主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2025, Vol. 33 ›› Issue (11): 1-13.doi: 10.16381/j.cnki.issn1003-207x.2021.2663

Chao Wang1( ), Jianmin He2, Xiaoxing Liu2

), Jianmin He2, Xiaoxing Liu2

Received:2021-12-23

Revised:2022-11-04

Online:2025-11-25

Published:2025-11-28

Contact:

Chao Wang

E-mail:wangchaoedu@njau.edu.cn

CLC Number:

Chao Wang,Jianmin He,Xiaoxing Liu. Investment Diversification, Business Similarity and Systemic Risk[J]. Chinese Journal of Management Science, 2025, 33(11): 1-13.

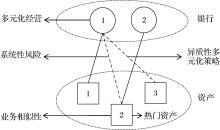

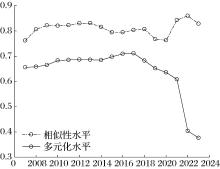

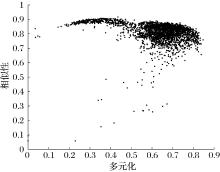

"

"

"

"

"

| (1) | (2) | (3) | |

|---|---|---|---|

| 门限值 | 0.55 | 0.41 | 0.51 |

0.12*** (0.03) | 0.49*** (0.06) | 0.25*** (0.04) | |

-0.17*** (0.02) | -0.12*** (0.02) | -0.16*** (0.02) | |

| 时间固定 | 是 | 否 | 是 |

| 类别固定 | 否 | 是 | 是 |

| 观测数量 | 2730 | 2730 | 2730 |

"

| 银行类别 | <门限值 | >门限值 | 平均值 | 数量 |

|---|---|---|---|---|

| A | 1.25% | 98.75% | 0.66 | 81 |

| B | 10.34% | 89.66% | 0.65 | 203 |

| C | 12.69% | 87.31% | 0.66 | 1032 |

| D | 20.41% | 79.59% | 0.58 | 1132 |

| E | 14.18% | 85.82% | 0.59 | 282 |

"

"

"

"

"

"

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| DIV | 0.97** (0.45) | 0.20*** (0.06) | 0.47 (0.41) | 0.97** (0.47) | 0.20*** (0.06) | 0.43 (0.43) |

| DIV2 | -1.56*** (0.40) | -0.58*** (0.06) | -0.69* (0.37) | -1.45*** (0.42) | -0.58*** (0.06) | -0.57 (0.39) |

| SIM | 3.12*** (0.14) | 3.14*** (0.15) | ||||

| CAP | -0.41*** (0.00) | -0.00 (0.00) | -0.41*** (0.00) | -0.41*** (0.00) | -0.00 (0.00) | -0.42*** (0.00) |

| ASS | 1.02*** (0.01) | -0.00*** (0.00) | 1.04*** (0.01) | 1.01*** (0.01) | -0.00*** (0.00) | 1.03*** (0.01) |

| 时间固定 | -0.41 (0.30) | 0.86*** (0.04) | -3.10*** (0.30) | -0.72** (0.31) | 0.86*** (0.04) | -3.41*** (0.32) |

| 类别固定 | 是 | 是 | 是 | 是 | 是 | 是 |

| 观测数量 | 是 | 是 | 是 | 是 | 是 | 是 |

| Adj. R2 | 2662 | 2729 | 2662 | 2658 | 2729 | 2658 |

| [1] | Roncoroni A, Battiston S, D’Errico M, et al. Interconnected banks and systemically important exposures[J]. Journal of Economic Dynamics and Control, 2021, 133: 104266. |

| [2] | 周爱民, 赵业翔. 价格冲击、资产抛售与银行网络系统性金融风险[J]. 财贸经济, 2023, 44(10): 40-56. |

| Zhou A M, Zhao Y X. Price shocks, fire sale and systemic financial risk in the banking network[J]. Finance & Trade Economics, 2023, 44(10): 40-56. | |

| [3] | Caccioli F, Farmer J D, Foti N, et al. Overlapping portfolios, contagion, and financial stability[J]. Journal of Economic Dynamics and Control, 2015, 51: 50-63. |

