主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2026, Vol. 34 ›› Issue (5): 21-34.doi: 10.16381/j.cnki.issn1003-207x.2024.1454

Previous Articles Next Articles

Pengfei Zhu1,2, Tuantuan Lu3( ), Yu Wei4, Sha Lin5

), Yu Wei4, Sha Lin5

Received:2024-08-26

Revised:2025-01-14

Online:2026-05-25

Published:2026-04-21

Contact:

Tuantuan Lu

E-mail:lutuantuan0624@163.com

CLC Number:

Pengfei Zhu,Tuantuan Lu,Yu Wei, et al. Research on Estimating Hedging Ratio in Stock Futures Using a Multi-Wavelet Denoising and Fractal Scale-Amplitude Dual Integration Method[J]. Chinese Journal of Management Science, 2026, 34(5): 21-34.

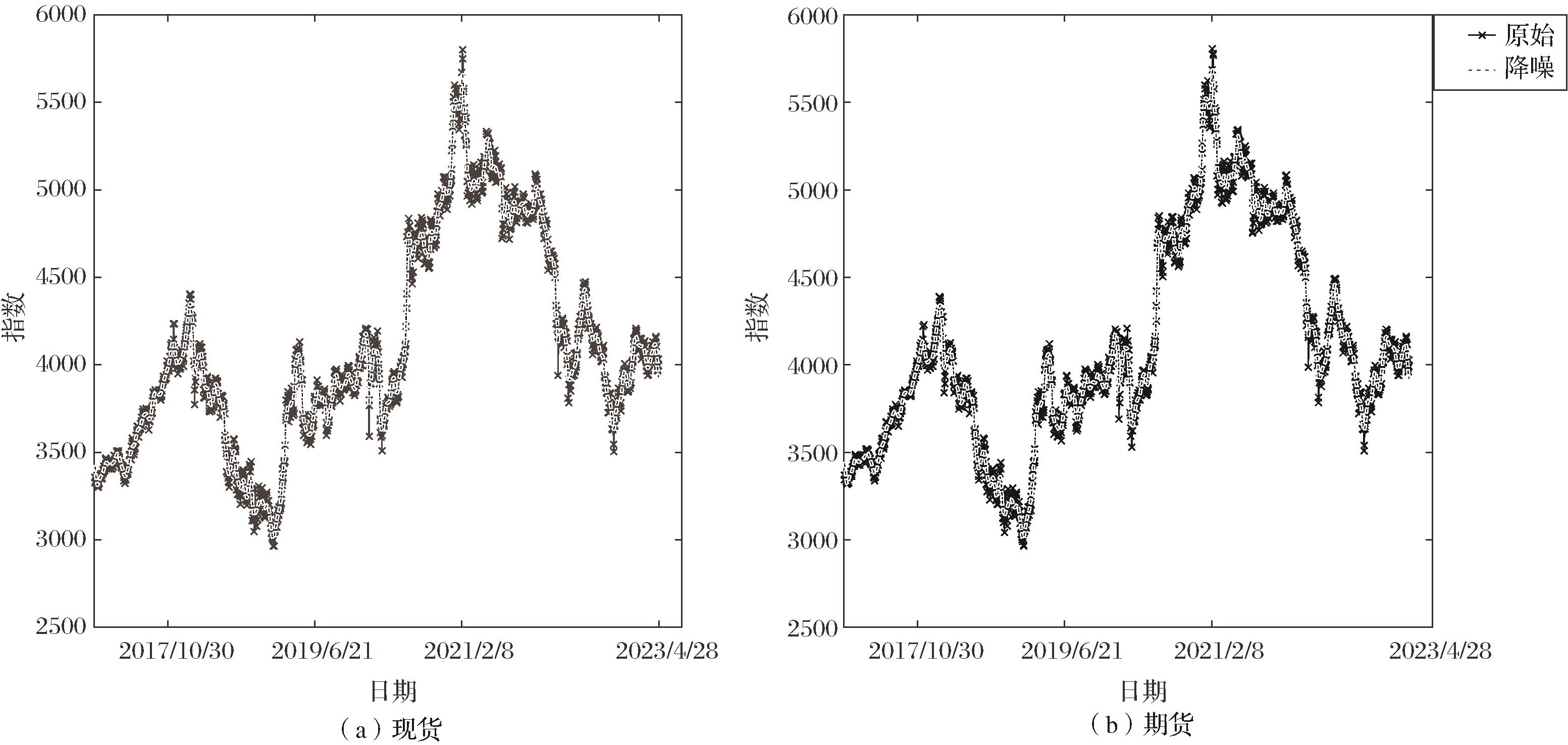

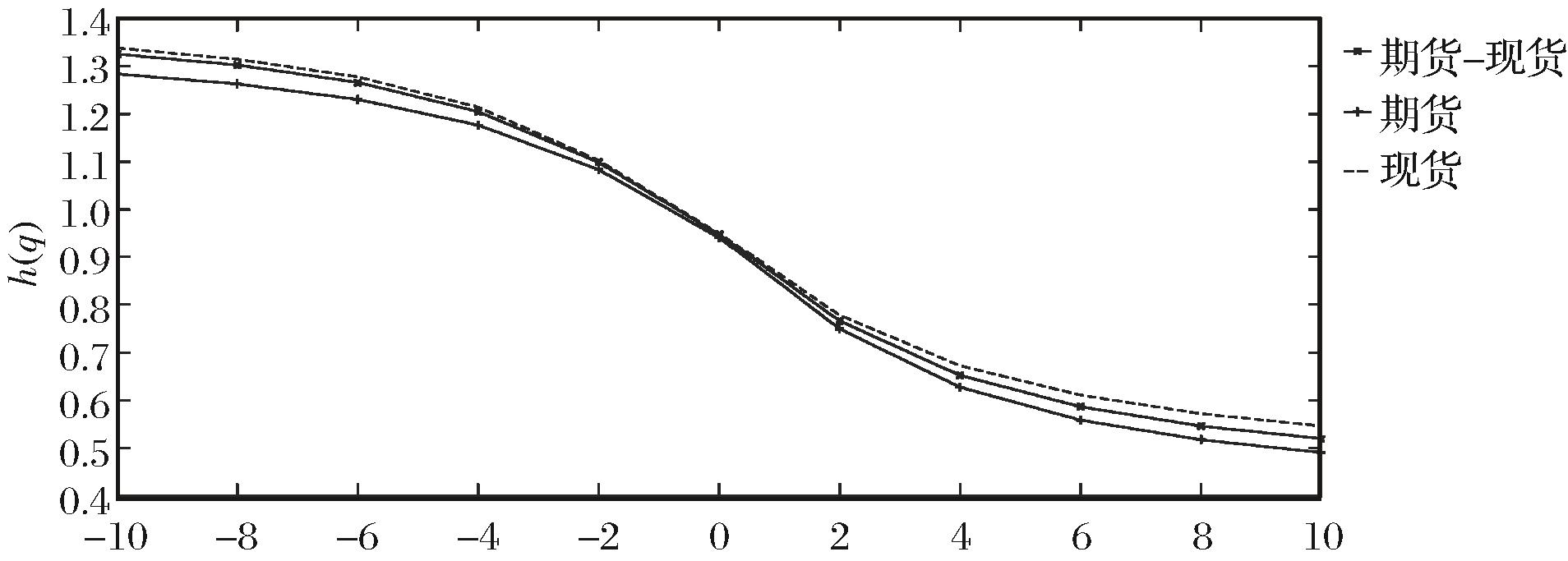

"

"

"

"

"

