主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2026, Vol. 34 ›› Issue (4): 22-33.doi: 10.16381/j.cnki.issn1003-207x.2022.1305

Previous Articles Next Articles

Xinyu Wu1( ), Xuebao Yin1, Haibin Xie2, Chaoqun Ma3

), Xuebao Yin1, Haibin Xie2, Chaoqun Ma3

Received:2022-06-16

Revised:2024-07-19

Online:2026-04-25

Published:2026-03-27

Contact:

Xinyu Wu

E-mail:xywu@aufe.edu.cn

CLC Number:

Xinyu Wu,Xuebao Yin,Haibin Xie, et al. Option Pricing with Component Realized EGARCH Model[J]. Chinese Journal of Management Science, 2026, 34(4): 22-33.

"

| 价值状态 | DTM < 30 | 30 < DTM < 60 | 60 < DTM < 120 | DTM > 120 | All |

|---|---|---|---|---|---|

| 合约数目 | |||||

| S/K< 0.94 | 1417 | 1071 | 1376 | 1542 | 5406 |

| 0.94 <S/K< 0.97 | 508 | 456 | 432 | 659 | 2055 |

| 0.97 <S/K< 1.00 | 531 | 480 | 447 | 682 | 2140 |

| All | 2456 | 2007 | 2255 | 2883 | 9601 |

| 平均价格 | |||||

| S/K< 0.94 | 0.0043 | 0.0153 | 0.0324 | 0.0775 | 0.0345 |

| 0.94 <S/K< 0.97 | 0.0149 | 0.0379 | 0.0717 | 0.1196 | 0.0655 |

| 0.97 <S/K< 1.00 | 0.0338 | 0.0638 | 0.1030 | 0.1536 | 0.0932 |

| All | 0.0128 | 0.0320 | 0.0539 | 0.1052 | 0.0542 |

| 平均隐含波动率 | |||||

| S/K< 0.94 | 0.3528 | 0.2715 | 0.2627 | 0.2417 | 0.2821 |

| 0.94 <S/K< 0.97 | 0.2237 | 0.2075 | 0.2094 | 0.2014 | 0.2100 |

| 0.97 <S/K< 1.00 | 0.2066 | 0.2005 | 0.2020 | 0.1974 | 0.2013 |

| All | 0.2945 | 0.2400 | 0.2405 | 0.2220 | 0.2486 |

"

"

