主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2026, Vol. 34 ›› Issue (4): 298-308.doi: 10.16381/j.cnki.issn1003-207x.2024.1451

Previous Articles Next Articles

Jujie Wang( ), Xin Zhang

), Xin Zhang

Received:2024-08-26

Revised:2024-10-23

Online:2026-04-25

Published:2026-03-27

Contact:

Jujie Wang

E-mail:jujiewang@126.com

CLC Number:

Jujie Wang,Xin Zhang. Carbon Price Interval Forecasting Study Based on the Hybrid Quantile and Time-Varying Weights[J]. Chinese Journal of Management Science, 2026, 34(4): 298-308.

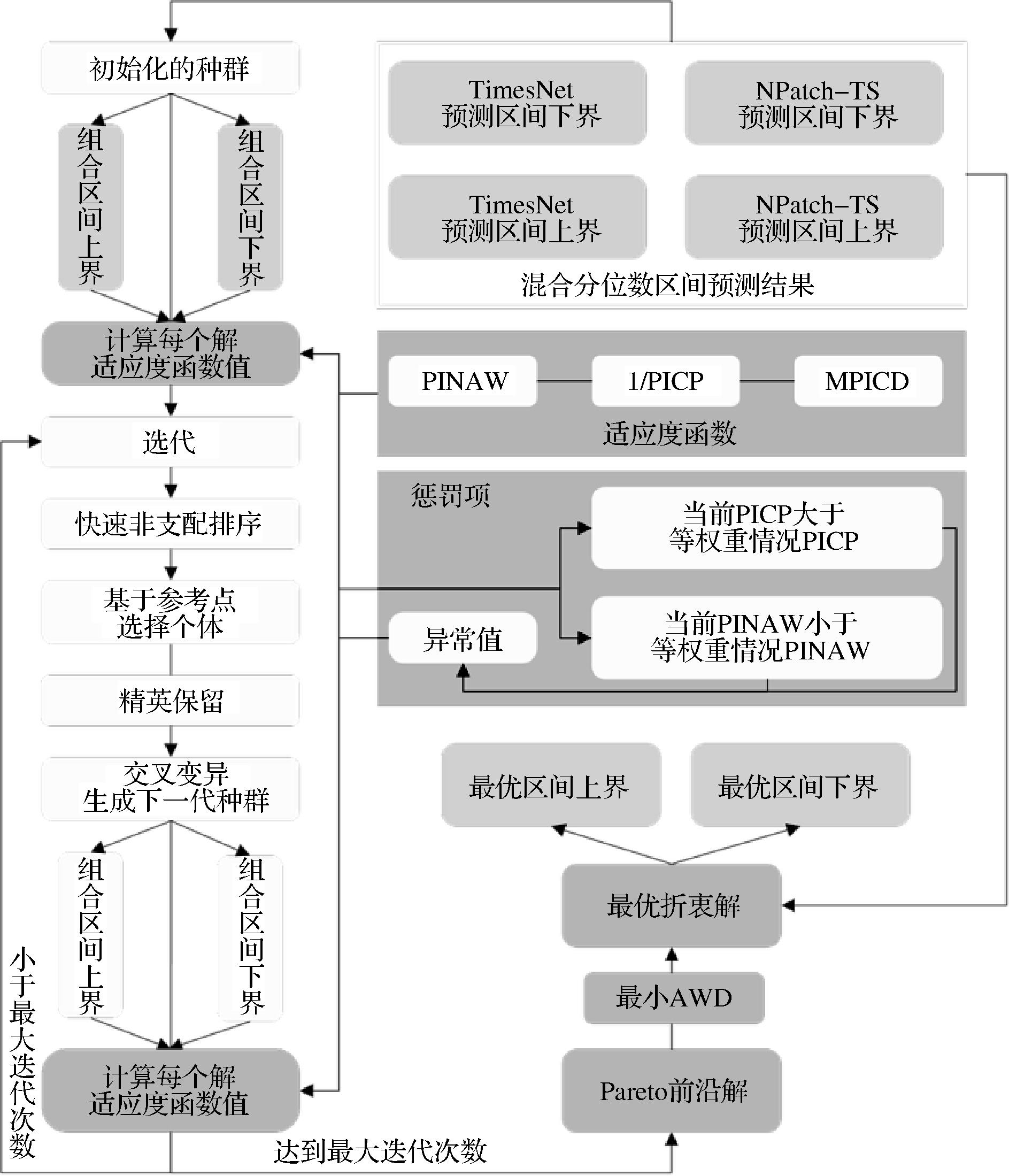

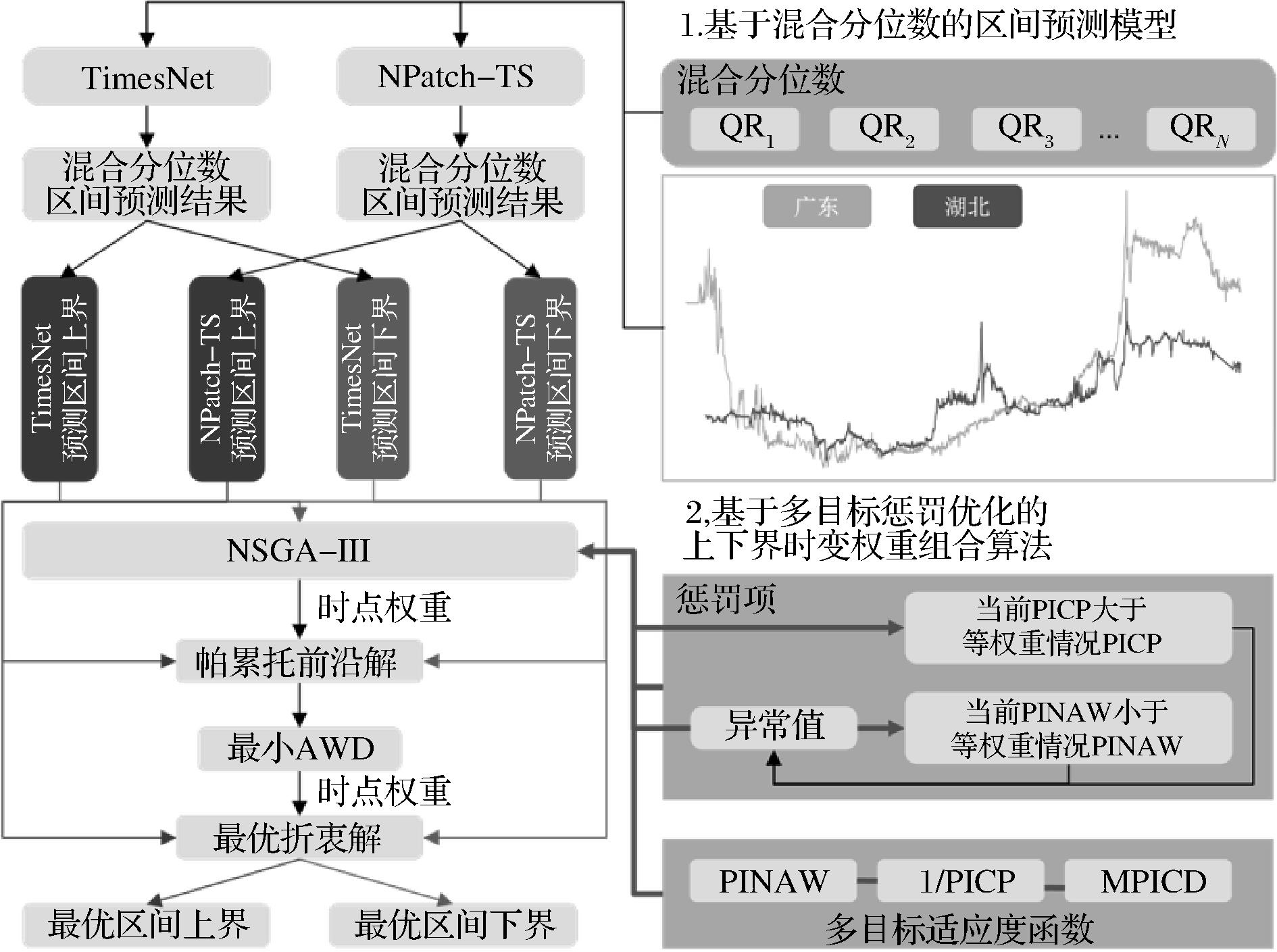

"

