主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2025, Vol. 33 ›› Issue (12): 41-56.doi: 10.16381/j.cnki.issn1003-207x.2024.2305cstr: 32146.14.j.cnki.issn1003-207x.2024.2305

黄兆荣1, 宋正阳1, 杨博1,2, 曾能民3,4, 余乐安1,2( )

)

收稿日期:2024-12-19

修回日期:2025-05-17

出版日期:2025-12-25

发布日期:2025-12-25

通讯作者:

余乐安

E-mail:yulean@amss.ac.cn

基金资助:

Zhaorong Huang1, Zhengyang Song1, Bo Yang1,2, Nengmin Zeng3,4, Le’an Yu1,2()

Received:2024-12-19

Revised:2025-05-17

Online:2025-12-25

Published:2025-12-25

Contact:

Le’an Yu

E-mail:yulean@amss.ac.cn

摘要:

黄金资产的价格形成机制错综复杂,难以通过单变量时间序列分析框架全面揭示其内在特征空间中所蕴含的丰富多维信息。为此,本文基于分解-重构-集成思想,提出一种稳健分解和分层集成策略的混合回归模型用于黄金价格预测,有效地挖掘多种金融影响因素在不同时间尺度间的协同作用。首先,开发了一种稳定变分模式分解(stable variational mode decomposition, SVMD)技术,以提取黄金价格序列的稳定中心频率分量边界,用于连续的特征学习。接着,运用Hurst指数作为记忆性重构指标,将分解分量重构成短期、中期和长期尺度分量。其次,利用缩放主成分分析回归和最小最大凹度惩罚回归的特征选择优势构建混合线性回归(hybrid linear regression, HLR)模型,在不同时间尺度上提取重要金融特征用于预测,从而提高整体预测泛化能力。最后,分层集成方法将原始层、重构层和分量层的预测结果进行综合,得到调和的黄金价格预测值。该模型采用两个国际黄金价格数据进行实证分析,研究结果验证了所提出的模型在分解、重构和集成三个步骤的有效性,并且,对比已有研究的多种预测模型和分解建模策略验证了所提出模型的优势。

中图分类号:

黄兆荣,宋正阳,杨博, 等. 黄金价格的混合多元回归预测研究:基于分解-重构-集成方法论[J]. 中国管理科学, 2025, 33(12): 41-56.

Zhaorong Huang,Zhengyang Song,Bo Yang, et al. Hybrid Multivariate Regression Forecasting for Gold Prices: A Decomposition-Reconstruction-Ensemble Methodology[J]. Chinese Journal of Management Science, 2025, 33(12): 41-56.

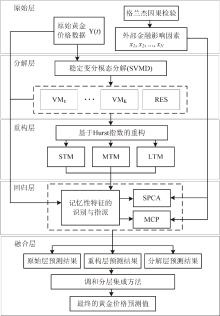

图1

SVMD算法逐步分解示意图"

图2

SVMD分解-记忆性重构-分层集成预测框架"

表1

筛选得到的影响因素与被选中的因素"