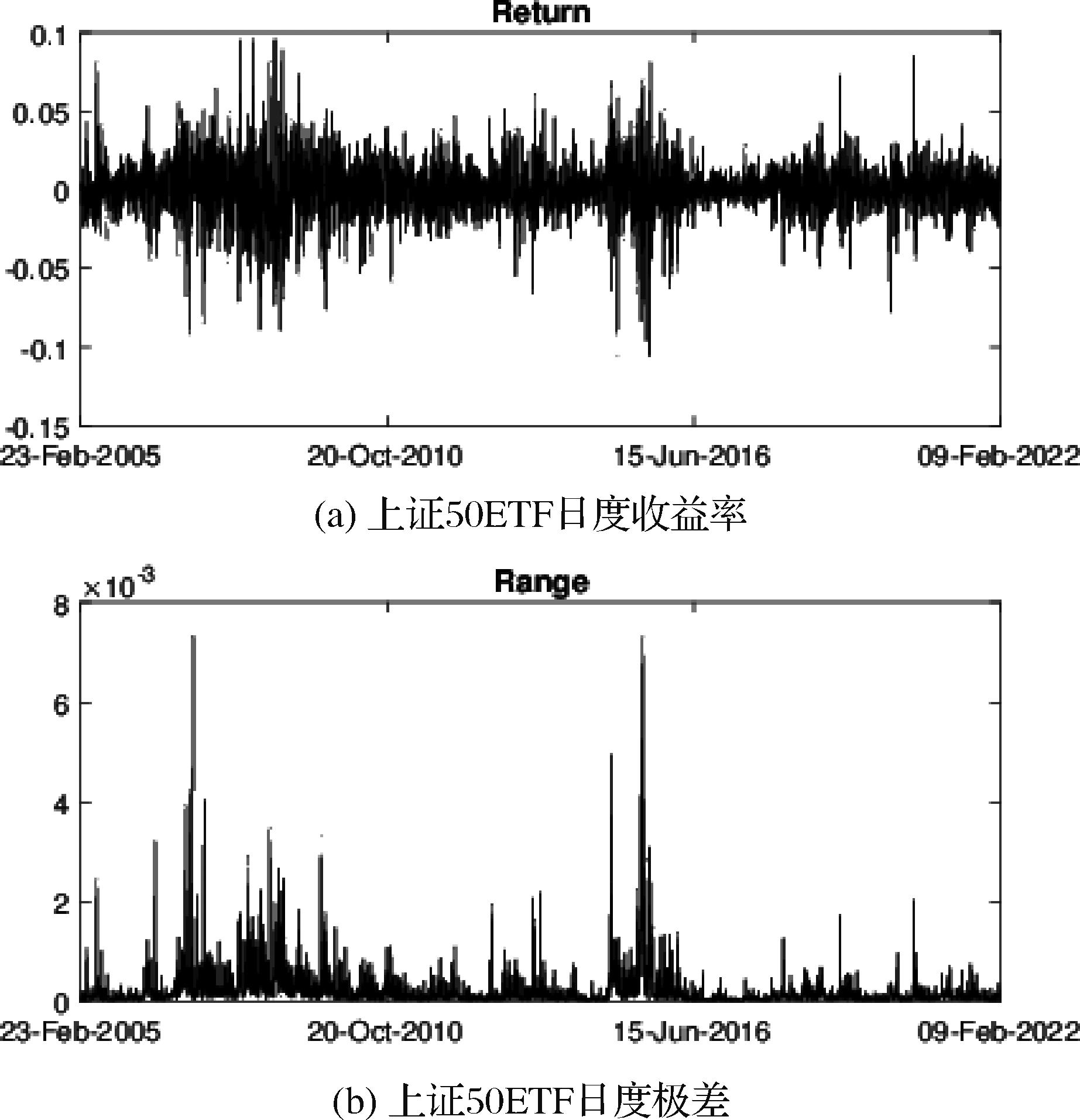

| 统计量 | 收益率 | 极差 | 对数极差 |

|---|---|---|---|

| 样本数 | 4123 | 4123 | 4123 |

| 均值 | 0.0003 | 0.0002 | -9.2080 |

| 最小值 | -0.1052 | 0.0000 | -12.5720 |

| 最大值 | 0.0955 | 0.0073 | -4.9171 |

| 标准差 | 0.0170 | 0.0004 | 1.1739 |

| 偏度 | -0.1669 | 6.9482 | 0.2722 |

| 峰度 | 8.0099 | 79.6974 | 3.0168 |

| Q(10) | 38.6646 | 4265.4813 | 10273.9500 |

"

