主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2025, Vol. 33 ›› Issue (3): 80-92.doi: 10.16381/j.cnki.issn1003-207x.2022.0634cstr: 32146.14.j.cnki.issn1003-207x.2022.0634

汪刘凯, 张小波, 王未卿( ), 刘澄

), 刘澄

收稿日期:2022-03-29

修回日期:2022-08-10

出版日期:2025-03-25

发布日期:2025-04-07

作者简介:王未卿(1973-),女(汉族),天津人,北京科技大学经济管理学院,金融工程系主任兼书记,副教授,研究方向:金融科技与大数据分析、供应链金融、金融风险管理,E-mail: wangwq@manage.ustb.edu.cn.

基金资助:

Liukai Wang, Xiaobo Zhang, Weiqing Wang(), Cheng Liu

Received:2022-03-29

Revised:2022-08-10

Online:2025-03-25

Published:2025-04-07

摘要:

存货质押作为供应链金融的典型融资方式,质押物价值波动是供应链金融面临的主要风险之一,因此,如何测度质押物价格波动风险是学界和业界关注的焦点。VaR作为Basel协议主推的风险度量工具,已被学界和业界广泛使用。然而,关于VaR测度的现有方法存在:收益分布误设、非线性关系刻画不准确和混频数据信息提取不充分等潜在挑战,因此,本文提出了一种测度供应链金融质押物VaR的新方法:MIDAS-SVQR。一方面,该方法基于分位数框架下利用核函数捕获非线性关系以直接输出分位数,而无需分布假设;同时,利用MIDAS处理混频数据,提升其利用混频数据信息的能力。此外,本文基于二次规划详细给出了MIDAS-SVQR的求解过程。最后,本文选取钢铁、铜等六种典型质押物为研究对象,选择GARCH类和QR类等模型作为基准模型,并基于Kupiec检验等三种回测方法来评价模型准确性。结果表明:MIDAS-SVQR在所有样本的三种回测检验下表现最优。此外,分位数回归类模型总体表现明显优于GARCH类模型。因此,本文提出的MIDAS-SVQR新方法既有效度量了供应链金融质押物的风险价值,也为供应链金融风险管理提供了新技术支持。

中图分类号:

汪刘凯,张小波,王未卿, 等. 基于MIDAS-SVQR的供应链金融质押物风险价值测度新方法[J]. 中国管理科学, 2025, 33(3): 80-92.

Liukai Wang,Xiaobo Zhang,Weiqing Wang, et al. MIDAS-SVQR: A Novel Model for Measuring VaR of Supply Chain Finance Pledge[J]. Chinese Journal of Management Science, 2025, 33(3): 80-92.

