主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (11): 29-40.doi: 10.16381/j.cnki.issn1003-207x.2024.0438

Previous Articles Next Articles

Gang Li1, Chaochao Qiu1, Zhipeng Zhang2( ), Simeng Qin1, Xingnan Xue1

), Simeng Qin1, Xingnan Xue1

Received:2024-03-28

Revised:2024-07-05

Online:2025-11-25

Published:2025-11-28

Contact:

Zhipeng Zhang

E-mail:zhangzhipeng@sjtu.edu.cn

CLC Number:

Gang Li,Chaochao Qiu,Zhipeng Zhang, et al. Research on Predicting Corporate Fraud of Listed Companies Based on Multi-Source Text Data and Feature-Augmented Tree Models[J]. Chinese Journal of Management Science, 2025, 33(11): 29-40.

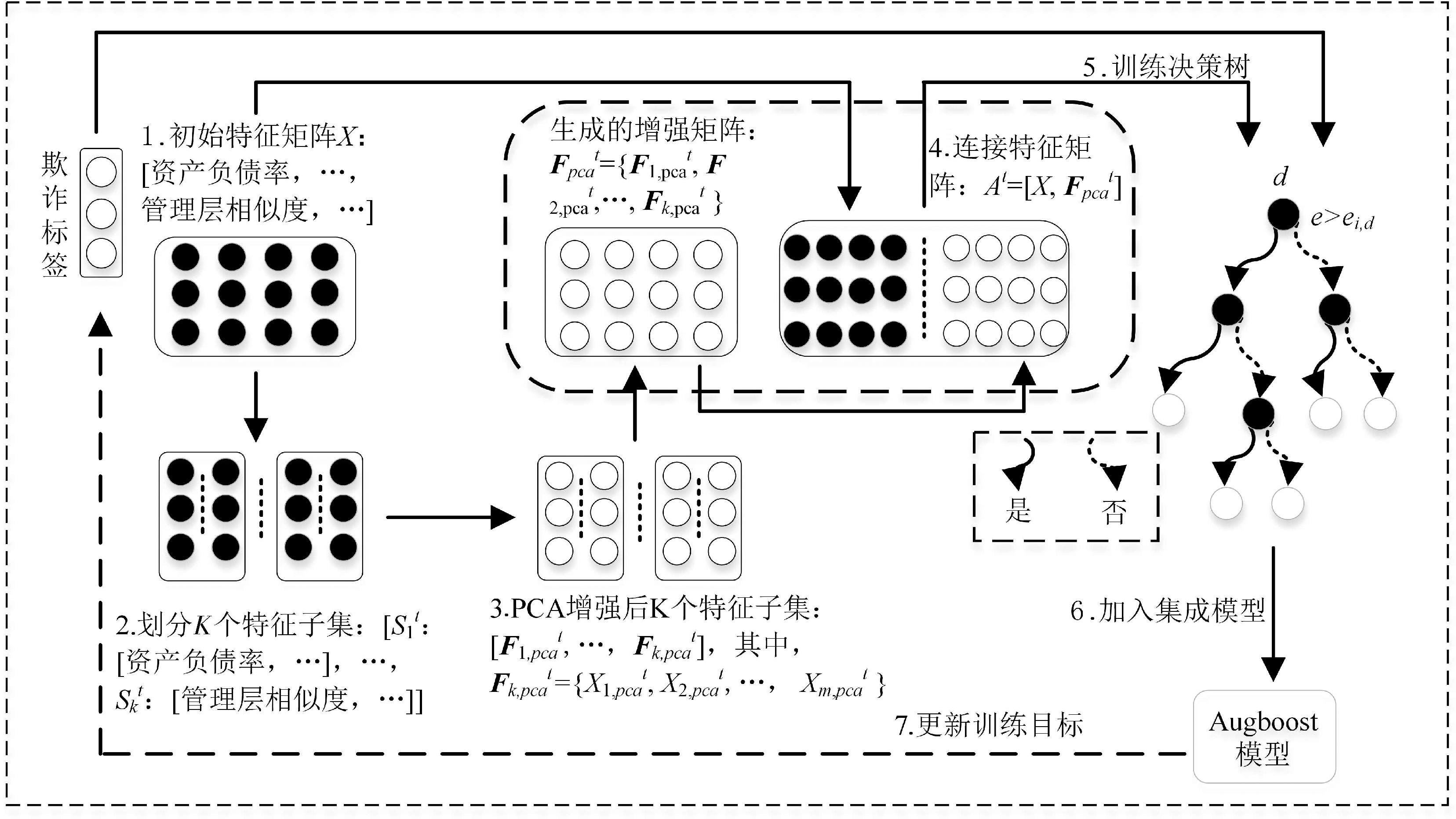

"