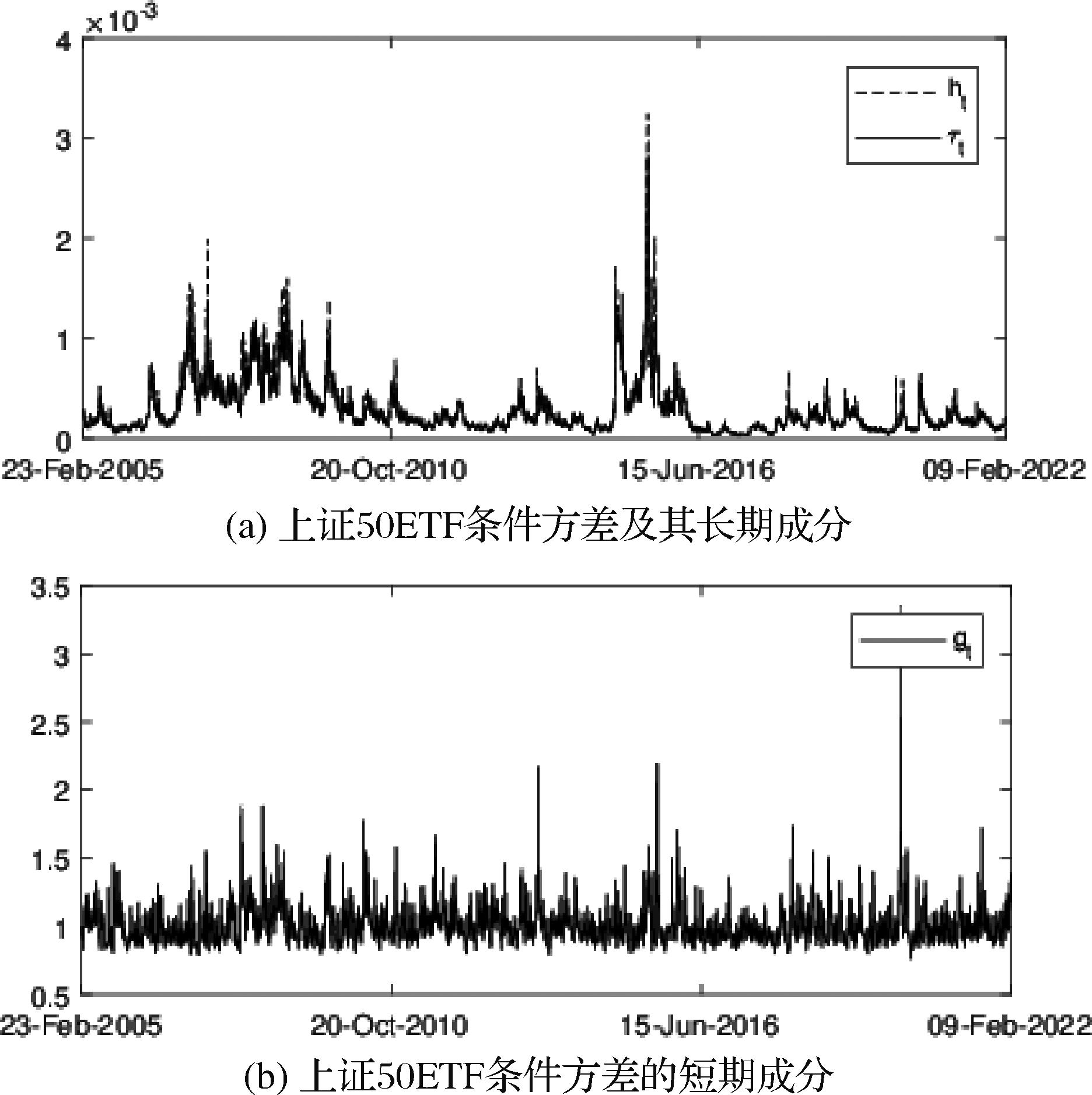

| 参数 | EGARCH | C-EGARCH | R-EGARCH | CR-EGARCH |

|---|---|---|---|---|

| 客观参数 | ||||

| 0.0270 | 0.0294 | 0.0305 | 0.0300 | |

| (0.0066) | (0.0062) | (0.0036) | (0.0038) | |

| -0.0797 | -0.0214 | -0.1216 | -0.0766 | |

| (0.0008) | (0.0004) | (0.0013) | (0.0010) | |

| 0.1084 | ||||

| (0.0026) | ||||

| 0.9968 | 0.9910 | |||

| (0.0001) | (0.0002) | |||

| 0.0097 | 0.0109 | |||

| (0.0030) | (0.0021) | |||

| 0.0789 | 0.0388 | |||

| (0.0033) | (0.0017) | |||

| 0.1372 | 0.0371 | |||

| (0.0025) | (0.0037) | |||

| 0.9892 | 0.9143 | 0.9857 | 0.7910 | |

| (0.0003) | (0.0089) | (0.0002) | (0.0057) | |

| -0.0068 | -0.0332 | -0.0160 | -0.0597 | |

| (0.0027) | (0.0053) | (0.0019) | (0.0038) | |

| 0.1574 | 0.1096 | 0.0527 | 0.0216 | |

| (0.0032) | (0.0075) | (0.0016) | (0.0025) | |

| -0.7385 | -0.7376 | |||

| (0.0030) | (0.0021) | |||

| 0.4789 | 0.4743 | |||

| (0.0092) | (0.0095) | |||

| 0.0628 | 0.0572 | |||

| (0.0039) | (0.0055) | |||

| 0.2575 | 0.2555 | |||

| (0.0032) | (0.0032) | |||

| 波动率风险溢价 | ||||

| 0.1266 | 0.0748 | |||

| (0.0104) | (0.0101) | |||

| 对数似然 | ||||

| 11530.5911 | 11542.8590 | 11577.6242 | 11581.3346 | |

| 7209.9617 | 7232.1409 | |||

| 2526.1689 | 2700.0491 | |||

"

