主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2026, Vol. 34 ›› Issue (8): 12-27.doi: 10.16381/j.cnki.issn1003-207x.2024.2113

Previous Articles Next Articles

Haixiang Yao1,2, Feiting He1, Xiaoguang Yang3,4( )

)

Received:2024-11-23

Revised:2025-11-18

Online:2026-08-25

Published:2026-07-14

Contact:

Xiaoguang Yang

E-mail:xgyang@iss.ac.cn

CLC Number:

Haixiang Yao,Feiting He,Xiaoguang Yang. Research on the Risk Contagion Effect of Global Foreign Exchange Rate Markets under Extreme Event Shocks[J]. Chinese Journal of Management Science, 2026, 34(8): 12-27.

"

| 货币名称 | 简称(货币代码) | 货币名称 | 简称(货币) |

|---|---|---|---|

| 丹麦克朗 | DKK | 英镑 | GBP |

| 挪威克朗 | NOK | 人民币 | CNY |

| 波兰兹罗提 | PLN | 印度卢比 | INR |

| 新加坡元 | SGD | 墨西哥比索 | MXN |

| 瑞典克朗 | SEK | 巴西雷亚尔 | BRL |

| 瑞士法朗 | CHF | 韩元 | KRW |

| 新西兰元 | NZD | 土耳其里拉 | TRY |

| 泰铢 | THB | 南非兰特 | ZAR |

| 马来西亚林吉特 | MYR | 美元 | USD |

| 港币 | HKD | 澳大利亚元 | AUD |

| 俄罗斯卢布 | RUB | 日元 | JPY |

| 印尼卢比 | IDR | 沙特里亚尔 | SAR |

| 欧元 | EUR | 阿根廷比索 | ARS |

| 加拿大元 | CAD |

"

| edge | copula | edge | copula | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Panel A.平稳期 | Panel B.次贷危机时期 | ||||||||||||