"

| 序号 | 1 | 2 | 3 | … | 4217 | … | 6748 |

|---|---|---|---|---|---|---|---|

| 积极词 | 敬献 | 敬业 | 爱国心 | … | 尊法 | ||

| 消极词 | 贫乏 | 劫数 | 短视 | … | 猖狂 | … | 哀悼 |

"

| 股票代码-年份 | 上市公司年报文本 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 文本相似度 | 文本净语调 | 文本负语调 | 文本可读性 | 短视指标 | 竞争战略 | |||||

| 短视综合指标 | 数月 | … | 还款压力 | Cost | Diff | |||||

| 000004-2010 | 0.690 | 0.754 | 0.123 | 56.857 | 0.259 | 0.833 | 0.965 | 0.003 | 0.001 | |

| 000004-2011 | 0.590 | 0.448 | 0.276 | 52.313 | 0.295 | 0.474 | 0.549 | 0.005 | 0.001 | |

| … | … | … | … | … | … | … | … | … | … | … |

| 000016-2001 | 0.597 | 0.398 | 0.301 | 43.645 | 0.193 | 1.242 | 1.440 | 0.008 | 0.003 | |

| 000016-2002 | 0.523 | 0.813 | 0.093 | 191.286 | 0.000 | 1.085 | 1.257 | 0.003 | 0.005 | |

| … | … | … | … | … | … | … | … | … | … | … |

| 688981-2020 | 0.825 | 0.171 | 0.414 | 55.247 | 0.032 | 0.102 | 0.096 | 0.003 | 0.002 | |

"

| 股票代码-年份 | 央行文本 | 省级政府工作报告文本 | ||||||

|---|---|---|---|---|---|---|---|---|

| 文本相似度 | 文本净语调 | 文本负语调 | 文本可读性 | 文本相似度 | 文本净语调 | 文本负语调 | 文本可读性 | |

| 000004-2010 | 0.313 | 0.582 | 0.209 | 45.461 | 0.699 | 0.862 | 0.069 | 33.813 |

| 000004-2011 | 0.421 | 0.427 | 0.287 | 45.096 | 0.707 | 0.903 | 0.048 | 28.723 |

| … | … | … | … | … | … | … | … | … |

| 000016-2001 | 0.512 | 0.499 | 0.251 | 46.161 | 0.655 | 0.848 | 0.076 | 34.569 |

| 000016-2002 | 0.512 | 0.552 | 0.224 | 48.429 | 0.736 | 0.811 | 0.094 | 31.425 |

| … | … | … | … | … | … | … | … | … |

| 688981-2020 | 0.484 | 0.584 | 0.208 | 45.718 | 0.702 | 0.171 | 0.414 | 55.247 |

"

| 样本数 | 初始特征矩阵 | |||

|---|---|---|---|---|

| X1 | X2 | … | X146 | |

| 1 | 1.6175 | 1.2867 | … | 0.005233 |

| 2 | 0.3553 | 0.3441 | … | 0.001661 |

| 3 | 1.75361 | 1.1987 | … | 0.004289 |

| … | … | … | … | … |

| 12866 | 0.3010 | 0.1617 | … | 0.005182 |

| 12867 | 1.3127 | 0.9226 | … | 0.000947 |

| 增强后矩阵 | ||||

| X’1 | X’2 | … | X’146 | |

| 1 | -0.2557714 | -0.03033657 | … | -0.426517 |

| 2 | -0.2569253 | -0.06300148 | … | 0.0241909 |

| 3 | 0.18951760 | -0.06886076 | … | 0.0418108 |

| … | … | … | … | … |

| 12866 | -0.2366145 | -0.04575666 | … | -0.033644 |

| 12867 | -0.2381984 | 0.002320920 | … | 0.7880405 |

"