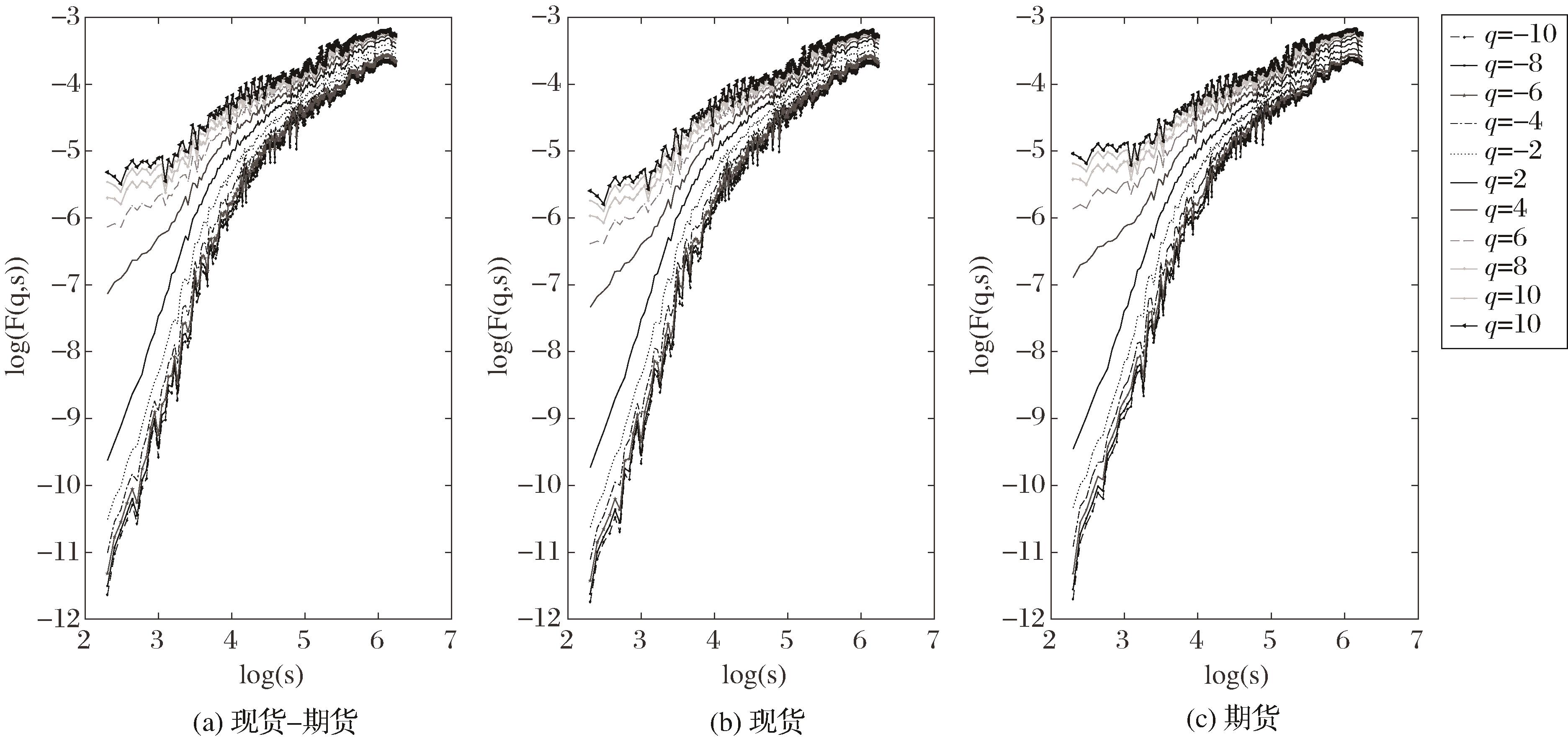

| 类别 | 均值 | 标准差 | 偏度 | 峰度 | JB | Q(5) | Q(10) | ADF |

|---|---|---|---|---|---|---|---|---|

| 期货 | 9.26E-5 | 0.005 | -1.299 | 35.441 | 67787.15*** | 2193.90*** | 2305.90*** | -12.816*** |

| 现货 | 8.89E-5 | 0.004 | -0.709 | 14.899 | 9189.98*** | 3085.10*** | 3238.20*** | -12.846*** |