| AUD,NZD | G | 1.40 | - | 0.29 | 0.36 | - | EUR,INR | F | -2.63 | - | -0.27 | - | - |

| DKK,GBP | N | -0.32 | - | -0.21 | - | - | EUR,DKK | t | 0.96 | 3.47 | 0.81 | 0.76 | 0.76 |

| NOK,SEK | t | 0.22 | 14.79 | 0.14 | 0.01 | 0.01 | HKD,RUB | G | 1.43 | - | 0.30 | 0.37 | - |

| THB,MYR | t | 0.31 | 8.16 | 0.20 | 0.06 | 0.06 | HKD,KRW | t | 1.00 | 30.00 | 0.99 | 0.97 | 0.97 |

| JPY,IDR | t | -0.34 | 11.88 | -0.22 | 0 | 0 | NZD,SGD | t | 0.47 | 6.60 | 0.31 | 0.14 | 0.14 |

| EUR,INR | t | -0.44 | 12.65 | -0.29 | 0 | 0 | AUD,NZD | t | 0.75 | 8.59 | 0.54 | 0.27 | 0.27 |

| THB,JPY | N | -0.36 | - | -0.24 | - | - | SAR,EUR | t | -0.79 | 3.85 | -0.58 | 0 | 0 |

| SAR,THB | t | 0.43 | 7.43 | 0.29 | 0.10 | 0.10 | SAR,HKD | t | 0.94 | 3.55 | 0.77 | 0.72 | 0.72 |

| HKD,KRW | t | 1.00 | 7.99 | 0.96 | 0.93 | 0.93 | JPY,GBP | t | -0.23 | 6.32 | -0.15 | 0.01 | 0.01 |

| HKD,SGD | t | -0.42 | 6.63 | -0.28 | 0 | 0 | JPY,IDR | t | -0.51 | 6.17 | -0.34 | 0 | 0 |

| EUR,CHF | F | 3.42 | - | 0.34 | - | - | JPY,CHF | t | 0.64 | 3.99 | 0.44 | 0.34 | 0.34 |

| SAR,HKD | t | 0.97 | 2.48 | 0.83 | 0.82 | 0.82 | THB,MYR | N | 0.37 | - | 0.24 | - | - |

| DKK,RUB | t | -0.42 | 17.33 | -0.28 | 0 | 0 | USD,PLN | G270 | -1.53 | - | -0.35 | - | - |

| EUR,DKK | t | 0.97 | 3.79 | 0.84 | 0.79 | 0.79 | CNY,THB | t | 0.61 | 5.97 | 0.41 | 0.23 | 0.23 |

| USD,PLN | t | -0.43 | 19.40 | -0.28 | 0 | 0 | SAR,CNY | t | 0.84 | 3.36 | 0.63 | 0.56 | 0.56 |

| CAD,NOK | t | 0.37 | 17.11 | 0.24 | 0.01 | 0.01 | TRY,JPY | t | -0.63 | 8.76 | -0.43 | 0 | 0 |

| CAD,AUD | t | 0.48 | 14.04 | 0.32 | 0.04 | 0.04 | BRL,MXN | t | 0.60 | 16.46 | 0.41 | 0.05 | 0.05 |

| ZAR,TRY | F | 3.56 | - | 0.35 | - | - | ZAR,TRY | t | 0.68 | 10.22 | 0.48 | 0.17 | 0.17 |

| MXN,ZAR | t | 0.56 | 7.09 | 0.38 | 0.17 | 0.17 | BRL,ZAR | t | 0.59 | 13.99 | 0.40 | 0.07 | 0.07 |

| ARS,BRL | F | -5.47 | - | -0.48 | - | - | USD,NOK | t | -0.50 | 8.51 | -0.34 | 0 | 0 |

| USD,ARS | F | 4.43 | - | 0.42 | - | - | USD,SEK | F | -3.29 | - | -0.33 | - | - |

| USD,CAD | t | -0.60 | 23.37 | -0.41 | 0 | 0 | USD,CAD | t | -0.64 | 6.19 | -0.45 | 0 | 0 |

| USD,MXN | t | -0.57 | 11.33 | -0.39 | 0 | 0 | USD,SAR | t | 0.90 | 5.12 | 0.71 | 0.59 | 0.59 |

| SAR,EUR | t | -0.57 | 8.26 | -0.39 | 0 | 0 | ARS,BRL | t | -0.72 | 13.46 | -0.51 | 0 | 0 |

| SAR,CNY | t | 0.72 | 2.10 | 0.51 | 0.52 | 0.52 | ARS,USD | t | 0.62 | 5.00 | 0.42 | 0.28 | 0.28 |

| SAR,USD | t | 0.91 | 3.40 | 0.73 | 0.67 | 0.67 | ARS,AUD | t | -0.61 | 7.10 | -0.41 | 0 | 0 |

| Panel C.新冠疫情时期 | Panel D.俄乌冲突时期 | ||||||||||||

| JPY,THB | t | -0.27 | 6.22 | -0.17 | 0.01 | 0.01 | USD,SEK | N | -0.53 | - | -0.36 | - | - |

| JPY,IDR | t | -0.36 | 5.99 | -0.24 | 0.01 | 0.01 | JPY,CHF | SC | 0.33 | - | 0.14 | 0.12 | - |

| JPY,CHF | F | 3.81 | - | 0.37 | - | - | CNY,JPY | t | -0.35 | 8.92 | -0.22 | 0 | 0 |

| DKK,RUB | t | -0.61 | 2.00 | -0.42 | 0.04 | 0.04 | EUR,CNY | G270 | -1.41 | -0.29 | - | - | |

| EUR,DKK | t | 0.96 | 20.25 | 0.82 | 0.52 | 0.52 | EUR,DKK | t | 0.92 | 10.03 | 0.74 | 0.51 | 0.51 |

| AUD,NOK | t | 0.80 | 3.98 | 0.59 | 0.49 | 0.49 | USD,PLN | t | -0.49 | 10.50 | -0.32 | 0 | 0 |

| AUD,CAD | t | 0.84 | 4.62 | 0.63 | 0.51 | 0.51 | AUD,SGD | N | 0.40 | - | 0.27 | - | - |

| NZD,GBP | t | 0.41 | 8.00 | 0.27 | 0.08 | 0.08 | NZD,GBP | F | 2.85 | - | 0.29 | - | - |

| SAR,MYR | t | 0.77 | 2.00 | 0.56 | 0.58 | 0.58 | AUD,NZD | N | 0.71 | - | 0.50 | - | - |

| CNY,JPY | t | -0.44 | 5.43 | -0.29 | 0.01 | 0.01 | TRY,EUR | t | -0.62 | 7.64 | -0.43 | 0 | 0 |

| SAR,PLN | t | -0.66 | 12.23 | -0.46 | 0 | 0 | USD,TRY | t | 0.74 | 3.25 | 0.53 | 0.47 | 0.47 |

| EUR,CNY | t | -0.65 | 2.99 | -0.45 | 0.01 | 0.01 | USD,INR | t | 0.55 | 4.74 | 0.37 | 0.24 | 0.24 |

| EUR,TRY | N | -0.70 | - | -0.50 | - | - | CAD,NOK | t | 0.58 | 14.11 | 0.39 | 0.06 | 0.06 |

| HKD,KRW | N | 1.00 | - | 0.97 | - | - | AUD,CAD | t | 0.70 | 11.80 | 0.49 | 0.15 | 0.15 |

| SAR,HKD | F | 27.78 | - | 0.86 | - | - | USD,MXN | G270 | -1.33 | - | -0.25 | - | - |

| EUR,INR | N | -0.69 | - | -0.48 | - | - | USD,AUD | t | -0.59 | 7.38 | -0.40 | 0 | 0 |

| SAR,EUR | t | -0.64 | 2.38 | -0.44 | 0.02 | 0.02 | SAR,THB | N | -0.29 | -0.19 | - | - | |

| USD,SAR | t | 0.99 | 3.57 | 0.89 | 0.86 | 0.86 | HKD,KRW | t | 1.00 | 26.13 | 0.95 | 0.85 | 0.85 |

| MXN,ZAR | t | 0.92 | 6.96 | 0.75 | 0.59 | 0.59 | SAR,HKD | t | 0.97 | 4.46 | 0.85 | 0.80 | 0.80 |

| ARS,BRL | t | -0.89 | 3.62 | -0.70 | 0 | 0 | SAR,MYR | t | 0.51 | 2.24 | 0.34 | 0.38 | 0.38 |

| USD,ARS | F | 9.63 | - | 0.66 | - | - | SAR,RUB | F | 2.34 | - | 0.25 | - | - |

| USD,MXN | t | -0.91 | 3.27 | -0.73 | 0 | 0 | SAR,IDR | SG | 1.23 | - | 0.19 | - | 0.25 |

| USD,SEK | N | -0.63 | - | -0.43 | - | - | USD,ZAR | t | -0.47 | 10.50 | -0.31 | 0 | 0 |

| AUD,NZD | F | 7.46 | - | 0.58 | - | - | USD,SAR | t | 0.96 | 3.73 | 0.83 | 0.78 | 0.78 |

| AUD,SGD | t | 0.75 | 3.42 | 0.54 | 0.47 | 0.47 | ARS,BRL | t | -0.65 | 5.59 | -0.45 | 0 | 0 |

| AUD,USD | t | -0.83 | 4.76 | -0.63 | 0 | 0 | ARS,USD | G | 2.14 | - | 0.53 | 0.62 | - |

"

"

"

"

"

"

"

"

"

| 平稳期 | 次贷危机时期 | 疫情时期 | 俄乌冲突时期 | ||||

|---|---|---|---|---|---|---|---|

| 币种 | 净溢出 | 币种 | 净溢出 | 币种 | 净溢出 | 币种 | 净溢出 |

| USD | 50.9 | SAR | 50.8 | USD | 10.3 | USD | 90.4 |

| HKD | 43.0 | USD | 50.6 | CAD | 9.6 | SAR | 83.7 |

| SAR | 34.1 | CNY | 47.3 | INR | 9.3 | HKD | 74.8 |

| EUR | 23.1 | DKK | 46.8 | ARS | 9.2 | RUB | 42.4 |

| DKK | 15.5 | HKD | 44.6 | SAR | 9.0 | EUR | 18.2 |

| JPY | 15.3 | JPY | 37.2 | SGD | 8.9 | ARS | 15.2 |

| RUB | 6.2 | BRL | 35.4 | BRL | 8.9 | CHF | 10.5 |

| ARS | 3.4 | AUD | 30.2 | CHF | 8.6 | PLN | -3.8 |

| NOK | 2.2 | EUR | 25.0 | IDR | 8.6 | MXN | -4.9 |

| CHF | 2.1 | MXN | 15.4 | NOK | 8.0 | TRY | -5.1 |

| GBP | -2.9 | CHF | 14.8 | HKD | 7.8 | ZAR | -5.2 |

| SGD | -3.5 | TRY | 13.3 | CNY | 7.4 | AUD | -6.3 |

| CNY | -5.2 | ARS | 0.1 | MXN | 7.3 | JPY | -8.9 |

| IDR | -5.5 | THB | -3.2 | AUD | 7.3 | IDR | -11.1 |

| THB | -6.2 | NZD | -11.1 | MYR | 7.0 | SGD | -11.6 |

| BRL | -6.5 | ZAR | -15.5 | KRW | 6.3 | CNY | -11.7 |

| AUD | -6.6 | RUB | -15.6 | DKK | 4.8 | CAD | -12.0 |

| INR | -6.9 | INR | -18.1 | TRY | 3.9 | GBP | -12.5 |

| TRY | -8.1 | KRW | -23.2 | EUR | 2.1 | THB | -13.7 |

| ZAR | -9.8 | MYR | -26.1 | THB | -0.2 | DKK | -16.0 |

| PLN | -10.9 | IDR | -28.4 | ZAR | -0.2 | NZD | -16.3 |

| SEK | -11.2 | NOK | -38.8 | RUB | -2.9 | NOK | -19.5 |

| MXN | -11.8 | PLN | -41.5 | SEK | -14.2 | KRW | -21.2 |

| CAD | -21.6 | CAD | -43.4 | PLN | -15.4 | MYR | -24.5 |

| KRW | -23.4 | SEK | -46.7 | JPY | -16.6 | INR | -38.3 |

| NZD | -26.8 | GBP | -49.7 | NZD | -28.6 | BRL | -44.6 |

| MYR | -28.7 | SGD | -50.3 | GBP | -66.2 | SEK | -48.1 |

"

| Panel A.平稳期 | Panel B.次贷危机时期 | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