| 序号 | 模型 | AUC | KS | G-mean | F-score | Precision | Recall | Accuracy | BM |

|---|---|---|---|---|---|---|---|---|---|

| 1 | Augboost | 0.723 | 0.340 | 0.652 | 0.394 | 0.298 | 0.581 | 0.707 | 0.313 |

| 2 | LR | 0.466 | 0.014 | 0.081 | 0.013 | 0.240 | 0.007 | 0.834 | 0.013 |

| 3 | NB | 0.536 | 0.025 | 0.164 | 0.283 | 0.165 | 0.983 | 0.184 | 0.081 |

| 4 | DT | 0.560 | 0.118 | 0.480 | 0.266 | 0.260 | 0.272 | 0.754 | 0.120 |

| 5 | KNN | 0.518 | 0.026 | 0.197 | 0.067 | 0.218 | 0.040 | 0.819 | 0.029 |

| 6 | RF | 0.720 | 0.058 | 0.100 | 0.020 | 0.563 | 0.010 | 0.836 | 0.331 |

| 7 | LDA | 0.685 | 0.070 | 0.172 | 0.056 | 0.397 | 0.030 | 0.834 | 0.283 |

| 8 | ANN | 0.501 | 0.007 | 0.066 | 0.009 | 0.211 | 0.004 | 0.834 | 0.004 |

| 9 | Ada | 0.691 | 0.199 | 0.630 | 0.360 | 0.257 | 0.600 | 0.651 | 0.276 |

"

| 序号 | 指标组合 | AUC | KS | G-mean | F-score | Accuracy | BM | Precision | Recall |

|---|---|---|---|---|---|---|---|---|---|

| 0 | T | 0.627 | 0.188 | 0.582 | 0.314 | 0.622 | 0.169 | 0.224 | 0.529 |

| 1 | A | 0.635 | 0.208 | 0.595 | 0.328 | 0.642 | 0.197 | 0.237 | 0.534 |

| 2 | A+T | 0.674 | 0.253 | 0.615 | 0.348 | 0.658 | 0.235 | 0.253 | 0.558 |

| 3 | A+B | 0.670 | 0.258 | 0.615 | 0.350 | 0.663 | 0.238 | 0.256 | 0.553 |

| 4 | A+B+T | 0.690 | 0.273 | 0.621 | 0.357 | 0.673 | 0.250 | 0.263 | 0.554 |

| 5 | A+B+C | 0.702 | 0.304 | 0.632 | 0.372 | 0.693 | 0.276 | 0.280 | 0.555 |

| 6 | A+B+C+T | 0.720 | 0.321 | 0.647 | 0.387 | 0.700 | 0.302 | 0.291 | 0.577 |

| 7 | A+B+C+D | 0.722 | 0.327 | 0.642 | 0.384 | 0.702 | 0.294 | 0.290 | 0.565 |

| 8 | A+B+C+D+T | 0.723 | 0.340 | 0.652 | 0.394 | 0.707 | 0.313 | 0.298 | 0.580 |

"

| 模型序号 | 指标 | AUC | KS | G-mean | F-score | Accuracy | BM | Precision | Recall |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 管理层文本指标 | 0.586 | 0.140 | 0.564 | 0.297 | 0.604 | 0.133 | 0.210 | 0.511 |

| 2 | 政府文本指标 | 0.584 | 0.118 | 0.552 | 0.287 | 0.564 | 0.106 | 0.196 | 0.537 |

| 3 | 央行文本指标 | 0.605 | 0.162 | 0.578 | 0.310 | 0.580 | 0.156 | 0.212 | 0.574 |

| 4 | T | 0.627 | 0.188 | 0.582 | 0.314 | 0.622 | 0.169 | 0.224 | 0.529 |

| 5 | A | 0.635 | 0.208 | 0.595 | 0.328 | 0.642 | 0.197 | 0.237 | 0.534 |

| 6 | A+管理层文本指标 | 0.650 | 0.225 | 0.600 | 0.336 | 0.661 | 0.212 | 0.248 | 0.524 |

| 7 | A+政府文本指标 | 0.650 | 0.227 | 0.603 | 0.336 | 0.648 | 0.212 | 0.243 | 0.543 |

| 8 | A+央行文本指标 | 0.668 | 0.242 | 0.614 | 0.347 | 0.651 | 0.233 | 0.250 | 0.565 |

| 9 | A+T | 0.674 | 0.253 | 0.615 | 0.348 | 0.658 | 0.235 | 0.253 | 0.558 |

"