| 影响因素 | 芝加哥黄金数据集 | 伦敦黄金数据集 | ||

|---|---|---|---|---|

| 是否通过格兰杰因果检验 | 有无被MCP 回归选中 | 是否通过格兰杰因果检验 | 有无被MCP 回归选中 | |

| 恒生股指 | 是 | RES,STM | 是 | 无 |

| 印度股指 | 是 | 无 | 否 | 无 |

| 泰国股指 | 是 | VM7 | 是 | STM |

| 韩国股指 | 是 | RES,STM | 否 | VM7,VM8,RES,STM |

| 俄罗斯股指 | 否 | 无 | 是 | RES,STM |

| 巴西股指 | 是 | VM7,RES,STM | 是 | VM6,VM7,VM8,RES,STM |

| 墨西哥股指 | 是 | RES | 是 | 无 |

| 意大利股指 | 是 | RES | 否 | 无 |

| 西班牙股指 | 是 | 无 | 否 | 无 |

| 土耳其股指 | 是 | VM7,RES,STM | 是 | VM7,VM8,RES,STM |

| 立陶宛股指 | 是 | 无 | 否 | VM7,VM8,STM |

| 捷克股指 | 是 | VM7,RES,STM | 否 | 无 |

| 加拿大股指 | 是 | RES | 是 | 无 |

| 哥伦比亚股指 | 是 | 无 | 是 | 无 |

| 菲律宾股指 | 是 | 无 | 否 | 无 |

| 法国股指 | 是 | RES | 否 | 无 |

| 比利时股指 | 是 | RES,STM | 是 | VM7,VM8,RES,STM |

| 澳大利亚股指 | 是 | VM7,RES,STM | 否 | 无 |

| 爱沙尼亚股指 | 是 | 无 | 是 | RES |

| 冰岛股指 | 是 | RES | 是 | 无 |

| 沙特阿拉伯股指 | 否 | 无 | 是 | RES,STM |

| 瑞士股指 | 否 | 无 | 是 | VM7,VM8,RES,STM |

| 立陶宛股指 | 否 | 无 | 是 | VM7,VM8,STM |

| 原油期货价格 | 是 | 无 | 是 | 无 |

| 铜期货价格 | 是 | RES,STM | 是 | STM |

| 白银期货价格 | 是 | VM8,RES,STM | 是 | VM7,VM8,RES,STM |

| 标准普尔高盛商品指数 | 是 | 无 | 是 | VM7,VM8,RES,STM |

| 路透商品研究局指数 | 是 | RES | 是 | VM7,VM8,RES,STM |

| 美元(英镑)对港币汇率 | 是 | 无 | 否 | 无 |

| 美元(英镑)对人民币汇率 | 是 | VM7,RES,STM | 是 | RES,STM |

| 美元(英镑)对印度卢比汇率 | 是 | 无 | 是 | 无 |

| 美元(英镑)对日元汇率 | 是 | RES,STM | 否 | 无 |

| 美元(英镑)对加拿大元汇率 | 是 | 无 | 否 | 无 |

| 美元(英镑)对澳大利亚元汇率 | 是 | 无 | 是 | VM7,RES,STM |

| 美元(英镑)对瑞典克朗汇率 | 是 | 无 | 是 | VM7,VM8,RES,STM |

| 美元(英镑)对新西兰元汇率 | 是 | 无 | 是 | 无 |

| 美元(英镑)对欧元汇率 | 是 | 无 | 否 | 无 |

| 美元(英镑)对丹麦克朗汇率 | 是 | 无 | 是 | RES |

| 美元(英镑)对挪威克朗汇率 | 是 | 无 | 是 | VM7,VM8,RES,STM |

| 美元(英镑)对瑞士法郎汇率 | 是 | RES,STM | 是 | 无 |

| 美元(英镑)对英镑(美元)汇率 | 否 | 无 | 是 | VM7,VM8,STM |

| 香港10年期政府债收益率 | 是 | VM7,RES,STM | 是 | VM7,VM8,RES,STM |

| 中国10年期国债收益率 | 否 | 无 | 是 | STM |

| 俄罗斯10年期国债收益率 | 否 | 无 | 是 | VM7,VM8,RES,STM |

| 加拿大10年期国债收益率 | 是 | RES,STM | 是 | RES,STM |

| 法国10年期国债收益率 | 是 | 无 | 是 | 无 |

| 德国10年期国债收益率 | 是 | VM7,RES,STM | 是 | VM7,VM8,RES,STM |

| 英国10年期国债收益率 | 是 | RES,STM | 是 | VM7,VM8,RES,STM |

| 美国10年期国债收益率 | 是 | VM7,RES,STM | 是 | VM6,VM7,VM8,RES,STM |

| 韩国10年期国债收益率 | 是 | RES,STM | 是 | 无 |

| 英文地区推特文本经济不确定性指数 | 是 | VM7,RES,STM | 是 | VM7,VM8,STM |

| 美国地区推特文本经济不确定性指数 | 是 | 无 | 是 | RES,STM |

| 恐慌指数 | 是 | RES,STM | 否 | 无 |

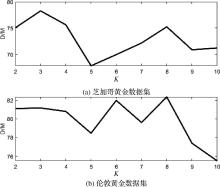

图3

不同K值分解预测性能"

图4

SVMD分解和记忆性重构结果"

表2

分解层Hurst指数和分类结果"

| Hurst指数 | VM1 | VM2 | VM3 | VM4 | VM5 | VM6 | VM7 | VM8 | RES |

|---|---|---|---|---|---|---|---|---|---|

| 芝加哥黄金 | 0.9937 | 0.9940 | 0.9651 | 0.8438 | 0.4142 | 0.1364 | -0.0767 | -0.0953 | -0.0078 |

| 分类结果 | 长期尺度模态(LTM) | 中期尺度模态(MTM) | 短期尺度模态(STM) | ||||||

| 伦敦黄金 | 0.9922 | 0.9952 | 0.9758 | 0.8436 | 0.5993 | 0.2051 | -0.0653 | -0.0840 | -0.0121 |

