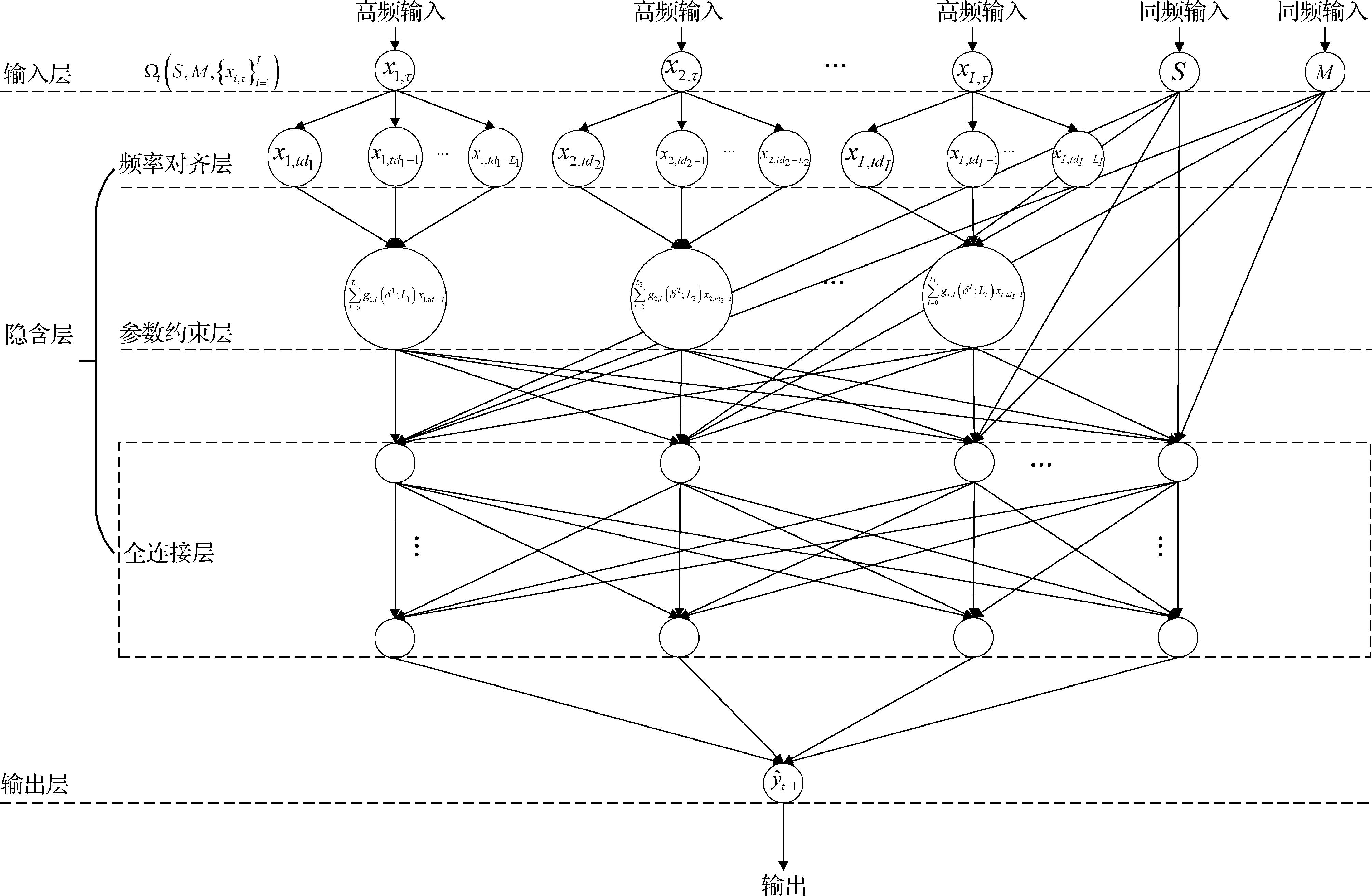

"

"

"

| 模型 | 混频数据处理能力 | 生成对抗博弈机制 | SDF理论架构 | 非线性定价结构 |

|---|---|---|---|---|

| MIDAS-SDF-GAN | √ | √ | √ | √ |

| GAN | × | √ | √ | √ |

| DL-MIDAS | √ | × | √ | √ |

| ANN | × | × | × | √ |

| LSDF | × | × | √ | × |

"

