主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

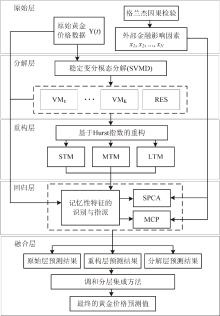

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (12): 41-56.doi: 10.16381/j.cnki.issn1003-207x.2024.2305

Previous Articles Next Articles

Zhaorong Huang1, Zhengyang Song1, Bo Yang1,2, Nengmin Zeng3,4, Le’an Yu1,2( )

)

Received:2024-12-19

Revised:2025-05-17

Online:2025-12-25

Published:2025-12-25

Contact:

Le’an Yu

E-mail:yulean@amss.ac.cn

CLC Number:

Zhaorong Huang,Zhengyang Song,Bo Yang, et al. Hybrid Multivariate Regression Forecasting for Gold Prices: A Decomposition-Reconstruction-Ensemble Methodology[J]. Chinese Journal of Management Science, 2025, 33(12): 41-56.

"

"

"

| 影响因素 | 芝加哥黄金数据集 | 伦敦黄金数据集 | ||

|---|---|---|---|---|

| 是否通过格兰杰因果检验 | 有无被MCP 回归选中 | 是否通过格兰杰因果检验 | 有无被MCP 回归选中 | |

| 恒生股指 | 是 | RES,STM | 是 | 无 |

| 印度股指 | 是 | 无 | 否 | 无 |

| 泰国股指 | 是 | VM7 | 是 | STM |

| 韩国股指 | 是 | RES,STM | 否 | VM7,VM8,RES,STM |

| 俄罗斯股指 | 否 | 无 | 是 | RES,STM |

| 巴西股指 | 是 | VM7,RES,STM | 是 | VM6,VM7,VM8,RES,STM |

| 墨西哥股指 | 是 | RES | 是 | 无 |

| 意大利股指 | 是 | RES | 否 | 无 |

| 西班牙股指 | 是 | 无 | 否 | 无 |

| 土耳其股指 | 是 | VM7,RES,STM | 是 | VM7,VM8,RES,STM |

| 立陶宛股指 | 是 | 无 | 否 | VM7,VM8,STM |

| 捷克股指 | 是 | VM7,RES,STM | 否 | 无 |

| 加拿大股指 | 是 | RES | 是 | 无 |

| 哥伦比亚股指 | 是 | 无 | 是 | 无 |

| 菲律宾股指 | 是 | 无 | 否 | 无 |

| 法国股指 | 是 | RES | 否 | 无 |

| 比利时股指 | 是 | RES,STM | 是 | VM7,VM8,RES,STM |

| 澳大利亚股指 | 是 | VM7,RES,STM | 否 | 无 |

| 爱沙尼亚股指 | 是 | 无 | 是 | RES |

| 冰岛股指 | 是 | RES | 是 | 无 |

| 沙特阿拉伯股指 | 否 | 无 | 是 | RES,STM |

| 瑞士股指 | 否 | 无 | 是 | VM7,VM8,RES,STM |

| 立陶宛股指 | 否 | 无 | 是 | VM7,VM8,STM |

| 原油期货价格 | 是 | 无 | 是 | 无 |

| 铜期货价格 | 是 | RES,STM | 是 | STM |

| 白银期货价格 | 是 | VM8,RES,STM | 是 | VM7,VM8,RES,STM |

| 标准普尔高盛商品指数 | 是 | 无 | 是 | VM7,VM8,RES,STM |