| 分类结果 | 长期尺度模态(LTM) | 中期尺度模态(MTM) | 短期尺度模态(STM) | ||||||

表3

原始层和重构层Hurst指数和子模型指派结果"

| Hurst指数 | 原始序列 | LTM | MTM | STM |

|---|---|---|---|---|

| 芝加哥黄金 | 0.4781 | 0.9735 | 0.5651 | -0.0328 |

| 预测子模型 | SPCA回归 | SPCA回归 | SPCA回归 | MCP回归 |

| 伦敦黄金 | 0.4745 | 0.9794 | 0.6420 | -0.0391 |

| 预测子模型 | SPCA回归 | SPCA回归 | SPCA回归 | MCP回归 |

表4

各模型黄金价格预测性能评价"

| 数据集 | 芝加哥黄金 | 伦敦黄金 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 预测模型 | MSE | MAE | D stat (%) | D/M | MSE | MAE | D stat (%) | D/M | |

| UV-LR | 296.8443 | 12.8515 | 53.78 | 76.28 | 274.7381 | 12.3111 | 52.44 | 77.61 | |

| SVMD-UV-LR | 292.1239 | 12.8125 | 52.89 | 75.23 | 273.7696 | 12.2915 | 52.22 | 77.39 | |

| MV-MCP | 297.8840 | 12.8130 | 51.11 | 72.74 | 277.8917 | 12.3349 | 46.89 | 69.29 | |

| MV-SPCA | 271.4506 | 12.8347 | 58.41 | 82.85 | 259.1138 | 12.5937 | 58.67 | 84.66 | |

| SVMD-MCP | 287.3581 | 12.6657 | 56.00 | 80.55 | 259.1964 | 11.9655 | 56.89 | 86.54 | |

| SVMD-SPCA | 278.3768 | 12.7978 | 56.22 | 80.04 | 266.1858 | 12.1785 | 58.00 | 86.71 | |

| SVMD-HLR | 268.7421 | 12.3836 | 57.78 | 85.05 | 254.4346 | 11.9089 | 59.78 | 91.38 | |

| SVMD-MR-MCP | 296.8475 | 13.0529 | 50.89 | 71.07 | 269.2959 | 12.2898 | 55.33 | 82.05 | |

| SVMD-MR-SPCA | 269.4559 | 12.5037 | 56.67 | 82.59 | 257.7426 | 11.9982 | 56.44 | 85.65 | |

| SVMD-MTD-HLR | 260.2057 | 12.1709 | 58.67 | 87.87 | 249.7207 | 11.8350 | 59.56 | 91.64 | |

| HLR-SVR | 334.6570 | 14.0353 | 59.56 | 77.08 | 291.7949 | 13.0435 | 58.89 | 82.11 | |

| LR-HE-minT | 295.2399 | 12.8258 | 53.11 | 67.44 | 274.6680 | 12.2752 | 54.89 | 81.44 | |

| SPCA-HE-minT | 11.6965 | ||||||||

| HLR-HE-minT | 242.1298 | 11.7271 | 62.44 | 97.07 | 236.9659 | 62.00 | 96.43 | ||

表5

DM检验结果"

| 预测模型 | 芝加哥黄金 | 伦敦黄金 |

|---|---|---|

| SVMD-UV-LR | -0.384 | 0.480 |

| MV-MCP | -0.504 | 0.249 |

| MV-SPCA | -0.003 | 0.859 |

| SVMD-MCP | -1.091 | -2.257* |

| SVMD-SPCA | -0.152 | -0.786 |

| SVMD-HLR | -2.263* | -2.837** |

| SVMD-MR-MCP | 1.274 | -0.154 |

| SVMD-MR-SPCA | -1.131 | -1.584 |

| SVMD-MTD-HLR | -3.181*** | -3.173** |

| HLR-SVR | 2.867** | 1.935 |

| LR-HE-minT | -0.521 | -0.913 |

| SPCA-HE-minT | -3.435*** | -3.023** |

| HLR-HE-minT | -4.392*** | -3.017** |

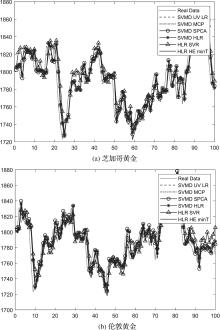

图5

黄金价格预测结果"