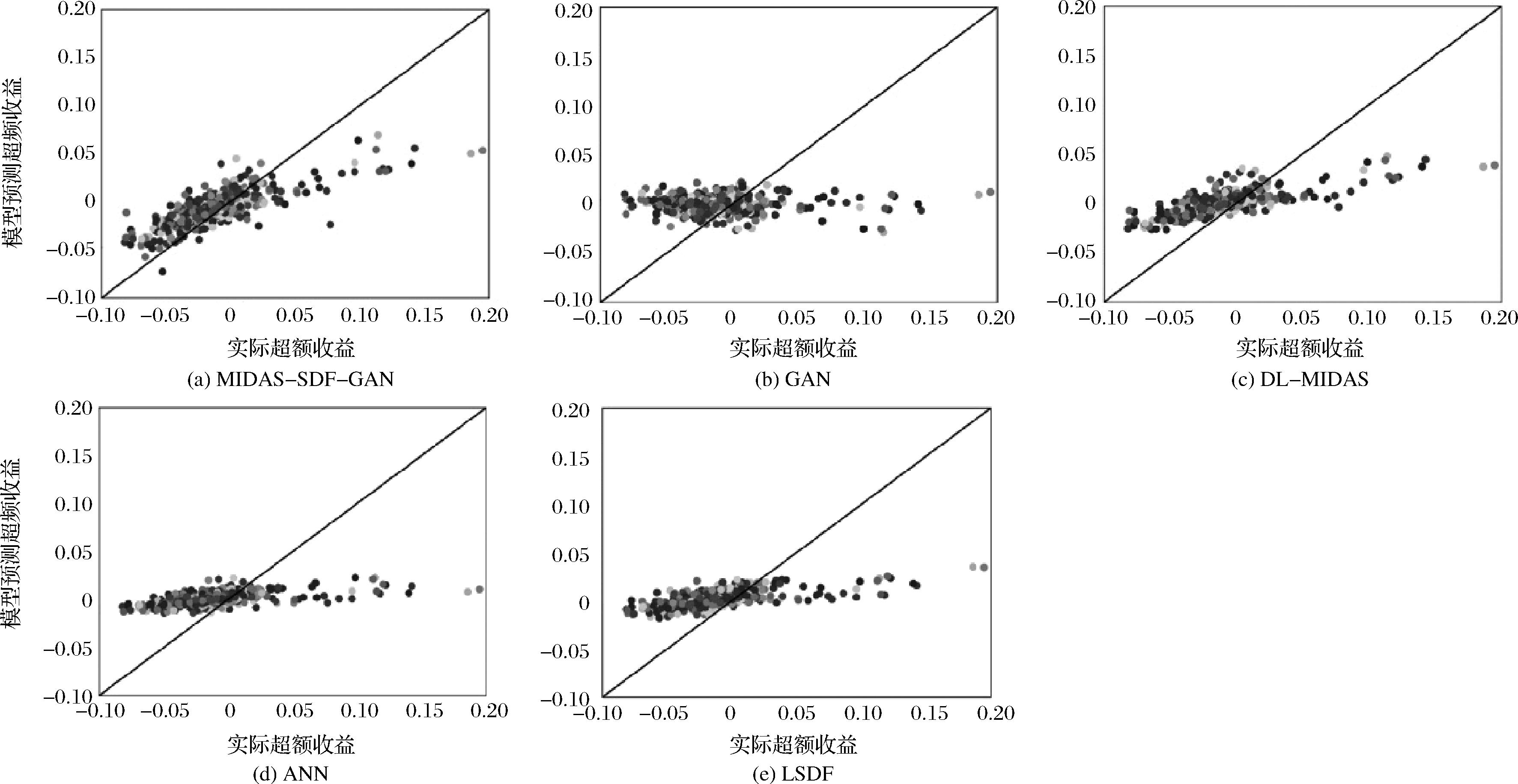

| 模型 | EV | |

|---|---|---|

| MIDAS-SDF-GAN | 0.18 | 0.19 |

| GAN | 0.15 | 0.15 |

| DL-MIDAS | 0.12 | 0.13 |

| ANN | 0.14 | 0.14 |

| LSDF | 0.10 | 0.10 |

"