| 路透商品研究局指数 | 是 | RES | 是 | VM7,VM8,RES,STM |

| 美元(英镑)对港币汇率 | 是 | 无 | 否 | 无 |

| 美元(英镑)对人民币汇率 | 是 | VM7,RES,STM | 是 | RES,STM |

| 美元(英镑)对印度卢比汇率 | 是 | 无 | 是 | 无 |

| 美元(英镑)对日元汇率 | 是 | RES,STM | 否 | 无 |

| 美元(英镑)对加拿大元汇率 | 是 | 无 | 否 | 无 |

| 美元(英镑)对澳大利亚元汇率 | 是 | 无 | 是 | VM7,RES,STM |

| 美元(英镑)对瑞典克朗汇率 | 是 | 无 | 是 | VM7,VM8,RES,STM |

| 美元(英镑)对新西兰元汇率 | 是 | 无 | 是 | 无 |

| 美元(英镑)对欧元汇率 | 是 | 无 | 否 | 无 |

| 美元(英镑)对丹麦克朗汇率 | 是 | 无 | 是 | RES |

| 美元(英镑)对挪威克朗汇率 | 是 | 无 | 是 | VM7,VM8,RES,STM |

| 美元(英镑)对瑞士法郎汇率 | 是 | RES,STM | 是 | 无 |

| 美元(英镑)对英镑(美元)汇率 | 否 | 无 | 是 | VM7,VM8,STM |

| 香港10年期政府债收益率 | 是 | VM7,RES,STM | 是 | VM7,VM8,RES,STM |

| 中国10年期国债收益率 | 否 | 无 | 是 | STM |

| 俄罗斯10年期国债收益率 | 否 | 无 | 是 | VM7,VM8,RES,STM |

| 加拿大10年期国债收益率 | 是 | RES,STM | 是 | RES,STM |

| 法国10年期国债收益率 | 是 | 无 | 是 | 无 |

| 德国10年期国债收益率 | 是 | VM7,RES,STM | 是 | VM7,VM8,RES,STM |

| 英国10年期国债收益率 | 是 | RES,STM | 是 | VM7,VM8,RES,STM |

| 美国10年期国债收益率 | 是 | VM7,RES,STM | 是 | VM6,VM7,VM8,RES,STM |

| 韩国10年期国债收益率 | 是 | RES,STM | 是 | 无 |

| 英文地区推特文本经济不确定性指数 | 是 | VM7,RES,STM | 是 | VM7,VM8,STM |

| 美国地区推特文本经济不确定性指数 | 是 | 无 | 是 | RES,STM |

| 恐慌指数 | 是 | RES,STM | 否 | 无 |

"

"

"

| Hurst指数 | VM1 | VM2 | VM3 | VM4 | VM5 | VM6 | VM7 | VM8 | RES |

|---|---|---|---|---|---|---|---|---|---|

| 芝加哥黄金 | 0.9937 | 0.9940 | 0.9651 | 0.8438 | 0.4142 | 0.1364 | -0.0767 | -0.0953 | -0.0078 |

| 分类结果 | 长期尺度模态(LTM) | 中期尺度模态(MTM) | 短期尺度模态(STM) | ||||||

| 伦敦黄金 | 0.9922 | 0.9952 | 0.9758 | 0.8436 | 0.5993 | 0.2051 | -0.0653 | -0.0840 | -0.0121 |

| 分类结果 | 长期尺度模态(LTM) | 中期尺度模态(MTM) | 短期尺度模态(STM) | ||||||

"

| Hurst指数 | 原始序列 | LTM | MTM | STM |

|---|---|---|---|---|

| 芝加哥黄金 | 0.4781 | 0.9735 | 0.5651 | -0.0328 |

| 预测子模型 | SPCA回归 | SPCA回归 | SPCA回归 | MCP回归 |

| 伦敦黄金 | 0.4745 | 0.9794 | 0.6420 | -0.0391 |

| 预测子模型 | SPCA回归 | SPCA回归 | SPCA回归 | MCP回归 |

"