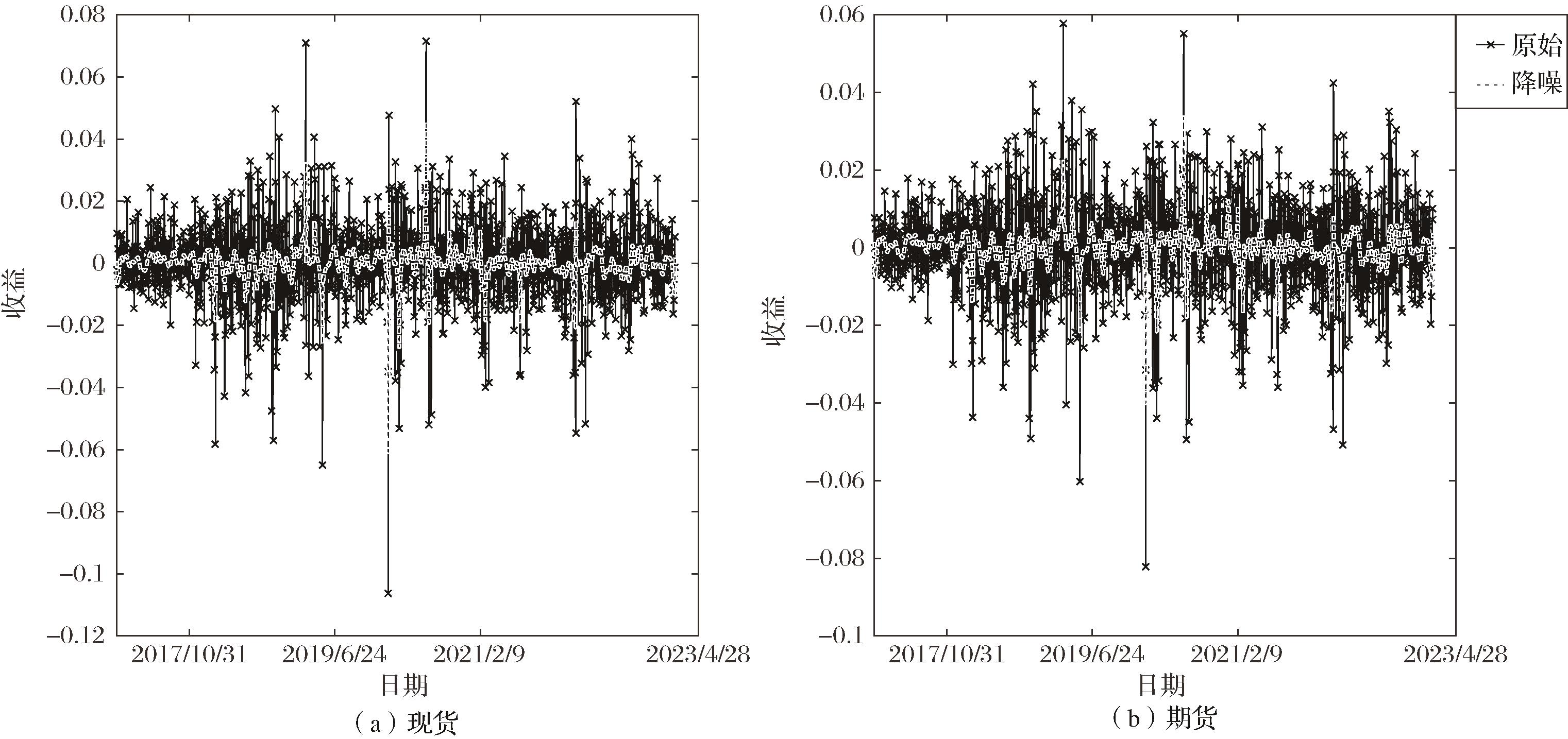

"