表6

各分解方案下黄金价格预测性能评价"

| 数据集 | 芝加哥黄金 | 伦敦黄金 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 预测模型 | MSE | MAE | D stat (%) | D/M | MSE | MAE | D stat (%) | D/M | |

| SVMD-C-LR | 327.8487 | 13.8126 | 52.22 | 68.79 | |||||

| SVMD-B-LR | 298.0214 | 12.9116 | 51.11 | 72.15 | 274.7381 | 12.3111 | 52.44 | 77.61 | |

| FixFreVMD-C-LR | 330.0396 | 13.8498 | 51.56 | 67.73 | 294.4208 | 13.1148 | 51.33 | 71.29 | |

| FixFreVMD-B-LR | 322.5728 | 13.5973 | 51.78 | 296.4623 | 13.1438 | 52.67 | 72.99 | ||

| FixloopVMD-C-LR | 423.1488 | 15.7798 | 54.89 | 63.22 | 325.7307 | 13.6047 | 52.00 | 69.58 | |

| FixloopVMD-B-LR | 429.6582 | 15.7663 | 52.00 | 59.98 | 404.1694 | 15.2342 | 52.67 | 63.02 | |

| OriginVMD-C-LR | 536.3667 | 17.8578 | 51.78 | 52.69 | 368.2220 | 14.5860 | 50.89 | 63.45 | |

| OriginVMD-B-LR | 461.9472 | 16.5685 | 52.44 | 57.54 | 459.9807 | 16.6394 | 53.33 | 58.37 | |

| ICEEMDAN-C-LR | 385.6285 | 15.0648 | 50.44 | 61.09 | 335.4319 | 14.0542 | 50.22 | 65.13 | |

| ICEEMDAN-B-LR | 399.0081 | 15.0950 | 55.11 | 66.45 | 366.6509 | 14.3582 | 53.11 | 67.32 | |

| EMD-C-LR | 515.4149 | 17.3192 | 55.49 | 2767.7068 | 40.8141 | 51.33 | 22.99 | ||

| EMD-B-LR | 539.5172 | 18.0621 | 45.78 | 46.24 | 571.5142 | 18.8239 | 48.44 | 46.95 | |

| DWT-C-LR | 395.1280 | 15.1754 | 50.00 | 60.02 | 343.6984 | 13.9168 | 53.33 | 69.78 | |

| DWT-B-LR | 377.0423 | 14.6884 | 65.54 | 363.1614 | 14.5267 | 52.44 | 65.75 | ||

| SSA-C-LR | 407.4101 | 16.0148 | 46.00 | 52.39 | 320.8109 | 14.1457 | 47.33 | 61.01 | |

| SSA-B-LR | 308.0430 | 13.6496 | 46.89 | 62.69 | 325.8507 | 13.8043 | 47.11 | 62.30 | |

图6

各分解技术的分解边界"

表7

SVMD框架下各预测器对于黄金价格预测性能评价"

| 数据集 | 芝加哥黄金 | 伦敦黄金 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| 预测模型 | MSE | MAE | D stat (%) | D/M | MSE | MAE | D stat (%) | D/M | |

| SVMD-RF-RFE | 420.9253 | 15.4028 | 57.11 | 67.81 | 518.0661 | 17.9090 | 49.11 | 49.89 | |

| SVMD-GBDT | 336.0971 | 13.8461 | 53.78 | 70.73 | 356.0066 | 14.3416 | 54.67 | 69.32 | |

| SVMD-XGBoost | 347.8793 | 14.1455 | 50.89 | 65.41 | 327.9640 | 13.7461 | 53.56 | 70.84 | |

| SVMD-LightGBM | 329.3842 | 13.8780 | 51.78 | 67.86 | 308.1727 | 13.3176 | 54.00 | 73.69 | |