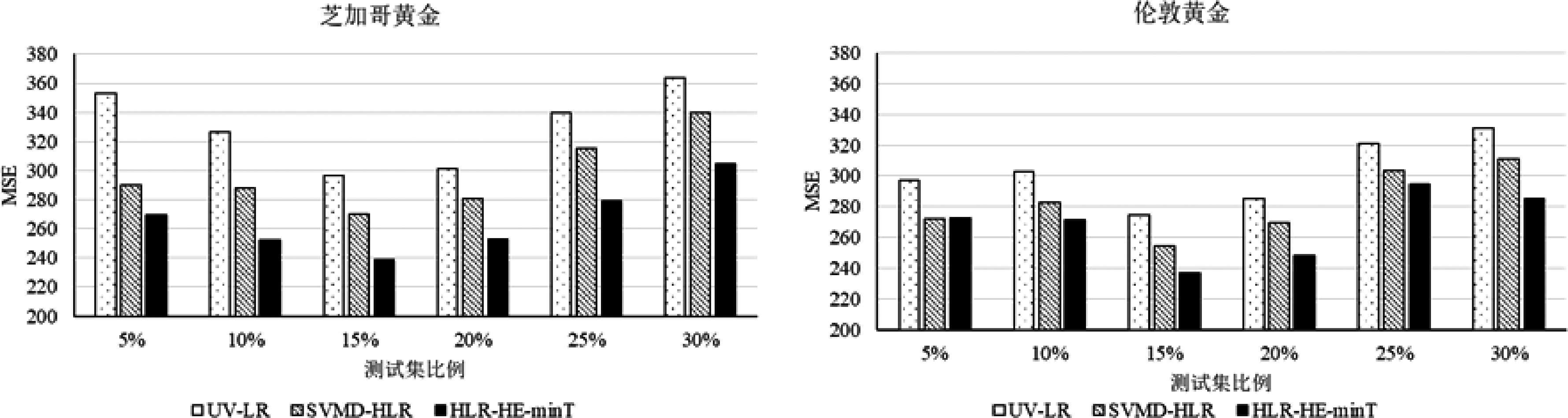

| 数据集 | 芝加哥黄金 | 伦敦黄金 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 预测模型 | MSE | MAE | D stat (%) | D/M | MSE | MAE | D stat (%) | D/M | |

| UV-LR | 296.8443 | 12.8515 | 53.78 | 76.28 | 274.7381 | 12.3111 | 52.44 | 77.61 | |

| SVMD-UV-LR | 292.1239 | 12.8125 | 52.89 | 75.23 | 273.7696 | 12.2915 | 52.22 | 77.39 | |

| MV-MCP | 297.8840 | 12.8130 | 51.11 | 72.74 | 277.8917 | 12.3349 | 46.89 | 69.29 | |

| MV-SPCA | 271.4506 | 12.8347 | 58.41 | 82.85 | 259.1138 | 12.5937 | 58.67 | 84.66 | |

| SVMD-MCP | 287.3581 | 12.6657 | 56.00 | 80.55 | 259.1964 | 11.9655 | 56.89 | 86.54 | |

| SVMD-SPCA | 278.3768 | 12.7978 | 56.22 | 80.04 | 266.1858 | 12.1785 | 58.00 | 86.71 | |

| SVMD-HLR | 268.7421 | 12.3836 | 57.78 | 85.05 | 254.4346 | 11.9089 | 59.78 | 91.38 | |

| SVMD-MR-MCP | 296.8475 | 13.0529 | 50.89 | 71.07 | 269.2959 | 12.2898 | 55.33 | 82.05 | |

| SVMD-MR-SPCA | 269.4559 | 12.5037 | 56.67 | 82.59 | 257.7426 | 11.9982 | 56.44 | 85.65 | |

| SVMD-MTD-HLR | 260.2057 | 12.1709 | 58.67 | 87.87 | 249.7207 | 11.8350 | 59.56 | 91.64 | |

| HLR-SVR | 334.6570 | 14.0353 | 59.56 | 77.08 | 291.7949 | 13.0435 | 58.89 | 82.11 | |

| LR-HE-minT | 295.2399 | 12.8258 | 53.11 | 67.44 | 274.6680 | 12.2752 | 54.89 | 81.44 | |

| SPCA-HE-minT | 11.6965 | ||||||||

| HLR-HE-minT | 242.1298 | 11.7271 | 62.44 | 97.07 | 236.9659 | 62.00 | 96.43 | ||

"

| 预测模型 | 芝加哥黄金 | 伦敦黄金 |

|---|---|---|

| SVMD-UV-LR | -0.384 | 0.480 |

| MV-MCP | -0.504 | 0.249 |

| MV-SPCA | -0.003 | 0.859 |

| SVMD-MCP | -1.091 | -2.257* |

| SVMD-SPCA | -0.152 | -0.786 |

| SVMD-HLR | -2.263* | -2.837** |

| SVMD-MR-MCP | 1.274 | -0.154 |

| SVMD-MR-SPCA | -1.131 | -1.584 |

| SVMD-MTD-HLR | -3.181*** | -3.173** |

| HLR-SVR | 2.867** | 1.935 |

| LR-HE-minT | -0.521 | -0.913 |

| SPCA-HE-minT | -3.435*** | -3.023** |

| HLR-HE-minT | -4.392*** | -3.017** |

"