| 模型序号 | 指标构成 | 非文本指标% | 文本指标% | 央行文本指标% | 政府文本指标% | 管理层文本指标% |

|---|---|---|---|---|---|---|

| 2 | A+T | 57.8 | 42.2 | 7.0 | 6.9 | 28.3 |

| 4 | A+B+T | 70.5 | 29.5 | 6.0 | 5.7 | 17.8 |

| 6 | A+B+C+T | 76.2 | 23.8 | 4.1 | 4.0 | 15.7 |

| 8 | A+B+C+D+T | 84.7 | 15.3 | 0.8 | 2.8 | 11.7 |

"

| 指标 | 数据集 | 方法 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| ADT | Bag | BagNN | Boost | LMT | RF | RotFor | SGB | Augboost | ||

| KS | AC | 0.742 | 0.736 | 0.739 | 0.734 | 0.744 | 0.751 | 0.750 | 0.740 | 0.815 |

| GC | 0.429 | 0.437 | 0.487 | 0.443 | 0.403 | 0.457 | 0.431 | 0.412 | 0.467 | |

| GMC | 0.567 | 0.545 | 0.530 | 0.563 | 0.524 | 0.573 | 0.518 | 0.567 | 0.574 | |

| 综合排序 | 5 | 6.333 | 5 | 6 | 7 | 2.333 | 6 | 5.667 | 1.333 | |

| ACC | AC | 0.863 | 0.856 | 0.858 | 0.856 | 0.861 | 0.865 | 0.865 | 0.858 | 0.874 |

| GC | 0.734 | 0.744 | 0.757 | 0.740 | 0.729 | 0.751 | 0.739 | 0.728 | 0.750 | |

| GMC | 0.924 | 0.922 | 0.923 | 0.924 | 0.923 | 0.925 | 0.922 | 0.924 | 0.937 | |

| 综合排序 | 4.667 | 6.667 | 4.333 | 5.333 | 6.333 | 2 | 5.333 | 6 | 1.667 | |

| AUC | AC | 0.929 | 0.922 | 0.927 | 0.930 | 0.930 | 0.931 | 0.929 | 0.928 | 0.952 |

| GC | 0.758 | 0.779 | 0.802 | 0.772 | 0.747 | 0.789 | 0.773 | 0.751 | 0.777 | |

| GMC | 0.860 | 0.847 | 0.838 | 0.860 | 0.833 | 0.864 | 0.820 | 0.860 | 0.864 | |

| 综合排序 | 5 | 6 | 5.333 | 4 | 6.667 | 1.667 | 6.333 | 6 | 2 | |

| [1] | Dyck A, Morse A, Zingales L. Who blows the whistle on corporate fraud?[J]. The Journal of Finance, 2010, 65(6): 2213-2253. |

| [2] | 谢碧鹭. 去年超30家上市公司因财务造假被处罚[N]. 经济参考报, 2024-01-08(4). |

| Xie B L. Last year, more than 30 listed companies were punished for financial fraud[N]. Economic Information Daily, 2024-01-08(4). | |

| [3] | 中国证券监督管理委员会. 证监会要闻: 证监会依法从严打击欺诈发行、财务造假等信息披露违法行为[EB/OL]. (2024-02-04) [2024-03-08]. . |

| China Securities Regulatory Commission. CSRC News: CSRC severely crack down on fraudulent issuance, financial fraud and other information disclosure violations [EB/OL]. (2024-02-04) [2024-03-08]. . | |

| [4] | 姜富伟, 胡逸驰, 黄楠. 央行货币政策报告文本信息、宏观经济与股票市场[J]. 金融研究, 2021(6): 95-113. |

| Jiang F W, Hu Y C, Huang N. Textual information of central bank monetary policy report, macroeconomy and stock market performance[J]. Journal of Financial Research, 2021(6): 95-113. | |

| [5] | 陈艺云. 基于信息披露文本的上市公司财务困境预测: 以中文年报管理层讨论与分析为样本的研究[J]. 中国管理科学, 2019, 27(7): 23-34. |

| Chen Y Y. Forecasting financial distress of listed companies with textual content of the information disclosure: A study based MD & a in Chinese annual reports[J]. Chinese Journal of Management Science, 2019, 27(7): 23-34. | |

| [6] | 李爱华, 王迪文, 续维佳, 等. 基于多数据源融合的创业板上市公司财务造假异常检测[J]. 数据分析与知识发现, 2023, 7(5): 33-47. |