| [4] | Silva T C, da Silva Alexandre M, Tabak B M. Bank lending and systemic risk: A financial-real sector network approach with feedback[J]. Journal of Financial Stability, 2018, 38: 98-118. |

| [5] | 张天顶, 张宇. 模型不确定下我国商业银行系统性风险影响因素分析[J]. 国际金融研究, 2017(3): 45-54. |

| Zhang T D, Zhang Y. Analysis of systemic risk determinants of China’s commercial banks—Based on the model uncertainty[J]. Studies of International Finance, 2017(3): 45-54. | |

| [6] | Shim J. Loan portfolio diversification, market structure and bank stability[J]. Journal of Banking & Finance, 2019, 104: 103-115. |

| [7] | Cai J, Eidam F, Saunders A, et al. Syndication, interconnectedness, and systemic risk[J]. Journal of Financial Stability, 2018, 34: 105-120. |

| [8] | Wang C, Liu X, He J. Does diversification promote systemic risk?[J]. The North American Journal of Economics and Finance, 2022, 61: 101680. |

| [9] | 钱崇秀, 宋光辉, 许林. 信贷扩张、资产多元化与商业银行流动性风险[J].管理评论,2018, 30(12): 13-22. |

| Qian C X, Song G H, Xu L. Credit expansion, asset diversification and liquidity risk of commercial banks[J]. Management Review, 2018, 30(12): 13-22. | |

| [10] | 张琳, 廉永辉. 债券投资如何影响商业银行系统性风险?——基于系统性风险分解的视角[J]. 国际金融研究, 2020(2): 66-76. |

| Zhang L, Lian Y H. How does bond investment affect the systemic risk of commercial banks?——From the perspective of systemic risk decomposition[J]. Studies of International Finance, 2020(2): 66-76. | |

| [11] | 翟永会. 系统性风险管理视角下实体行业与银行业间风险溢出效应研究[J]. 国际金融研究, 2019(12): 74-84. |

| Zhai Y H. Research on the risk spillover effect between entity industry and banking industry from the perspective of systemic risk management[J]. Studies of International Finance, 2019(12): 74-84. | |

| [12] | De Jonghe O, Diepstraten M, Schepens G. Banks’ size, scope and systemic risk: What role for conflicts of interest?[J]. Journal of Banking & Finance, 2015, 61: S3-S13. |

| [13] | 朱波, 杨文华, 邓叶峰. 非利息收入降低了银行的系统性风险吗?——基于规模异质的视角[J]. 国际金融研究, 2016(4): 62-73. |

| Zhu B, Yang W H, Deng Y F. Does the non-interest income of China’s listed banks reduce the systemic risk?——An analysis from the perspective of size heterogeneity[J]. Studies of International Finance, 2016(4): 62-73. | |

| [14] | 马传慧, 方军雄. 贷款跨行业多元化是否降低了银行系统性风险?——基于中国上市银行的证据[J]. 会计研究, 2024(5): 143-155. |

| Ma C H, Fang J X. Does cross-industry loan diversification reduce bank systemic risk? evidence from listed banks in China[J]. Accounting Research, 2024(5): 143-155. | |

| [15] | Glasserman P, Young H P. How likely is contagion in financial networks?[J]. Journal of Banking & Finance, 2015, 50: 383-399. |

| [16] | 黄玮强, 范铭杰, 庄新田. 基于借贷关联网络的我国银行间市场风险传染[J]. 系统管理学报, 2019, 28(5): 899-906. |

| Huang W Q, Fan M J, Zhuang X T. Risk contagion in China’s interbank based on interbank lending network[J]. Journal of Systems & Management, 2019, 28(5): 899-906. | |

| [17] | 姚鸿, 王超, 何建敏, 等. 银行投资组合多元化与系统性风险的关系研究[J]. 中国管理科学, 2019, 27(2): 9-18. |

| Yao H, Wang C, He J M, et al. Study on the relationship between investment portfolios diversification and systemic risk[J]. Chinese Journal of Management Science, 2019, 27(2): 9-18. | |