"

"

| 评估指标 | 定义 | 公式 |

|---|---|---|

| PIAW | 区间平均宽度 | |

| PINAW | 区间归一化平均宽度 | |

| PICP | 区间覆盖率 | |

| MPICD | 平均区间中心偏差 | |

| AWD | 累积宽度偏差 |

"

"

"

"

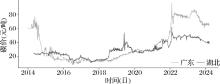

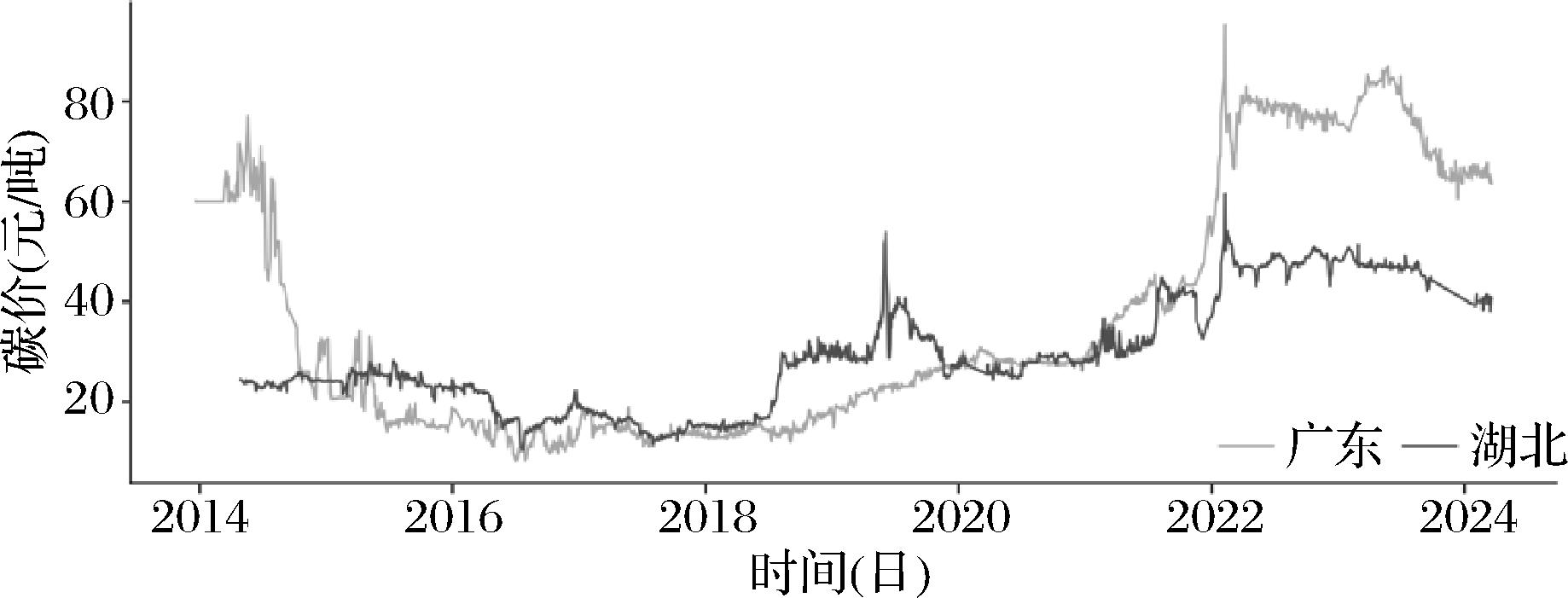

| 试点 | 样本量 | 均值 | 标准差 | 最小值 | 25% | 50% | 75% | 最大值 | 偏度 | 峰度 |

|---|---|---|---|---|---|---|---|---|---|---|

| 广东 | 2084 | 35.62 | 24.37 | 8.10 | 15.29 | 27.06 | 60.24 | 95.26 | 0.85 | -0.83 |

| 湖北 | 2149 | 28.42 | 10.89 | 10.38 | 20.90 | 26.29 | 33.35 | 61.48 | 0.60 | -0.63 |

"

"