"

"

"

"

"

"

"

| 指标 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| AAR | 4.13E-4 | 3.99E-4 | 4.01E-4 | 3.86E-4 | 3.99E-4 | 4.17E-4 | 3.38E-4 | 5.11E-4 | 4.05E-4 | 5.15E-4# |

| VRR | 0.920 | 0.945 | 0.946 | 0.938 | 0.945 | 0.953 | 0.896 | 0.948 | 0.954 | 0.956# |

| RVR | 0.166 | 0.192 | 0.196 | 0.175 | 0.192 | 0.218 | 0.119 | 0.253 | 0.213 | 0.277# |

"

| 指标 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| AAR | 1.08E-4 | 7.30E-5 | 4.69E-5 | 7.33E-5 | 7.31E-5 | 6.97E-5 | 1.15E-4 | 3.24E-5 | -7.88E-5 | 1.23E-4# |

| VRR | 0.941 | 0.949 | 0.949 | 0.945 | 0.949 | 0.953# | 0.916 | 0.943 | 0.917 | 0.948 |

| RVR | 0.049 | 0.035 | 0.023 | 0.034 | 0.035 | 0.035 | 0.043 | 0.015 | NA | 0.059# |

"

| 指标 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| AAR | 2.84E-4 | 2.52E-4 | 2.53E-4 | 2.43E-4 | 2.52E-4 | 2.63E-4 | 2.14E-4 | 3.22E-4# | 2.94E-4 | 2.71E-4 |

| VRR | 0.924 | 0.942 | 0.943 | 0.935 | 0.942 | 0.950 | 0.893 | 0.937 | 0.947 | 0.958# |

| RVR | 0.118 | 0.120 | 0.122 | 0.109 | 0.120 | 0.135 | 0.075 | 0.147 | 0.147 | 0.152# |

"

| 指标 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| AAR | 3.49E-4 | 2.98E-4 | 3.01E-4 | 2.93E-4 | 3.00E-4 | 3.12E-4 | 2.55E-4 | 4.08E-4 | 3.51E-4 | 4.31E-4# |

| VRR | 0.914 | 0.935 | 0.937 | 0.932 | 0.937 | 0.942 | 0.890 | 0.920 | 0.944# | 0.942 |

| RVR | 0.138 | 0.136 | 0.139 | 0.130 | 0.138 | 0.150 | 0.089 | 0.167 | 0.171 | 0.206# |

"

| 指标 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 11 | 12 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| AAR | 4.13E-4 | 3.99E-4 | 4.01E-4 | 3.86E-4 | 3.99E-4 | 4.17E-4 | 3.38E-4 | 5.11E-4 | 4.05E-4 | 4.69E-4 | 5.23E-4# |

| VRR | 0.920 | 0.945 | 0.946 | 0.938 | 0.945 | 0.953 | 0.896 | 0.948 | 0.954 | 0.957# | 0.955# |

| RVR | 0.166 | 0.192 | 0.196 | 0.175 | 0.192 | 0.218 | 0.119 | 0.253 | 0.213 | 0.255# | 0.281# |

"

| 指标 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 13 | 14 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| AAR | 4.13E-4 | 3.99E-4 | 4.01E-4 | 3.86E-4 | 3.99E-4 | 4.17E-4 | 3.38E-4 | 5.11E-4 | 4.05E-4 | 5.03E-4 | 5.17E-4# |

| VRR | 0.920 | 0.945 | 0.946 | 0.938 | 0.945 | 0.953 | 0.896 | 0.948 | 0.954 | 0.955# | 0.955# |

| RVR | 0.166 | 0.192 | 0.196 | 0.175 | 0.192 | 0.218 | 0.119 | 0.253 | 0.213 | 0.267# | 0.276# |

"