| Li A H, Wang D W, Xu W J, et al. Financial fraud detection for growth enterprise market listed companies based on data fusion[J]. Data Analysis and Knowledge Discovery, 2023, 7(5): 33-47. | |

| [7] | Bhattacharya I, Mickovic A. Accounting fraud detection using contextual language learning[J]. International Journal of Accounting Information Systems, 2024, 53: 100682. |

| [8] | Purda L, Skillicorn D. Accounting variables, deception, and a bag of words: Assessing the tools of fraud detection[J]. Contemporary Accounting Research, 2015, 32(3): 1193-1223. |

| [9] | 陈述, 游家兴, 朱书谊. 地方政府工作目标完成度与公司盈余管理——基于政府工作报告文本分析的视角[J]. 会计研究, 2022(6): 32-42. |

| Chen S, Yong J X, Zhu S Y. The completion degree of government work objectives and earnings management: From the perspective of government work report[J]. Accounting Research, 2022(6): 32-42. | |

| [10] | 林建浩, 陈良源, 罗子豪, 等. 央行沟通有助于改善宏观经济预测吗?——基于文本数据的高维稀疏建模[J]. 经济研究, 2021, 56(3): 48-64. |

| Lin J H, Chen L Y, Luo Z H, et al. Does central bank communication improve macroeconomic forecasting? High-dimensional sparse modeling based on text data[J]. Economic Research Journal,2021,56(3): 48-64. | |

| [11] | 胡楠, 邱芳娟, 梁鹏. 竞争战略与盈余质量——基于文本分析的实证研究[J]. 当代财经, 2020(9): 138-148. |

| Hu N, Qiu F J, Liang P. Competitive strategy and earnings quality: An empirical study based on text analysis[J]. Contemporary Finance & Economics, 2020(9): 138-148. | |

| [12] | 胡楠, 薛付婧, 王昊楠. 管理者短视主义影响企业长期投资吗?——基于文本分析和机器学习[J]. 管理世界, 2021, 37(5): 139-156+11+19-21. |

| Hu N, Xue F J, Wang H N. Does managerial myopia affect long-term Investment? Based on text analysis and machine learning[J]. Journal of Management World, 2021, 37(5): 139-156+11+19-21. | |

| [13] | 钱爱民, 朱大鹏. 财务报告文本相似度与违规处罚——基于文本分析的经验证据[J].会计研究,2020(9): 44-58. |

| Qian A M, Zhu D P. Financial report textual similarity and the likelihood of regulatory penalties: Based on the empirical evidence of textual analysis[J]. Accounting Research, 2020(9): 44-58. | |

| [14] | 李双燕, 蒋丽华, 卞舒晨. 年报文本情绪与上市公司违规行为识别——基于机器学习文本分析方法的实证研究[J]. 当代经济科学, 2023, 45(6): 97-109. |

| Li S Y, Jiang L H, Bian S C. Annual reports’ tone and violation behavior identification of listed companies: Evidence from textual analysis based on machine learning[J].Modern Economic Science,2023,45(6): 97-109. | |

| [15] | 郭松林, 宁祺器, 窦斌. 上市公司年报文本增量信息与违规风险预测——基于语调和可读性的视角[J]. 统计研究, 2022, 39(12): 69-84. |

| Guo S L, Ning Q Q, Dou B. Listed companies' annual report incremental text information and fraud risk prediction: From the perspective of tone and readability[J]. Statistical Research, 2022, 39(12): 69-84. | |

| [16] | 刘逸爽, 陈艺云. 管理层语调与上市公司信用风险预警——基于公司年报文本内容分析的研究[J]. 金融经济学研究, 2018, 33(4): 46-54. |

| Liu Y S, Chen Y Y. Tone at the top and credit risk warning for listed companies: Textual analysis of company annual reports[J]. Financial Economics Research, 2018, 33(4): 46-54. | |

| [17] | 伍翕婷, 游家兴, 于明洋. 政府言行一致与企业股价崩盘风险[J]. 系统工程理论与实践, 2024, 44(3): 853-873. |

| Wu X T, You J X, Yu M Y. Government’s actions according with words and stock price crash risk[J]. Systems Engineering-Theory & Practice, 2024, 44(3): 853-873. | |