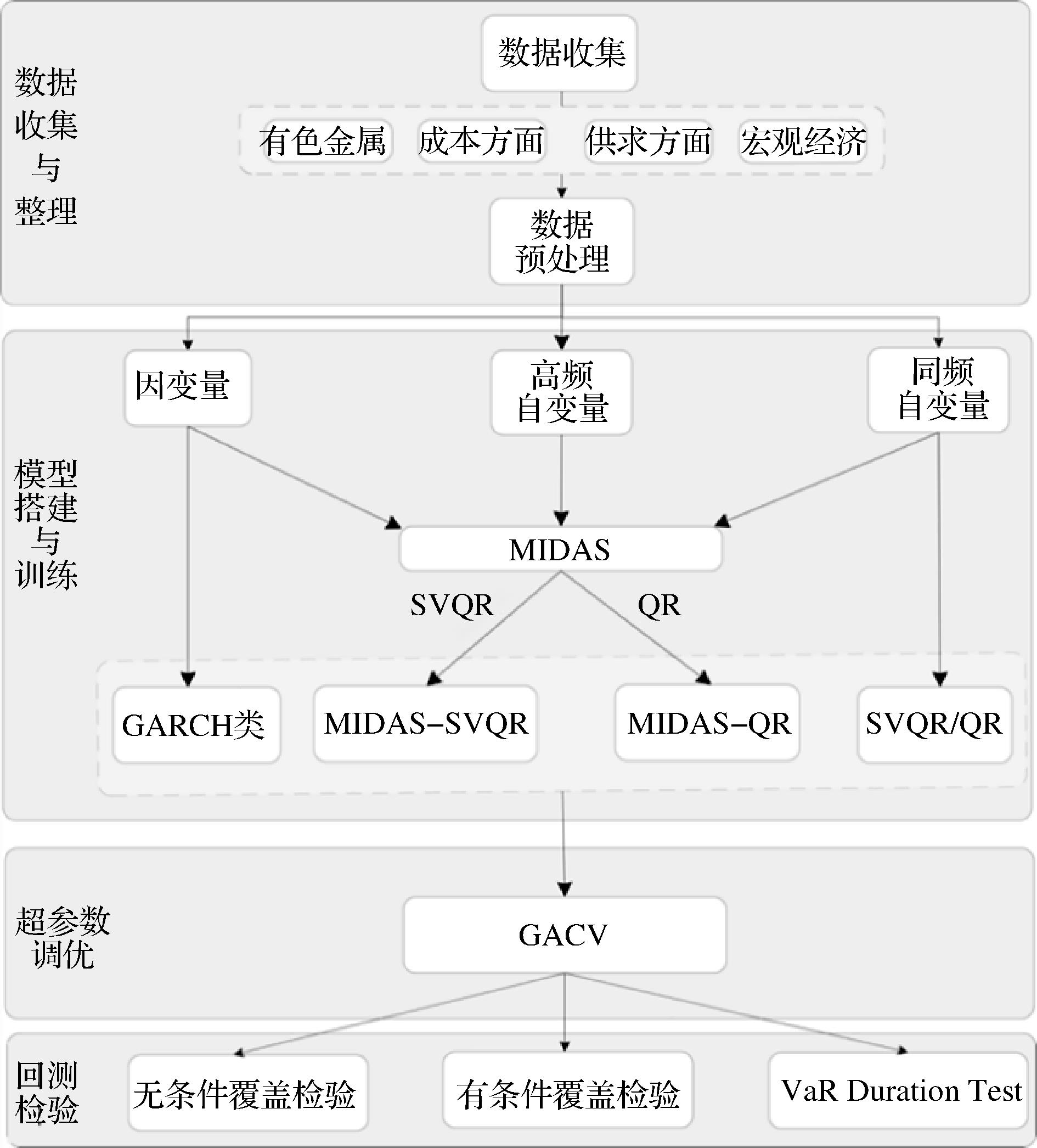

图 1

实证方案设计"

表 1

六种质押物样本的描述性统计分析"

| 指标 | 铜 | 铝 | 铅 | 锌 | 锡 | 钢铁 |

|---|---|---|---|---|---|---|

| 样本区间 | 2007-01 | 2007-01 | 2007-11 | 2007-11 | 2007-11 | 2007-01 |

| 2021-08 | 2021-08 | 2021-08 | 2021-08 | 2021-08 | 2021-08 | |

| 样本量 | 173 | 173 | 163 | 163 | 163 | 173 |

| 最大值 | 17.961 | 14.856 | 26.307 | 14.537 | 14.373 | 14.132 |

| 最小值 | -43.570 | -13.312 | -42.764 | -40.733 | -38.378 | -2.041 |

| 均值 | -0.112 | -0.012 | -0.386 | -0.342 | 0.234 | 0.325 |

| 中位数 | -0.274 | -0.052 | -0.469 | 0.267 | 0.000 | 0.274 |

| 偏度 | -1.824 | -0.182 | -1.229 | -1.830 | -2.071 | -0.512 |

| 峰度 | 11.398 | 1.424 | 10.143 | 10.437 | 16.077 | 6.259 |

| S–W检验 | 0.860* | 0.957* | 0.836* | 0.879* | 0.846* | 0.590* |

表 2

六种质押物的解释变量说明"