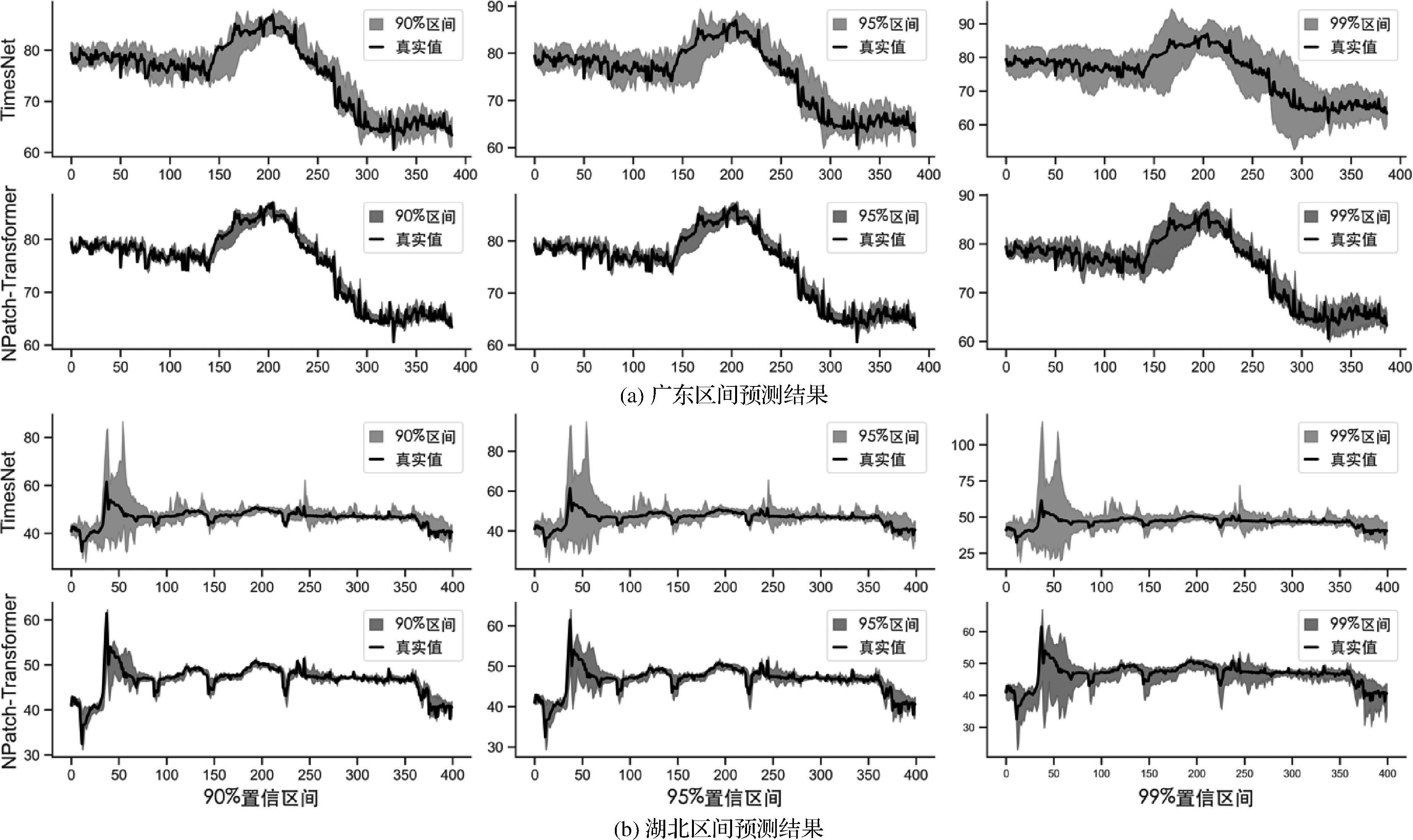

| 试点 | 预测模型 | 评估指标 | 90%置信区间 | 95%置信区间 | 99%置信区间 |

|---|---|---|---|---|---|

| 广东 | TimesNet | PIAW | 4.9707 | 6.4727 | 12.0167 |

| PINAW | 0.1884 | 0.2453 | 0.4554 | ||

| PICP | 87.8553 | 93.5401 | 99.2248 | ||

| MPICD | 1.2588 | 1.2891 | 1.0609 | ||

| AWD | 10.6520 | 4.7815 | 0.5437 | ||

| NPatch-Transformer | PIAW | 1.9174 | 2.5889 | 4.9693 | |

| PINAW | 0.0727 | 0.0981 | 0.1883 | ||

| PICP | 58.9147 | 67.9587 | 88.1137 | ||

| MPICD | 0.9845 | 0.9902 | 1.0609 | ||

| AWD | 104.0048 | 58.7865 | 10.1403 | ||

| 湖北 | TimesNet | PIAW | 6.9430 | 9.2918 | 13.4438 |

| PINAW | 0.2394 | 0.3204 | 0.4636 | ||

| PICP | 92.0000 | 95.7500 | 98.7500 | ||

| MPICD | 1.2158 | 1.2778 | 1.4227 | ||

| AWD | 9.8612 | 4.5588 | 1.8592 | ||

| NPatch-Transformer | PIAW | 2.0910 | 3.0382 | 6.2523 | |

| PINAW | 0.0721 | 0.1048 | 0.2156 | ||

| PICP | 75.0000 | 87.2500 | 97.0000 | ||

| MPICD | 0.7405 | 0.7385 | 1.1602 | ||

| AWD | 48.7236 | 23.1186 | 3.7926 |

"

"

"