| [18] | 陈艺云. 基于文本信息的上市中小企业财务困境预测研究[J]. 运筹与管理, 2022, 31(4): 136-143. |

| Chen Y Y. Financial distress prediction for listed SME based on the text information[J]. Operations Research and Management Science, 2022, 31(4): 136-143. | |

| [19] | 唐晓波, 谭明亮, 李诗轩, 等. 企业破产预测系统模型构建及实现研究[J].情报学报,2019,38(10):1051-1065. |

| Tang X B, Tan M L, Li S X, et al. Research on construction and implementation of a corporate bankruptcy prediction system model[J]. Journal of the China Society for Scientific and Technical Information, 2019, 38(10): 1051-1065. | |

| [20] | Altman E I. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy[J]. The Journal of Finance, 1968, 23(4): 589-609. |

| [21] | 方匡南, 范新妍, 马双鸽.基于网络结构Logistic模型的企业信用风险预警[J].统计研究,2016,33(4): 50-55. |

| Fang K N, Fan X Y, Ma S G. Forecasting of enterprise’s credit risk based on network-logistic model[J]. Statistical Research, 2016, 33(4): 50-55. | |

| [22] | Yu L, Yao X, Wang S, et al. Credit risk evaluation using a weighted least squares SVM classifier with design of experiment for parameter selection[J]. Expert Systems with Applications, 2011, 38(12): 15392-15399. |

| [23] | Lee T S, Chiu C C, Chou Y C, et al. Mining the customer credit using classification and regression tree and multivariate adaptive regression splines[J]. Computational Statistics & Data Analysis, 2006, 50(4): 1113-1130. |

| [24] | 李莹, 曲晓辉. 基于机器学习的公司违规预测研究[J]. 财务研究, 2022(4): 54-66. |

| Li Y, Qu X H. Corporate fraud prediction based on machine learning[J]. Finance Research, 2022(4): 54-66. | |

| [25] | Brown I, Mues C. An experimental comparison of classification algorithms for imbalanced credit scoring data sets[J]. Expert Systems with Applications, 2012, 39(3): 3446-3453. |

| [26] | Liu W, Fan H, Xia M. Credit scoring based on tree-enhanced gradient boosting decision trees[J]. Expert Systems with Applications, 2022, 189: 116034. |

| [27] | Liu W, Fan H, Xia M. Step-wise multi-grained augmented gradient boosting decision trees for credit scoring[J]. Engineering Applications of Artificial Intelligence, 2021, 97: 104036. |

| [28] | Khanna V, Kim E H, Lu Y. CEO connectedness and corporate fraud[J]. The Journal of Finance, 2015, 70(3): 1203-1252. |

| [29] | Denis D J, Hanouna P, Sarin A. Is there a dark side to incentive compensation?[J]. Journal of Corporate Finance, 2006, 12(3): 467-488. |

| [30] | Cornett M M, Marcus A J, Tehranian H. Corporate governance and pay-for-performance: The impact of earnings management[J]. Journal of Financial Economics, 2008, 87(2): 357-373. |

| [31] | Bao Y, Ke B, Li B, et al. Detecting accounting fraud in publicly traded U.S. firms using a machine learning approach[J]. Journal of Accounting Research, 2020, 58(1): 199-235. |

| [32] | Dechow P M, Ge W, Larson C R, et al. Predicting material accounting misstatements[J]. Contemporary Accounting Research, 2011, 28(1): 17-82. |

| [33] | 李建平, 孙灏, 常闫芃, 等. 考虑审计要素多重语义关联的财务欺诈识别[J]. 管理科学学报, 2024, 27(3): 58-70. |

| Li J P, Sun H, Chang Y P, et al. Financial statement fraud identification considering the multiple-dimensional semantic associations of auditing elements[J]. Journal of Management Sciences in China, 2024, 27(3): 58-70. | |

| [34] | 袁先智, 周云鹏, 严诚幸, 等. 财务欺诈风险特征筛选框架的建立和应用[J]. 中国管理科学, 2022, 30(3): 43-54. |

| Yuan X Z, Zhou Y P, Yan C X, et al. The framework for the risk feature extraction method on corporate financial fraud George[J]. Chinese Journal of Management Science, 2022, 30(3): 43-54. | |