| SVMD-SVM-RFE | 289.6998 | 12.8452 | 53.33 | 75.68 | 269.1036 | 12.1347 | 55.78 | 83.67 | |

| SVMD-GRNN | 293.9155 | 12.8797 | 52.67 | 74.44 | 284.5915 | 12.7583 | 51.33 | 73.24 | |

| SVMD-LSTM | 292.0098 | 12.8331 | 53.56 | 76.01 | 271.7906 | 12.3726 | 54.67 | 80.43 | |

| SVMD-GRU | 332.5922 | 13.9642 | 53.11 | 69.13 | 292.2901 | 12.8820 | 54.00 | 76.09 | |

| SVMD-PLS | 292.1650 | 12.8039 | 53.56 | 76.23 | 274.6803 | 12.3561 | 52.67 | 77.60 | |

| SVMD-Lasso | 290.4264 | 12.7861 | 53.78 | 76.64 | 56.89 | 85.51 | |||

| SVMD-MCP | 287.3581 | 56.00 | 80.55 | 258.9699 | 11.9655 | 87.55 | |||

| SVMD-PCA | 80.02 | 271.6163 | 12.4526 | 55.11 | 80.52 | ||||

| SVMD-SPCA | 278.3768 | 12.7978 | 56.22 | 266.1858 | 12.1785 | 58.00 | |||

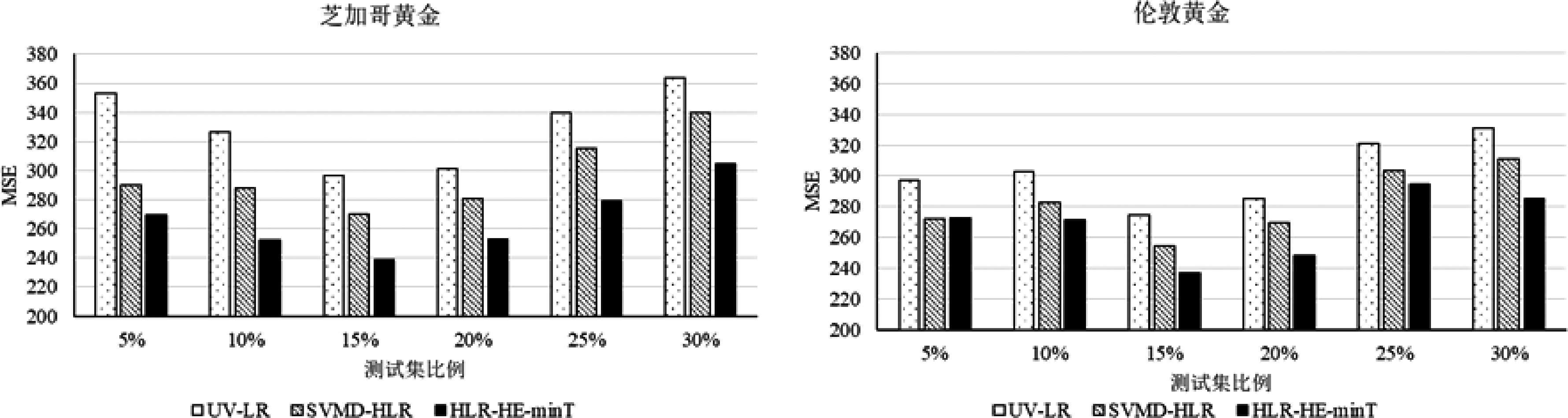

图7

不同测训比下回归模型稳健性"

图8

不同数据量估计下分层预测模型稳健性"

| [1] | 谭德凯, 田利辉. 黄金是股票市场的“避险天堂”吗?——基于动态条件相关混频数据抽样模型[J]. 中国管理科学, 2022, 30(10): 14-24. |

| Tan D K, Tian L H. Is gold a safe haven of the stock market? Based on dynamic conditional correlation mixed data sampling model[J]. Chinese Journal of Management Science, 2022, 30(10): 14-24. | |

| [2] | Koziuk V. Role of gold in foreign exchange reserves of commodity exporting countries[J]. Journal of European Economy, 2021, 20(2): 211-232. |

| [3] | Arslanalp S, Eichengreen B, Simpson-Bell C. Gold as international reserves: A barbarous relic no more?[J]. Journal of International Economics, 2023, 145: 103822. |

| [4] | Pattnaik D, Hassan M K, DSouza A, et al. Investment in gold: A bibliometric review and agenda for future research[J]. Research in International Business and Finance, 2023, 64: 101854. |

| [5] | 郭杨莉, 马锋. 基于马尔科夫和混频数据模型的黄金期货市场波动率预测研究[J]. 中国管理科学, 2024, 32(1): 13-22. |

| Guo Y L, Ma F. Forecasting the Chinese gold futures market volatility using Markov-switching regime and mixed data sampling model[J]. Chinese Journal of Management Science, 2024, 32(1): 13-22. | |

| [6] | 吕永健, 符廷銮, 胡颖毅, 等. 基于拔靴滤波历史模拟法的黄金市场VaR测度研究[J]. 中国管理科学, 2019, 27(7): 46-55. |

| Lv Y J, Fu T L, Hu Y Y, et al. A study of risk measurements of Chinese gold market based on bootstraped filtered historical simulation approaches[J]. Chinese Journal of Management Science, 2019, 27(7): 46-55. | |

| [7] | 范彩云, 童君逸, 程俊彦, 等. 基于ML-DMA的黄金期货价格预测研究[J]. 数理统计与管理, 2024, 43(3): 541-558. |