IFO- mean | OTO- mean | IFO- mean | OTO- mean | ||||||||||||||

| a | 亚洲 | 欧洲 | 大洋洲 | 北美洲 | 南美洲 | 非洲 | a | 亚洲 | 欧洲 | 大洋洲 | 北美洲 | 南美洲 | 非洲 | ||||

| b | b | ||||||||||||||||

| 亚洲 | 7.348 | 1.348 | 1.060 | 3.337 | 0.620 | 0.960 | 1.556 | 1.635 | 亚洲 | 6.266 | 2.289 | 2.290 | 2.653 | 1.650 | 0.850 | 2.194 | 2.378 |

| 欧洲 | 1.377 | 8.954 | 0.622 | 1.119 | 0.200 | 0.567 | 1.074 | 1.174 | 欧洲 | 2.758 | 5.867 | 1.933 | 2.811 | 2.111 | 3.189 | 2.627 | 2.052 |

| 大洋洲 | 1.815 | 1.322 | 28.300 | 3.617 | 0.550 | 1.350 | 1.734 | 1.056 | 大洋洲 | 1.855 | 1.522 | 18.375 | 3.550 | 8.650 | 3.000 | 2.528 | 2.914 |

| 北美洲 | 3.130 | 1.185 | 2.600 | 16.367 | 0.767 | 2.167 | 2.119 | 2.304 | 北美洲 | 2.587 | 1.756 | 4.733 | 11.733 | 6.117 | 1.433 | 2.700 | 3.019 |

| 南美洲 | 0.440 | 0.367 | 0.600 | 1.250 | 42.800 | 1.750 | 0.576 | 0.516 | 南美洲 | 1.335 | 1.456 | 7.125 | 5.117 | 20.175 | 3.550 | 2.384 | 3.092 |

| 非洲 | 1.500 | 0.722 | 1.200 | 2.133 | 1.500 | 62.800 | 1.281 | 1.054 | 非洲 | 1.460 | 2.833 | 4.100 | 3.300 | 6.150 | 29.700 | 2.712 | 2.100 |

| Panel C.疫情时期 | Panel D.俄乌冲突时期 | ||||||||||||||||

IFO- mean | OTO- mean | IFO- mean | OTO- mean | ||||||||||||||

| a | 亚洲 | 欧洲 | 大洋洲 | 北美洲 | 南美洲 | 非洲 | a | 亚洲 | 欧洲 | 大洋洲 | 北美洲 | 南美洲 | 非洲 | ||||

| b | b | ||||||||||||||||

| 亚洲 | 3.995 | 3.212 | 3.135 | 3.967 | 3.960 | 4.980 | 3.528 | 3.762 | 亚洲 | 7.409 | 0.857 | 1.220 | 3.833 | 1.785 | 0.590 | 1.518 | 1.625 |

| 欧洲 | 3.688 | 3.884 | 3.461 | 4.248 | 4.233 | 0.011 | 3.612 | 3.119 | 欧洲 | 1.220 | 7.940 | 2.606 | 2.630 | 1.411 | 0.378 | 1.583 | 1.373 |

| 大洋洲 | 3.730 | 3.528 | 4.675 | 4.367 | 4.300 | 0.000 | 3.630 | 3.034 | 大洋洲 | 1.420 | 3.433 | 17.425 | 4.767 | 2.475 | 0.750 | 2.604 | 2.148 |

| 北美洲 | 3.840 | 3.574 | 3.550 | 4.511 | 4.450 | 0.000 | 3.607 | 3.860 | 北美洲 | 2.400 | 2.070 | 4.567 | 14.144 | 2.683 | 0.500 | 2.401 | 3.421 |

| 南美洲 | 3.395 | 3.106 | 1.350 | 3.000 | 2.325 | 0.000 | 2.944 | 3.986 | 南美洲 | 2.880 | 1.328 | 1.900 | 4.717 | 20.350 | 0.700 | 2.376 | 1.786 |

| 非洲 | 4.990 | 0.033 | 0.000 | 0.000 | 0.000 | 49.800 | 1.931 | 1.919 | 非洲 | 0.840 | 0.411 | 0.550 | 1.133 | 1.100 | 81.100 | 0.723 | 0.527 |

"

| Panel A.平稳期 | Panel B.次贷危机时期 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| IFO-mean | OTO-mean | IFO-mean | OTO-mean | ||||||||

| a | 高度 | 中高 | 中低 | a | 高度 | 中高 | 中低 | ||||

| b | b | ||||||||||

| 高度 | 5.843 | 0.859 | 0.955 | 1.396 | 1.702 | 高度 | 4.754 | 3.548 | 2.281 | 2.574 | 2.499 |

| 中高 | 2.888 | 16.333 | 1.047 | 2.121 | 2.281 | 中高 | 3.002 | 9.767 | 2.873 | 2.949 | 3.288 |

| 中低 | 1.346 | 1.463 | 7.673 | 1.367 | 0.971 | 中低 | 2.349 | 2.923 | 5.835 | 2.450 | 2.386 |

| Panel C.疫情时期 | Panel D.俄乌冲突时期 | ||||||||||

| IFO-mean | OTO-mean | IFO-mean | OTO-mean | ||||||||

| a | 高度 | 中高 | 中低 | a | 高度 | 中高 | 中低 | ||||

| b | b | ||||||||||

| 高度 | 3.915 | 3.940 | 3.336 | 3.476 | 3.190 | 高度 | 5.356 | 2.924 | 1.623 | 1.923 | 2.041 |

| 中高 | 3.764 | 4.356 | 3.433 | 3.626 | 3.638 | 中高 | 2.160 | 18.311 | 1.487 | 1.879 | 2.921 |

| 中低 | 3.018 | 3.213 | 4.807 | 3.052 | 3.354 | 中低 | 2.006 | 2.917 | 6.308 | 2.166 | 1.599 |

"

"