| 投资组合 | EV | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| MIDAS-SDF-GAN | GAN | DL-MIDAS | ANN | LSDF | MIDAS-SDF-GAN | GAN | DL-MIDAS | ANN | LSDF | ||

| bm单排序投资组合 | 0.0475 | 0.0477 | 0.0500 | 0.0507 | 0.0501 | 0.8072 | 0.7845 | 0.7798 | 0.7591 | 0.7821 | |

| mom36m单排序投资组合 | 0.0450 | 0.0524 | 0.0532 | 0.0482 | 0.0607 | 0.9306 | 0.8783 | 0.9091 | 0.9208 | 0.8769 | |

| volatility单排序投资组合 | 0.0537 | 0.0595 | 0.0577 | 0.0637 | 0.0623 | 0.8010 | 0.7244 | 0.7548 | 0.7059 | 0.7230 | |

| lev单排序投资组合 | 0.0674 | 0.0892 | 0.0797 | 0.0891 | 0.0847 | 0.7943 | 0.5387 | 0.6693 | 0.5897 | 0.5821 | |

| bm-mve双排序投资组合 | 0.0333 | 0.0441 | 0.0397 | 0.0428 | 0.0428 | 0.9078 | 0.7940 | 0.8535 | 0.8241 | 0.8113 | |

| mom36m-chmom双排序投资组合 | 0.0333 | 0.0441 | 0.0397 | 0.0428 | 0.0428 | 0.9192 | 0.8745 | 0.8987 | 0.9119 | 0.8693 | |

| I/A单排序投资组合 | 0.0358 | 0.0528 | 0.0453 | 0.0480 | 0.0613 | 0.9442 | 0.8780 | 0.8437 | 0.9184 | 0.8744 | |

| ROE单排序投资组合 | 0.0382 | 0.0526 | 0.0447 | 0.0480 | 0.0612 | 0.9492 | 0.8775 | 0.9274 | 0.9184 | 0.8743 | |

| I/A-ROE双排序投资组合 | 0.0447 | 0.0532 | 0.0545 | 0.0490 | 0.0620 | 0.9255 | 0.8776 | 0.9066 | 0.9078 | 0.8713 | |

"

| 模型 | EV | |

|---|---|---|

| MIDAS-SDF-GAN | 0.0489 | 0.7934 |

| GAN | 0.0514 | 0.7514 |

| DL-MIDAS | 0.0521 | 0.7683 |

| ANN | 0.0554 | 0.7356 |

| LSDF | 0.0524 | 0.7537 |

"

"