| 指标 | 多小波降噪-分形标幅双集成法-FPA | 多小波降噪-分形标幅双集成法-MOFA |

|---|---|---|

| AAR | 5.24E-4# | 5.15E-4 |

| VRR | 0.953 | 0.956# |

| RVR | 0.273 | 0.277# |

"

| 保证金 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|

| 保证金8% | 4.10E-4 | 3.96E-4 | 3.99E-4 | 3.84E-4 | 3.97E-4 | 4.14E-4 | 3.36E-4 | 5.07E-4 | 3.99E-4 | 5.12E-4# |

| 保证金10% | 4.10E-4 | 3.96E-4 | 3.98E-4 | 3.83E-4 | 3.96E-4 | 4.14E-4 | 3.36E-4 | 5.06E-4 | 3.99E-4 | 5.11E-4# |

| 保证金20% | 4.07E-4 | 3.93E-4 | 3.95E-4 | 3.80E-4 | 3.93E-4 | 4.11E-4 | 3.34E-4 | 5.02E-4 | 3.97E-4 | 5.08E-4# |

| [1] | 韦立坚,张大卫,骆兴国,等. 股指期货市场的高频交易与价格发现[J].管理科学学报,2022, 25(1): 95-106. |

| Wei L J, Zhang D W, Luo X G, et al. High-frequency trading and price discovery in Chinese stock index futures market[J]. Journal of Management Sciences in China, 2022, 25(1): 95-106. | |

| [2] | 迟国泰, 余方平, 王玉刚. 基于动态规划多期期货套期保值优化模型研究[J]. 中国管理科学, 2010, 18(3): 17-24. |

| Chi G T, Yu F P, Wang Y G. Research on multi-period futures dynamic hedging model[J]. Chinese Journal of Management Science, 2010, 18(3): 17-24. | |

| [3] | 林昱, 常晋源, 黄雁勇. 融合经验模态分解与深度时序模型的股价预测[J]. 系统工程理论与实践, 2022, 42(6): 1663-1677. |

| Lin Y, Chang J Y, Huang Y Y. On the prediction of the stock price based on empirical mode decomposition and deep time series model[J]. Systems Engineering-Theory & Practice, 2022, 42(6): 1663-1677. | |

| [4] | Zhang C, Lan Q, Mi X, et al. A denoising method based on the nonlinear relationship between the target variable and input features[J]. Expert Systems with Applications, 2023, 218: 119585. |

| [5] | 朱鹏飞, 唐勇, 洪晓梅, 等. P2P网贷利率存在波动溢出吗?——基于时-频域溢出指数的实证研究[J]. 中国管理科学, 2021, 29(4): 82-92. |

| Zhu P F, Tang Y, Hong X M, et al. Does the P2P lending interest rate have volatility spillovers? An empirical study based on time-frequency domains spillover index[J]. Chinese Journal of Management Science, 2021, 29(4): 82-92. | |

| [6] | Feng Y, Yang J, Huang Q. Multiscale correlation analysis of Sino-US corn futures markets and the impact of international crude oil price: A new perspective from the multifractal method[J]. Finance Research Letters, 2023, 53: 103691. |

| [7] | Johnson L L. The Theory of Hedging and Speculation in Commodity Futures[J]. Review of Economic Studies, 1960, 27 (3):139-151. |

| [8] | Olson E, Vivian A, Wohar M E. Do commodities make effective hedges for equity investors?[J]. Research in International Business and Finance, 2017, 42: 1274-1288. |

| [9] | Thomson D, van Vuuren G. Attribution of hedge fund returns using a Kalman filter[J]. Applied Economics, 2018, 50(9): 1043-1058. |

| [10] | Choi S, Shin J. Bitcoin: An inflation hedge but not a safe haven[J]. Finance Research Letters, 2022, 46: 102379. |

