主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

中国管理科学 ›› 2026, Vol. 34 ›› Issue (3): 39-50.doi: 10.16381/j.cnki.issn1003-207x.2022.0618cstr: 32146.14.j.cnki.issn1003-207x.2022.0618

蒋志强1, 胡海燕1, 戴鹏飞2( ), 王莉1, 周炜星1

), 王莉1, 周炜星1

收稿日期:2022-03-29

修回日期:2022-07-02

出版日期:2026-03-25

发布日期:2026-03-06

通讯作者:

戴鹏飞

E-mail:pfdai@whut.edu.cn

基金资助:

Zhiqiang Jiang1, Haiyan Hu1, Pengfei Dai2(), Li Wang1, Weixing Zhou1

Received:2022-03-29

Revised:2022-07-02

Online:2026-03-25

Published:2026-03-06

Contact:

Pengfei Dai

E-mail:pfdai@whut.edu.cn

摘要:

将粮食价格维持在合理范围,防止极端波动发生是保障国家粮食安全的首要任务。本文以粮食期货价格为研究对象,聚焦粮食期货价格极端波动,运用事件流模型对极端波动的发生规模和发生过程同时建模,并应用于极端风险测度的计算。针对中美粮食期货(CBOT稻谷、CBOT小麦、CBOT玉米、郑商早籼、郑商强麦、大商玉米)价格的研究表明,事件流模型可以较好地刻画粮食期货价格波动的胖尾特征和集聚特征,对极端波动的发生规律和发生规模表现出较好的拟合效果。针对极端风险测度的样本内外检验表明,事件流模型可有效地提升风险测度计算的准确性。本文的研究结果不仅有助于更好地理解粮食期货价格极端波动的发生模式,也为粮食价格风险管理和粮食市场平稳运行提供了科学思路和技术手段。

中图分类号:

蒋志强,胡海燕,戴鹏飞, 等. 基于事件流模型的粮食期货极端风险测度计算研究[J]. 中国管理科学, 2026, 34(3): 39-50.

Zhiqiang Jiang,Haiyan Hu,Pengfei Dai, et al. Estimating Extreme Risk Measures of Grain Future Market Based on Event Flow Models[J]. Chinese Journal of Management Science, 2026, 34(3): 39-50.

表1

期货收益率数据的描述性统计结果"

| 粮食期货 | 起始时间 | 均值 | 标准差 | 偏度 | 峰度 | JB统计量 | ADF统计量 | LB统计量 |

|---|---|---|---|---|---|---|---|---|

| CBOT稻谷 | 2000.01.01 | 0.021 | 1.907 | 0.189 | 47.261 | 424891.125*** | -68.039*** | 51.461*** |

| CBOT小麦 | 2000.01.01 | 0.024 | 1.894 | 0.026 | 8.240 | 6259.317*** | -72.974*** | 10.634 |

| CBOT玉米 | 2000.01.01 | 0.040 | 1.616 | 0.202 | 4.783 | 751.940*** | -69.853*** | 27.100*** |

| 郑商早籼 | 2009.04.20 | 0.008 | 0.905 | 0.696 | 8.016 | 2451.313*** | -49.254*** | 20.073** |

| 郑商强麦 | 2003.03.28 | -0.013 | 0.768 | 0.054 | 7.033 | 2809.193*** | -64.060*** | 15.026 |

| 大商玉米 | 2004.09.22 | 0.024 | 0.756 | 0.240 | 6.665 | 2301.564*** | -66.919*** | 27.097*** |

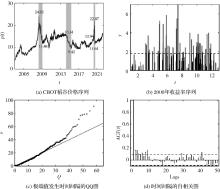

图1

样本数据基本统计分析结果"