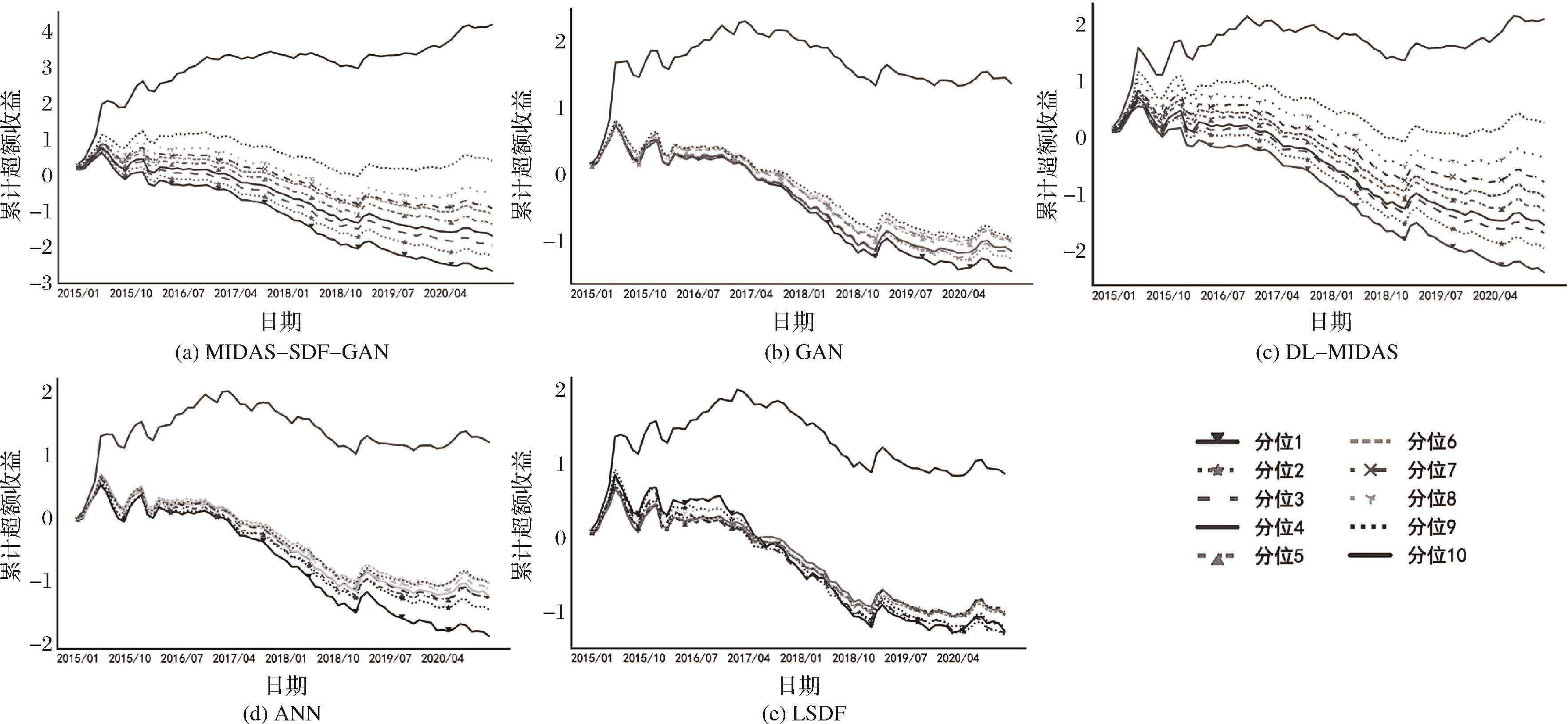

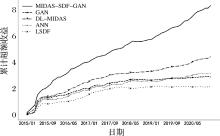

| 模型 | SR | AR | MaxLoss | MD |

|---|---|---|---|---|

| MIDAS-SDF-GAN | 0.90 | 0.05 | 0.05 | 0.06 |

| GAN | 0.42 | 0.03 | 0.12 | 0.15 |

| DL-MIDAS | 0.62 | 0.03 | 0.06 | 0.14 |

| ANN | 0.32 | 0.02 | 0.15 | 0.25 |

| LSDF | 0.23 | 0.01 | 0.12 | 0.35 |

"

"

"

| 模型 | SR | AR | MaxLoss | MD |

|---|---|---|---|---|

| MIDAS-SDF-GAN | 1.1477 | 0.1153 | 0.0456 | 0.0081 |

| GAN | 0.5426 | 0.0438 | 0.0545 | 0.0307 |

| DL-MIDAS | 0.7813 | 0.0615 | 0.0172 | 0.0123 |

| ANN | 0.4604 | 0.0402 | 0.0572 | 0.0326 |

| LSDF | 0.5491 | 0.0305 | 0.0551 | 0.0662 |

"

| 1 |

|

| 2 |

|

| 3 |

|

| 4 |

|

| 5 |

|

| 6 |

|

| 7 |

|

| 8 |

|

| 9 |

姜富伟, 马甜, 张宏伟. 高风险低收益? 基于机器学习的动态CAPM模型解释[J]. 管理科学学报, 2021, 24(1): 109-126.

|

|

|

|

| 10 |

|

| 11 |

|

| 12 |

|

| 13 |

|

| 14 |

|

| 15 |

|

| 16 |

|

| 17 |

|

| 18 |

|

| 19 |

许启发, 卓杏轩, 蒋翠侠. 反向有约束混频数据模型的市场化利率预测[J]. 管理科学学报, 2019, 22(10): 55-71.

|

|

|

|

| 20 |

谭德凯, 田利辉.黄金是股票市场的“避险天堂”吗?——基于动态条件相关混频数据抽样模型[J]. 中国管理科学, 2022, 30(10): 1-12.

