主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2026, Vol. 34 ›› Issue (7): 12-21.doi: 10.16381/j.cnki.issn1003-207x.2024.1481

Previous Articles Next Articles

Jinqing Zhang1( ), Suoer Xu1,2

), Suoer Xu1,2

Received:2024-08-28

Revised:2025-03-20

Online:2026-07-25

Published:2026-06-18

Contact:

Jinqing Zhang

E-mail:zhangjq@fudan.edu.cn

CLC Number:

Jinqing Zhang,Suoer Xu. Efficient Portfolios Based on Mean-Variance Shrinkage Estimation under Mixed Normal[J]. Chinese Journal of Management Science, 2026, 34(7): 12-21.

"

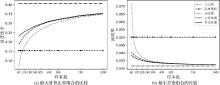

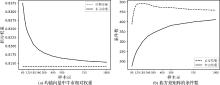

| 样本量 | 均值向量 | 协方差矩阵 | ||||

|---|---|---|---|---|---|---|

| 无收缩 | 已有收缩 | 本文收缩 | 无收缩 | 已有收缩 | 本文收缩 | |

| 60 | 5.57 | 3.99 | 1.39 | 3.76 | 3.69 | 3.45 |

| 80 | 4.83 | 3.49 | 1.38 | 3.23 | 3.18 | 3.11 |

| 100 | 4.47 | 3.33 | 1.38 | 2.88 | 2.85 | 2.74 |

| 120 | 4.16 | 3.18 | 1.38 | 2.74 | 2.71 | 2.71 |

| 180 | 3.28 | 2.54 | 1.38 | 2.15 | 2.14 | 1.94 |

| 240 | 2.83 | 2.22 | 1.33 | 1.89 | 1.88 | 1.69 |

| 300 | 2.54 | 2.05 | 1.32 | 1.70 | 1.69 | 1.57 |

| 400 | 2.19 | 1.82 | 1.27 | 1.44 | 1.43 | 1.36 |

| 500 | 1.96 | 1.66 | 1.21 | 1.29 | 1.28 | 1.25 |

| 750 | 1.62 | 1.44 | 1.08 | 1.07 | 1.07 | 1.03 |

| 1000 | 1.39 | 1.26 | 1.03 | 0.91 | 0.91 | 0.89 |

"

"