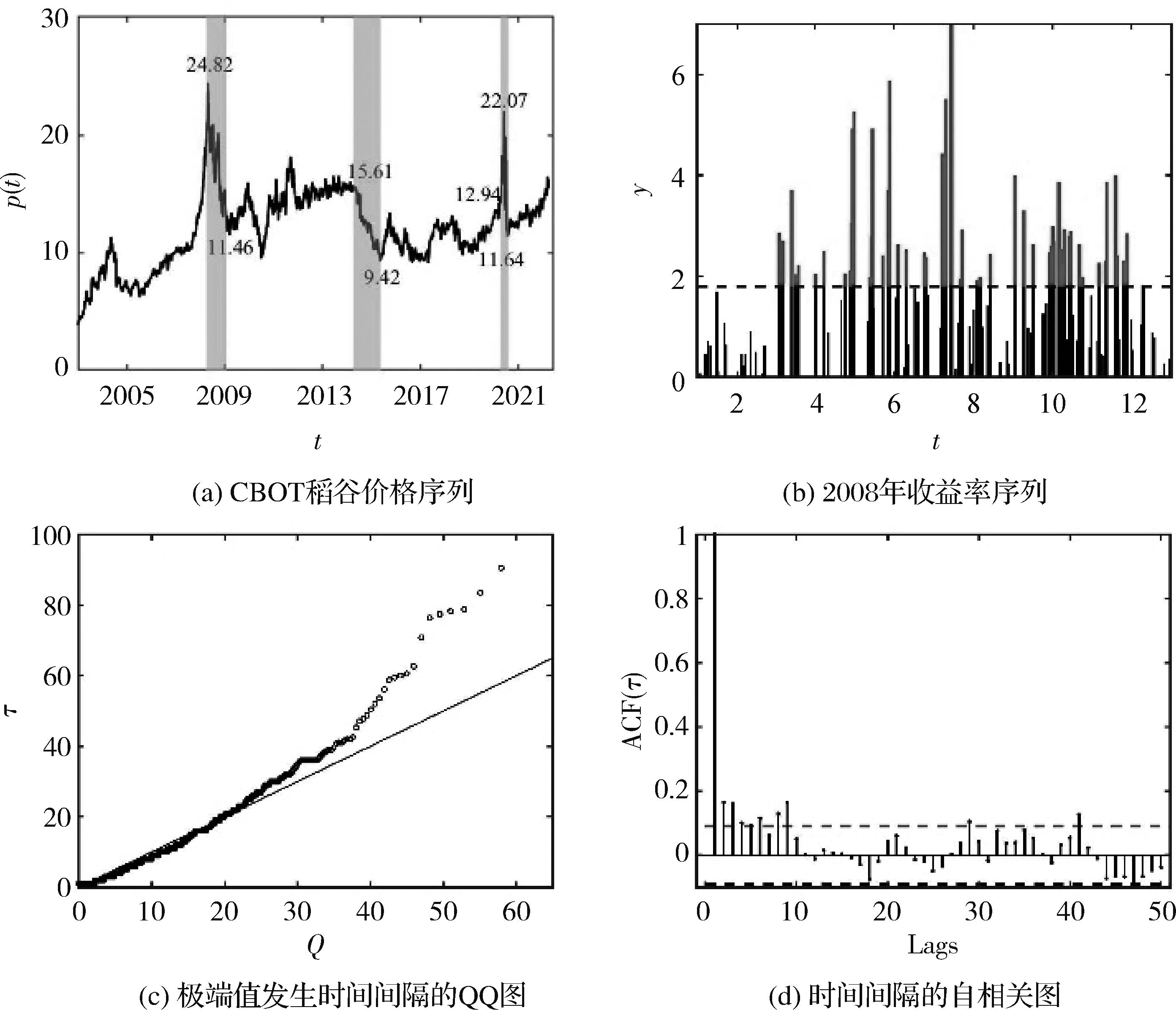

图2

样本内拟合优度检验结果"

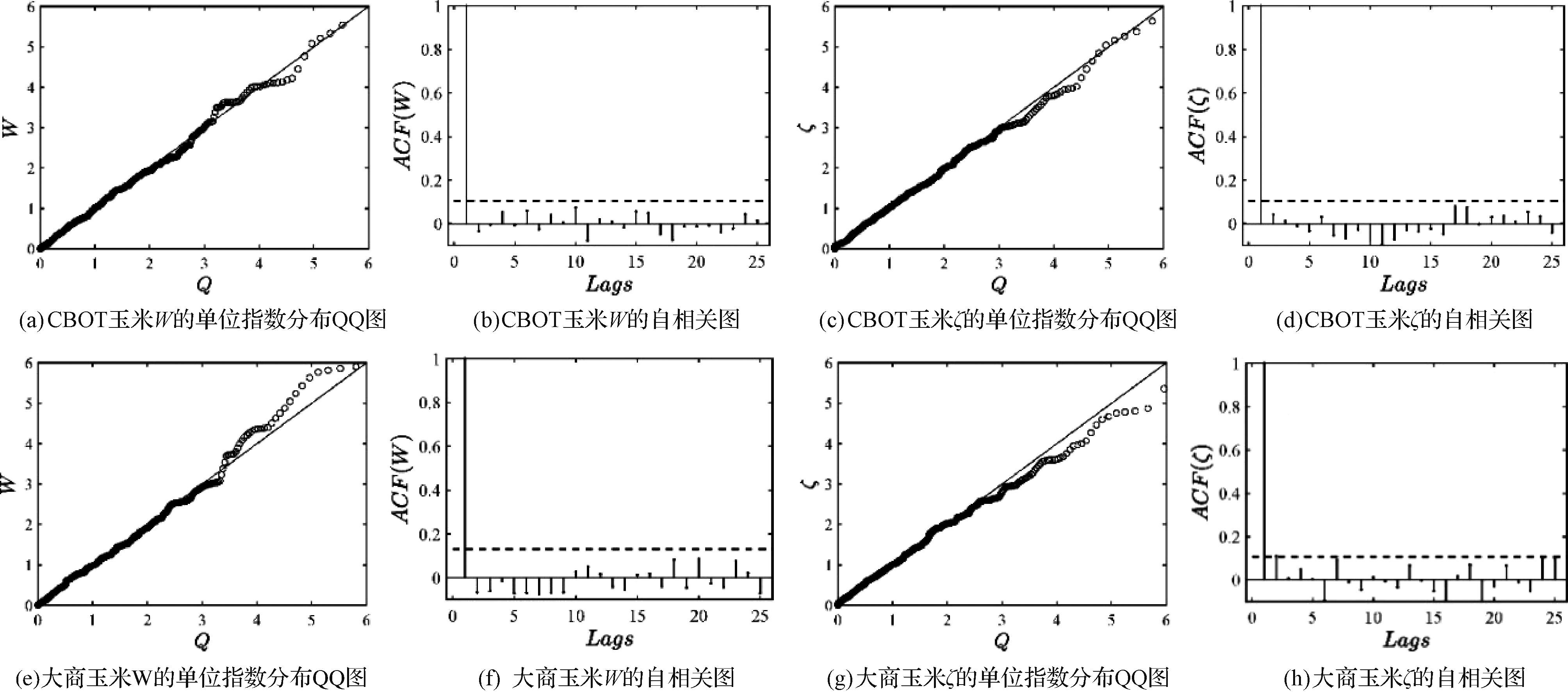

图3

CBOT玉米收益率和不同模型VaR估计值的比较分析"