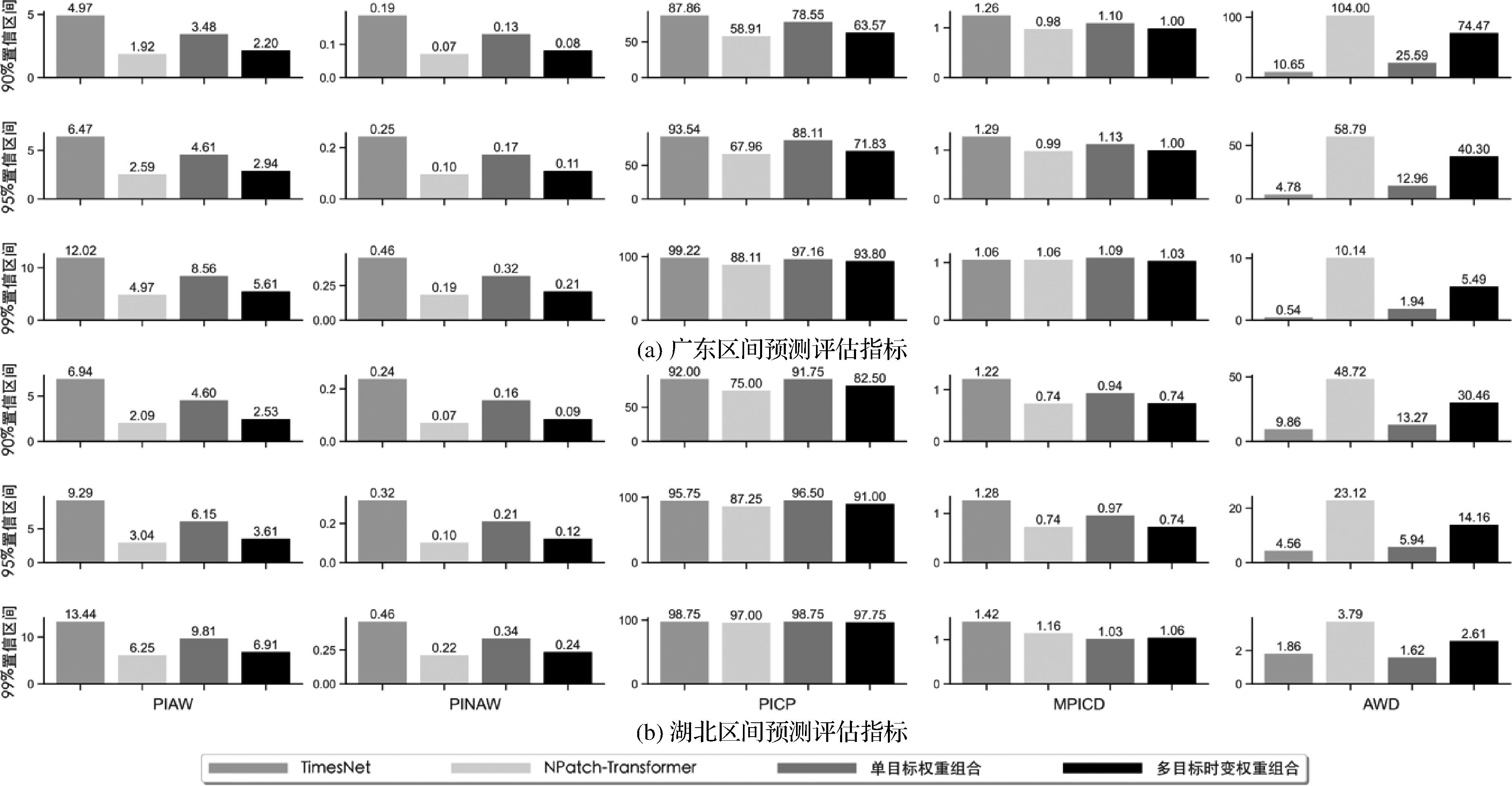

| 试点 | 组合算法 | 评估 指标 | 90%置信区间 | 95%置信区间 | 99%置信区间 |

|---|---|---|---|---|---|

| 广东 | 单目标优化 | PIAW | 2.1950 | 2.9419 | 5.6100 |

| PINAW | 0.0832 | 0.1115 | 0.2126 | ||

| PICP | 63.5659 | 71.8346 | 93.7984 | ||

| MPICD | 0.9956 | 1.0042 | 1.0334 | ||

| AWD | 74.4730 | 40.2967 | 5.4947 | ||

| 多目标时变优化 | PIAW | 3.4808 | 4.6129 | 8.5559 | |

| PINAW | 0.1319 | 0.1748 | 0.3242 | ||

| PICP | 78.5530 | 88.1137 | 97.1576 | ||

| MPICD | 1.1033 | 1.1330 | 1.0909 | ||

| AWD | 25.5929 | 12.9593 | 1.9371 | ||

| 湖北 | 单目标优化 | PIAW | 2.5321 | 3.6067 | 6.9060 |

| PINAW | 0.0873 | 0.1244 | 0.2381 | ||

| PICP | 82.5000 | 91.0000 | 97.7500 | ||

| MPICD | 0.7447 | 0.7380 | 1.0571 | ||

| AWD | 30.4614 | 14.1638 | 2.6147 | ||

| 多目标时变优化 | PIAW | 4.5970 | 6.1485 | 9.8145 | |

| PINAW | 0.1585 | 0.2120 | 0.3384 | ||

| PICP | 91.7500 | 96.5000 | 98.7500 | ||

| MPICD | 0.9441 | 0.9709 | 1.0262 | ||

| AWD | 13.2713 | 5.9440 | 1.6238 |

| [1] | 章高敏, 王腾, 娄渊雨, 等. 基于LSTM神经网络的中国省级碳达峰路径分析[J]. 中国管理科学, 2025, 33(3): 339-350. |