"

| 模型 | B-S | EGARCH | C-EGARCH | R-EGARCH | CR-EGARCH |

|---|---|---|---|---|---|

| Overall IVRMSE | 0.0729 | 0.0775 | 0.0614 | 0.0547 | 0.0473 |

| IVRMSE by moneyness | |||||

| S/K< 0.94 | 0.0750 | 0.0732 | 0.0599 | 0.0564 | 0.0473 |

| 0.94 <S/K< 0.97 | 0.0695 | 0.0723 | 0.0565 | 0.0485 | 0.0423 |

| 0.97 <S/K< 1.00 | 0.0707 | 0.0917 | 0.0692 | 0.0558 | 0.0515 |

| IVRMSE by maturity | |||||

| DTM < 30 | 0.0679 | 0.0613 | 0.0516 | 0.0666 | 0.0560 |

| 30 < DTM < 60 | 0.0716 | 0.0547 | 0.0464 | 0.0455 | 0.0425 |

| 60 < DTM < 120 | 0.0760 | 0.0672 | 0.0558 | 0.0450 | 0.0413 |

| DTM > 120 | 0.0755 | 0.1058 | 0.0797 | 0.0561 | 0.0467 |

| [1] | Black F, Scholes M. The pricing of options and corporate liabilities[J]. Journal of Political Economy,1973,81(3): 637-654. |

| [2] | Yue T, Gehricke S A, Zhang J E, et al. The implied volatility smirk in the Chinese equity options market[J]. Pacific-Basin Finance Journal, 2021, 69: 101624. |

| [3] | Heston S L. A closed-form solution for options with stochastic volatility with applications to bond and currency options[J]. The Review of Financial Studies, 1993, 6(2): 327-343. |

| [4] | Duan J C. The garch option pricing model[J]. Mathematical Finance, 1995, 5(1): 13-32. |

| [5] | Heston S L, Nandi S. A closed-form GARCH option valuation model[J]. The Review of Financial Studies, 2000, 13(3): 585-625. |

| [6] | Merton R C. Option pricing when underlying stock returns are discontinuous[J]. Journal of Financial Economics, 1976, 3(1-2): 125-144. |

| [7] | Kou S G. A jump-diffusion model for option pricing[J]. Management Science, 2002, 48(8): 1086-1101. |

| [8] | Corsi F, Fusari N, La Vecchia D. Realizing smiles: Options pricing with realized volatility[J]. Journal of Financial Economics, 2013, 107(2): 284-304. |

| [9] | Christoffersen P, Feunou B, Jacobs K, et al. The economic value of realized volatility: Using high-frequency returns for option valuation[J]. The Journal of Financial and Quantitative Analysis, 2014, 49(3): 663-697. |

| [10] | Majewski A A, Bormetti G, Corsi F. Smile from the past: A general option pricing framework with multiple volatility and leverage components[J]. Journal of Econometrics, 2015, 187(2): 521-531. |

| [11] | Christoffersen P, Jacobs K, Ornthanalai C. GARCH option valuation: Theory and evidence[J]. The Journal of Derivatives, 2013, 21(2): 8-41. |

| [12] | Chorro C, Fanirisoa Zazaravaka R H. Discriminating between GARCH models for option pricing by their ability to compute accurate VIX measures[J]. Journal of Financial Econometrics, 2022, 20(5): 902-941. |

| [13] | Escobar-Anel M, Rastegari J, Stentoft L. Option pricing with conditional GARCH models[J]. European Journal of Operational Research, 2021, 289(1): 350-363. |

| [14] | Andersen T G, Bollerslev T, Diebold F X, et al. The distribution of realized stock return volatility[J]. Journal of Financial Economics, 2001, 61(1): 43-76. |

| [15] | 赵树然, 李金宸, 张洁, 等. 高频网络波动率矩阵模型构建及其应用[J].中国管理科学,2024, DOI:10.16381/j.cnki.issn1003-207x.2023.0115 . |