| 平稳期 | 次贷危机时期 | 疫情时期 | 俄乌冲突时期 | |

|---|---|---|---|---|

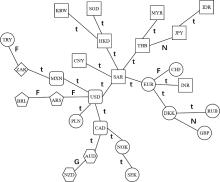

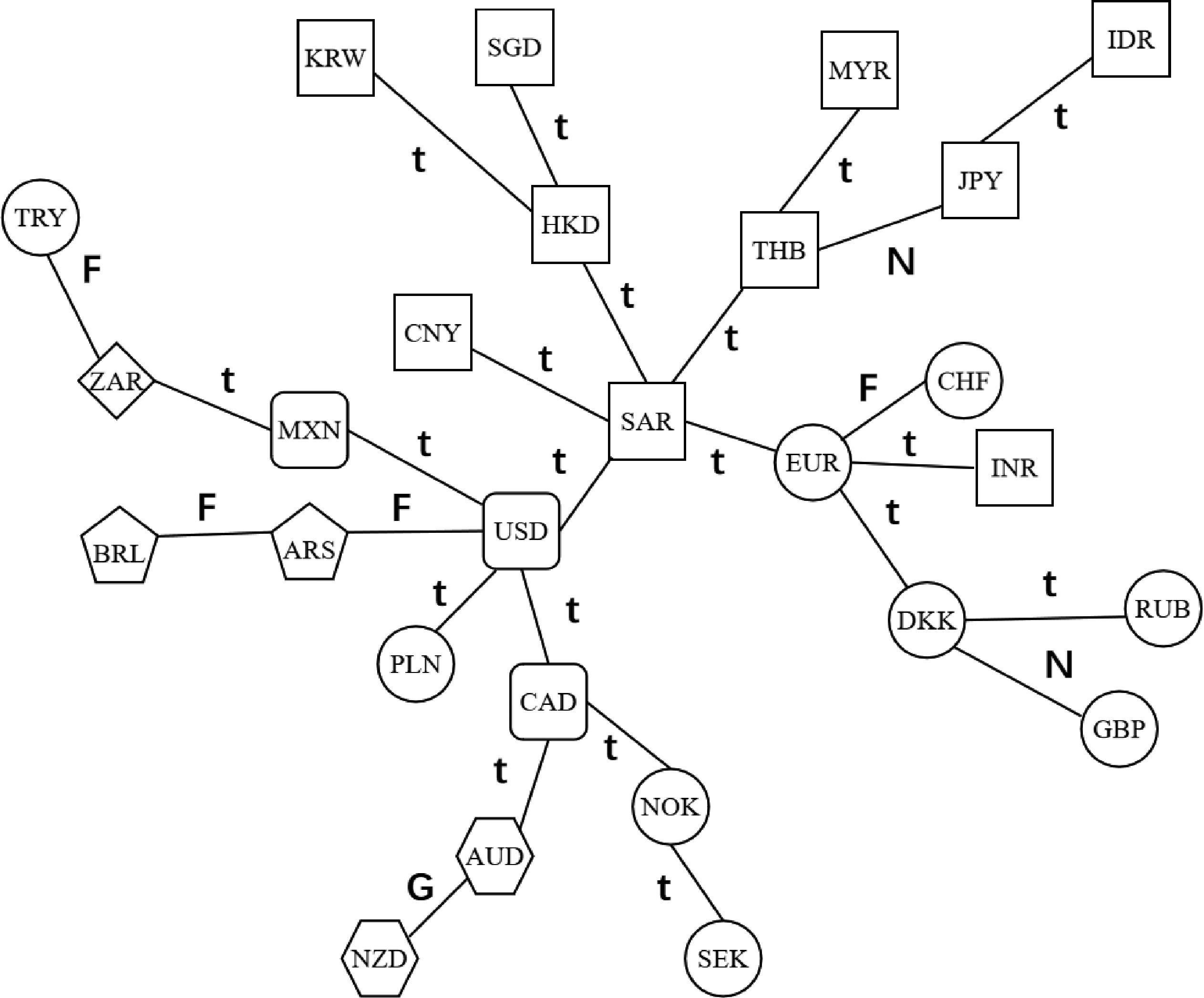

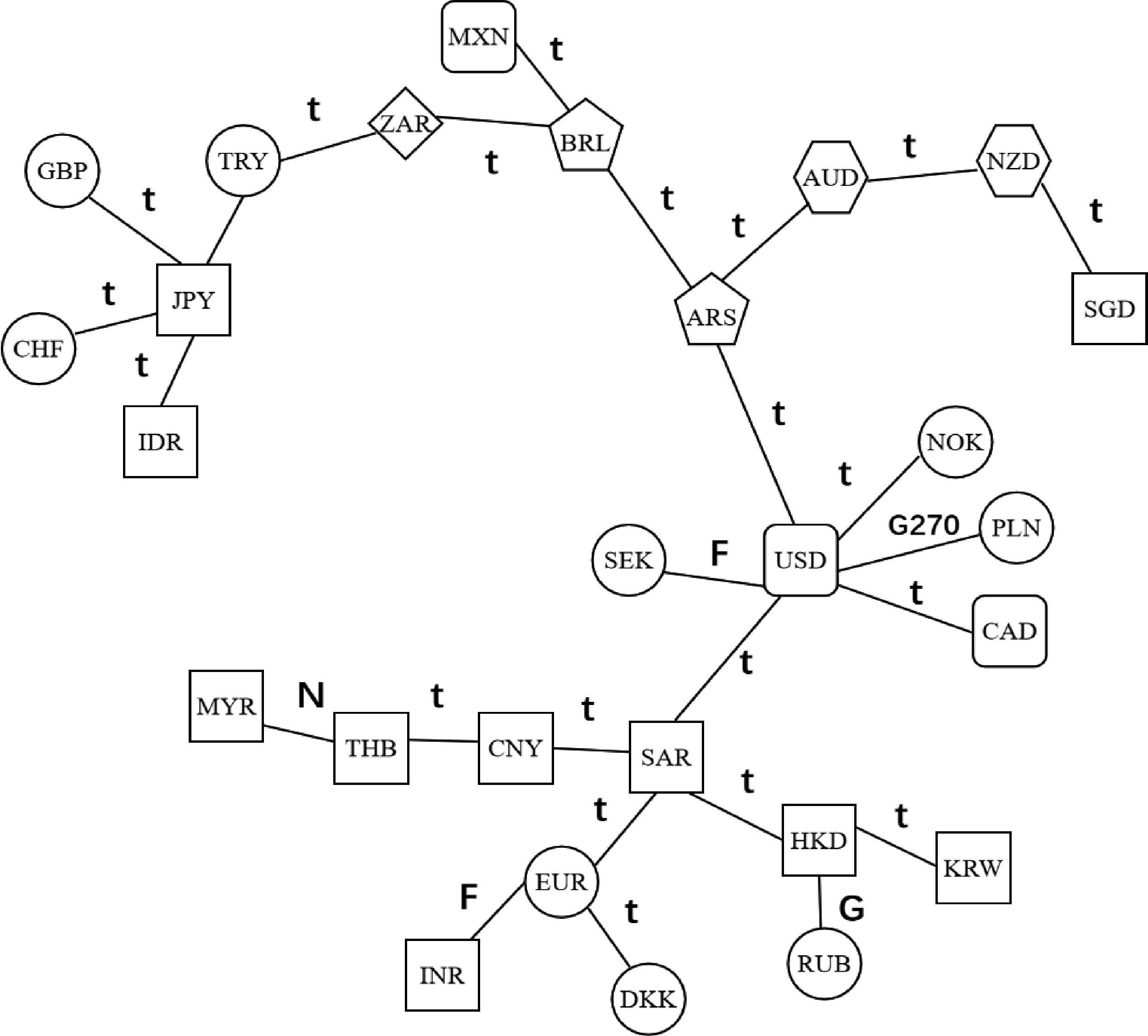

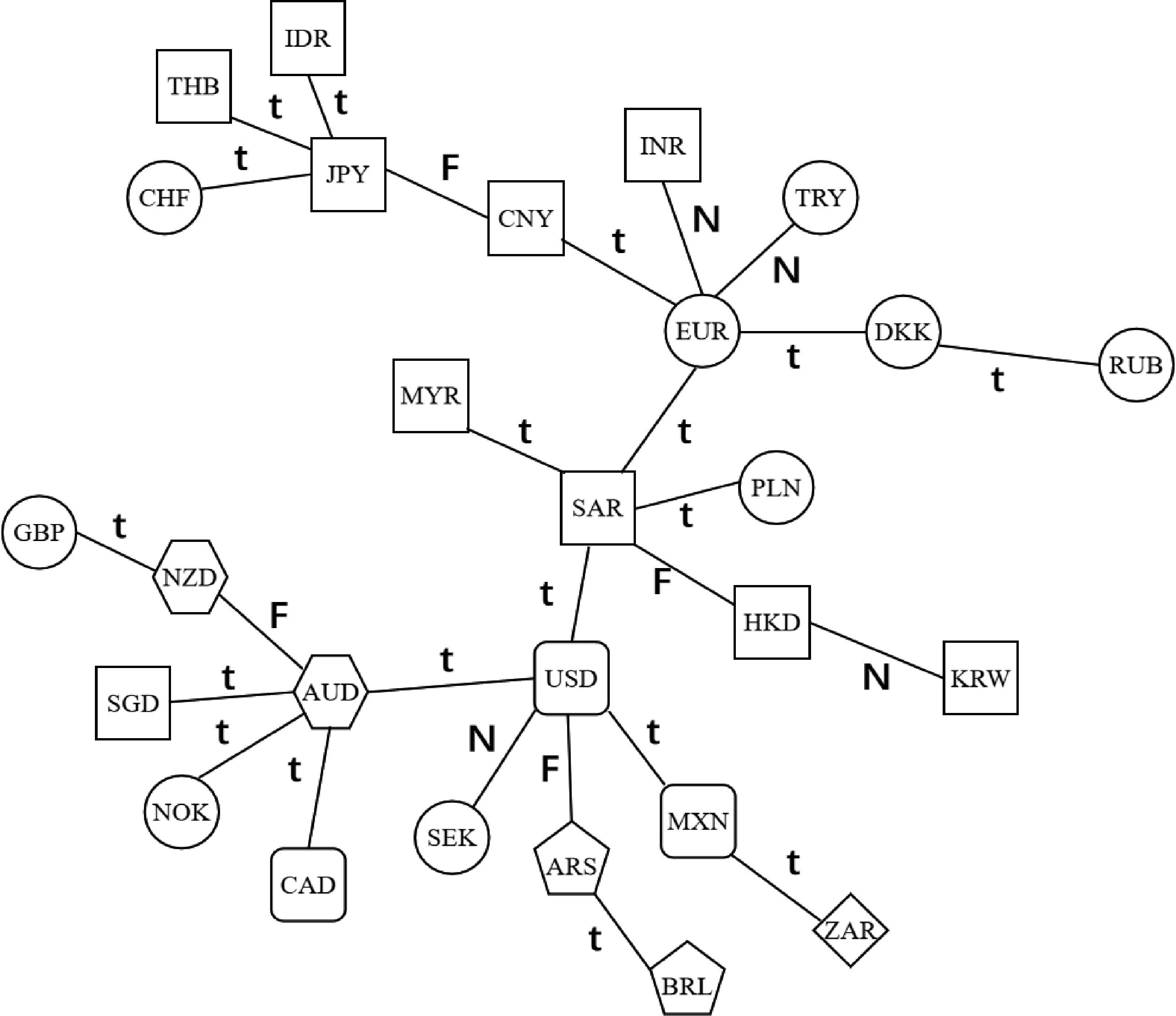