| 类别 | 指标 | 变量名称 | 频率 | 说明 |

|---|---|---|---|---|

| 成本 | 能源成本 | 中国大宗商品价格指数能源类 | 月 | 无 |

| 运输成本 | 长江干散货综合运价指数 | 月 | 无 | |

| 供需关系 | 供给 | 精炼铜产量 | 月 | 单位:千吨 |

| 精铝产量 | 月 | 单位:千吨 | ||

| 精炼铅产量 | 月 | 单位:千吨 | ||

| 锌锭产量 | 月 | 单位:千吨 | ||

| 精炼锡产量 | 月 | 单位:千吨 | ||

| 粗钢产量 | 月 | 单位:万吨 | ||

| 需求 | 精炼铜消费量 | 月 | 单位:千吨 | |

| 精铝消费量 | 月 | 单位:千吨 | ||

| 精炼铅消费量 | 月 | 单位:千吨 | ||

| 锌锭消费量 | 月 | 单位:千吨 | ||

| 精炼锡消费量 | 月 | 单位:千吨 | ||

| 粗钢消费量 | 月 | 单位:万吨 | ||

| 宏观经济环境 | 无 | 中国制造业采购经理人指数 | 月 | 无 |

| 汇率 | 日 | 人民比对美元 | ||

| LME铜现货结算价 | 日 | 单位:美元/吨 | ||

| LME铝现货结算价 | 日 | 单位:美元/吨 | ||

| LME铅现货结算价 | 日 | 单位:美元/吨 | ||

| LME锌现货结算价 | 日 | 单位:美元/吨 | ||

| LME锡现货结算价 | 日 | 单位:美元/吨 | ||

| LME基本金属指数 | 日 | 无 |

表 3

MIDAS-SVQR模型最优超参数集"

| 超参数设置 | ||||||

|---|---|---|---|---|---|---|

| 铜 | 1 | 0.16 | 1 | 0.25 | 6.0 | 0.25 |

| 铝 | 1 | 0.46 | 1 | 0.33 | 5.0 | 0.55 |

| 铅 | 1 | 0.31 | 1 | 0.82 | 7.0 | 0.60 |

| 锌 | 1 | 0.36 | 1 | 0.66 | 11.0 | 0.50 |

| 锡 | 1 | 0.37 | 1 | 0.53 | 6.5 | 1.00 |

| 钢铁 | 1 | 0.19 | 1 | 0.64 | 13.0 | 0.90 |

表 4

质押物铜回测检验结果"

| 模型 | VaR回测检验结果 | ||||

|---|---|---|---|---|---|

| GARCH-N | 0.040 | 0.672 | 0.666 | 0.445 | 0.595 |

| GARCH-t | 0.046 | 0.818 | 0.659 | 0.168 | 0.549 |

| GARCH-St | 0.052 | 0.903 | 0.604 | 0.413 | 0.640 |

| GARCH-GED | 0.046 | 0.818 | 0.659 | 0.188 | 0.555 |

| GARCH-SGED | 0.046 | 0.818 | 0.659 | 0.188 | 0.555 |

| QR | 0.052 | 0.903 | 0.604 | 0.114 | 0.540 |

| SVQR | 0.052 | 0.903 | 0.767 | 0.922 | 0.864 |

| MIDAS-QR | 0.052 | 0.903 | 0.604 | 0.498 | 0.668 |

| MIDAS-SVQR | 0.052 | 0.903 | 0.768 | 0.954 | 0.884 |

表 5

质押物铅回测检验结果"