| Zhao S R, Li J C, Zhang J, et al. Construction and application of high-frequency network volatility matrix model[J]. Chinese Journal of Management Science, In Press, 2024,DOI:10.16381/j.cnki.issn1003-207x.2023.0115 . | |

| [16] | Hansen P R, Huang Z, Shek H H. Realized garch: A joint model for returns and realized measures of volatility[J]. Journal of Applied Econometrics, 2012, 27(6): 877-906. |

| [17] | Hansen P R, Huang Z. Exponential GARCH modeling with realized measures of volatility[J]. Journal of Business & Economic Statistics, 2016, 34(2): 269-287. |

| [18] | Huang Z, Wang T, Hansen P R. Option pricing with the realized GARCH model: An analytical approximation approach[J]. Journal of Futures Markets, 2017, 37(4): 328-358. |

| [19] | Tong C, Hansen P R, Huang Z. Option pricing with state-dependent pricing kernel[J]. Journal of Futures Markets, 2022, 42(8): 1409-1433. |

| [20] | Hansen P R, Huang Z, Tong C, et al. Realized GARCH, CBOE VIX, and the volatility risk premium[J]. Journal of Financial Econometrics, 2024, 22(1): 187-223. |

| [21] | Tong C, Huang Z. Pricing VIX options with realized volatility[J]. Journal of Futures Markets, 2021, 41(8): 1180-1200. |

| [22] | Park Y H. The roles of short-run and long-run volatility factors in options market: A term structure perspective[J/OL]. SSRN Electronic Journal, 2011. . |

| [23] | Bardgett C, Gourier E, Leippold M. Inferring volatility dynamics and risk premia from the S&P 500 and VIX markets[J]. Journal of Financial Economics, 2019, 131(3): 593-618. |

| [24] | 吴鑫育, 李心丹, 马超群. 基于期权与高频数据信息的VaR度量研究[J]. 中国管理科学, 2021, 29(8): 13-23. |

| Wu X Y, Li X D, Ma C Q. Measuring VaR based on the information content of option and high-frequency data[J]. Chinese Journal of Management Science, 2021, 29(8): 13-23. | |

| [25] | 朱福敏, 宋佳音, 郑尊信. 动态跳扩散双因子与长短期波动率: 来自期权市场的证据[J]. 系统工程理论与实践, 2024, 44(6): 1913-1933. |

| Zhu F M, Song J Y, Zheng Z X. Jump-Diffusion dynamics and long-short term volatility: Evidence from option pricing[J]. Systems Engineering —Theory & Practice, 2024, 44(6): 1913-1933. | |

| [26] | Wang F, Ghysels E. Econometric analysis of volatility component models[J]. Econometric Theory, 2015, 31(2): 362-393. |

| [27] | Conrad C, Kleen O. Two are better than one: Volatility forecasting using multiplicative component GARCH-MIDAS models[J]. Journal of Applied Econometrics, 2020, 35(1): 19-45. |

| [28] | 吴鑫育, 谢海滨, 李心丹. 基于双成分已实现EGARCH模型的VaR度量研究[J]. 数理统计与管理, 2021, 40(3): 556-570. |

| Wu X Y, Xie H B, Li X D. Measuring VaR based on two-component realized EGARCH model[J]. Jouranl of Applied Statistics and Management, 2021, 40(3): 556-570. | |

| [29] | Christoffersen P, Jacobs K, Ornthanalai C, et al. Option valuation with long-run and short-run volatility components[J]. Journal of Financial Economics, 2008, 90(3): 272-297. |

| [30] | Christoffersen P, Dorion C, Jacobs K, et al. Volatility components, affine restrictions, and nonnormal innovations[J]. Journal of Business & Economic Statistics, 2010, 28(4): 483-502. |

| [31] | 杨兴林, 王鹏. 基于时变波动率的50ETF参数欧式期权定价[J]. 数理统计与管理, 2018,37(1): 162-178. |

| Yang X L, Wang P. Parametric European option pricing of 50ETF options based on time-varying volatility[J]. Journal of Applied Statistics and Management, 2018, 37(1): 162-178. | |