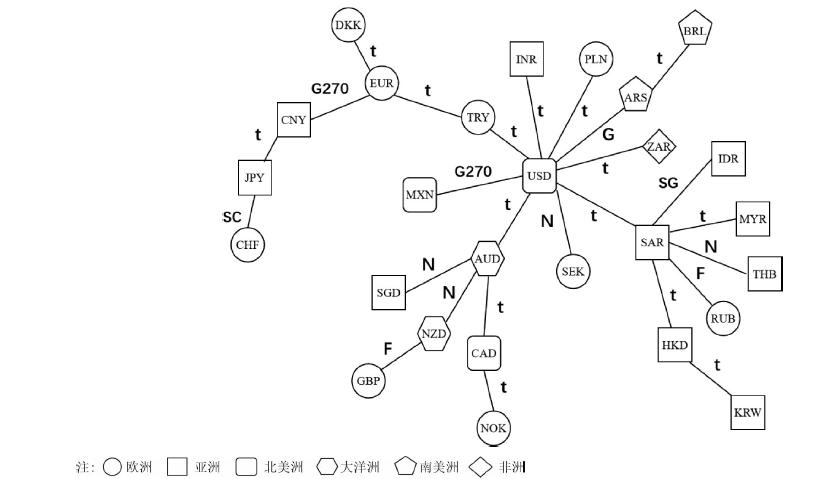

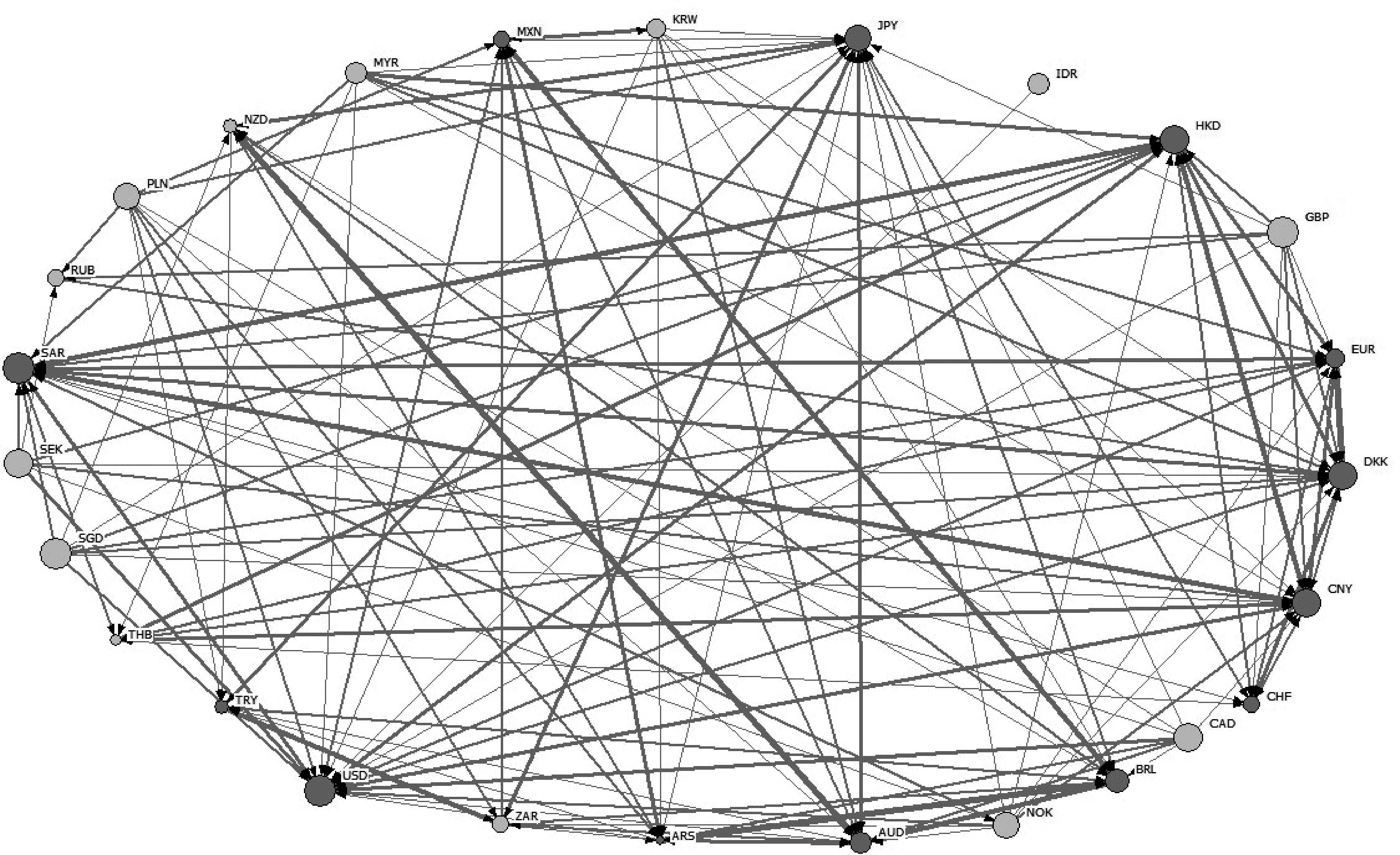

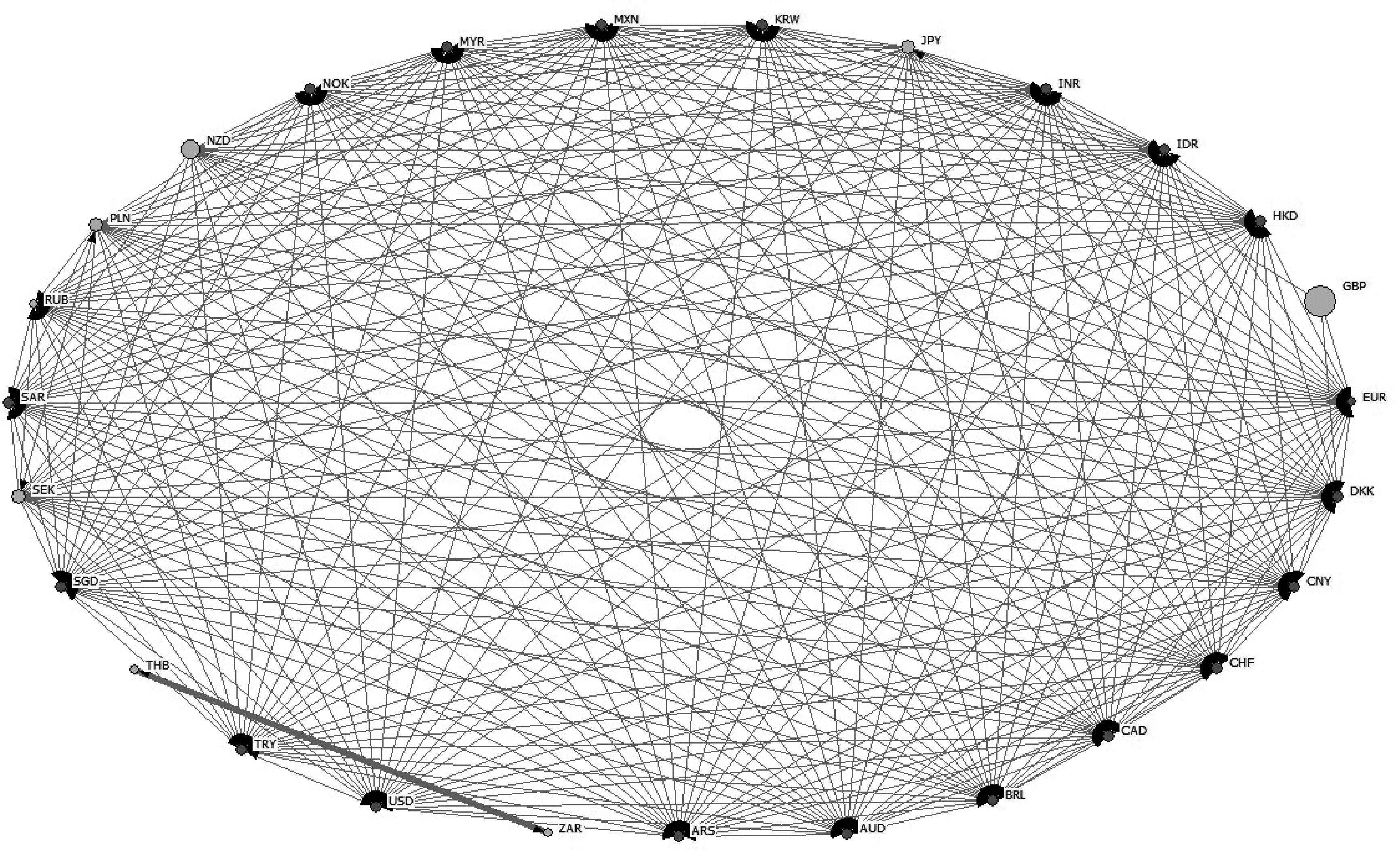

| 联动网络 | (1)美元是全球货币连接的关键节点,沙特里亚尔是美元与欧亚货币之间重要的风险传导枢纽。 (2)风险相依结构大体呈地理区域聚集特征。 | (1)美元是全球货币连接的关键节点,沙特里亚尔是美元与欧亚货币之间重要的风险传导枢纽。 (2)风险相依结构杂乱,产生较多的跨区域风险联动,跨区域联结广泛存在于全球各经济体汇率市场之间。 | (1)美元是全球货币连接的关键节点,沙特里亚尔是美元与欧亚货币之间重要的风险传导枢纽。 (2)风险相依结构杂乱,产生较多的跨区域风险联动,跨区域联结广泛存在于全球各经济体汇率市场之间。 | (1)美元是全球货币连接的关键节点,沙特里亚尔是美元与欧亚货币之间重要的风险传导枢纽。 (2)跨区域风险联动发生在局部,主要体现在以美元为中心节点与部分亚洲货币、欧洲货币、大洋洲货币之间的跨区域联结,而欧洲货币与亚洲货币的联动明显减少。 |