| 模型 | VaR回测检验结果 | ||||

|---|---|---|---|---|---|

| GARCH-N | 0.043 | 0.672 | 0.453 | 0.414 | 0.513 |

| GARCH-t | 0.037 | 0.418 | 0.572 | 0.099 | 0.363 |

| GARCH-St | 0.037 | 0.418 | 0.572 | 0.099 | 0.363 |

| GARCH-GED | 0.043 | 0.672 | 0.453 | 0.467 | 0.530 |

| GARCH-SGED | 0.037 | 0.418 | 0.572 | 0.099 | 0.363 |

| QR | 0.049 | 0.957 | 0.133 | 0.167 | 0.419 |

| SVQR | 0.049 | 0.957 | 0.623 | 0.922 | 0.834 |

| MIDAS-QR | 0.049 | 0.957 | 0.659 | 0.768 | 0.795 |

| MIDAS-SVQR | 0.049 | 0.957 | 0.687 | 0.989 | 0.877 |

表 6

质押物铝回测检验结果"

| 模型 | VaR回测检验结果 | ||||

|---|---|---|---|---|---|

| GARCH-N | 0.046 | 0.818 | 0.643 | 0.921 | 0.794 |

| GARCH-t | 0.046 | 0.818 | 0.643 | 0.921 | 0.794 |

| GARCH-St | 0.046 | 0.818 | 0.711 | 0.960 | 0.830 |

| GARCH-GED | 0.046 | 0.818 | 0.582 | 0.632 | 0.677 |

| GARCH-SGED | 0.052 | 0.645 | 0.607 | 0.476 | 0.576 |

| QR | 0.046 | 0.818 | 0.659 | 0.040 | 0.506 |

| SVQR | 0.052 | 0.903 | 0.767 | 0.837 | 0.836 |

| MIDAS-QR | 0.052 | 0.903 | 0.604 | 0.120 | 0.542 |

| MIDAS-SVQR | 0.052 | 0.903 | 0.767 | 0.986 | 0.885 |

表 7

质押物锌回测检验结果"

| 模型 | VaR回测检验结果 | ||||

|---|---|---|---|---|---|

| GARCH-N | 0.043 | 0.672 | 0.698 | 0.341 | 0.570 |

| GARCH-t | 0.055 | 0.764 | 0.598 | 0.796 | 0.719 |

| GARCH-St | 0.037 | 0.418 | 0.595 | 0.938 | 0.651 |

| GARCH-GED | 0.055 | 0.764 | 0.598 | 0.168 | 0.510 |

| GARCH-SGED | 0.037 | 0.418 | 0.595 | 0.938 | 0.651 |

| QR | 0.055 | 0.764 | 0.563 | 0.332 | 0.553 |

| SVQR | 0.049 | 0.957 | 0.623 | 0.907 | 0.829 |

| MIDAS-QR | 0.049 | 0.957 | 0.695 | 0.425 | 0.692 |

| MIDAS-SVQR | 0.049 | 0.957 | 0.695 | 0.993 | 0.882 |

表 8

质押物锡回测检验结果"

| 模型 | VaR回测检验结果 | ||||

|---|---|---|---|---|---|

| GARCH-N | 0.043 | 0.672 | 0.666 | 0.445 | 0.595 |

| GARCH-t | 0.043 | 0.672 | 0.666 | 0.445 | 0.595 |

| GARCH-St | 0.055 | 0.764 | 0.563 | 0.493 | 0.606 |

| GARCH-GED | 0.049 | 0.957 | 0.659 | 0.841 | 0.819 |

| GARCH-SGED | 0.049 | 0.957 | 0.659 | 0.841 | 0.819 |

| QR | 0.055 | 0.764 | 0.563 | 0.607 | 0.644 |

| SVQR | 0.049 | 0.957 | 0.659 | 0.902 | 0.839 |

| MIDAS-QR | 0.049 | 0.957 | 0.687 | 0.870 | 0.838 |

| MIDAS-SVQR | 0.049 | 0.957 | 0.687 | 0.963 | 0.869 |

表 9

质押物钢铁回测检验结果"