| [11] | 孙洁, 金鑫, 张云. 不同市场状态下股指期货套期保值效率研究——异常波动事件的影响效应[J]. 系统工程理论与实践, 2023, 43(1): 76-90. |

| Sun J, Jin X, Zhang Y. The research on the hedging efficiency of CSI300 stock index futures in different market states: The impact of abnormal fluctuation[J]. Systems Engineering —Theory & Practice, 2023, 43(1): 76-90. | |

| [12] | Bouri E, Alsagr N. Hedging investment-grade and high-yield bonds with credit VIX[J]. Economics Letters, 2024, 237: 111630. |

| [13] | Aziz G, Sarwar S, Yuan Q, et al. Reinvestigating the role of oil and gold for portfolio optimization in view of COVID-19 and structural breaks: Empirical evidence of BEKK, DCC and wavelet quantile based estimations[J]. Resources Policy, 2024, 92: 104957. |

| [14] | 朱鹏飞, 唐勇, 卢团团, 等. 时-频域视角下最优套期保值比率研究——基于集成EEMD-SJC Copula-GARCHSK模型[J]. 系统工程理论与实践, 2020, 40(10): 2563-2580. |

| Zhu P F, Tang Y, Lu T T, et al. Optimal hedging ratio from time-frequency domain perspective: Based on integrated EEMD-SJC Copula-GARCHSK model[J]. Systems Engineering —Theory & Practice, 2020, 40(10): 2563-2580. | |

| [15] | Gong X L, Liu X H, Xiong X. Measuring tail risk with GAS time varying copula, fat tailed GARCH model and hedging for crude oil futures[J]. Pacific-Basin Finance Journal, 2019, 55: 95-109. |

| [16] | Zhu P, Lu T, Chen S. How do crude oil futures hedge crude oil spot risk after the COVID-19 outbreak? A wavelet denoising-GARCHSK-SJC Copula hedge ratio estimation method[J]. Physica A: Statistical Mechanics and Its Applications, 2022, 607: 128217. |

| [17] | Ren X, Yu X. Hedging performance analysis of energy markets: Evidence from copula quantile regression[J]. Journal of Futures Markets, 2024, 44(3): 432-450. |

| [18] | Cui T, Liu P. Computational modeling of financial system via a new fractal–fractional mathematical model[J]. Fractals, 2023, 31(10): 2340083. |

| [19] | Ling M J, Cao G X. Dynamics of asymmetric multifractal cross-correlations between cryptocurrencies and global stock markets: Role of gold and portfolio implications[J]. Chaos, Solitons & Fractals, 2024, 182: 114739. |

| [20] | Liang C, Xu Y, Chen Z, et al. Forecasting China’s stock market volatility with shrinkage method: Can Adaptive Lasso select stronger predictors from numerous predictors?[J]. International Journal of Finance & Economics, 2023, 28(4): 3689-3699. |

| [21] | Wang G J, Xie C, He L Y, et al. Detrended minimum-variance hedge ratio: A new method for hedge ratio at different time scales[J]. Physica A: Statistical Mechanics and Its Applications, 2014, 405: 70-79. |

| [22] | Wang X T, Li Z, Zhuang L. Risk preference, option pricing and portfolio hedging with proportional transaction costs[J]. Chaos, Solitons & Fractals, 2017, 95: 111-130. |

| [23] | 苑莹, 张同辉, 庄新田. 中国股市多分形波动率建模及预测研究[J]. 系统工程理论与实践, 2020, 40(9): 2269-2281. |

| Yuan Y, Zhang T H, Zhuang X T. Multifractal volatility forecast of Chinese stock market[J]. Systems Engineering —Theory & Practice, 2020, 40(9): 2269-2281. | |

| [24] | Mittal P. Forecasting of crude oil prices using wavelet decomposition based denoising with ARMA model[J]. Asia-Pacific Financial Markets,2024,31(2): 355-365. |