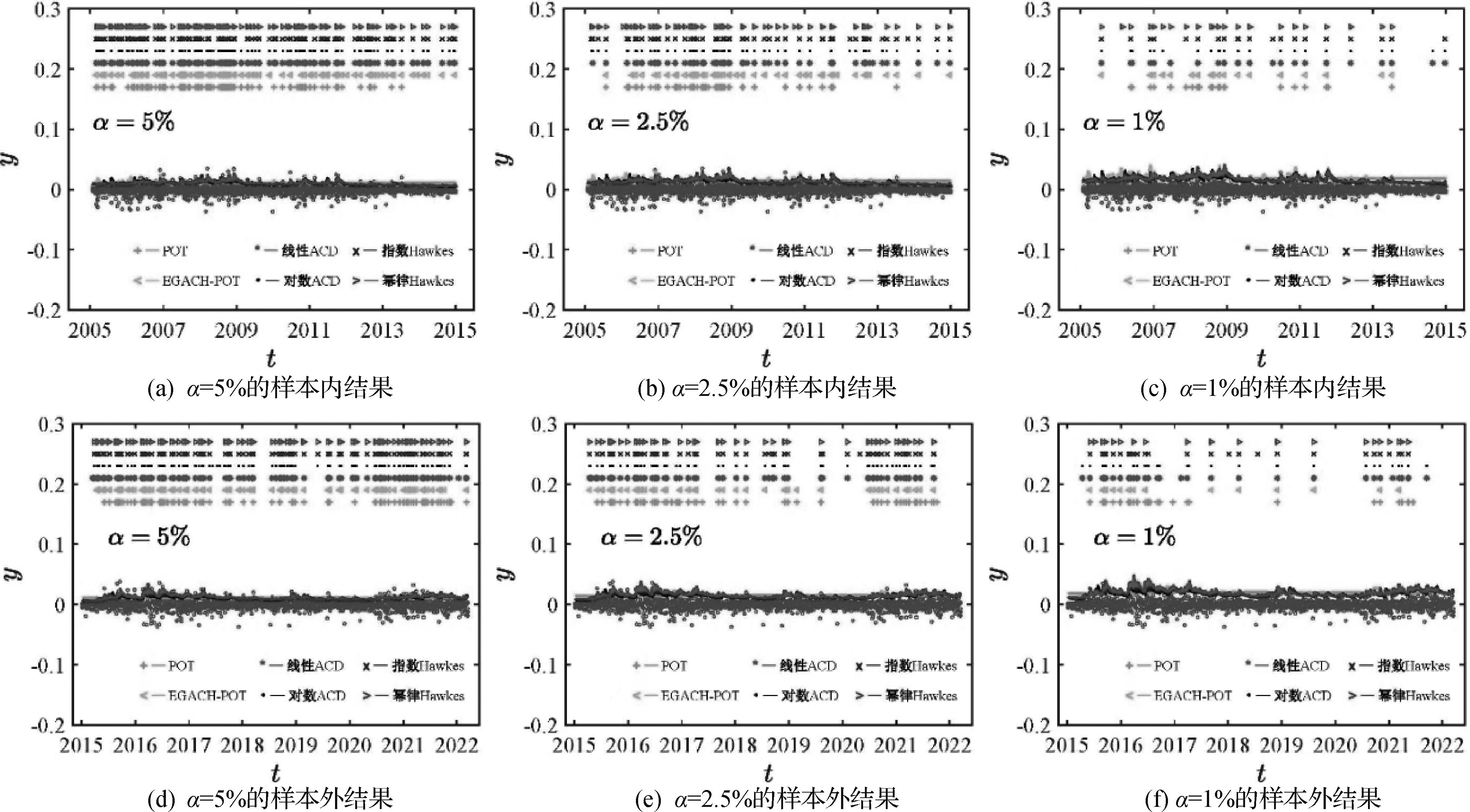

图4

大商玉米收益率和不同模型VaR估计值的比较分析图。(a-c)样本内结果。(d-f)样本外结果。"

表2

ACD-POT模型和Hawkes-POT模型的样本内参数估计和拟合优度检验"

| 模型 | ACD模型参数 | Hawkes过程参数 | POT模型参数 | lnL | AIC | 拟合优度检验 | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ω | a | b | γ | κ | μ | n | δ | η | ρ | ξ | β0 | β1 | β2 | KS W | KS ζ | |||

| CBOT稻谷 | ||||||||||||||||||

| 线性 | 1.121 | 0.237 | 0.700 | 0.660 | 1.121 | 0.129 | 0.520 | 0.190 | 2.253 | -1535.6 | 3089.2 | 0.292 | 0.367 | |||||

| ACD | (0.196) | (0.026) | (0.020) | (0.030) | (0.196) | (0.034) | (0.058) | (0.043) | (0.505) | |||||||||

| 对数 | 0.436 | 0.205 | 0.671 | 0.666 | 1.500 | 0.124 | 0.512 | 0.192 | 2.330 | -1534.0 | 3085.9 | 0.322 | 0.283 | |||||

| ACD | (0.023) | (0.013) | (0.010) | (0.031) | (0.143) | (0.034) | (0.058) | (0.044) | (0.498) | |||||||||

| 指数 | 0.037 | 0.553 | 0.048 | 0.036 | 0.184 | 0.620 | 2.738 | -1544.1 | 3102.1 | 0.492 | 0.306 | |||||||

| 衰减 | (0.004) | (0.048) | (0.024) | (0.008) | (0.037) | (0.059) | (0.501) | |||||||||||

| 幂律 | 0.039 | 0.268 | 0.201 | 0.843 | 0.161 | 0.166 | 0.518 | 3.754 | -1544.2 | 3104.3 | 0.445 | 0.337 | ||||||

| 衰减 | (0.004) | (0.025) | (0.016) | (0.502) | (0.023) | (0.034) | (0.058) | (0.511) | ||||||||||

| CBOT小麦 | ||||||||||||||||||

| 线性 | 0.723 | 0.158 | 0.789 | 0.888 | 1.126 | -0.068 | 0.420 | -0.014 | 5.697 | -1543.3 | 3104.5 | 0.113 | 0.063 | |||||

| ACD | (0.098) | (0.012) | (0.010) | (0.032) | (0.054) | (0.025) | (0.048) | (0.034) | (0.445) | |||||||||

| 对数 | 0.516 | 0.159 | 0.661 | 0.852 | 1.174 | -0.055 | 0.526 | 0.020 | 4.407 | -1550.2 | 3118.5 | 0.195 | 0.090 | |||||

| ACD | (0.018) | (0.009) | (0.008) | (0.033) | (0.062) | (0.027) | (0.049) | (0.036) | (0.459) | |||||||||

| 指数 | 0.040 | 0.213 | 0.317 | 0.013 | -0.062 | 0.334 | 6.163 | -1538.3 | 3090.6 | 0.160 | 0.135 | |||||||

| 衰减 | (0.004) | (0.017) | (0.022) | (0.004) | (0.026) | (0.046) | 0.450 | |||||||||||

| 幂律 | 0.046 | 0.404 | 0.380 | 0.014 | 1.128 | -0.052 | 0.394 | 5.546 | -1540.4 | 3096.7 | 0.175 | 0.096 | ||||||

| 衰减 | (0.004) | (0.037) | (0.016) | (0.005) | (0.137) | (0.026) | (0.046) | 0.455 | ||||||||||