| [18] | Šeho M, Bacha O I, Smolo E. Bank financing diversification, market structure, and stability in a dual-banking system[J]. Pacific-Basin Finance Journal, 2024, 86: 102461. |

| [19] | Shabir M, Jiang P, Shahab Y, et al. Diversification and bank stability: Role of political instability and climate risk[J]. International Review of Economics & Finance, 2024, 89: 63-92. |

| [20] | 李政, 朱明皓, 范颖岚. 我国金融机构的传染性风险与系统性风险贡献——基于极端风险网络视角的研究[J]. 南开经济研究, 2019(6): 132-157. |

| Li Z, Zhu M H, Fan Y L. The contagious risk and systemic risk contribution of Chinese financial institutions: A study based on the perspective of extreme risk network[J].Nankai Economic Studies,2019(6): 132-157. | |

| [21] | Acharya V V, Pedersen L H, Philippon T, et al. Measuring systemic risk[J]. The Review of Financial Studies, 2017, 30(1): 2-47. |

| [22] | Brownlees C, Engle R F. SRISK: A conditional capital shortfall measure of systemic risk[J]. The Review of Financial Studies, 2017, 30(1): 48-79. |

| [23] | 陈湘鹏, 周皓, 金涛, 等. 微观层面系统性金融风险指标的比较与适用性分析——基于中国金融系统的研究[J]. 金融研究, 2019(5): 17-36. |

| Chen X P, Zhou H, Jin T, et al. Comparison and applicability analysis of micro-level systemic risk measures: A study based on China’s financial system[J]. Journal of Financial Research, 2019(5): 17-36. | |

| [24] | 杨子晖, 陈里璇, 陈雨恬. 经济政策不确定性与系统性金融风险的跨市场传染——基于非线性网络关联的研究[J]. 经济研究, 2020, 55(1): 65-81. |

| Yang Z H, Chen L X, Chen Y T. Cross-market contagion of economic policy uncertainty and systemic financial risk: A nonlinear network connectedness analysis[J].Economic Research Journal, 2020,55(1): 65-81. | |

| [25] | 欧阳资生, 周学伟. 中国金融机构系统性风险回测与关联研究——基于MES和ΔCoVaR的实证分析[J]. 中国管理科学, 2025, 33(6): 14-26. |

| Ouyang Z S, Zhou X W. Systemic risk backtesting and connectedness of Chinese financial institutions: Evidence from MES and ΔCoVaR[J]. Chinese Journal of Management Science, 2025, 33(6): 14-26. | |

| [26] | 章秀, 周尧婷, 李岳山. 中国系统重要性银行的关联网络与风险贡献研究——基于极端事件冲击视角[J]. 中央财经大学学报, 2025(4): 24-40. |

| Zhang X, Zhou Y T, Li Y S. Research on the network connectivity and risk contributions of China’s systemically important banks: A perspective of extreme event shocks[J]. Journal of Central University of Finance & Economics, 2025(4): 24-40. | |

| [27] | Tasca P, Battiston S, Deghi A. Portfolio diversification and systemic risk in interbank networks[J]. Journal of Economic Dynamics and Control,2017,82: 96-124. |

| [28] | Roukny T, Battiston S, Stiglitz J E. Interconnectedness as a source of uncertainty in systemic risk[J]. Journal of Financial Stability, 2018, 35: 93-106. |

| [29] | 方意, 刘江龙. 银行关联性与系统性金融风险: 传染还是分担?[J]. 金融研究, 2023(6): 57-74. |

| Fang Y, Liu J L. Bank interconnectedness and systemic risk: Contagion or sharing?[J]. Journal of Financial Research, 2023(6): 57-74. | |

| [30] | 黄岩渠, 何阳, 喻采平. 资产异质视角下我国的系统性金融风险研究[J].中国软科学,2024(4): 176-188. |

| Huang Y Q, He Y, Yu C P. Research on systemic financial risk in China from the perspective of asset heterogeneity[J].China Soft Science,2024(4): 176-188. | |