| [25] | Jena S K, Tiwari A K, Abakah E J A, et al. Integration between emerging market equity and global markets; is it fundamental or noisy? Evidence from wavelet denoised volatility spillover analysis in time and frequency domain[J]. Applied Economics, 2023, 55(12): 1312-1327. |

| [26] | 周坤, 高晓辉, 李廉水. 基于EMD-XGB-ELM和FSGM双元处理的碳排放交易价格集成预测[J]. 中国管理科学, 2024, 32(10): 325-334. |

| Zhou K, Gao X H, Li L S. Integrated carbon emission trading price prediction based on EMD-XGB-ELM and FSGM from the perspective of dual processing[J]. Chinese Journal of Management Science, 2024, 32(10): 325-334. | |

| [27] | Zhang S, Luo J, Wang S, et al. Oil price forecasting: A hybrid GRU neural network based on decomposition- reconstruction methods[J]. Expert Systems with Applications, 2023, 218: 119617. |

| [28] | Li G, Wei X, Yang H. Decomposition integration and error correction method for photovoltaic power forecasting[J]. Measurement, 2023, 208: 112462. |

| [29] | Li J, Liu D. Carbon price forecasting based on secondary decomposition and feature screening[J]. Energy, 2023, 278: 127783. |

| [30] | Yang F, Huang G. An optimized decomposition integration model for deterministic and probabilistic air pollutant concentration prediction considering influencing factors[J]. Atmospheric Pollution Research, 2024, 15(7): 102144. |

| [31] | Guo H, Xi Y, Yu F, et al. Time–frequency domain based optimization of hedging strategy: Evidence from CSI 500 spot and futures[J]. Expert Systems with Applications, 2024, 238: 121785. |

| [32] | He Y, Peng H, Deng C, et al. Reference point reconstruction-based firefly algorithm for irregular multi-objective optimization[J]. Applied Intelligence, 2023, 53(1): 962-983. |

| [33] | Wang J, Liu H, Sun J, et al. Research on concrete early shrinkage characteristics based on machine learning algorithms for multi-objective optimization[J]. Journal of Building Engineering, 2024, 89: 109415. |

| [34] | Wang J, Zhang L, Liu Z, et al. A novel decomposition-ensemble forecasting system for dynamic dispatching of smart grid with sub-model selection and intelligent optimization[J]. Expert Systems with Applications, 2022, 201: 117201. |

| [35] | Lu P, Yang J, Ye L, et al. A novel adaptively combined model based on induced ordered weighted averaging for wind power forecasting[J]. Renewable Energy, 2024, 226: 120350. |

| [36] | Zheng C, Su K, Yao Y. Hedging futures performance with denoising and noise-assisted strategies[J]. The North American Journal of Economics and Finance, 2021, 58: 101466. |

| [37] | 罗长青, 刘澜, 朱慧明, 等. 基于多尺度信息份额模型的原油市场定价能力动态演变研究[J]. 中国管理科学, 2024, 32(6): 1-12. |

| Luo C Q, Liu L, Zhu H M, et al. An empirical study on the dynamic evolution of crude oil market pricing power based on multi-scale information share model[J]. Chinese Journal of Management Science, 2024, 32(6): 1-12. | |

| [38] | Fenn G W, Kupiec P. Prudential margin policy in a futures-style settlement system[J]. Journal of Futures Markets, 1993, 13(4): 389-408. |

| [1] | PENG Hong-feng, CHEN Yi. The Estimation of Optimal Hedging Ratioof Copper Future Market of China——Based on Markov Regime-Switching GARCH Model [J]. Chinese Journal of Management Science, 2015, 23(5): 14-22. |

| [2] | PENG Hong-feng, YE Yong-gang. The Evaluation and Comparison Research of Dynamic Optimal Hedging Ratios Based on Modified ECM-GARCH [J]. Chinese Journal of Management Science, 2007, 15(5): 29-35. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||