| CBOT玉米 | ||||||||||||||||||

| 线性 | 3.247 | 0.241 | 0.505 | 0.659 | 1.517 | -0.061 | 0.350 | 0.025 | 5.392 | -1492.2 | 3002.3 | 0.980 | 0.139 | |||||

| ACD | (0.291) | (0.033) | (0.026) | (0.026) | (0.130) | (0.035) | (0.044) | (0.035) | (0.448) | |||||||||

| 对数 | 0.909 | 0.180 | 0.493 | 0.645 | 1.551 | -0.061 | 0.372 | 0.019 | 5.313 | -1494.7 | 3007.4 | 0.967 | 0.183 | |||||

| ACD | (0.030) | (0.016) | (0.012) | (0.025) | (0.137) | (0.036) | (0.045) | (0.036) | (0.450) | |||||||||

| 指数 | 0.051 | 0.199 | 0.314 | 0.051 | -0.076 | 0.446 | 4.809 | -1491.4 | 2996.8 | 0.982 | 0.174 | |||||||

| 衰减 | (0.004) | (0.021) | (0.033) | (0.012) | (0.034) | (0.045) | (0.439) | |||||||||||

| 幂律 | 0.045 | 0.311 | 0.364 | 0.120 | 0.562 | -0.066 | 0.476 | 4.444 | -1491.3 | 2998.6 | 0.940 | 0.226 | ||||||

| 衰减 | (0.004) | (0.031) | (0.024) | (0.045) | (0.058) | (0.032) | (0.044) | (0.443) | ||||||||||

| 郑商早籼 | ||||||||||||||||||

| 线性 | 3.028 | 0.230 | 0.536 | 0.671 | 1.491 | 0.158 | 0.160 | -0.045 | 2.252 | -434.2 | 886.4 | 0.731 | 0.098 | |||||

| ACD | (0.470) | (0.058) | (0.044) | (0.045) | (0.202) | (0.093) | (0.038) | (0.072) | (0.363) | |||||||||

| 对数 | 1.083 | 0.155 | 0.438 | 0.636 | 1.572 | 0.158 | 0.198 | -0.045 | 1.915 | -435.0 | 888.1 | 0.969 | 0.131 | |||||

| ACD | (0.062) | (0.032) | (0.026) | (0.045) | (0.242) | (0.095) | (0.038) | (0.072) | (0.364) | |||||||||

| 指数 | 0.065 | 0.232 | 0.412 | 0.096 | 0.175 | 0.211 | 1.573 | -436.5 | 887.0 | 0.959 | 0.137 | |||||||

| 衰减 | (0.008) | (0.068) | (0.193) | (0.046) | (0.096) | (0.038) | (0.362) | |||||||||||

| 幂律 | 0.051 | 0.183 | 0.352 | 9.999 | 2E-6 | 0.168 | 0.200 | 1.667 | -435.3 | 886.5 | 0.978 | 0.141 | ||||||

| 衰减 | (0.008) | (0.038) | (0.073) | (61.02) | (0.031) | (0.095) | (0.038) | (0.356) | ||||||||||

| 郑商强麦 | ||||||||||||||||||

| 线性 | 1.995 | 0.323 | 0.542 | 0.710 | 1.408 | -0.100 | 0.505 | 0.173 | 0.774 | -1001.9 | 2021.7 | 0.985 | 0.123 | |||||

| ACD | (0.316) | (0.043) | (0.034) | (0.041) | (0.149) | (0.038) | (0.036) | (0.060) | (0.309) | |||||||||

| 对数 | 0.554 | 0.259 | 0.577 | 0.680 | 1.470 | -0.099 | 0.494 | 0.167 | 0.891 | -1004.0 | 2026.1 | 0.986 | 0.172 | |||||

| ACD | (0.034) | (0.017) | (0.014) | (0.040) | (0.169) | (0.037) | (0.036) | (0.060) | (0.315) | |||||||||

| 指数 | 0.024 | 0.340 | 0.504 | 0.031 | -0.093 | 0.481 | 1.743 | -1003.3 | 2020.7 | 0.938 | 0.214 | |||||||

| 衰减 | (0.005) | (0.027) | (0.041) | (0.008) | (0.036) | (0.035) | (0.322) | |||||||||||

| 幂律 | 0.021 | 0.427 | 0.736 | 0.082 | 0.658 | -0.100 | 0.493 | 1.651 | -1003.1 | 2022.3 | 0.991 | 0.256 | ||||||

| 衰减 | (0.004) | (0.034) | (0.036) | (0.027) | (0.061) | (0.037) | (0.036) | (0.319) | ||||||||||

| 大商玉米 | ||||||||||||||||||

| 线性 | 0.158 | 0.028 | 0.669 | 0.599 | 4.199 | -0.024 | 0.226 | -0.016 | 1.997 | -788.4 | 1594.8 | 0.605 | 0.144 | |||||

| ACD | (0.026) | (0.004) | (0.024) | (0.015) | (0.052) | (0.046) | (0.029) | (0.048) | (0.238) | |||||||||

| 对数 | 0.061 | 0.280 | 0.519 | 0.548 | 3.317 | -0.036 | 0.237 | -0.018 | 1.938 | -787.2 | 1592.4 | 0.760 | 0.123 | |||||

| ACD | (0.036) | (0.019) | (0.033) | (0.019) | (0.067) | (0.047) | (0.029) | (0.049) | (0.233) | |||||||||

| 指数 | 0.025 | 0.701 | 0.069 | 0.033 | -0.014 | 0.238 | 1.823 | -793.7 | 1601.4 | 0.636 | 0.374 | |||||||

| 衰减 | (0.005) | (0.056) | (0.066) | (0.007) | (0.048) | (0.029) | (0.241) | |||||||||||

| 幂律 | 0.020 | 0.428 | 0.779 | 0.116 | 0.460 | -0.014 | 0.275 | 1.507 | -795.6 | 1607.2 | 0.655 | 0.380 | ||||||

| 衰减 | (0.005) | (0.036) | (0.044) | (0.046) | (0.041) | (0.047) | (0.029) | (0.235) | ||||||||||