"

| 数据集 | 芝加哥黄金 | 伦敦黄金 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 预测模型 | MSE | MAE | D stat (%) | D/M | MSE | MAE | D stat (%) | D/M | |

| SVMD-C-LR | 327.8487 | 13.8126 | 52.22 | 68.79 | |||||

| SVMD-B-LR | 298.0214 | 12.9116 | 51.11 | 72.15 | 274.7381 | 12.3111 | 52.44 | 77.61 | |

| FixFreVMD-C-LR | 330.0396 | 13.8498 | 51.56 | 67.73 | 294.4208 | 13.1148 | 51.33 | 71.29 | |

| FixFreVMD-B-LR | 322.5728 | 13.5973 | 51.78 | 296.4623 | 13.1438 | 52.67 | 72.99 | ||

| FixloopVMD-C-LR | 423.1488 | 15.7798 | 54.89 | 63.22 | 325.7307 | 13.6047 | 52.00 | 69.58 | |

| FixloopVMD-B-LR | 429.6582 | 15.7663 | 52.00 | 59.98 | 404.1694 | 15.2342 | 52.67 | 63.02 | |

| OriginVMD-C-LR | 536.3667 | 17.8578 | 51.78 | 52.69 | 368.2220 | 14.5860 | 50.89 | 63.45 | |

| OriginVMD-B-LR | 461.9472 | 16.5685 | 52.44 | 57.54 | 459.9807 | 16.6394 | 53.33 | 58.37 | |

| ICEEMDAN-C-LR | 385.6285 | 15.0648 | 50.44 | 61.09 | 335.4319 | 14.0542 | 50.22 | 65.13 | |

| ICEEMDAN-B-LR | 399.0081 | 15.0950 | 55.11 | 66.45 | 366.6509 | 14.3582 | 53.11 | 67.32 | |

| EMD-C-LR | 515.4149 | 17.3192 | 55.49 | 2767.7068 | 40.8141 | 51.33 | 22.99 | ||

| EMD-B-LR | 539.5172 | 18.0621 | 45.78 | 46.24 | 571.5142 | 18.8239 | 48.44 | 46.95 | |

| DWT-C-LR | 395.1280 | 15.1754 | 50.00 | 60.02 | 343.6984 | 13.9168 | 53.33 | 69.78 | |

| DWT-B-LR | 377.0423 | 14.6884 | 65.54 | 363.1614 | 14.5267 | 52.44 | 65.75 | ||

| SSA-C-LR | 407.4101 | 16.0148 | 46.00 | 52.39 | 320.8109 | 14.1457 | 47.33 | 61.01 | |

| SSA-B-LR | 308.0430 | 13.6496 | 46.89 | 62.69 | 325.8507 | 13.8043 | 47.11 | 62.30 | |

"

"

| 数据集 | 芝加哥黄金 | 伦敦黄金 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 预测模型 | MSE | MAE | D stat (%) | D/M | MSE | MAE | D stat (%) | D/M | |

| SVMD-RF-RFE | 420.9253 | 15.4028 | 57.11 | 67.81 | 518.0661 | 17.9090 | 49.11 | 49.89 | |

| SVMD-GBDT | 336.0971 | 13.8461 | 53.78 | 70.73 | 356.0066 | 14.3416 | 54.67 | 69.32 | |

| SVMD-XGBoost | 347.8793 | 14.1455 | 50.89 | 65.41 | 327.9640 | 13.7461 | 53.56 | 70.84 | |

| SVMD-LightGBM | 329.3842 | 13.8780 | 51.78 | 67.86 | 308.1727 | 13.3176 | 54.00 | 73.69 | |

| SVMD-SVM-RFE | 289.6998 | 12.8452 | 53.33 | 75.68 | 269.1036 | 12.1347 | 55.78 | 83.67 | |

| SVMD-GRNN | 293.9155 | 12.8797 | 52.67 | 74.44 | 284.5915 | 12.7583 | 51.33 | 73.24 | |

| SVMD-LSTM | 292.0098 | 12.8331 | 53.56 | 76.01 | 271.7906 | 12.3726 | 54.67 | 80.43 | |

| SVMD-GRU | 332.5922 | 13.9642 | 53.11 | 69.13 | 292.2901 | 12.8820 | 54.00 | 76.09 | |

| SVMD-PLS | 292.1650 | 12.8039 | 53.56 | 76.23 | 274.6803 | 12.3561 | 52.67 | 77.60 | |

| SVMD-Lasso | 290.4264 | 12.7861 | 53.78 | 76.64 | 56.89 | 85.51 | |||

| SVMD-MCP | 287.3581 | 56.00 | 80.55 | 258.9699 | 11.9655 | 87.55 | |||

| SVMD-PCA | 80.02 | 271.6163 | 12.4526 | 55.11 | 80.52 | ||||

| SVMD-SPCA | 278.3768 | 12.7978 | 56.22 | 266.1858 | 12.1785 | 58.00 | |||

"