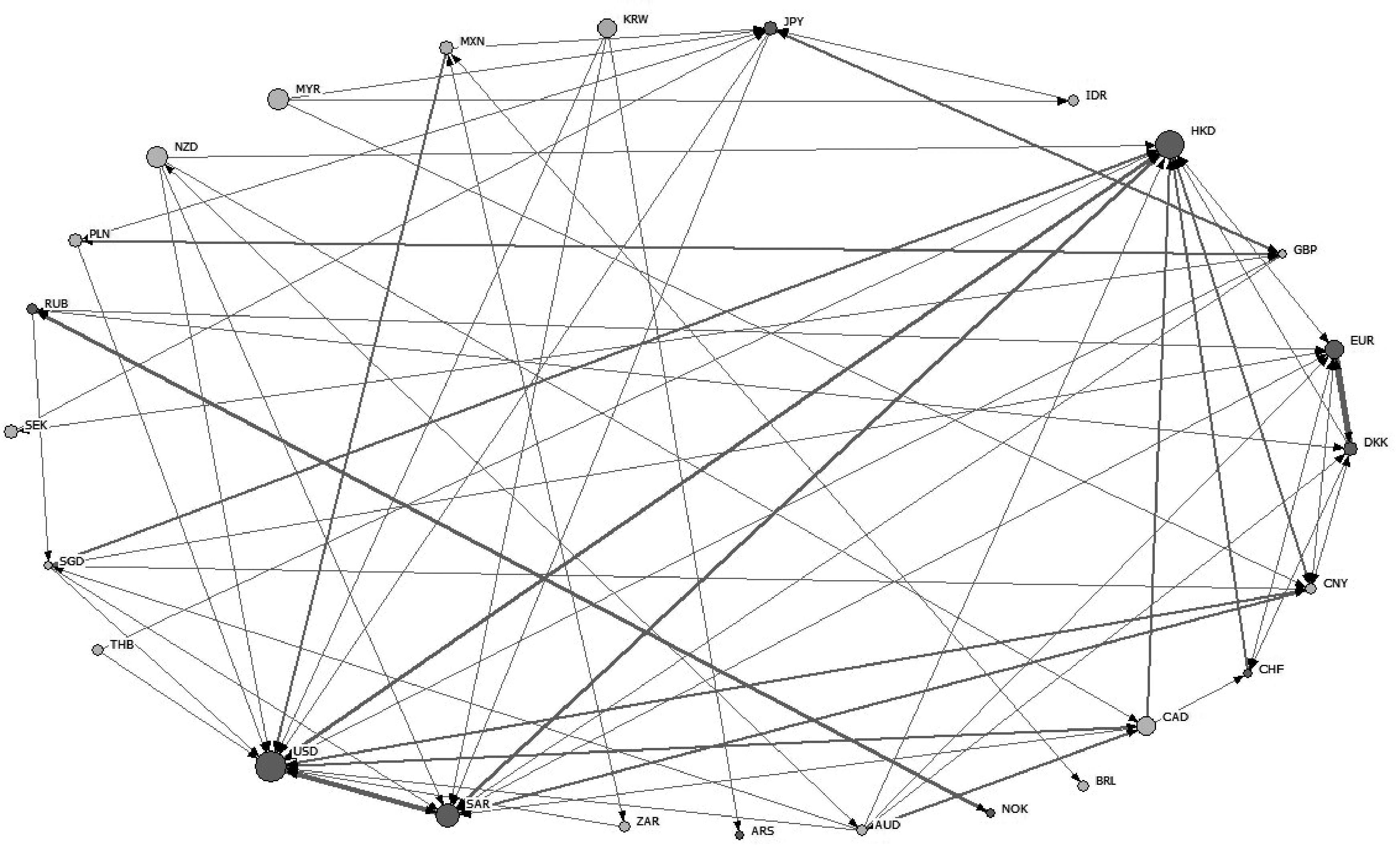

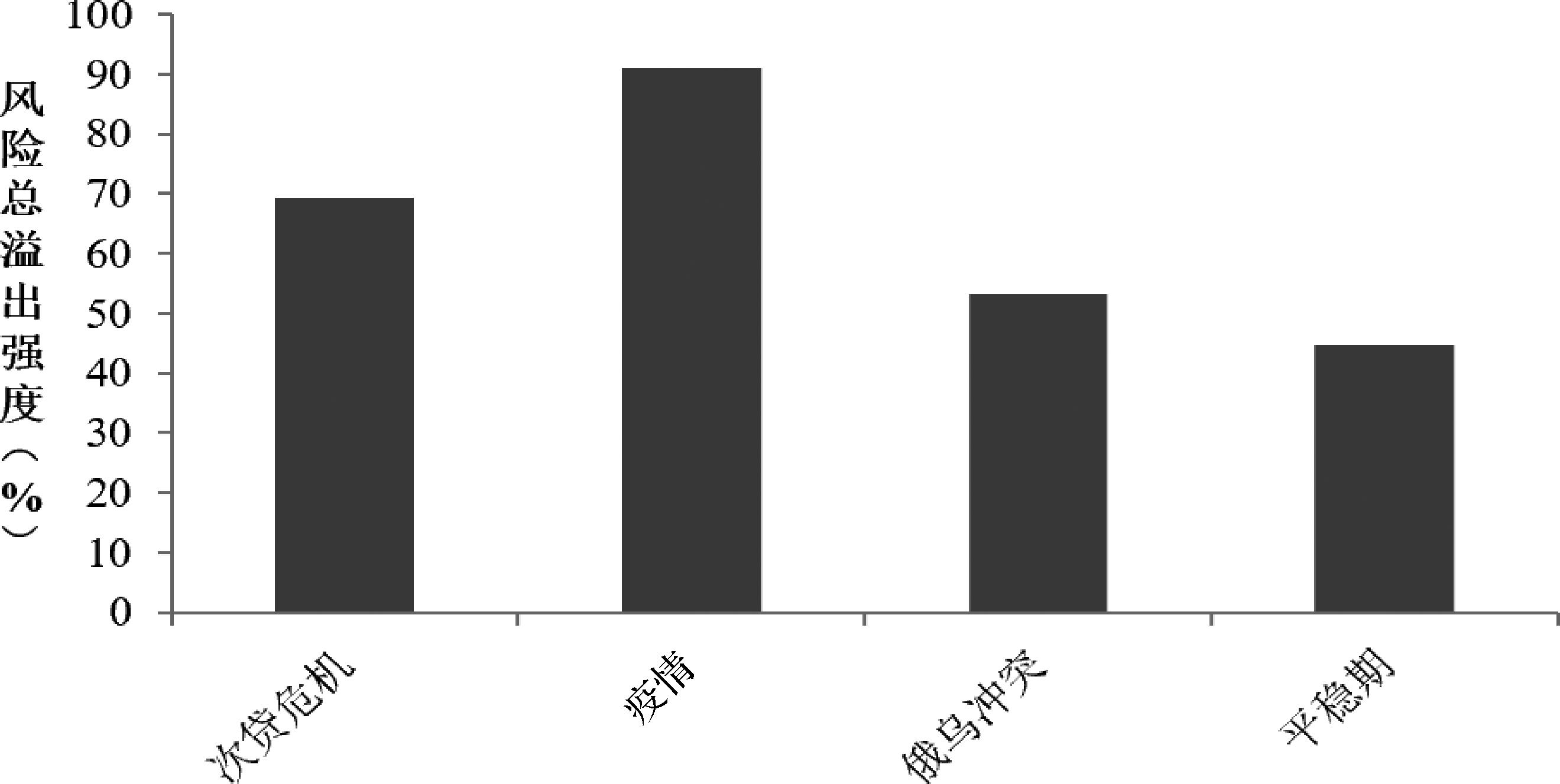

| 溢出网络 | (1)美元与沙特里亚尔是整个汇率网络的风险净输出核心。 (2)较高水平的风险溢出主要集中于同区域的汇率市场内部。 | (1)美元与沙特里亚尔是整个汇率网络的风险净输出核心。 (2)相比于新冠疫情,同区域货币内部的风险溢出与跨区域货币的风险溢出,高强度溢出水平的值较多。 (3)根据网络拓扑分组,相比于平稳期,各组跨地理区域或跨资本开放程度类型的风险溢出强度会增强。 | (1)美元与沙特里亚尔是整个汇率网络的风险净输出核心。 (2)该网络中的溢出关系是四个阶段中最为复杂的,跨区域风险溢出的范围比次贷危机更广泛,并且整个系统内货币之间的风险溢出均达到中高强度水平。同时,该时期整个系统的风险溢出总效应最高,其次是次贷危机时期、俄乌冲突时期、平稳时期。 (3)根据网络拓扑分组,相比于平稳期,各组跨地理区域或跨资本开放程度类型的风险溢出强度会增强,在疫情期间这种现象最为显著,其次为次贷危机,最后为俄乌冲突。 | (1)美元与沙特里亚尔是整个汇率网络的风险净输出核心。 (2)货币的跨区域风险溢出范围有限,主要体现在北美洲与欧洲之间、北美洲与亚洲之间、北美洲与大洋洲之间、北美洲与南美洲之间的货币跨区域风险溢出,其中美元作为最主要的风险驱动因素出现。 (3)根据网络拓扑分组,相比于平稳期,各组跨地理区域或跨资本开放程度类型的风险溢出强度会增大。 |