| Zhang G M, Wang T, Lou Y Y, et al. Path analysis of china provincial peak carbon dioxide emissions Based on LSTM neural network[J]. Chinese Journal of Management Science, 2025, 33(3): 339-350. | |

| [2] | 刘金培, 张了丹, 陈意, 等. 文本数据驱动的碳交易价格区间二层分解预测方法[J]. 管理评论, 2023, 35(12): 31-39. |

| Liu J P, Zhang L D, Chen Y, et al. A two-layer decomposition method with textual data for carbon price interval forecast[J]. Management Review, 2023, 35(12): 31-39. | |

| [3] | 张希良, 黄晓丹, 张达, 等. 碳中和目标下的能源经济转型路径与政策研究[J]. 管理世界, 2022, 38(1): 35-66. |

| Zhang X L, Huang X D, Zhang D, et al. Research on the pathway and policies for China’s energy and economy transformation toward carbon neutrality[J]. Journal of Management World, 2022, 38(1): 35-66. | |

| [4] | 范丽伟, 董欢欢, 渐令, 等. 基于滚动时间窗的碳市场价格分解集成预测研究[J]. 中国管理科学, 2023, 31(1): 277-286. |

| Fan L W, Dong H H, Jian L, et al. Research on integrated forecasting of carbon market price decomposition based on rolling time window[J]. Chinese Journal of Management Science, 2023, 31(1): 277-286. | |