表3

ACD-POT模型样本内外VaR估计值准确性检验结果"

| 模型 | α(%) | 线性ACD-POT | 对数ACD-POT | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 失败 | LRuc | LRind | LRcc | DQhit | DQVaR | 失败 | LRuc | LRind | LRcc | DQhit | DQVaR | ||

| 样本内检验 | |||||||||||||

CBOT 稻谷 | 5 | 190 | 0.30 | 0.00 | 0.00 | 0.00 | 0.00 | 190 | 0.30 | 0.00 | 0.00 | 0.00 | 0.00 |

| 2.5 | 87 | 0.89 | 0.03 | 0.08 | 0.01 | 0.00 | 91 | 0.77 | 0.04 | 0.11 | 0.03 | 0.01 | |

| 1 | 39 | 0.54 | 0.08 | 0.17 | 0.00 | 0.00 | 40 | 0.44 | 0.09 | 0.17 | 0.00 | 0.00 | |

CBOT 小麦 | 5 | 199 | 0.21 | 0.03 | 0.05 | 0.28 | 0.28 | 202 | 0.14 | 0.09 | 0.08 | 0.27 | 0.25 |

| 2.5 | 90 | 0.90 | 0.27 | 0.54 | 0.80 | 0.75 | 92 | 0.93 | 0.12 | 0.29 | 0.36 | 0.33 | |

| 1 | 35 | 0.81 | 0.35 | 0.63 | 0.92 | 0.92 | 36 | 0.94 | 0.37 | 0.67 | 0.85 | 0.84 | |

CBOT 玉米 | 5 | 191 | 0.36 | 0.00 | 0.00 | 0.00 | 0.00 | 197 | 0.17 | 0.00 | 0.00 | 0.00 | 0.00 |

| 2.5 | 93 | 0.71 | 0.00 | 0.00 | 0.00 | 0.00 | 91 | 0.87 | 0.00 | 0.00 | 0.00 | 0.00 | |

| 1 | 37 | 0.84 | 0.40 | 0.69 | 0.78 | 0.78 | 36 | 0.97 | 0.38 | 0.68 | 0.84 | 0.79 | |

郑商 早籼 | 5 | 69 | 0.35 | 0.12 | 0.20 | 0.08 | 0.03 | 69 | 0.36 | 0.12 | 0.20 | 0.16 | 0.10 |

| 2.5 | 34 | 0.58 | 0.08 | 0.18 | 0.01 | 0.00 | 33 | 0.71 | 0.01 | 0.04 | 0.00 | 0.00 | |

| 1 | 16 | 0.32 | 0.02 | 0.03 | 0.00 | 0.00 | 16 | 0.32 | 0.02 | 0.03 | 0.00 | 0.00 | |

郑商 强麦 | 5 | 211 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 183 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| 2.5 | 71 | 0.60 | 0.00 | 0.00 | 0.00 | 0.00 | 68 | 0.88 | 0.00 | 0.00 | 0.00 | 0.00 | |

| 1 | 27 | 0.96 | 0.00 | 0.01 | 0.00 | 0.00 | 26 | 0.89 | 0.00 | 0.01 | 0.00 | 0.00 | |

大商 玉米 | 5 | 127 | 0.28 | 1.00 | 0.56 | 0.89 | 0.78 | 125 | 0.37 | 0.38 | 0.46 | 0.90 | 0.88 |

| 2.5 | 55 | 0.71 | 0.57 | 0.79 | 1.00 | 0.99 | 57 | 0.92 | 0.63 | 0.89 | 1.00 | 1.00 | |

| 1 | 23 | 0.98 | 0.23 | 0.48 | 0.54 | 0.53 | 23 | 0.98 | 0.50 | 0.79 | 0.83 | 0.81 | |

| 样本外检验 | |||||||||||||

CBOT 稻谷 | 5 | 84 | 0.75 | 0.00 | 0.00 | 0.00 | 0.00 | 77 | 0.63 | 0.00 | 0.00 | 0.00 | 0.00 |

| 2.5 | 39 | 0.80 | 0.00 | 0.00 | 0.00 | 0.00 | 40 | 0.92 | 0.00 | 0.00 | 0.00 | 0.00 | |

| 1 | 20 | 0.37 | 0.00 | 0.00 | 0.00 | 0.00 | 17 | 0.85 | 0.01 | 0.04 | 0.00 | 0.00 | |

CBOT 小麦 | 5 | 96 | 0.43 | 0.41 | 0.52 | 0.74 | 0.46 | 90 | 0.88 | 0.79 | 0.96 | 0.73 | 0.63 |

| 2.5 | 48 | 0.58 | 0.78 | 0.83 | 0.95 | 0.78 | 45 | 0.92 | 0.89 | 0.99 | 0.99 | 0.98 | |

| 1 | 20 | 0.60 | 0.50 | 0.69 | 0.71 | 0.14 | 15 | 0.50 | 0.61 | 0.70 | 0.49 | 0.28 | |

CBOT 玉米 | 5 | 83 | 0.56 | 0.01 | 0.02 | 0.14 | 0.10 | 80 | 0.36 | 0.00 | 0.01 | 0.06 | 0.06 |

| 2.5 | 48 | 0.57 | 0.00 | 0.01 | 0.00 | 0.00 | 47 | 0.67 | 0.00 | 0.01 | 0.00 | 0.00 | |

| 1 | 34 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 31 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

郑商 早籼 | 5 | 82 | 0.00 | 0.59 | 0.00 | 0.00 | 0.00 | 83 | 0.00 | 0.40 | 0.00 | 0.00 | 0.00 |

| 2.5 | 56 | 0.00 | 0.44 | 0.00 | 0.00 | 0.00 | 55 | 0.00 | 0.17 | 0.00 | 0.00 | 0.00 | |

| 1 | 24 | 0.00 | 0.68 | 0.00 | 0.00 | 0.00 | 26 | 0.00 | 0.79 | 0.00 | 0.00 | 0.00 | |

郑商 强麦 | 5 | 69 | 0.81 | 0.00 | 0.01 | 0.01 | 0.00 | 68 | 0.71 | 0.01 | 0.02 | 0.03 | 0.00 |

| 2.5 | 31 | 0.43 | 0.00 | 0.01 | 0.00 | 0.00 | 32 | 0.55 | 0.01 | 0.02 | 0.01 | 0.00 | |

| 1 | 14 | 0.96 | 0.00 | 0.00 | 0.00 | 0.00 | 16 | 0.64 | 0.00 | 0.00 | 0.00 | 0.00 | |