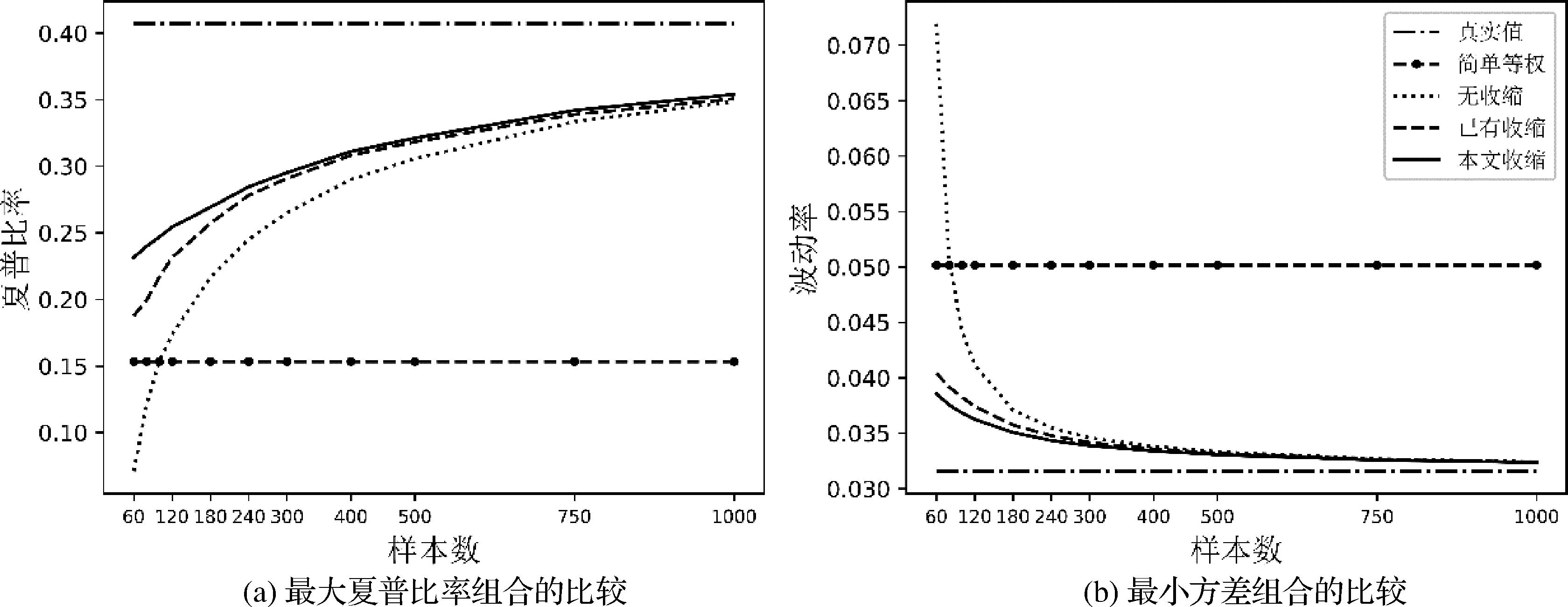

| 样本量 | 最大夏普比率组合 | 最小方差组合 | ||||

|---|---|---|---|---|---|---|

| 无收缩 | 已有收缩 | 本文收缩 | 无收缩 | 已有收缩 | 本文收缩 | |

| 60 | 2999.14 | 211.02 | 10.61 | 30.35 | 8.97 | 6.61 |

| 80 | 1732.09 | 203.38 | 10.53 | 18.32 | 8.87 | 6.58 |

| 100 | 275.69 | 170.62 | 10.53 | 14.43 | 8.59 | 6.45 |

| 120 | 234.26 | 123.11 | 10.43 | 12.22 | 8.19 | 6.28 |

| 180 | 61.42 | 73.63 | 10.32 | 9.08 | 7.19 | 5.82 |

| 240 | 79.36 | 28.22 | 9.74 | 7.45 | 6.34 | 5.36 |

| 300 | 32.29 | 14.11 | 9.62 | 6.58 | 5.81 | 5.05 |

| 400 | 25.66 | 12.39 | 9.46 | 5.56 | 5.09 | 4.56 |

| 500 | 22.11 | 11.17 | 9.04 | 4.90 | 4.57 | 4.19 |

| 750 | 17.27 | 9.56 | 8.88 | 3.91 | 3.74 | 3.53 |

| 1000 | 14.93 | 8.92 | 8.23 | 3.34 | 3.24 | 3.10 |

"

"

| 股票资产池 | 资产数 | 简写 |

|---|---|---|

| 沪深300一级行业指数 | 10 | HS-Ind10 |

| Wind一级行业指数 | 11 | W-Ind11 |

| Wind二级行业指数 | 24 | W-Ind24 |

| Wind三级行业指数 | 58 | W-Ind58 |

| Wind四级行业指数 | 100 | W-Ind100 |

"

| 编号 | 有效资产组合确定方法 | 简称 |

|---|---|---|

| 无收缩估计方法 | ||

| 1 | 最大夏普比率组合 | mv |

| 2 | 最小方差组合 | min |

| 3 | 简单等权组合 | ew |

| 无收缩估计方法+混合组合方法 | ||

| 4 | 最大夏普比率组合和最小方差组合的最优混合组合(Kan和Zhou[ | kz |

| 5 | 最大夏普比率组合和简单等权组合的最优混合组合(Tu和Zhou[ | tz |

| 收缩估计方法 | ||

| 6 | 最大夏普比率组合,基于Jorion[ | mv-bs |

| 7 | 最小方差组合,基于Ledoit和Wolf[ | min-lw |

| 8 | 最大夏普比率组合,基于DeMiguel等[ | mv-dm |

| 9 | 最大夏普比率组合,基于本文的收缩估计量 | mv-mn |

| 10 | 最小方差组合,基于本文的收缩估计量 | min-mn |

"