| 模型 | VaR回测检验结果 | ||||

|---|---|---|---|---|---|

| GARCH-N | 0.064 | 0.431 | 0.688 | 0.363 | 0.494 |

| GARCH-t | 0.064 | 0.431 | 0.278 | 0.795 | 0.501 |

| GARCH-St | 0.069 | 0.268 | 0.267 | 0.736 | 0.424 |

| GARCH-GED | 0.058 | 0.645 | 0.780 | 0.513 | 0.646 |

| GARCH-SGED | 0.058 | 0.645 | 0.780 | 0.371 | 0.599 |

| QR | 0.046 | 0.818 | 0.659 | 0.074 | 0.517 |

| SVQR | 0.052 | 0.903 | 0.767 | 0.919 | 0.863 |

| MIDAS-QR | 0.046 | 0.818 | 0.643 | 0.946 | 0.802 |

| MIDAS-SVQR | 0.052 | 0.903 | 0.767 | 0.952 | 0.874 |

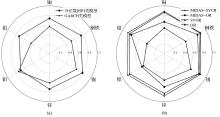

图 2

各模型结果对比图"

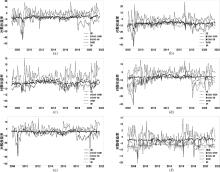

图 3

分位数回归类模型在各样本上的测度结果"

| 1 | 顾天下, 刘勤明. 面向高维和不平衡数据的供应链金融信用评价研究[J]. 计算机应用研究, 2022, 39(11): 3396-3401. |

| Gu T X, Liu Qi M. Credit evaluation of supply chain finance for high dimensional and unbalanced data [J]. Application Research of Computers, 2022, 39(11): 3396-3401. | |

| 2 | 鲁其辉, 曾利飞, 周伟华. 供应链应收账款融资的决策分析与价值研究[J]. 管理科学学报, 2012, 15(5): 10-18. |

| Lu Q H, Zeng L F, Zhou W H. Research on decision-making and value of supply chain financing with a counts receivables [J]. Journal of Management Science in China, 2012, 15(5): 10-18. | |

| 3 | 冯耕中. 物流金融业务创新分析[J]. 预测, 2007,26(1): 49-54. |

| Feng G Z. Analysis of logistics financing business innovation in China [J]. Forecasting, 2007, 26(1): 49-54. | |

| 4 | Markowitz H. Portfolol selection[J]. The Journal of Finance, 1952, 7(1): 77-91. |

| 5 | Jondeau E, Rockinger M. Conditional volatility, skewness, and kurtosis: Existence, persistence, and comovements[J]. Journal of Economic Dynamics and Control, 2003, 27(10): 1699-1737. |

| 6 | Wu D D, Olson D. Enterprise risk management: A DEA VaR approach in vendor selection[J]. International Journal of Production Research, 2010, 48(16): 4919-4932. |

| 7 | 江涛. 基于GARCH与半参数法VaR模型的证券市场风险的度量和分析:来自中国上海股票市场的经验证据[J]. 金融研究, 2010(6): 103-111. |

| Jiang T. Measurement and analysis of securities market risk based on GARCH and semi-parametric VaR model: Empirical evidence from China's shanghai stock market [J]. Journal of Financial Research, 2010(6): 103-111. | |

| 8 | 何娟, 王建, 蒋祥林. 存货质押业务质物组合价格风险决策[J]. 管理评论, 2013, 25(11): 163-176. |

| He J, Wang J, Jiang X L. The risk decision of inventory portfolio in supply chain finance[J].Management Review, 2013, 25(11): 163-176. | |

| 9 | 胡海青, 陈迪, 张丹, 等. 基于Copula的供应链金融质物组合价格风险测度研究[J]. 运筹与管理, 2020, 29(3): 77-90. |

| Hu H Q, Chen D, Zhang D, et al. Study of price risk measurement of pledged portfolio in supply chain based on Copula [J]. Operations Research and Management Science, 2020, 29(3): 77-90. | |

| 10 | 吕永健, 符廷銮, 胡颖毅, 等. 基于拔靴滤波历史模拟法的黄金市场 VaR 测度研究[J]. 中国管理科学, 2019, 27(7): 46-55. |