大商 玉米 | 5 | 106 | 0.02 | 0.20 | 0.03 | 0.23 | 0.10 | 107 | 0.01 | 0.11 | 0.01 | 0.11 | 0.05 |

| 2.5 | 62 | 0.00 | 0.10 | 0.00 | 0.03 | 0.02 | 61 | 0.01 | 0.09 | 0.01 | 0.04 | 0.04 | |

| 1 | 31 | 0.00 | 0.13 | 0.00 | 0.00 | 0.00 | 29 | 0.01 | 0.10 | 0.01 | 0.00 | 0.00 | |

表4

Hawkes-POT模型样本内外VaR估计值准确性检验结果"

| 模型 | α(%) | 指数Hawkes-POT | 幂律Hawkes-POT | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 失败 | LRuc | LRind | LRcc | DQhit | DQVaR | 失败 | LRuc | LRind | LRcc | DQhit | DQVaR | ||

| 样本内检验 | |||||||||||||

CBOT 稻谷 | 5 | 173 | 0.83 | 0.01 | 0.02 | 0.00 | 0.00 | 183 | 0.58 | 0.26 | 0.45 | 0.35 | 0.35 |

| 2.5 | 85 | 0.76 | 0.22 | 0.44 | 0.00 | 0.00 | 85 | 0.76 | 0.22 | 0.44 | 0.32 | 0.24 | |

| 1 | 30 | 0.37 | 0.26 | 0.35 | 0.00 | 0.00 | 31 | 0.47 | 0.28 | 0.43 | 0.04 | 0.03 | |

CBOT 小麦 | 5 | 183 | 0.92 | 0.22 | 0.46 | 0.87 | 0.86 | 184 | 0.86 | 0.23 | 0.48 | 0.79 | 0.79 |

| 2.5 | 81 | 0.29 | 0.41 | 0.40 | 0.66 | 0.64 | 82 | 0.34 | 0.91 | 0.63 | 0.66 | 0.65 | |

| 1 | 28 | 0.15 | 0.21 | 0.16 | 0.68 | 0.57 | 29 | 0.21 | 0.23 | 0.22 | 0.75 | 0.61 | |

CBOT 玉米 | 5 | 177 | 0.93 | 0.02 | 0.06 | 0.38 | 0.38 | 184 | 0.66 | 0.04 | 0.11 | 0.47 | 0.44 |

| 2.5 | 79 | 0.27 | 0.85 | 0.53 | 0.03 | 0.02 | 80 | 0.32 | 0.88 | 0.60 | 0.28 | 0.26 | |

| 1 | 37 | 0.82 | 0.40 | 0.69 | 0.91 | 0.91 | 32 | 0.53 | 0.45 | 0.62 | 0.97 | 0.97 | |

郑商 早籼 | 5 | 67 | 0.44 | 0.47 | 0.57 | 0.67 | 0.64 | 66 | 0.52 | 0.79 | 0.79 | 0.55 | 0.48 |

| 2.5 | 30 | 0.92 | 0.04 | 0.11 | 0.06 | 0.06 | 31 | 0.93 | 0.79 | 0.96 | 0.70 | 0.69 | |

| 1 | 11 | 0.72 | 0.66 | 0.85 | 1.00 | 1.00 | 13 | 0.82 | 0.60 | 0.85 | 1.00 | 1.00 | |

郑商 强麦 | 5 | 133 | 0.99 | 0.01 | 0.03 | 0.04 | 0.03 | 131 | 0.87 | 0.09 | 0.22 | 0.55 | 0.46 |

| 2.5 | 76 | 0.25 | 0.00 | 0.00 | 0.00 | 0.00 | 67 | 0.94 | 0.12 | 0.30 | 0.68 | 0.58 | |

| 1 | 19 | 0.12 | 0.01 | 0.01 | 0.00 | 0.00 | 23 | 0.48 | 0.20 | 0.33 | 0.25 | 0.25 | |

大商 玉米 | 5 | 117 | 0.83 | 0.37 | 0.65 | 0.40 | 0.40 | 118 | 0.76 | 0.15 | 0.34 | 0.58 | 0.38 |

| 2.5 | 56 | 0.85 | 0.74 | 0.93 | 0.96 | 0.95 | 60 | 0.73 | 0.62 | 0.83 | 0.99 | 0.96 | |

| 1 | 20 | 0.53 | 0.55 | 0.69 | 0.73 | 0.73 | 22 | 0.84 | 0.51 | 0.79 | 0.99 | 0.91 | |

| 样本外检验 | |||||||||||||

CBOT 稻谷 | 5 | 74 | 0.41 | 0.00 | 0.00 | 0.00 | 0.00 | 63 | 0.03 | 0.00 | 0.00 | 0.01 | 0.00 |

| 2.5 | 40 | 0.92 | 0.00 | 0.00 | 0.00 | 0.00 | 30 | 0.08 | 0.02 | 0.01 | 0.08 | 0.05 | |

| 1 | 20 | 0.37 | 0.00 | 0.00 | 0.00 | 0.00 | 14 | 0.57 | 0.62 | 0.75 | 0.50 | 0.29 | |

CBOT 小麦 | 5 | 92 | 0.72 | 0.92 | 0.93 | 0.77 | 0.76 | 89 | 0.97 | 0.80 | 0.97 | 0.79 | 0.73 |

| 2.5 | 48 | 0.58 | 0.78 | 0.83 | 0.95 | 0.95 | 47 | 0.69 | 0.81 | 0.90 | 0.97 | 0.97 | |

| 1 | 19 | 0.76 | 0.52 | 0.78 | 0.71 | 0.71 | 19 | 0.76 | 0.52 | 0.78 | 0.71 | 0.71 | |

CBOT 玉米 | 5 | 70 | 0.04 | 0.03 | 0.01 | 0.19 | 0.19 | 66 | 0.01 | 0.01 | 0.00 | 0.07 | 0.06 |

| 2.5 | 47 | 0.67 | 0.01 | 0.03 | 0.05 | 0.04 | 47 | 0.67 | 0.04 | 0.12 | 0.21 | 0.18 | |

| 1 | 24 | 0.15 | 0.00 | 0.01 | 0.00 | 0.00 | 22 | 0.32 | 0.28 | 0.34 | 0.68 | 0.68 | |