| 有效资产组合 | HS-Ind10 | W-Ind11 | W-Ind23 | W-Ind58 | W-Ind100 |

|---|---|---|---|---|---|

| mv | |||||

| min | 0.076 | 0.136 | 0.094 | 0.026 | |

| ew | 0.104 | 0.147 | 0.111 | ||

| kz | |||||

| tz | 0.063 | ||||

| mv-bs | 0.106 | 0.104 | 0.078 | 0.044 | 0.029 |

| min-lw | 0.124 | 0.175 | 0.159 | 0.089 | 0.053 |

| mv-dm | 0.113 | 0.117 | 0.094 | 0.054 | 0.040 |

| mv-mn | 0.124 | 0.121 | 0.107 | 0.072 | 0.103 |

| min-mn | 0.148 | 0.179 | 0.177 | 0.118 | 0.148 |

"

| 不同聚类算法 | HS-Ind10 | W-Ind11 | W-Ind23 | W-Ind58 | W-Ind100 |

|---|---|---|---|---|---|

| 面板a:最大夏普比率组合 | |||||

| 0.122 | 0.121 | 0.107 | 0.074 | 0.103 | |

| 0.120 | 0.120 | 0.102 | 0.073 | 0.103 | |

| 0.117 | 0.120 | 0.098 | 0.069 | 0.102 | |

| 0.110 | 0.116 | 0.093 | 0.060 | 0.097 | |

| 面板b:最小方差组合 | |||||

| 0.148 | 0.177 | 0.174 | 0.118 | 0.153 | |

| 0.146 | 0.177 | 0.174 | 0.116 | 0.153 | |

| 0.140 | 0.176 | 0.172 | 0.111 | 0.149 | |

| 0.136 | 0.170 | 0.161 | 0.105 | 0.140 | |

| [1] | Tu X, Li B. Robust portfolio selection with smart return prediction[J].Economic Modelling, 2024, 135: 106719. |

| [2] | 吴文生, 盛世杰, 韩其恒. 变动均值和方差资产配置模型的应用研究[J]. 中国管理科学, 2018, 26(2): 107-115. |

| Wu W S, Sheng S J, Han Q H. Variable mean and variance of asset allocation model in Chinese market[J]. Chinese Journal of Management Science, 2018, 26(2): 107-115. | |

| [3] | DeMiguel V, Martin-Utrera A, Nogales F J. Size matters: Optimal calibration of shrinkage estimators for portfolio selection[J]. Journal of Banking & Finance, 2013, 37(8): 3018-3034. |

| [4] | Ledoit O, Wolf M. Nonlinear shrinkage of the covariance matrix for portfolio selection: Markowitz meets goldilocks[J]. The Review of Financial Studies, 2017, 30(12): 4349-4388. |

| [5] | Jiang L, Wu K, Zhou G. Asymmetry in stock comovements: An entropy approach[J]. Journal of Financial and Quantitative Analysis, 2018, 53(4): 1479-1507. |

| [6] | Liu J, Maheu J M, Song Y. Identification and forecasting of bull and bear markets using multivariate returns[J]. Journal of Applied Econometrics, 2024, 39(5): 723-745. |

| [7] | Paolella M S. Multivariate asset return prediction with mixture models[J]. The European Journal of Finance, 2015, 21(13-14): 1214-1252. |

| [8] | 韩立岩, 胡艺鸽, 闫酣寰. 基于混合正态分布的金融资产相关性[J]. 计量经济学报, 2021, 1(4): 935-954. |

| Han L Y, Hu Y G, Yan H H. Normal mixture based linkage between financial assets[J]. China Journal of Econometrics, 2021, 1(4): 935-954. | |