| Lv Y J, Fu T L, Hu Y Y, et al. A study of Chinese gold market based on bootstrapped filtered historical simulation approaches [J]. Chinese Journal of Management Science, 2019, 27(7): 46-55. | |

| 11 | Koenker R, Bassett G. Regression quantiles[J]. Econometrica, 1978, 46(1): 33-50. |

| 12 | Taylor J W. A quantile regression approach to estimating the distribution of multiperiod returns[J]. The Journal of Derivatives, 1999, 7(1): 64-78. |

| 13 | 刘向丽, 张翼鹏. 钢铁行业供给侧改革对股市影响研究——基于系统风险管理视角[J]. 管理评论, 2020, 32(7): 258-266. |

| Liu X L, Zhang Y P. Research on the impact of supply-side reform of iron and steel industry on stock market: From the perspective of systemic risk management[J].Management Review,2020,32(7):258-266. | |

| 14 | 杨子晖, 陈雨恬, 张平淼. 股票与外汇市场尾部风险的跨市场传染研究[J]. 管理科学学报, 2020,23(8): 54-77. |

| Yang Z H, Chen Y T, Zhang P M. Cross-market contagion effect on tail risk between stock markets and exchange markets [J]. Journal of Management Science in China, 2020, 23(8): 54-77. | |

| 15 | Calmon W, Ferioli E, Lettieri D, et al. An extensive comparison of some well-established value at risk methods[J]. International Statistical Review, 2021, 89(1): 148-166. |

| 16 | Li Y J, Liu Y F, Zhu J. Quantile regression in reproducing kernel hilbert spaces[J]. Journal of the American Statistical Association, 2007, 102(477): 255-268. |

| 17 | Cannon A J. Quantile regression neural networks: Implementation in R and application to precipitation downscaling[J]. Computers & Geosciences, 2011, 37(9): 1277-1284. |

| 18 | 许启发, 李辉艳, 蒋翠侠, 等. 基于QRNN+GARCH方法的供应链金融多期价格风险测度及防范[J]. 数理统计与管理, 2018, 37(4): 728-740. |

| Xu Q F, Li H Y, Jiang C X, et al. Evaluating and preventing multi-period price risk in supply chain finance via QRNN+GARCH method [J]. Journal of Applied Statistics and Management, 2018, 37(4): 728-740. | |

| 19 | 许启发, 张金秀, 蒋翠侠. 基于非线性分位数回归模型的多期VaR风险测度[J]. 中国管理科学, 2015, 23(3): 56-65. |

| Xu Q F, Zhang J X, Jiang C X. Evaluating multiperiod VaR via nonlinear quantile regression model[J]. Chinese Journal of Management Science, 2015, 23(3):56-65. | |

| 20 | Lima L R, Meng F N, Godeiro L. Quantile forecasting with mixed-frequency data[J]. International Journal of Forecasting, 2020, 36(3): 1149-1162. |

| 21 | Xu Q F, Wang L K, Jiang C X, et al. A novel UMIDAS-SVQR model with mixed frequency investor sentiment for predicting stock market volatility[J]. Expert Systems with Applications, 2019, 132: 12-27. |

| 22 | 许启发, 刘书婷, 蒋翠侠. 基于 MIDAS 分位数回归的条件偏度组合投资决策[J]. 中国管理科学, 2021, 29(3): 24-36. |

| Xu Q F, Liu S T, Jiang C X. Portfolio selection with conditional skewness estimated via MIDAS quantile regression[J]. Chinese Journal of Management Science, 2021, 29(3): 24-36. | |

| 23 | 陈强, 龚玉婷, 袁超文. 基于MIDAS模型的中国股市对居民消费的影响效应[J]. 系统管理学报, 2018, 27(6): 1028-1035. |

| Chen Q, Gong Y T, Yuan C W. An examination of stock market impacts on residential consumption in China:An empirical analysis based on the MIDAS model[J]. Journal of System & Management, 2018, 27(6):1028-1035. | |