| [32] | 周仁才. 基于波动率分解的期权定价[J]. 系统工程理论与实践, 2018, 38(8): 1919-1929. |

| Zhou R C. Option valuation based on volatility decomposition[J]. Systems Engineering-Theory & Practice, 2018, 38(8): 1919-1929. | |

| [33] | 吴鑫育, 李心丹, 马超群. 考虑微观结构噪声的非仿射期权定价研究——基于上证50ETF期权高频数据的实证分析[J].中国管理科学, 2017, 25(12): 99-108. |

| Wu X Y, Li X D, Ma C Q. Non-affine option pricing in the presence of microstructure noises: An empirical study based on the high-frequency Shanghai 50ETF options data[J]. Chinese Journal of Management Science, 2017, 25(12): 99-108. | |

| [34] | 孙有发, 吴碧云, 郭婷, 等. 非仿射随机波动率模型下的50ETF期权定价: 基于Fourier-Cosine方法[J]. 系统工程理论与实践, 2020, 40(4): 888-904. |

| Sun Y F, Wu B Y, Guo T, et al. Fourier-Cosine based option pricing for SSE 50 ETF under non-affine stochastic volatility model[J]. Systems Engineering —Theory & Practice, 2020, 40(4): 888-904. | |

| [35] | 吴鑫育, 赵凯, 李心丹, 等. 时变风险厌恶下的期权定价——基于上证50ETF期权的实证研究[J]. 中国管理科学, 2019, 27(11): 11-22. |

| Wu X Y, Zhao K, Li X D, et al. Option pricing under time-varying risk aversion: An empirical study based on SSE 50ETF options[J]. Chinese Journal of Management Science, 2019, 27(11): 11-22. | |

| [36] | 王西梅, 赵延龙, 史若诗, 等. 基于局部波动率模型的上证50ETF期权定价研究[J]. 系统工程理论与实践, 2019, 39(10): 2487-2501. |

| Wang X M, Zhao Y L, Shi R S, et al. Empirical analysis of Shanghai 50ETF options pricing based on local volatility model[J]. Systems Engineering-Theory & Practice, 2019, 39(10): 2487-2501. | |

| [37] | 瞿慧, 何佳诺. 基于已实现波动率的50ETF期权定价研究[J]. 管理科学, 2019, 32(3): 148-160. |

| Qu H, He J N. Pricing 50ETF options using realized volatility[J]. Journal of Management Science, 2019, 32(3): 148-160. | |

| [38] | 吴鑫育, 姜晓晴, 李心丹,等.基于已实现EGARCH-FHS模型的上证50ETF期权定价研究[J]. 中国管理科学, 2024, 32(3): 105-115. |

| Wu X Y, Jiang X Q, Li X D, et al. The pricing of SSE 50 ETF options with realized EGARCH-FHS model[J]. Chinese Journal of Management Science, 2024, 32(3): 105-115. | |

| [39] | Huang Z, Tong C, Wang T. Which volatility model for option valuation in China? Empirical evidence from SSE 50 ETF options[J]. Applied Economics, 2020, 52(17): 1866-1880. |

| [40] | 余湄, 程志勇, 邓军, 等. 一个新的期权定价方法: 基于混合次分数布朗运动的新视角[J]. 系统工程理论与实践, 2021, 41(11): 2761-2776. |

| Yu M, Cheng Z Y, Deng J, et al. A new option pricing method: Based on the perspective of sub-mixed fractional Brownian motion[J]. Systems Engineering-Theory & Practice, 2021, 41(11): 2761-2776. | |

| [41] | Byun S J, Jeon B H, Min B, et al. The role of the variance premium in Jump-GARCH option pricing models[J]. Journal of Banking & Finance, 2015, 59: 38-56. |

| [42] | Duan J C, Simonato J G. Empirical martingale simulation for asset prices[J]. Management Science, 1998, 44(9): 1218-1233. |

| [43] | Broadie M, Chernov M, Johannes M. Model specification and risk premia: Evidence from futures options[J]. The Journal of Finance, 2007, 62(3): 1453-1490. |

| [44] | Parkinson M. The extreme value method for estimating the variance of the rate of return[J]. The Journal of Business, 1980, 53(1): 61-65. |