"

| [1] | 谭德凯, 田利辉. 黄金是股票市场的“避险天堂”吗?——基于动态条件相关混频数据抽样模型[J]. 中国管理科学, 2022, 30(10): 14-24. |

| Tan D K, Tian L H. Is gold a safe haven of the stock market? Based on dynamic conditional correlation mixed data sampling model[J]. Chinese Journal of Management Science, 2022, 30(10): 14-24. | |

| [2] | Koziuk V. Role of gold in foreign exchange reserves of commodity exporting countries[J]. Journal of European Economy, 2021, 20(2): 211-232. |

| [3] | Arslanalp S, Eichengreen B, Simpson-Bell C. Gold as international reserves: A barbarous relic no more?[J]. Journal of International Economics, 2023, 145: 103822. |

| [4] | Pattnaik D, Hassan M K, DSouza A, et al. Investment in gold: A bibliometric review and agenda for future research[J]. Research in International Business and Finance, 2023, 64: 101854. |

| [5] | 郭杨莉, 马锋. 基于马尔科夫和混频数据模型的黄金期货市场波动率预测研究[J]. 中国管理科学, 2024, 32(1): 13-22. |

| Guo Y L, Ma F. Forecasting the Chinese gold futures market volatility using Markov-switching regime and mixed data sampling model[J]. Chinese Journal of Management Science, 2024, 32(1): 13-22. | |

| [6] | 吕永健, 符廷銮, 胡颖毅, 等. 基于拔靴滤波历史模拟法的黄金市场VaR测度研究[J]. 中国管理科学, 2019, 27(7): 46-55. |

| Lv Y J, Fu T L, Hu Y Y, et al. A study of risk measurements of Chinese gold market based on bootstraped filtered historical simulation approaches[J]. Chinese Journal of Management Science, 2019, 27(7): 46-55. | |

| [7] | 范彩云, 童君逸, 程俊彦, 等. 基于ML-DMA的黄金期货价格预测研究[J]. 数理统计与管理, 2024, 43(3): 541-558. |

| Fan C Y, Tong J Y, Cheng J Y, et al. Gold futures price forecasting based on ML-DMA[J]. Journal of Applied Statistics and Management, 2024, 43(3): 541-558. | |

| [8] | 王海燕, 盛昭瀚. 大数据驱动的复杂系统管理情景建模: 技术与流程[J]. 中国管理科学, 2025, 33(1): 22-33. |

| Wang H Y, Sheng Z H. Modeling of complex system management scenarios driven by big data: Techniques and processes[J]. Chinese Journal of Management Science, 2025, 33(1): 22-33. | |

| [9] | 王方, 张颂扬, 余乐安, 等. 数据特征驱动的单变量预测建模研究[J]. 计量经济学报, 2024, 4(4): 1124-1148. |

| Wang F, Zhang S Y, Yu L A, et al. Data-trait-driven univariate predictive modeling[J]. China Journal of Econometrics, 2024, 4(4): 1124-1148. | |

| [10] | Yu L, Wang Z, Tang L. A decomposition–ensemble model with data-characteristic-driven reconstruction for crude oil price forecasting[J]. Applied Energy, 2015, 156: 251-267. |

| [11] | 柴建, 寇红红. 基于TEI@I方法论的系统管理预测技术研究综述及展望[J]. 管理评论, 2020, 32(7): 280-292. |

| Chai J, Kou H H. Review and prospect of system management prediction technology based on TEI@I methodology[J]. Management Review, 2020, 32(7): 280-292. | |

| [12] | 高晓辉, 周坤, 李廉水. 基于XGBOOST和ELM的混合空气质量预警系统: 以南京为例[J]. 中国管理科学, 2023, 31(5): 269-278. |

| Gao X H, Zhou K, Li L S. Hybrid air quality early warning system based on XGBoost and ELM: A case study of Nanjing[J]. Chinese Journal of Management Science, 2023, 31(5): 269-278. | |

| [13] | 曾能民, 张明, 余乐安. 基于“拆分-填充-分解-集成”的我国线上零售额预测研究[J]. 中国管理科学, 2022, 30(12): 63-76. |

| Zeng N M, Zhang M, Yu L A. Forecasting online retail sales of China based on splitting-filling-decomposition-ensemble model[J]. Chinese Journal of Management Science, 2022, 30(12): 63-76. | |

| [14] | 梁小珍, 赵欣, 杨明歌, 等. 基于二次分解和模型选择策略的港口集装箱吞吐量组合预测[J]. 管理评论, 2024, 36(8): 52-64. |

| Liang X Z, Zhao X, Yang M G, et al. A combination forecast method of port container throughput based on secondary decomposition and model selection strategy[J]. Management Review, 2024, 36(8): 52-64. | |