郑商 早籼 | 5 | 68 | 0.00 | 0.72 | 0.00 | 0.03 | 0.03 | 64 | 0.00 | 0.86 | 0.02 | 0.10 | 0.10 |

| 2.5 | 40 | 0.00 | 0.49 | 0.00 | 0.01 | 0.01 | 33 | 0.03 | 0.11 | 0.03 | 0.05 | 0.03 | |

| 1 | 15 | 0.06 | 0.47 | 0.13 | 0.20 | 0.09 | 11 | 0.48 | 0.60 | 0.68 | 0.98 | 0.83 | |

郑商 强麦 | 5 | 77 | 0.47 | 0.08 | 0.16 | 0.20 | 0.03 | 81 | 0.23 | 0.05 | 0.08 | 0.10 | 0.02 |

| 2.5 | 35 | 0.93 | 0.06 | 0.18 | 0.60 | 0.10 | 37 | 0.80 | 0.09 | 0.22 | 0.69 | 0.40 | |

| 1 | 16 | 0.64 | 0.01 | 0.04 | 0.00 | 0.00 | 19 | 0.22 | 0.02 | 0.04 | 0.00 | 0.00 | |

大商 玉米 | 5 | 101 | 0.07 | 0.23 | 0.09 | 0.37 | 0.32 | 99 | 0.10 | 0.62 | 0.23 | 0.64 | 0.52 |

| 2.5 | 58 | 0.02 | 0.06 | 0.01 | 0.06 | 0.06 | 48 | 0.36 | 0.21 | 0.30 | 0.62 | 0.56 | |

| 1 | 27 | 0.02 | 0.45 | 0.05 | 0.14 | 0.12 | 20 | 0.45 | 0.49 | 0.59 | 0.95 | 0.90 | |

| [1] | Engle R F. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation[J]. Econometrica, 1982, 50(4): 987-1007. |

| [2] | Herrera R. Energy risk management through self-exciting marked point process[J]. Energy Economics, 2013, 38: 64-76. |

| [3] | Herrera R, Rodriguez A, Pino G. Modeling and forecasting extreme commodity prices: A Markov-Switching based extreme value model[J]. Energy Economics, 2017, 63: 129-143. |

| [4] | Hawkes J. A lower lipschitz condition for the stable subordinator[J]. Zeitschrift Für Wahrscheinlichkeitstheorie und Verwandte Gebiete, 1971, 17(1): 23-32. |

| [5] | Chavez-Demoulin V, Davison A C, McNeil A J. Estimating value-at-risk: A point process approach[J]. Quantitative Finance, 2005, 5(2): 227-234. |

| [6] | Aït-Sahalia Y. Maximum likelihood estimation of discretely sampled diffusions: A closed-form approximation approach[J].Econometrica,2002,70(1): 223-262. |

| [7] | 刘志东, 郑雪飞. 基于Hawkes因子模型的股价共同跳跃研究[J]. 中国管理科学, 2018, 26(7): 18-31. |

| Liu Z D, Zheng X F. A study of stock price co-jumps with hawkes factor model[J]. Chinese Journal of Management Science, 2018, 26(7): 18-31. | |

| [8] | 汪冬华, 张裕恒. 基于Hawkes过程中美股市大幅波动互激效应的研究[J]. 中国管理科学, 2018, 26(7): 32-39. |

| Wang D H, Zhang Y H. Research on large volatility mutually exciting effect of Chinese and American stock markets based on hawkes process[J]. Chinese Journal of Management Science, 2018, 26(7): 32-39. | |

| [9] | 张峭, 王川, 王克. 我国畜产品市场价格风险度量与分析[J]. 经济问题, 2010(3): 90-94. |

| Zhang Q, Wang C, Wang K. Measure and analyze price risk for livestock in China[J]. On Economic Problems, 2010(3): 90-94. | |

| [10] | 王川, 赵俊晔, 钟永玲. 我国粮食市场风险的度量与评估——基于风险价值法的实证分析[J]. 中国农业资源与区划, 2012, 33(2): 15-22. |

| Wang C, Zhao J Y, Zhong Y L. Quantifying and assessment of the grain market risk in China[J]. Chinese Journal of Agricultural Resources and Regional Planning, 2012, 33(2): 15-22. | |

| [11] | 韩德宗. 基于VaR的我国商品期货市场风险的预警研究[J]. 管理工程学报, 2008, 22(1): 117-121. |

| Han D Z. Study on early warning of risk of commodity futures market in China based on measurement of VaR[J]. Journal of Industrial Engineering and Engineering Management, 2008, 22(1): 117-121. | |

| [12] | 谢赤, 贺慧敏, 王纲金, 等. 基于复杂网络的泛金融市场极端风险溢出效应及其演变研究[J]. 系统工程理论与实践, 2021, 41(8): 1926-1941. |

| Xie C, He H M, Wang G J, et al. Extreme risk spillover effects of pan-financial markets and its evolution based on complex networks[J]. Systems Engineering-Theory & Practice, 2021, 41(8): 1926-1941. | |

| [13] | 李秋萍, 李长健, 肖小勇. 产业链视角下农产品价格溢出效应研究——基于三元VAR-BEKK-GARCH(1, 1)模型[J]. 财贸经济, 2014, 35(10): 125-136. |

| Li Q P, Li C J, Xiao X Y. Spillover effect of agricultural product price in the perspective of agricultural chain: Based on VAR-BEKK-GARCH(1, 1) model[J]. Finance & Trade Economics, 2014, 35(10): 125-136. | |

| [14] | Caballero R J, Krishnamurthy A. Bubbles and capital flow volatility: Causes and risk management[J]. Journal of Monetary Economics, 2006, 53(1): 35-53. |

| [15] | Gutierrez L. Speculative bubbles in agricultural commodity markets[J]. European Review of Agricultural Economics, 2013, 40(2): 217-238. |

| [16] | Liu X, Filler G, Odening M. Testing for speculative bubbles in agricultural commodity prices: A regime switching approach[J]. Agricultural Finance Review, 2013, 73(1): 179-200. |