| Fan C Y, Tong J Y, Cheng J Y, et al. Gold futures price forecasting based on ML-DMA[J]. Journal of Applied Statistics and Management, 2024, 43(3): 541-558. | |

| [8] | 王海燕, 盛昭瀚. 大数据驱动的复杂系统管理情景建模: 技术与流程[J]. 中国管理科学, 2025, 33(1): 22-33. |

| Wang H Y, Sheng Z H. Modeling of complex system management scenarios driven by big data: Techniques and processes[J]. Chinese Journal of Management Science, 2025, 33(1): 22-33. | |

| [9] | 王方, 张颂扬, 余乐安, 等. 数据特征驱动的单变量预测建模研究[J]. 计量经济学报, 2024, 4(4): 1124-1148. |

| Wang F, Zhang S Y, Yu L A, et al. Data-trait-driven univariate predictive modeling[J]. China Journal of Econometrics, 2024, 4(4): 1124-1148. | |

| [10] | Yu L, Wang Z, Tang L. A decomposition–ensemble model with data-characteristic-driven reconstruction for crude oil price forecasting[J]. Applied Energy, 2015, 156: 251-267. |

| [11] | 柴建, 寇红红. 基于TEI@I方法论的系统管理预测技术研究综述及展望[J]. 管理评论, 2020, 32(7): 280-292. |

| Chai J, Kou H H. Review and prospect of system management prediction technology based on TEI@I methodology[J]. Management Review, 2020, 32(7): 280-292. | |

| [12] | 高晓辉, 周坤, 李廉水. 基于XGBOOST和ELM的混合空气质量预警系统: 以南京为例[J]. 中国管理科学, 2023, 31(5): 269-278. |

| Gao X H, Zhou K, Li L S. Hybrid air quality early warning system based on XGBoost and ELM: A case study of Nanjing[J]. Chinese Journal of Management Science, 2023, 31(5): 269-278. | |

| [13] | 曾能民, 张明, 余乐安. 基于“拆分-填充-分解-集成”的我国线上零售额预测研究[J]. 中国管理科学, 2022, 30(12): 63-76. |

| Zeng N M, Zhang M, Yu L A. Forecasting online retail sales of China based on splitting-filling-decomposition-ensemble model[J]. Chinese Journal of Management Science, 2022, 30(12): 63-76. | |

| [14] | 梁小珍, 赵欣, 杨明歌, 等. 基于二次分解和模型选择策略的港口集装箱吞吐量组合预测[J]. 管理评论, 2024, 36(8): 52-64. |

| Liang X Z, Zhao X, Yang M G, et al. A combination forecast method of port container throughput based on secondary decomposition and model selection strategy[J]. Management Review, 2024, 36(8): 52-64. | |

| [15] | 李霞, 李守伟. 基于EMD与DVG的非线性时间序列预测模型及其应用研究[J]. 中国管理科学, 2022, 30(9): 275-286. |

| Li X, Li S W. Non-linear time series prediction model based on EMD and DVG and its application[J]. Chinese Journal of Management Science, 2022, 30(9): 275-286. | |

| [16] | 杨晨, 陈贵词. 基于EMD-LSTM的国际黄金期货价格预测[J]. 中南民族大学学报(自然科学版), 2023, 42(6): 857-864. |

| Yang C, Chen G C. International gold futures price forecast based on EMD-LSTM[J]. Journal of South-Central Minzu University (Natural Science Edition), 2023, 42(6): 857-864. | |

| [17] | Yang M, Wang R, Zeng Z, et al. Improved prediction of global gold prices: An innovative Hurst-reconfiguration-based machine learning approach[J]. Resources Policy, 2024, 88: 104430. |

| [18] | 何林芸. 基于ICEEMDAN-SE-SSA-ELM算法的黄金期货价格预测[J]. 兰州文理学院学报(自然科学版), 2023, 37(1):35-39. |

| He L Y. Gold futures price forecast based on ICEEMDAN-SE-SSA-ELM algorithm[J]. Journal of Lanzhou University of Arts and Science (Natural Sciences), 2023, 37(1): 35-39. | |

| [19] | Lu W, Qiu T, Shi W, et al. International gold price forecast based on CEEMDAN and support vector regression with grey wolf algorithm[J]. Complexity, 2022, 2022(1): 1511479. |

| [20] | Liang Y, Lin Y, Lu Q. Forecasting gold price using a novel hybrid model with ICEEMDAN and LSTM-CNN-CBAM[J]. Expert Systems with Applications, 2022, 206: 117847. |