|

|

|

|

| 21 |

夏婷, 闻岳春. 经济不确定性是股市波动的因子吗?——基于GARCH-MIDAS模型的分析[J]. 中国管理科学, 2018, 26(12): 1-11.

|

|

|

|

| 22 |

|

| 23 |

|

| 24 |

张鹏, 党世力, 黄梅雨. 基于机器学习预测股票收益率的两步骤M-SV投资组合优化[J].中国管理科学, 2022,31(12):96-106.

|

|

|

| [1] | Zezhou Wang, Qifa Xu, Cuixia Jiang. Can Interaction and Dissemination of Mixed-Frequency Information in Companies' Multi-Layer Relationship Networks Improve Asset Pricing? Asset Pricing Study Based on Graph Neural Networks [J]. Chinese Journal of Management Science, 2026, 34(4): 47-62. |

| [2] | Juanjuan Lin, Zhigang Huang, Yong Tang. Data Quality, Quantity and Data Asset Pricing: Based on the Perspective of Consumer Heterogeneity [J]. Chinese Journal of Management Science, 2025, 33(5): 88-98. |

| [3] | Xingyi Li, Zhongfei Li, Qiqian Li, Yujun Liu, Wenjin Tang. A Review of Research on Asset Return Prediction Based on Machine Learning [J]. Chinese Journal of Management Science, 2025, 33(1): 311-322. |

| [4] | Xuanming Ni,Tiantian Zheng,Huimin Zhao,Kangping Wu. Asset Pricing Based on the Optimal Idiosyncratic Return Factor [J]. Chinese Journal of Management Science, 2024, 32(8): 50-60. |

| [5] | CHEN Miao-xin, HUANG Zhen-wei. Long Memory Volatility and Cross-section Stock Returns: Empirical Research in Chinese Stock Market [J]. Chinese Journal of Management Science, 2023, 31(4): 1-10. |

| [6] | LU Jing, ZHANG Yin-ying. Idiosyncratic Volatility Puzzle and Its Estimation Model [J]. Chinese Journal of Management Science, 2022, 30(9): 36-48. |

| [7] | LIU Yan, ZHU Hong-quan. Individual Investor or Institutional Investor, Who Dominates Asset Pricing in Chinese A-share Stock Market? [J]. Chinese Journal of Management Science, 2018, 26(4): 120-130. |

| [8] | XU Yuan-dong. The Consistency of Logical Structure about Asset Pricing in BSV, DHS model and Asset Pricing under Ambiguity [J]. Chinese Journal of Management Science, 2017, 25(6): 22-31. |

| [9] | GONG Xu, WEN Feng-hua, HUANG Chuang-xia, YANG Xiao-guang. Downside Risk, Signed Jump Risk and Asset Pricing of Industry Portfolios [J]. Chinese Journal of Management Science, 2017, 25(10): 1-10. |

| [10] | LIU Wei-qi, XING Hong-wei, ZHANG Xin-dong. Investment Preference and the Idiosyncratic Volatility Puzzle——Evidence from China Stock Market [J]. Chinese Journal of Management Science, 2014, 22(8): 10-20. |

| [11] | ZHOU Fang, ZHANG Wei, ZHOU Bing. Capital Asset Pricing Model Based on Liquidity Risk [J]. Chinese Journal of Management Science, 2013, 21(5): 1-7. |

| [12] | WU Xin-yu, ZHOU Hai-lin, MA Chao-qun, WANG Shou-yang. Stochastic Discount Factor-Based Approach for Warrant Pricing [J]. Chinese Journal of Management Science, 2012, (4): 1-7. |

| [13] | ZHU Hong-quan, CHEN Lin, PAN Ning-ning. Industry, Local and Market Information, Who Dominates Price Movement in Chinese Stock Market? [J]. Chinese Journal of Management Science, 2011, 19(4): 1-8. |

| [14] | LUO Deng-yue, WANG Chun-feng, FANG Zhen-ming. An Empirical Research on the Relationship between Aggregate Liquidity and Asset Pricing in China Stock Market [J]. Chinese Journal of Management Science, 2007, 15(2): 33-38. |

| [15] | LU Jing, TANG Xiao-wo. The Empirical Study on Multi-Factor Pricing Model Based on Liquidity Risk [J]. Chinese Journal of Management Science, 2006, (5): 45-51. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||