| [15] | 李霞, 李守伟. 基于EMD与DVG的非线性时间序列预测模型及其应用研究[J]. 中国管理科学, 2022, 30(9): 275-286. |

| Li X, Li S W. Non-linear time series prediction model based on EMD and DVG and its application[J]. Chinese Journal of Management Science, 2022, 30(9): 275-286. | |

| [16] | 杨晨, 陈贵词. 基于EMD-LSTM的国际黄金期货价格预测[J]. 中南民族大学学报(自然科学版), 2023, 42(6): 857-864. |

| Yang C, Chen G C. International gold futures price forecast based on EMD-LSTM[J]. Journal of South-Central Minzu University (Natural Science Edition), 2023, 42(6): 857-864. | |

| [17] | Yang M, Wang R, Zeng Z, et al. Improved prediction of global gold prices: An innovative Hurst-reconfiguration-based machine learning approach[J]. Resources Policy, 2024, 88: 104430. |

| [18] | 何林芸. 基于ICEEMDAN-SE-SSA-ELM算法的黄金期货价格预测[J]. 兰州文理学院学报(自然科学版), 2023, 37(1):35-39. |

| He L Y. Gold futures price forecast based on ICEEMDAN-SE-SSA-ELM algorithm[J]. Journal of Lanzhou University of Arts and Science (Natural Sciences), 2023, 37(1): 35-39. | |

| [19] | Lu W, Qiu T, Shi W, et al. International gold price forecast based on CEEMDAN and support vector regression with grey wolf algorithm[J]. Complexity, 2022, 2022(1): 1511479. |

| [20] | Liang Y, Lin Y, Lu Q. Forecasting gold price using a novel hybrid model with ICEEMDAN and LSTM-CNN-CBAM[J]. Expert Systems with Applications, 2022, 206: 117847. |

| [21] | 秦全德, 黄兆荣, 周至昊, 等. 基于包络熵的双层分解流感预测模型研究[J]. 系统工程理论与实践, 2023, 43(12): 3505-3519. |

| Qin Q D, Huang Z R, Zhou Z H, et al. A two-layer decomposition model based on envelope entropy for influenza forecasting[J]. Systems Engineering-Theory & Practice, 2023, 43(12): 3505-3519. | |

| [22] | 陈凯杰, 唐振鹏, 吴俊传, 等. 贵金属期货价格预测方法及实证研究[J]. 中国管理科学, 2022, 30(12): 245-253. |

| Chen K J, Tang Z P, Wu J C, et al. Prediction method and empirical study of precious metal futures Price[J]. Chinese Journal of Management Science, 2022, 30(12): 245-253. | |

| [23] | E J, Ye J, Jin H. A novel hybrid model on the prediction of time series and its application for the gold price analysis and forecasting[J]. Physica A: Statistical Mechanics and Its Applications, 2019, 527: 121454. |

| [24] | 范丽伟, 董欢欢, 渐令, 等. 基于滚动时间窗的碳市场价格分解集成预测研究[J]. 中国管理科学, 2023, 31(1): 277-286. |

| Fan L W, Dong H H, Jian L, et al. A Decomposition ensemble model with sliding time window for forecasting carbon market prices [J]. Chinese Journal of Management Science, 2023, 31(1): 277-286. | |

| [25] | Chen Y, Yu S, Islam S, et al. Decomposition-based wind power forecasting models and their boundary issue: An in-depth review and comprehensive discussion on potential solutions[J]. Energy Reports, 2022, 8: 8805-8820. |

| [26] | Barzegar R, Aalami M T, Adamowski J. Coupling a hybrid CNN-LSTM deep learning model with a Boundary Corrected Maximal Overlap Discrete Wavelet Transform for multiscale Lake water level forecasting[J]. Journal of Hydrology, 2021, 598: 126196. |

| [27] | 崔明明, 刘晓亭, 李秀婷, 等. 数据特征驱动的房地产市场集成预测研究[J].管理评论,2020, 32(7): 89-101. |

| Cui M M, Liu X T, Li X T, et al. Integrated data characteristic driven forecasting research on real estate market[J]. Management Review, 2020, 32(7): 89-101. | |

| [28] | Yu L, Ma M. A memory-trait-driven decomposition- reconstruction-ensemble learning paradigm for oil price forecasting[J]. Applied Soft Computing, 2021, 111: 107699. |

| [29] | 王方, 赵桉坤, 余乐安. 数据特征驱动的新能源汽车月度销量二次分解集成预测[J].中国管理科学, 2024, DOI:10.16381/j.cnki.issn1003-207x.2023.2035 . |