| [21] | 秦全德, 黄兆荣, 周至昊, 等. 基于包络熵的双层分解流感预测模型研究[J]. 系统工程理论与实践, 2023, 43(12): 3505-3519. |

| Qin Q D, Huang Z R, Zhou Z H, et al. A two-layer decomposition model based on envelope entropy for influenza forecasting[J]. Systems Engineering-Theory & Practice, 2023, 43(12): 3505-3519. | |

| [22] | 陈凯杰, 唐振鹏, 吴俊传, 等. 贵金属期货价格预测方法及实证研究[J]. 中国管理科学, 2022, 30(12): 245-253. |

| Chen K J, Tang Z P, Wu J C, et al. Prediction method and empirical study of precious metal futures Price[J]. Chinese Journal of Management Science, 2022, 30(12): 245-253. | |

| [23] | E J, Ye J, Jin H. A novel hybrid model on the prediction of time series and its application for the gold price analysis and forecasting[J]. Physica A: Statistical Mechanics and Its Applications, 2019, 527: 121454. |

| [24] | 范丽伟, 董欢欢, 渐令, 等. 基于滚动时间窗的碳市场价格分解集成预测研究[J]. 中国管理科学, 2023, 31(1): 277-286. |

| Fan L W, Dong H H, Jian L, et al. A Decomposition ensemble model with sliding time window for forecasting carbon market prices [J]. Chinese Journal of Management Science, 2023, 31(1): 277-286. | |

| [25] | Chen Y, Yu S, Islam S, et al. Decomposition-based wind power forecasting models and their boundary issue: An in-depth review and comprehensive discussion on potential solutions[J]. Energy Reports, 2022, 8: 8805-8820. |

| [26] | Barzegar R, Aalami M T, Adamowski J. Coupling a hybrid CNN-LSTM deep learning model with a Boundary Corrected Maximal Overlap Discrete Wavelet Transform for multiscale Lake water level forecasting[J]. Journal of Hydrology, 2021, 598: 126196. |

| [27] | 崔明明, 刘晓亭, 李秀婷, 等. 数据特征驱动的房地产市场集成预测研究[J].管理评论,2020, 32(7): 89-101. |

| Cui M M, Liu X T, Li X T, et al. Integrated data characteristic driven forecasting research on real estate market[J]. Management Review, 2020, 32(7): 89-101. | |

| [28] | Yu L, Ma M. A memory-trait-driven decomposition- reconstruction-ensemble learning paradigm for oil price forecasting[J]. Applied Soft Computing, 2021, 111: 107699. |

| [29] | 王方, 赵桉坤, 余乐安. 数据特征驱动的新能源汽车月度销量二次分解集成预测[J].中国管理科学, 2024, DOI:10.16381/j.cnki.issn1003-207x.2023.2035 . |

| Wang F, Zhao A K, Yu L A.Quadratic decomposition- ensemble method for multi-step forecast of monthly sales volume of new energy vehicles [J]. Chinese Journal of Management Science, 2024, DOI: 10.16381/j.cnki.issn1003-207x.2023.2035 . | |

| [30] | Yu L, Liang S, Chen R, et al. Predicting monthly biofuel production using a hybrid ensemble forecasting methodology[J]. International Journal of Forecasting, 2022, 38(1): 3-20. |

| [31] | 秦全德, 黄兆荣, 黄凯珊. 一种基于局部回归的多尺度碳市场价格预测模型研究[J]. 运筹与管理, 2022, 31(1): 107-114. |

| Qin Q D, Huang Z R, Huang K S. A multi-scale carbon price forecasting model withLocal regression approach[J]. Operations Research and Management Science, 2022, 31(1): 107-114. | |

| [32] | Athanasopoulos G, Hyndman R J, Kourentzes N, et al. Forecast reconciliation: A review[J]. International Journal of Forecasting, 2024, 40(2): 430-456. |

| [33] | Dragomiretskiy K, Zosso D. Variational mode decomposition[J]. IEEE Transactions on Signal Processing, 2014, 62(3): 531-544. |

| [34] | Huang D, Jiang F, Li K, et al. Scaled PCA: A new approach to dimension reduction[J]. Management Science, 2022, 68(3): 1678-1695. |

| [35] | Wang J, Guo X, Tan X, et al. Which exogenous driver is informative in forecasting European carbon volatility: Bond, commodity, stock or uncertainty?[J]. Energy Economics, 2023, 117: 106419. |

| [36] | He M, Zhang Y, Wen D, et al. Forecasting crude oil prices: A scaled PCA approach[J]. Energy Economics, 2021, 97: 105189. |