| [9] | Jorion P. Bayes-stein estimation for portfolio analysis[J]. The Journal of Financial and Quantitative Analysis, 1986, 21(3): 279-292. |

| [10] | Black F, Litterman R B. Asset allocation: Combining investor views with market equilibrium[J]. The Journal of Fixed Income, 1991, 1(2): 7-18. |

| [11] | 孟勇, 任梦, 赵心. 行业资产的Black-Litterman模型配置研究——基于社交网络情绪文本挖掘算法[J]. 数量经济技术经济研究, 2022, 39(1): 154-173. |

| Meng Y, Ren M, Zhao X. Research on black-litterman model allocation of industry asset[J]. The Journal of Quantitative & Technical Economics, 2022, 39(1): 154-173. | |

| [12] | 李仲飞, 周骐. 一个基于BL模型和复杂网络的行业配置模型[J]. 中国管理科学, 2024, 32(4): 1-13. |

| Li Z F, Zhou Q. An industry allocation model based on BL model and complex network[J]. Chinese Journal of Management Science, 2024, 32(4): 1-13. | |

| [13] | 赵大萍, 张超梁, 房勇. 基于贝叶斯理论的长、短数据资产组合选择[J]. 中国管理科学, 2015, 23(S1): 504-509. |

| Zhao D P, Zhang C L, Fang Y. Portfolio selection of unequal histories of returns with Bayesian tramework[J]. Chinese Journal of Management Science, 2015, 23(S1): 504-509. | |

| [14] | Zhang J, Jin Z, An Y. Dynamic portfolio optimization with ambiguity aversion[J]. Journal of Banking & Finance, 2017, 79: 95-109. |

| [15] | 赵钊. 高维条件协方差矩阵的非线性压缩估计及其在构建最优投资组合中的应用[J]. 中国管理科学, 2017, 25(8): 46-57. |

| Zhao Z. Nonlinear shrinkage estimation of high dimensional conditional covariance matrix and its application in portfolio selection[J]. Chinese Journal of Management Science, 2017, 25(8): 46-57. | |

| [16] | De Nard G, Ledoit O, Wolf M. Factor models for portfolio selection in large dimensions: The good, the better and the ugly[J]. Journal of Financial Econometrics, 2021, 19(2): 236-257. |

| [17] | Shi F, Shu L, He F, et al. Improving minimum-variance portfolio through shrinkage of large covariance matrices[J].Economic Modelling, 2025, 144: 106981. |

| [18] | Kan R, Zhou G. Optimal portfolio choice with parameter uncertainty[J]. Journal of Financial and Quantitative Analysis, 2007, 42(3): 621-656. |

| [19] | Tu J, Zhou G. Markowitz meets Talmud: A combination of sophisticated and naive diversification strategies[J]. Journal of Financial Economics, 2011, 99(1): 204-215. |

| [20] | Levy M, Kaplanski G. Portfolio selection in a two-regime world[J]. European Journal of Operational Research, 2015, 242(2): 514-524. |

| [21] | Kocuk B, Cornuéjols G. Incorporating Black-Litterman views in portfolio construction when stock returns are a mixture of normals[J]. Omega, 2020, 91: 102008. |

| [22] | MacLean L, Zhao Y, Zhang O. Mean-variance optimization with inferred regimes[J]. Annals of Operations Research, 2025, 346(1): 341-368. |

| [23] | McLachlan G J, Krishnan T. The EM Algorithm and Extensions, 2E[M]. Hoboken, NJ, USA: John Wiley & Sons, Inc. 2008. |

| [24] | Yang M S, Lai C Y, Lin C Y. A robust EM clustering algorithm for Gaussian mixture models[J]. Pattern Recognition, 2012, 45(11): 3950-3961. |