| Wang F, Zhao A K, Yu L A.Quadratic decomposition- ensemble method for multi-step forecast of monthly sales volume of new energy vehicles [J]. Chinese Journal of Management Science, 2024, DOI: 10.16381/j.cnki.issn1003-207x.2023.2035 . | |

| [30] | Yu L, Liang S, Chen R, et al. Predicting monthly biofuel production using a hybrid ensemble forecasting methodology[J]. International Journal of Forecasting, 2022, 38(1): 3-20. |

| [31] | 秦全德, 黄兆荣, 黄凯珊. 一种基于局部回归的多尺度碳市场价格预测模型研究[J]. 运筹与管理, 2022, 31(1): 107-114. |

| Qin Q D, Huang Z R, Huang K S. A multi-scale carbon price forecasting model withLocal regression approach[J]. Operations Research and Management Science, 2022, 31(1): 107-114. | |

| [32] | Athanasopoulos G, Hyndman R J, Kourentzes N, et al. Forecast reconciliation: A review[J]. International Journal of Forecasting, 2024, 40(2): 430-456. |

| [33] | Dragomiretskiy K, Zosso D. Variational mode decomposition[J]. IEEE Transactions on Signal Processing, 2014, 62(3): 531-544. |

| [34] | Huang D, Jiang F, Li K, et al. Scaled PCA: A new approach to dimension reduction[J]. Management Science, 2022, 68(3): 1678-1695. |

| [35] | Wang J, Guo X, Tan X, et al. Which exogenous driver is informative in forecasting European carbon volatility: Bond, commodity, stock or uncertainty?[J]. Energy Economics, 2023, 117: 106419. |

| [36] | He M, Zhang Y, Wen D, et al. Forecasting crude oil prices: A scaled PCA approach[J]. Energy Economics, 2021, 97: 105189. |

| [37] | Zhang C H. Nearly unbiased variable selection under minimax concave penalty[J]. The Annals of Statistics, 2010, 38(2): 894-942. |

| [38] | 罗孝敏, 彭定涛, 张弦. 基于MCP正则的最小一乘回归问题研究[J]. 系统科学与数学, 2021, 41(8): 2327-2337. |

| Luo X M, Peng D T, Zhang X. On least absolute deviation regression problems with MCP regularization[J]. Journal of Systems Science and Mathematical Sciences, 2021, 41(8): 2327-2337. | |

| [39] | Lila M F, Meira E, Cyrino Oliveira F L. Forecasting unemployment in Brazil: A robust reconciliation approach using hierarchical data[J]. Socio-Economic Planning Sciences, 2022, 82: 101298. |

| [40] | Athanasopoulos G, Ahmed R A, Hyndman R J. Hierarchical forecasts for Australian domestic tourism[J]. International Journal of Forecasting, 2009, 25(1): 146-166. |

| [41] | Wickramasuriya S L, Athanasopoulos G, Hyndman R J. Optimal forecast reconciliation for hierarchical and grouped time series through trace minimization[J]. Journal of the American Statistical Association, 2019, 114(526): 804-819. |

| [42] | Cohen G, Aiche A. Forecasting gold price using machine learning methodologies[J]. Chaos, Solitons & Fractals, 2023, 175: 114079. |

| [43] | Gök R, Bouri E, Gemici E. Can Twitter-based economic uncertainty predict safe-haven assets under all market conditions and investment horizons?[J]. Technological Forecasting and Social Change, 2022, 185: 122091. |

| [44] | Hong Y, Ma F, Wang L, et al. How does the COVID-19 outbreak affect the causality between gold and the stock market? New evidence from the extreme Granger causality test[J]. Resources Policy, 2022, 78: 102859. |

| [45] | 蔡超敏, 凌立文, 牛超, 等. 国内猪肉市场价格的EMD-SVM集成预测模型[J]. 中国管理科学, 2016, 24(S1): 845-851. |

| Cai C M, Ling L W, Niu C, et al. Integration prediction of domestic pork market price based on empirical mode decomposition and support vector machine[J]. Chinese Journal of Management Science, 2016, 24(S1): 845-851. | |

| [46] | Xiao N, Xu Q S. Multi-step adaptive elastic-net: Reducing false positives in high-dimensional variable selection[J]. Journal of Statistical Computation and Simulation, 2015, 85(18): 3755-3765. |