| [31] | 隋聪, 王宪峰, 王宗尧. 银行间债务网络流动性差异对风险传染的影响[J]. 管理科学学报, 2020, 23(3): 65-72. |

| Sui C, Wang X F, Wang Z Y. The impacts of interbank debt network liquidity differences on risk contagion[J]. Journal of Management Sciences in China, 2020, 23(3): 65-72. | |

| [32] | 王辉, 朱家雲, 陈旭. 银行间市场网络稳定性与系统性金融风险最优应对策略: 政府控股视角[J]. 经济研究, 2021, 56(11): 100-118. |

| Wang H, Zhu J Y, Chen X. Interbank network stability and optimal strategies to deal with systemic financial risk: Based on the perspective of government shareholding[J]. Economic Research Journal, 2021, 56(11): 100-118. | |

| [33] | Eboli M. A flow network analysis of direct balance-sheet contagion in financial networks[J]. Journal of Economic Dynamics and Control, 2019, 103: 205-233. |

| [34] | 范小云, 荣宇浩, 王博. 我国系统重要性银行评估: 网络层次结构视角[J]. 管理科学学报, 2021, 24(2): 48-74. |

| Fan X Y, Rong Y H, Wang B. Identifying systemically important banks in China: A network hierarchy structure perspective[J]. Journal of Management Sciences in China, 2021, 24(2): 48-74. | |

| [35] | 沈虹, 张晨曜, 刘晓星. 基于多层网络结构的行业间风险联动机制研究[J].中国管理科学, 2024, 32(12): 173-182. |

| Shen H, Zhang C Y, Liu X X. Analysis of risk spillover characteristics and mechanism among industries: Evidence from multilayer network[J]. Chinese Journal of Management Science, 2024, 32(12): 173-182. | |

| [36] | 徐国祥, 吴婷, 王莹. 基于共同冲击和异质风险叠加传导的风险传染研究——来自中国上市银行网络的传染模拟[J]. 金融研究, 2021(4): 38-54. |

| Xu G X, Wu T, Wang Y. A study of risk contagion based on the interaction between common shocks and idiosyncratic risks: Evidence from the simulation of listed banks in China[J]. Journal of Financial Research, 2021(4): 38-54. | |

| [37] | Bardoscia M, Barucca P, Codd A B, et al. Forward-looking solvency contagion[J]. Journal of Economic Dynamics and Control, 2019, 108: 103755. |

| [38] | Peltonen T A, Rancan M, Sarlin P. Interconnectedness of the banking sector as a vulnerability to crises[J]. International Journal of Finance & Economics, 2019, 24(2): 963-990. |

| [39] | De Lisa R, Zedda S, Vallascas F, et al. Modelling deposit insurance scheme losses in a Basel 2 framework[J]. Journal of Financial Services Research, 2011, 40(3): 123-141. |

| [40] | Benczur P, Cannas G, Cariboni J, et al. Evaluating the effectiveness of the new EU bank regulatory framework: A farewell to bail-out?[J]. Journal of Financial Stability, 2017, 33: 207-223. |

| [41] | 杨子晖, 李东承. 我国银行系统性金融风险研究——基于“去一法”的应用分析[J].经济研究,2018, 53(8): 36-51. |

| Yang Z H, Li D C. An investigation of the systemic risk of Chinese banks: An application based on leave-one-out[J]. Economic Research Journal, 2018, 53(8): 36-51. | |

| [42] | 宋清华, 宋一程, 刘金玉, 等. 多元化能降低银行风险吗?——来自中国上市银行的经验证据[J]. 财经理论与实践, 2016, 37(5): 9-15. |

| Song Q H, Song Y C, Liu J Y, et al. Can diversification reduce the risk of banks? -empirical evidence from listed banks in China[J]. The Theory and Practice of Finance and Economics, 2016, 37(5): 9-15. | |

| [43] | Sironi A, Zazzara C. Applying credit risk models to deposit insurance pricing: Empirical evidence from the Italian banking system[J]. Journal of International Banking Regulations, 2004, 6(1): 10-32. |

| [44] | Zedda S, Cannas G. Analysis of banks’ systemic risk contribution and contagion determinants through the leave-one-out approach[J]. Journal of Banking & Finance, 2020, 112: 105160. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||