| 24 | Ghysels E, Sinko A, Valkanov R. MIDAS regressions: Further results and new directions[J]. Econometric Reviews, 2007, 26(1): 53-90. |

| 25 | Kupiec P. Techniques for verifying the accuracy of risk measurement models[J]. The Journal of Derivatives, 1995, 3(2): 73-84. |

| 26 | Christoffersen P F. Evaluating interval forecasts[J]. International Economic Review, 1998, 39(4): 841-862. |

| 27 | Christoffersen P, Pelletier D. Backtesting value-at-risk: A duration-based approach[J]. Journal of Financial Econometrics, 2004, 2(1): 84-108. |

| 28 | Pan Y C, Xiao Z, Wang X N, et al. A multiple support vector machine approach to stock index forecasting with mixed frequency sampling[J]. Knowledge-Based Systems, 2017, 122: 90-102. |

| 29 | Xu Q F, Wang L K, Jiang C X, et al. A novel(U)MIDAS-SVR model with multi-source market sentiment for forecasting stock returns[J]. Neural Computing and Applications, 2020, 32(10): 5875-5888. |

| 30 | Pettenuzzo D, Timmermann A, Valkanov R.A MIDAS approach to modeling first and second moment dynamics[J]. Journal of Econometrics, 2016, 193(2): 315-334. |

| 31 | 刘汉, 刘金全. 中国宏观经济总量的实时预报与短期预测——基于混频数据预测模型的实证研究[J]. 经济研究, 2011, 46(3): 4-17. |

| Liu H, Liu J Q. Nowcasting and short-term forecasting of Chinese macroeconomic aggregates: Based on the empirical study of MIDAS model[J]. Economic Research, 2011, 46(3):4-17. | |

| 32 | Ma X, Liu Z B. Predicting the oil production using the novel multivariate nonlinear model based on Arps decline model and kernel method[J]. Neural Computing and Applications, 2018, 29(2): 579-591. |

| 33 | Yuan M. GACV for quantile smoothing splines[J]. Computational Statistics & Data Analysis, 2006, 50(3): 813-829. |

| 34 | Tsai C Y. On delineating supply chain cash flow under collectionrisk[J]. International Journal of Production Economics, 2011, 129(1): 186-194. |

| 35 | 钟美瑞, 谌杰宇, 黄健柏, 等. 基于MSVAR模型的有色金属价格波动影响因素的非线性效应研究[J]. 中国管理科学, 2016, 24(4): 45-53. |

| Zhong M R, Chen J Y, Huang J B, et al. Nonlinear effects studies of influence of nonferrous metals price flutuation based on MSVAR model[J]. Chinese Journal of Management Science, 2016, 24(4):45-53. | |

| 36 | Khoshalan H A, Shakeri J, Najmoddini I, et al. Forecasting copper price by application of robust artificial intelligence techniques[J]. Resources Policy, 2021, 73: 102239. |

| 37 | 叶翀, 曹峰, 张玲. 我国沿海与内河干散货运价指数联动性研究[J]. 价格理论与实践, 2019(3): 73-76. |

| Ye C, Cao F, Zhang L. Research on the linkage of China’s coastal and inland river dry bulk freight index[J]. Price Theory and Practice, 2019(3):73-76. | |

| 38 | Humphreys D. The great metals boom: A retrospective[J]. Resources Policy, 2010, 35(1): 1-13. |

| 39 | 刘超, 郑莹, 刘宸琦, 等. 股市是经济的晴雨表吗?——基于2005-2017年沪深300指数和采购经理人指数数据[J]. 系统工程理论与实践, 2020, 40(1): 55-68. |

| Liu C, Zheng Y, Liu C Q, et al. Is the stock market a barometer of the economy? Based on the 2005-2017 year's CSI 300 index and PMI data[J]. Systems Engineering-Theory & Practice,2020,40(1):55-68. | |

| 40 | 冯辉, 张蜀林. 国际黄金期货价格决定要素的实证分析[J]. 中国管理科学, 2012, 20(S1): 424-428. |

| Feng H, Zhang S L. The empirical analysis about the determining of international gold futures prices[J]. Chinese Journal of Management Science, 2012, 20(S1): 424-428. | |