| [1] | Chao Liu, Lantao Xu. Study on Optimal Portfolio Strategy from the Perspective of Multilayer Temporal Network [J]. Chinese Journal of Management Science, 2025, 33(9): 46-56. |

| [2] | Yinhong Yao, Xiaoxu Wang, Wei Chen, Zhensong Chen. Extreme Risk Spillover among Global Stock Markets Based on Transformer-LSTM Quantile Regression [J]. Chinese Journal of Management Science, 2025, 33(8): 1-13. |

| [3] | Haoyuan Feng, Jie Wu, Anqi Yu, Kun Guo. Will Leveraged Trading Increase the Liquidity of the Stock Market? Empirical Analysis Based on Individual Stocks of Micro-Level [J]. Chinese Journal of Management Science, 2025, 33(4): 1-11. |

| [4] | Xiong Xiong, Rongtian Zhou, Yibo Wang, Shen Lin. Research on the Optimization of Transaction Tax in China’s Capital Market: Based on the Perspective of Artificial Stock Market [J]. Chinese Journal of Management Science, 2025, 33(1): 356-368. |

| [5] | JIANG Chong-hui, LIU Lin. The Effectiveness of Momentum Factor Tracking Strategy: Evidence from China Stock Market [J]. Chinese Journal of Management Science, 2022, 30(5): 86-97. |

| [6] | TAN De-kai, TIAN Li-hui. Is Gold a Safe Haven of the Stock Market?——Based on Dynamic Conditional Correlation Mixed Data Sampling Model [J]. Chinese Journal of Management Science, 2022, 30(10): 14-24. |

| [7] | ZHU Xiao-neng, WU Jie-nan. The “Ripple Effect” in Stock Market Co-movement [J]. Chinese Journal of Management Science, 2021, 29(8): 1-12. |

| [8] | TANG Zhen-peng, WU Jun-chuan, RAN Meng, ZHANG Ting-ting. Research on The Self-exciting Effect of Chinese Stock Market Considering Investor Sentiment [J]. Chinese Journal of Management Science, 2020, 28(7): 1-12. |

| [9] | XIE Chi, HU Xue-jing, WANG Gang-jin. Dynamic Evolution and Market Robustness of Chinese Stock Market in the Past 10 Years of the Financial Crisis: An Empirical Research Based on Complex Network Perspective [J]. Chinese Journal of Management Science, 2020, 28(6): 1-12. |

| [10] | CHEN Qi-an, ZHANG Hui, CHEN Shu-yu. Does Stock Index Futures Trading Increase the Stock Market Volatility in China?——Theoretical and Empirical Research Based on Investor Structure [J]. Chinese Journal of Management Science, 2020, 28(4): 1-13. |

| [11] | ZHANG Tong-hui, YUAN Ying, ZENG Wen. Can Investor Attention Help to Predict Stock Market Volatility? An Empirical Research Based on Chinese Stock Market High-frequency Data [J]. Chinese Journal of Management Science, 2020, 28(11): 192-205. |

| [12] | LIU Feng-gen, WU Jun-chuan, YANG Xi-te, OUYANG Zi-sheng. Long-run Dynamic Effect of Macro-economy on Stock Market Volatility Based on Mixed Frequency Data Model [J]. Chinese Journal of Management Science, 2020, 28(10): 65-76. |

| [13] | YIN Li-bo, WEI Ya, HAN Fu-ling. Study on Characteristics and Influence Factors of Time-varying Anomalies in China's Stock Market [J]. Chinese Journal of Management Science, 2019, 27(8): 14-25. |

| [14] | ZHAO Peng-ju, ZHANG Wei. Stock Market Evolution Research Based on Random Dynamic System [J]. Chinese Journal of Management Science, 2019, 27(5): 50-56. |

| [15] | YIN Hai-yuan, Zhu Xu. Investor Heterogeneous Beliefs, Expect Evolution and Stock Market Liquidity [J]. Chinese Journal of Management Science, 2019, 27(10): 12-21. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||