| [45] | 沈根祥, 周泽峰. 拟得分驱动条件异方差自回归极差模型及其实证研究[J]. 中国管理科学, 2025, 33(5): 34-44. |

| Shen G X, Zhou Z F. Quasi score-driven conditional heteroskedastic autoregressive range model and it’s empirical study[J]. Chinese Journal of Management Science, 2025, 33(5): 34-44. |

| [1] | Genxiang Shen, Zefeng Zhou. Quasi Score-driven Conditional Heteroskedastic Autoregressive Range Model and It's Empirical Study [J]. Chinese Journal of Management Science, 2025, 33(5): 34-44. |

| [2] | Sicong Cheng,Tianyi Wang. Overnight Information and Option Pricing Model [J]. Chinese Journal of Management Science, 2024, 32(9): 1-10. |

| [3] | Xinyu Wu,Haibin Xie,Chaoqun Ma. Economic Policy Uncertainty and Renminbi Exchange Rate Volatility: Evidence from CARR-MIDAS Model [J]. Chinese Journal of Management Science, 2024, 32(8): 1-14. |

| [4] | Xinyu Wu,Xiaoqing Jiang,Xindan Li,Chaoqun Ma. The Pricing of SSE 50 ETF Options with Realized EGARCH-FHS Model [J]. Chinese Journal of Management Science, 2024, 32(3): 105-115. |

| [5] | Jiliang Sheng,Yi Huang,Juchao Li. Research on the Correlation Between Industry Risk and Industry Network Structure in China [J]. Chinese Journal of Management Science, 2024, 32(2): 199-209. |

| [6] | Xin-yu WU,Hai-bin XIE,Chao-qun MA. Score-driven Multiplicative Component Tealized CARR Model and its Empirical Study [J]. Chinese Journal of Management Science, 2023, 31(8): 214-225. |

| [7] | Jia-yi ZHOU, Lian-yong FENG, Jin-hong ZHU. A Model for Calculating the Value of Carbon Emission Rights Based on the Ideas of Biophysical Economics [J]. Chinese Journal of Management Science, 2023, 31(10): 96-105. |

| [8] | MA Ying-ying, WANG Guo-qiang, HU Xiao-xuan, LUO He. Weapon Target Assignment Method for Multiple UAVs in Beyond-Visual-Range Air Combat [J]. Chinese Journal of Management Science, 2022, 30(3): 248-257. |

| [9] | YIN Ya-hua, WU Heng-yu, ZHU Fu-min. VIX Option Pricing Based on Mean Reverting Model——From the Perspective of Calendar Time and Intrinsic Time [J]. Chinese Journal of Management Science, 2022, 30(2): 94-105. |

| [10] | LI Feng, ZHU Ping, LIANG Liang, KOU Gang. A Two-stage DEA Efficiency Evaluation Approach Based on Closest Targets [J]. Chinese Journal of Management Science, 2022, 30(10): 198-209. |

| [11] | WU Xin-yu, LI Xin-dan, MA Chao-qun. Measuring VaR Based on the Information Content of Option and High-frequency Data [J]. Chinese Journal of Management Science, 2021, 29(8): 13-23. |

| [12] | WANG Xian-dong, HE Jian-min. Pricing Asian Options under Uncertain Environment with Fuzziness and Randomness Considering Decision Maker's Subjective Judgment [J]. Chinese Journal of Management Science, 2020, 28(9): 33-44. |

| [13] | CHEN Mu-zi, ZHAO Ting-ting, LIU Cheng-lin, CHEN Min. Dynamic Evolution Study on Inter-sector Financial Institution Systemic Importance and Resonance Effects [J]. Chinese Journal of Management Science, 2020, 28(4): 36-47. |

| [14] | WU Ping, YUN Jun-chao, DONG Bin. “Pricing of CMS Digital Range Notes” Based on Multi-factor LIBOR Model [J]. Chinese Journal of Management Science, 2020, 28(3): 132-141. |

| [15] | HUANG Chuang-xia, WEN Shi-gang, YANG Xin, WEN Feng-hua, YANG Xiao-guang. The Interactive Relationship between Individual Investor Sentiment and Stock Price Behaviors [J]. Chinese Journal of Management Science, 2020, 28(3): 191-200. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||