| [37] | Zhang C H. Nearly unbiased variable selection under minimax concave penalty[J]. The Annals of Statistics, 2010, 38(2): 894-942. |

| [38] | 罗孝敏, 彭定涛, 张弦. 基于MCP正则的最小一乘回归问题研究[J]. 系统科学与数学, 2021, 41(8): 2327-2337. |

| Luo X M, Peng D T, Zhang X. On least absolute deviation regression problems with MCP regularization[J]. Journal of Systems Science and Mathematical Sciences, 2021, 41(8): 2327-2337. | |

| [39] | Lila M F, Meira E, Cyrino Oliveira F L. Forecasting unemployment in Brazil: A robust reconciliation approach using hierarchical data[J]. Socio-Economic Planning Sciences, 2022, 82: 101298. |

| [40] | Athanasopoulos G, Ahmed R A, Hyndman R J. Hierarchical forecasts for Australian domestic tourism[J]. International Journal of Forecasting, 2009, 25(1): 146-166. |

| [41] | Wickramasuriya S L, Athanasopoulos G, Hyndman R J. Optimal forecast reconciliation for hierarchical and grouped time series through trace minimization[J]. Journal of the American Statistical Association, 2019, 114(526): 804-819. |

| [42] | Cohen G, Aiche A. Forecasting gold price using machine learning methodologies[J]. Chaos, Solitons & Fractals, 2023, 175: 114079. |

| [43] | Gök R, Bouri E, Gemici E. Can Twitter-based economic uncertainty predict safe-haven assets under all market conditions and investment horizons?[J]. Technological Forecasting and Social Change, 2022, 185: 122091. |

| [44] | Hong Y, Ma F, Wang L, et al. How does the COVID-19 outbreak affect the causality between gold and the stock market? New evidence from the extreme Granger causality test[J]. Resources Policy, 2022, 78: 102859. |

| [45] | 蔡超敏, 凌立文, 牛超, 等. 国内猪肉市场价格的EMD-SVM集成预测模型[J]. 中国管理科学, 2016, 24(S1): 845-851. |

| Cai C M, Ling L W, Niu C, et al. Integration prediction of domestic pork market price based on empirical mode decomposition and support vector machine[J]. Chinese Journal of Management Science, 2016, 24(S1): 845-851. | |

| [46] | Xiao N, Xu Q S. Multi-step adaptive elastic-net: Reducing false positives in high-dimensional variable selection[J]. Journal of Statistical Computation and Simulation, 2015, 85(18): 3755-3765. |

| [47] | 刘金培, 罗瑞, 陈华友, 等. 非结构化数据驱动的混合二次分解汇率区间多尺度组合预测[J]. 中国管理科学, 2023, 31(6): 60-70. |

| Liu J P, Luo R, Chen H Y, et al. Multi-scale combination forecasting of interval exchange rate with hybrid secondary decomposition driven by unstructured data [J]. Chinese Journal of Management Science, 2023, 31(6): 60-70. | |

| [48] | Zhou F, Huang Z, Zhang C. Carbon price forecasting based on CEEMDAN and LSTM[J]. Applied Energy, 2022, 311: 118601. |

| [49] | Pan W T. Mixed modified fruit fly optimization algorithm with general regression neural network to build oil and gold prices forecasting model[J]. Kybernetes, 2014, 43(7): 1053-1063. |

| [50] | Wen F, Yang X, Gong X, et al. Multi-scale volatility feature analysis and prediction of gold price[J]. International Journal of Information Technology & Decision Making, 2017, 16(1): 205-223. |

| [51] | Roh T Y, Lee B Y, Xu Y. Extracting gold risk premium via dimension reduction tools: Implication on the gold-inflation relationship[J]. Applied Economics Letters,2024, DOI:10.1080/13504851.2024.23640021 . |

| [52] | Varshini A, Kayal P, Maiti M. How good are different machine and deep learning models in forecasting the future price of metals? Full sample versus sub-sample[J]. Resources Policy, 2024, 92: 105040. |

| [1] | 范丽伟, 董欢欢, 渐令. 基于滚动时间窗的碳市场价格分解集成预测研究[J]. 中国管理科学, 2023, 31(1): 277-286. |

| [2] | 陈凯杰, 唐振鹏, 吴俊传, 张婷婷, 杜晓旭. 贵金属期货价格预测方法及实证研究[J]. 中国管理科学, 2022, 30(12): 245-253. |

| [3] | 曾能民, 张明, 余乐安. 基于“拆分-填充-分解-集成”的我国线上零售额预测研究[J]. 中国管理科学, 2022, 30(12): 63-76. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||