| 41 | 李洁, 杨莉. 上海和伦敦金属期货市场价格联动性研究——以铜铝锌期货市场为例[J]. 价格理论与实践, 2017(8): 100-103. |

| Li J, Yang L. A study on the price linkage between the Shanghai and London metal futures markets: A case study of copper, aluminum, and zinc futures markets[J]. Price Theory and Practice, 2017(8): 100-103. | |

| 42 | 朱学红, 谌金宇, 邵留国. 信息溢出视角下的中国金属期货市场国际定价能力研究[J]. 中国管理科学, 2016, 24(9): 28-35. |

| Zhu X H, Chen J Y, Shao L G. The international pricing POWER of Chinese metal futures market based on information spillover[J]. Chinese Journal of Management Science, 2016, 24(9): 28-35. |

| [1] | 余方平, 张蕾, 孟斌. 匹配波动特征的班轮航线运价组合风险测度[J]. 中国管理科学, 2026, 34(6): 157-170. |

| [2] | 王泽舟, 许启发, 蒋翠侠. 上市公司多层关系网络中混频信息交互与传播能够提升资产定价性能吗?——基于图神经网络的资产定价研究[J]. 中国管理科学, 2026, 34(4): 47-62. |

| [3] | 杨晓叶, 胡雪芹, 宋华. 供应链金融动态折扣模式演进过程与最优决策[J]. 中国管理科学, 2026, 34(3): 159-169. |

| [4] | 林强, 单镇杰, 李文卓. CVaR条件下考虑授信额度的报童模型[J]. 中国管理科学, 2025, 33(9): 312-324. |

| [5] | 姚银红, 王晓旭, 陈炜, 陈振松. 基于Transformer-LSTM分位数回归的全球股市极端风险溢出研究[J]. 中国管理科学, 2025, 33(8): 1-13. |

| [6] | 王雄, 李景瑶, 任晓航, 王宗润. 国际新兴资产与中国传统资产的多维溢出效应[J]. 中国管理科学, 2025, 33(8): 37-49. |

| [7] | 田军, 董赞强, 李雅丽. 基于预付账款融资模式的供应链融资策略研究[J]. 中国管理科学, 2025, 33(7): 272-283. |

| [8] | 周昆树, 张波, 焦建玲. 预期视角下中央银行沟通的有效性与通货膨胀预期管理研究[J]. 中国管理科学, 2025, 33(7): 33-43. |

| [9] | 于辉, 王霜. 供应链金融:企业如何实现“鱼与熊掌”兼得?[J]. 中国管理科学, 2025, 33(5): 280-289. |

| [10] | 宋诗佳, 田飞, 李汉东. 基于时变极值方法的VaR预测模型以及应用[J]. 中国管理科学, 2025, 33(2): 61-70. |

| [11] | 韩松, 李璨. 多代理Nash Q-Learning模型行动选择策略研究[J]. 中国管理科学, 2025, 33(12): 110-120. |

| [12] | 谢楠,何海涛,周艳菊,王宗润. 乡村振兴背景下基于中央政府项目补贴分析的供应链金融决策研究[J]. 中国管理科学, 2024, 32(8): 214-229. |

| [13] | 蔡毅,唐振鹏,吴俊传,杜晓旭,陈凯杰. 基于灰狼优化的混频支持向量机在股指预测与投资决策中的应用研究[J]. 中国管理科学, 2024, 32(5): 73-80. |

| [14] | 孙睿,何大义,苏汇淋. 基于演化博弈的区块链技术在供应链金融中的应用研究[J]. 中国管理科学, 2024, 32(3): 125-134. |

| [15] | 陈杰,邢灵博,李胃胜,陈志祥,陈崇萍. 不完备质量下带有风险厌恶的库存决策模型[J]. 中国管理科学, 2024, 32(2): 54-64. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||