| [5] | Niu X, Wang J, Wei D, et al. A combined forecasting framework including point prediction and interval prediction for carbon emission trading prices[J]. Renewable Energy, 2022, 201: 46-59. |

| [6] | Tian C, Hao Y. Point and interval forecasting for carbon price based on an improved analysis-forecast system[J].Applied Mathematical Modelling,2020,79: 126-144. |

| [7] | 张学竞, 胡焕玲, 凌立文, 等. 基于SSA-LSSVM-KDE的农产品价格区间预测[J]. 系统科学与数学, 2024, 44(4): 1081-1096. |

| Zhang X J, Hu H L, Ling L W, et al. Interval prediction of agricultural price based on SSA-LSSVM-KDE[J]. Journal of Systems Science and Mathematical Sciences, 2024, 44(4): 1081-1096. | |

| [8] | Ahmadpour A, Gholami Farkoush S. Gaussian models for probabilistic and deterministic Wind Power Prediction: Wind farm and regional[J]. International Journal of Hydrogen Energy, 2020, 45(51): 27779-27791. |

| [9] | Lian C, Zeng Z, Wang X, et al. Landslide displacement interval prediction using lower upper bound estimation method with pre-trained random vector functional link network initialization[J]. Neural Networks, 2020, 130: 286-296. |

| [10] | Jiang F, Zhu Q, Tian T. An ensemble interval prediction model with change point detection and interval perturbation-based adjustment strategy: A case study of air quality[J]. Expert Systems with Applications, 2023, 222: 119823. |

| [11] | Li Q, Wang J, Zhang H. A wind speed interval forecasting system based on constrained lower upper bound estimation and parallel feature selection[J]. Knowledge- Based Systems, 2021, 231: 107435. |

| [12] | Wang J, He M, Jiang W. Causal carbon price interval prediction using lower upper bound estimation combined with asymmetric multi-objective evolutionary algorithm and long short-term memory[J]. Expert Systems with Applications, 2024, 236: 121286. |

| [13] | Wang Y, Hu Q, Meng D, et al. Deterministic and probabilistic wind power forecasting using a variational Bayesian-based adaptive robust multi-kernel regression model[J]. Applied Energy, 2017, 208: 1097-1112. |

| [14] | Wang J, Wang S, Li Z. Wind speed deterministic forecasting and probabilistic interval forecasting approach based on deep learning, modified tunicate swarm algorithm, and quantile regression[J]. Renewable Energy, 2021, 179: 1246-1261. |

| [15] | Pradeepkumar D, Ravi V. Forecasting financial time series volatility using particle swarm optimization trained quantile regression neural network[J].Applied Soft Computing, 2017, 58: 35-52. |

| [16] | Wan C, Lin J, Wang J, et al. Direct quantile regression for nonparametric probabilistic forecasting of wind power generation[J]. IEEE Transactions on Power Systems, 2017, 32(4): 2767-2778. |

| [17] | Wang W, Feng B, Huang G, et al. Conformal asymmetric multi-quantile generative transformer for day-ahead wind power interval prediction[J].Applied Energy, 2023, 333: 120634. |

| [18] | Wu H, Hu T, Liu Y, et al. Times net: Temporal 2D-variation modeling for general time series analysis [C]//Proceedings of the Eleventh International Conference on Learning Representations, Kigali Rwanda, May 1-5, 2023. |

| [19] | Nie Y, Nguyen N H, Sinthong P, et al. A time series is worth 64 words: Long-term forecasting with transformers [C]//Proceedings of the Eleventh International Conference on Learning Representations, Kigali Rwanda, May 1-5, 2023. |

| [20] | Liu Y, Wu H, Wang J, et al. Non-stationary transformers: Exploring the stationarity in time series forecasting[J]. Advances in Neural Information Processing Systems, 2022, 35: 9881-9893. |

| [21] | Jain H, Deb K. An evolutionary many-objective optimization algorithm using reference-point based nondominated sorting approach, part II: Handling constraints and extending to an adaptive approach[J]. IEEE Transactions on Evolutionary Computation, 2014, 18(4): 602-622. |