| [17] | Etienne X L, Irwin S H, Garcia P. Bubbles in food commodity markets: Four decades of evidence[J]. Journal of International Money and Finance, 2014, 42: 129-155. |

| [18] | Etienne X L, Irwin S H, Garcia P. Price explosiveness, speculation, and grain futures prices[J]. American Journal of Agricultural Economics, 2015, 97(1): 65-87. |

| [19] | 王燕青, 王晓蜀, 武拉平. 我国农产品期货市场的价格泡沫检验: 以鸡蛋期货为例[J]. 农业技术经济, 2015(12): 78-88. |

| Wang Y Q, Wang X S, Wu L P. Price bubble test in China’s agricultural products futures market: Taking egg futures as an example[J]. Journal of Agrotechnical Economics, 2015(12): 78-88. | |

| [20] | 黄慧莲, 熊涛, 李崇光. 我国农产品期货市场价格泡沫特征及品种差异性研究[J]. 农业技术经济, 2018(1): 32-47. |

| Huang H L, Xiong T, Li C G. Prices bubbles and differences in Chinese agricultural commodity futures markets[J]. Journal of Agrotechnical Economics, 2018(1): 32-47. | |

| [21] | Sanders D R, Irwin S H. Bubbles, froth and facts: Another look at the masters hypothesis in commodity futures markets[J]. Journal of Agricultural Economics, 2017, 68(2): 345-365. |

| [22] | Mao Q, Ren Y, Loy J P. Price bubbles in agricultural commodity markets and contributing factors: Evidence for corn and soybeans in China[J]. China Agricultural Economic Review, 2021, 13(1): 22-53. |

| [23] | 姬新龙, 周孝华. 基于马尔科夫随机波动和极值理论的风险测度[J]. 中国管理科学, 2014, 22(10): 44-51. |

| Ji X L, Zhou X H. Risk measurement based on Markov stochastic volatility and EVT[J]. Chinese Journal of Management Science, 2014, 22(10): 44-51. | |

| [24] | Jiang Z Q, Canabarro A, Podobnik B, et al. Early warning of large volatilities based on recurrence interval analysis in Chinese stock markets[J]. Quantitative Finance, 2016, 16(11): 1713-1724. |

| [25] | Jiang Z Q, Wang G J, Canabarro A, et al. Short term prediction of extreme returns based on the recurrence interval analysis[J]. Quantitative Finance, 2018, 18(3): 353-370. |

| [26] | Zhang M Y, Russell J R, Tsay R S. A nonlinear autoregressive conditional duration model with applications to financial transaction data[J]. Journal of Econometrics, 2001, 104(1): 179-207. |

| [27] | Kupiec P H. Techniques for verifying the accuracy of risk measurement models[J]. The Journal of Derivatives, 1995, 3(2): 73-84. |

| [28] | Christoffersen P F. Evaluating interval forecasts[J]. International Economic Review, 1998, 39(4): 841–862. |

| [29] | Engle R F, Manganelli S. CAViaR: Conditional autoregressive value at risk by regression quantiles[J]. Journal of Business & Economic Statistics, 2004, 22(4): 367-381. |

| [30] | Hajirahimi Z, Khashei M. Hybrid structures in time series modeling and forecasting: A review[J]. Engineering Applications of Artificial Intelligence, 2019, 86: 83-106. |

| [1] | 姚银红, 王晓旭, 陈炜, 陈振松. 基于Transformer-LSTM分位数回归的全球股市极端风险溢出研究[J]. 中国管理科学, 2025, 33(8): 1-13. |

| [2] | 杨科, 刘鑫, 田凤平. 中国与其他主要新兴市场国家间股市极端风险的跨市场传染[J]. 中国管理科学, 2025, 33(7): 44-53. |

| [3] | 宋诗佳, 田飞, 李汉东. 基于时变极值方法的VaR预测模型以及应用[J]. 中国管理科学, 2025, 33(2): 61-70. |

| [4] | 汪冬华, 姚钰雯, 王暖. 基于Hawkes过程的国际原油市场与中国股票市场大幅波动联动性研究[J]. 中国管理科学, 2022, 30(8): 36-43. |

| [5] | 黄金波, 吴莉莉, 尤亦玲. 非对称Laplace分布下的均值-VaR模型[J]. 中国管理科学, 2022, 30(5): 31-40. |

| [6] | 唐振鹏, 吴俊传, 冉梦, 张婷婷. 考虑投资者情绪的中国股市自激发效应研究[J]. 中国管理科学, 2020, 28(7): 1-12. |

| [7] | 李红权, 何敏园, 黄莹莹. 我国金融机构的系统重要性评估:基于多元极值理论[J]. 中国管理科学, 2020, 28(5): 14-24. |

| [8] | 杨坤, 于文华, 魏宇. 基于R-vine copula的原油市场极端风险动态测度研究[J]. 中国管理科学, 2017, 25(8): 19-29. |

| [9] | 黄金波, 李仲飞, 丁杰. 基于非参数核估计方法的均值-VaR模型[J]. 中国管理科学, 2017, 25(5): 1-10. |

| [10] | 任龙, 刘骏. 考虑下侧风险厌恶参与者的技术外包合同研究[J]. 中国管理科学, 2017, 25(4): 184-189. |

| [11] | 黄金波, 李仲飞, 周鸿涛. 期望效用视角下的风险对冲效率[J]. 中国管理科学, 2016, 24(3): 9-17. |

| [12] | 谢海滨, 田军, 汪寿阳. 极端风险下中国股市的反应特征研究[J]. 中国管理科学, 2015, 23(11): 39-45. |

| [13] | 张晨, 丁洋, 汪文隽. 国际碳市场风险价值度量的新方法——基于EVT-CAViaR模型[J]. 中国管理科学, 2015, 23(11): 12-20. |

| [14] | 姬新龙, 周孝华. 基于马尔科夫随机波动和极值理论的风险测度[J]. 中国管理科学, 2014, 22(10): 44-51. |

| [15] | 陆静, 张佳. 基于极值理论和多元Copula函数的商业银行操作风险计量研究[J]. 中国管理科学, 2013, 21(3): 11-19. |

| 阅读次数 | ||||||

|

全文 |

|

|||||

|

摘要 |

|

|||||

|

||