| [35] | 王爱萍, 马奔, 胡海峰. 公司欺诈问题研究进展[J]. 经济学动态, 2019(2): 115-132. |

| Wang A P, Ma B, Hu H F. The progress of research on corporate fraud[J]. Economic Perspectives, 2019(2): 115-132. | |

| [36] | Wang T Y, Winton A. Competition and corporate fraud waves[C]//Proceedings of the 7th Annual Conference on Empirical Legal Studies, Palo Alto, California, November 9-10, 2012. |

| [37] | 张学勇, 施懿. 基于元学习的财务舞弊识别研究[J]. 管理科学学报, 2023, 26(10): 95-113. |

| Zhang X Y, Shi Y. Financial fraud recognition model based on meta-learning[J]. Journal of Management Sciences in China, 2023, 26(10): 95-113. | |

| [38] | 沈隆, 周颖. 管理层讨论与分析能预示企业违约吗?——基于中国股市的实证分析[J]. 系统管理学报, 2024, 33(2): 441-459. |

| Shen L, Zhou Y. Can management discussion and analysis predict corporate defaults? An empirical analysis based on the Chinese stock market[J]. Journal of Systems & Management, 2024, 33(2): 441-459. | |

| [39] | Lessmann S, Baesens B, Seow H V, et al. Benchmarking state-of-the-art classification algorithms for credit scoring: An update of research[J]. European Journal of Operational Research, 2015, 247(1): 124-136. |

| [40] | 周颖, 苏小婷. 基于最优指标组合的企业信用风险预测[J]. 系统管理学报, 2021, 30(5): 817-838. |

| Zhou Y, Su X T. Credit risk prediction of company based on optimal feature set[J]. Journal of Systems & Management, 2021, 30(5): 817-838. | |

| [41] | You J, Zhang B, Zhang L. Who captures the power of the pen?[J]. The Review of Financial Studies, 2018, 31(1): 43-96. |

| [1] | Zhongyi Hu, Diancheng Shui, Jiang Wu. Measurement and Evolution of Digitization Level of Chinese Listed Companies: Empirical Evidence from Annual Report Text [J]. Chinese Journal of Management Science, 2025, 33(4): 36-49. |

| [2] | Dan Hu, Lingyun Zhou, Liang Liang. Research on the Effect of Targeted Poverty Alleviation of Chinese Listed Companies on Increasing Farmers’ Income [J]. Chinese Journal of Management Science, 2025, 33(4): 12-23. |

| [3] | Wanhai You, Senjie Chen, Jianyong Chen, Yinghua Ren. The Impact of “More Words Than Deeds” on Environmental Responsibility on Stock Price Crash Risk: The Mediation Effect of Investor Sentiment [J]. Chinese Journal of Management Science, 2025, 33(10): 12-23. |

| [4] | Dawen Yan,Cun Li,Guotai Chi. Dynamic Financial Distress Prediction for Chinese Listed Companies Based on the Mixed Frequency Data [J]. Chinese Journal of Management Science, 2024, 32(1): 1-12. |

| [5] | DONG Bing-jie, CHI Guo-tai. Study on Default Prediction Based on Sentiment Data [J]. Chinese Journal of Management Science, 2023, 31(4): 111-120. |

| [6] | LIU Zhong-wen, DUAN Sheng-sen, YU Yi-hao. Research on the Selection of Equity Incentive Tools for Listed Companies Based on Efficiency Perspective [J]. Chinese Journal of Management Science, 2019, 27(11): 31-38. |

| [7] | MA Jian, LIU Zhi-Xin, ZHANG Li-Jian. Financing Decision in Chinese Listed Companies: A Perspective of Dual Heterogeneous Beliefs [J]. Chinese Journal of Management Science, 2012, (2): 50-56. |

| [8] | CAO Yu, CHEN Xiao-hong, WAN Guang-yu. Study on the Financing Structure of Listed Companies Based on Enterprise Life Cycle [J]. Chinese Journal of Management Science, 2009, 17(3): 150-158. |

| [9] | REN Xia-yi, LIU Xing. A Game Model Description and Anlysis on the Quality of Independent Audit of Chinese Listed Companies [J]. Chinese Journal of Management Science, 2006, (6): 124-130. |

| [10] | ZHANG De-ming, CAO Xiu-ying, ZHANG Guo-chun. Demonstrative Study on Fabricated Governance Mechanism of China Listed Companies [J]. Chinese Journal of Management Science, 2004, (4): 137-143. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||