| [22] | Deb K, Jain H. An evolutionary many-objective optimization algorithm using reference-point-based nondominated sorting approach, part I: Solving problems with box constraints[J]. IEEE Transactions on Evolutionary Computation, 2014, 18(4): 577-601. |

| [23] | Zhou F, Huang Z, Zhang C. Carbon price forecasting based on CEEMDAN and LSTM[J]. Applied Energy, 2022, 311: 118601. |

| [1] | Qiyou Liu, Jia Chen, Chengke Zhang, Huainian Zhu. Research on Accounts Receivable Auction Financing under the Empowerment of Federated Learning and Blockchain [J]. Chinese Journal of Management Science, 2026, 34(6): 13-21. |

| [2] | Pu Wang, Kunpeng Li, Li Su. Can Dimensionality Reduction Enhance Deep Neural Networks in Learning Credit Risk? ——A Study Based on Factor-Augmented Explainable Learning Models [J]. Chinese Journal of Management Science, 2026, 34(5): 57-71. |

| [3] | Chao Liu, Fengfeng Gao, Mengwan Zhang, Qiwei Xie. Research on Risk Spillover Effect, Impact Effect and Risk Early Warning in China's Financial Market [J]. Chinese Journal of Management Science, 2025, 33(5): 1-12. |

| [4] | Zhongyi Hu, Diancheng Shui, Jiang Wu. Measurement and Evolution of Digitization Level of Chinese Listed Companies: Empirical Evidence from Annual Report Text [J]. Chinese Journal of Management Science, 2025, 33(4): 36-49. |

| [5] | Xin Li, Xu Zhang, Lean Yu, Shouyang Wang. Enhancing Short-term Tourist Flow Forecasting and Evaluation Using an Improved Transformer Framework [J]. Chinese Journal of Management Science, 2025, 33(2): 105-117. |

| [6] | Fulai Cui, Yidong Chai, Yuanchun Jiang, Yang Qian, Jianshan Sun, Yezheng Liu. Online Doctor Recommendation Considering the Uncertainty of Deep Learning Models [J]. Chinese Journal of Management Science, 2025, 33(11): 151-161. |

| [7] | Yi Cai,Zhenpeng Tang,Junchuang Wu,Xiaoxu Du,Kaijie Chen. Research on the Application of GWO-SVR Algorithm in the Prediction of Reverse Mixed Data in Stock Market and Investment Strategy [J]. Chinese Journal of Management Science, 2024, 32(5): 73-80. |

| [8] | Jiang-ze DU,Xi-zhuo CHEN,Le-an YU. Can Executives with IT Background Promote FinTech Innovation? [J]. Chinese Journal of Management Science, 2023, 31(12): 69-78. |

| [9] | Dong-xiao NIU,Zhuo-ya SIQIN,Dong-yu WANG,Xiao-min XU,Huan-fen ZHANG. Method and Application of Multi-value Chain Collaborative Data Mining in Power Equipment Enterprises Based on Deep Learning [J]. Chinese Journal of Management Science, 2023, 31(11): 321-331. |

| [10] | ZHAO Yang, HAO Jun, LI Jian-ping. A Trimmed Average Based Neural Network Ensemble Approach for Time Series Forecasting [J]. Chinese Journal of Management Science, 2022, 30(3): 211-220. |

| [11] | OUYANG Hong-bing, HUANG Kang, YAN Hong-ju. Prediction of Financial Time Series Based on LSTM Neural Network [J]. Chinese Journal of Management Science, 2020, 28(4): 27-35. |

| [12] | LI Ling, DING Shuai, LI Xiao-jian, YANG Shan-lin. Research on Smart Decision-Making Method for Upper Gastrointestinal Diseases Based on Electronic Gastroscopic Video [J]. Chinese Journal of Management Science, 2019, 27(11): 211-216. |

| [13] | FENG Wen-wen, KUANG Hai-bo, MENG Bin. Research of Baltic Dirty Tanker Index Model Based on the Improved Mean Reversion [J]. Chinese Journal of Management Science, 2018, 26(5): 40-50. |

| [14] | KONG Fan-hui, LI Jian. Resilient Operation and Promotion Strategy of OEM Supply Chain under Supply Disruption Risk [J]. Chinese Journal of Management Science, 2018, 26(2): 152-159. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||