| [47] | 刘金培, 罗瑞, 陈华友, 等. 非结构化数据驱动的混合二次分解汇率区间多尺度组合预测[J]. 中国管理科学, 2023, 31(6): 60-70. |

| Liu J P, Luo R, Chen H Y, et al. Multi-scale combination forecasting of interval exchange rate with hybrid secondary decomposition driven by unstructured data [J]. Chinese Journal of Management Science, 2023, 31(6): 60-70. | |

| [48] | Zhou F, Huang Z, Zhang C. Carbon price forecasting based on CEEMDAN and LSTM[J]. Applied Energy, 2022, 311: 118601. |

| [49] | Pan W T. Mixed modified fruit fly optimization algorithm with general regression neural network to build oil and gold prices forecasting model[J]. Kybernetes, 2014, 43(7): 1053-1063. |

| [50] | Wen F, Yang X, Gong X, et al. Multi-scale volatility feature analysis and prediction of gold price[J]. International Journal of Information Technology & Decision Making, 2017, 16(1): 205-223. |

| [51] | Roh T Y, Lee B Y, Xu Y. Extracting gold risk premium via dimension reduction tools: Implication on the gold-inflation relationship[J]. Applied Economics Letters,2024, DOI:10.1080/13504851.2024.23640021 . |

| [52] | Varshini A, Kayal P, Maiti M. How good are different machine and deep learning models in forecasting the future price of metals? Full sample versus sub-sample[J]. Resources Policy, 2024, 92: 105040. |

| [1] | Xia Liu, Yunyue Zhang, Mengqi Li, Yejun Xu. Quantum Supervised Game Model and Simulation Analysis for Manipulative Behavior in Trading Stock Market [J]. Chinese Journal of Management Science, 2025, 33(3): 24-33. |

| [2] | Dan-yang WANG,Lu-shi YAO. Mutual Funds' Dynamic Liquidity Risk Management [J]. Chinese Journal of Management Science, 2023, 31(10): 40-48. |

| [3] | SONG Yan, LIU Yue-ting, ZHANG Lu-guang. Heterogeneous Institutional Investors and Corporate Reputation:Social Responsibility: Intermediate Effect Test Based on Corporate Social Responsibility [J]. Chinese Journal of Management Science, 2023, 31(7): 103-114. |

| [4] | WANG Dan-yang, YAO Lu-shi. Mutual Funds’ Dynamic Liquidity Preference-Based on Expected Market Volatility and Investor Sentiment [J]. Chinese Journal of Management Science, 2023, 31(5): 39-48. |

| [5] | TANG Yong, ZHU Peng-fei. The Research on the Relationship between the Interest Rate And Volume in the P2P Lending Market——An Empirical Analysis Based on Data in Different Regulatory Periods [J]. Chinese Journal of Management Science, 2019, 27(7): 35-45. |

| [6] | QU Shao-jian, LU Yan-ling, JI Ying. The Analysis of Crowdfunding Financing Mechanism Based on Social Network [J]. Chinese Journal of Management Science, 2019, 27(3): 1-10. |

| [7] | YI Rong-hua, SHAO Jie-hao. International Comparison of Chinese Securities Market Competitiveness Based on DEA [J]. Chinese Journal of Management Science, 2019, 27(1): 11-21. |

| [8] | LIU Xue-wen. Study on the Optimization of Investor Sentiment Measure Indicators in Chinese Stock Market [J]. Chinese Journal of Management Science, 2019, 27(1): 22-33. |

| [9] | YI Rong-hua, JU Jin, LIU Jia-peng. Market Valuation Efficiency Measurementand Valuation Model Analysis-Based on Cross-listing Stocks [J]. Chinese Journal of Management Science, 2016, 24(1): 30-37. |

| [10] | YI Rong-hua, LIU Yun, LIU Jia-peng. The Measure on Relative Valuation Efficiency of Industries Based on DEA: Theory and Empirical Study [J]. Chinese Journal of Management Science, 2012, (3): 79-85. |

| [11] | WANG Ming-tao, ZHUANG Ya-ming. New Models for Measuring the Liquidity Risk of Stocks [J]. Chinese Journal of Management Science, 2011, 19(2): 1-9. |

| [12] | WU Wei-xing. Gradual Disclosure and Risky Asset Pricing [J]. Chinese Journal of Management Science, 2006, (2): 1-6. |

| [13] | WANG Gui-pu, CHI Ren-yong, CHEN Wei-zhong. Information Content of Insider Trading in China Securities Market and a Comparison with Market Manipulation [J]. Chinese Journal of Management Science, 2004, (4): 130-136. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||