| [1] | 方意, 贾妍妍, 赵阳. 重大冲击下全球外汇市场风险的生成机理研究[J]. 财贸经济, 2021, 42(5): 76-92. |

| Fang Y, Jia Y Y, Zhao Y. On the risk formulation mechanism in the global foreign exchange market under large shocks[J]. Finance Trade Economics, 2021, 42(5): 76-92. | |

| [2] | 李政, 梁琪, 涂晓枫. 我国上市金融机构关联性研究——基于网络分析法[J]. 金融研究, 2016(8): 95-110. |

| Li Z, Liang Q, Tu X F. The connectedness of Chinese listed financial institutions: A study based on network analysis[J]. Journal of Financial Research, 2016(8): 95-110. | |

| [3] | Chuliá H, Gupta R, Uribe J M, et al. Impact of US uncertainties on emerging and mature markets: Evidence from a quantile-vector autoregressive approach[J]. Journal of International Financial Markets, Institutions and Money, 2017, 48: 178-191. |

| [4] | Dungey M, Flavin T J, Lagoa-Varela D. Are banking shocks contagious? Evidence from the eurozone[J]. Journal of Banking Finance, 2020, 112: 105386. |

| [5] | 梁琪, 李政, 郝项超. 中国股票市场国际化研究: 基于信息溢出的视角[J].经济研究,2015,50(4): 150-164. |

| Liang Q, Li Z, Hao X C. The internationalization of Chinese stock market: Based on information spillover[J]. Economic Research Journal, 2015, 50(4): 150-164. | |

| [6] | 杨子晖, 周颖刚. 全球系统性金融风险溢出与外部冲击[J]. 中国社会科学, 2018(12): 69-90+200+201. |

| Yang Z H, Zhou Y G. Global systemic financial risk spillovers and their external impact[J]. Social Sciences in China, 2018(12): 69-90+200+201. | |

| [7] | Yang Z, Zhou Y. Quantitative easing and volatility spillovers across countries and asset classes[J]. Management Science, 2017, 63(2): 333-354. |

| [8] | Aït-Sahalia Y, Cacho-Diaz J, Laeven R J A. Modeling financial contagion using mutually exciting jump processes[J]. Journal of Financial Economics, 2015, 117(3): 585-606. |

| [9] | Opie W, Riddiough S J. Global currency hedging with common risk factors[J]. Journal of Financial Economics, 2020, 136(3): 780-805. |

| [10] | 梁芹, 陆静. 国际金融危机期间的汇率风险传染效应研究[J]. 当代经济科学, 2013, 35(2): 1-10+124. |

| Liang Q, Lu J. On the contagious effect of exchange rate risk during international financial crisis[J]. Modern Economic Science, 2013, 35(2): 1-10+124. | |

| [11] | 万蕤叶, 陆静. 金融危机期间汇率风险传染研究[J]. 管理科学学报, 2018, 21(6): 12-28. |

| Wan R Y, Lu J. Contagion of exchange rate risk during financial crises[J]. Journal of Management Sciences in China, 2018, 21(6): 12-28. | |

| [12] | 王璐, 黄登仕, 马锋, 等. 重大突发事件对国际外汇市场影响分析: 基于英国脱欧公投事件[J]. 数理统计与管理, 2020, 39(1): 174-190. |

| Wang L, Huang D S, Ma F, et al. The impact of major emergency on international foreign exchange markets: The case of Britain vote to leave the EU in the referendum[J]. Jouranl of Applied Statistics and Management, 2020, 39(1): 174-190. | |

| [13] | 方意, 贾妍妍. 新冠肺炎疫情冲击下全球外汇市场风险传染与中国金融风险防控[J]. 当代经济科学, 2021, 43(2): 1-15. |

| Fang Y, Jia Y Y. Risk contagion in global foreign exchange market under COVID-19 and China’s financial risk prevention[J]. Modern Economic Science, 2021, 43(2): 1-15. | |

| [14] | 王纲金, 马欣宇, 谢赤. 基于尾部风险溢出网络的全球外汇市场关联性研究[J]. 中国管理科学, 2025, 33(3): 13-23. |

| Wang G J, Ma X Y, Xie C. Measuring interconnectedness of global foreign exchange markets using tail risk spillover network[J]. Chinese Journal of Management Science, 2025, 33(3): 13-23. | |

| [15] | 隋建利, 杨庆伟, 宋涛. 汇率网络结构变迁、人民币影响力与汇率波动传导——来自“一带一路”沿线国家的证据[J]. 国际金融研究, 2020(10): 75-85. |

| Sui J L, Yang Q W, Song T. Structural change of exchange rate network, influences of RMB and transmission of exchange rate volatility: Evidence from countries along the Belt and Road[J]. Studies of International Finance, 2020(10): 75-85. | |

| [16] | Wei Z, Luo Y, Huang Z, et al. Spillover effects of RMB exchange rate among BR countries: Before and during COVID-19 event[J]. Finance Research Letters, 2020, 37: 101782. |

| [17] | Song D M, Tumminello M, Zhou W X, et al. Evolution of worldwide stock markets, correlation structure, and correlation-based graphs[J]. Physical Review E, 2011, 84(2): 026108. |

| [18] | 黄飞雪, 谷静, 李延喜, 等. 金融危机前后的全球主要股指联动与动态稳定性比较[J]. 系统工程理论与实践, 2010, 30(10): 1729-1740. |

| Huang F X, Gu J, Li Y X, et al. Linkages and dynamic stability of the national of global primary stock index before and after the financial crisis[J]. Systems Engineering-Theory Practice, 2010, 30(10): 1729-1740. | |

| [19] | Diebold F X, Yılmaz K. On the network topology of variance decompositions: Measuring the connectedness of financial firms[J]. Journal of Econometrics, 2014, 182(1): 119-134. |

| [20] | Jung Y C, Das A, McFarlane A. The asymmetric relationship between the oil price and the US-Canada exchange rate[J]. The Quarterly Review of Economics and Finance, 2020, 76: 198-206. |

| [21] | 宫晓莉, 熊熊, 张维. 我国金融机构系统性风险度量与外溢效应研究[J].管理世界,2020, 36(8): 65-83. |

| Gong X L, Xiong X, Zhang W. Research on systemic risk measurement and spillover effect of financial institutions in China[J].Journal of Management World, 2020, 36(8): 65-83. | |

| [22] | Demirer M, Diebold F X, Liu L, et al. Estimating global bank network connectedness[J]. Journal of Applied Econometrics, 2018, 33(1): 1-15. |

| [23] | Gross C, Siklos P L. Analyzing credit risk transmission to the nonfinancial sector in Europe: A network approach[J]. Journal of Applied Econometrics, 2020, 35(1): 61-81. |

| [24] | 王姝黛, 杨子晖, 张平淼. 城投债信用风险传染的地理集聚、路径演变与驱动机制——基于前沿弹性网络收缩技术的研究[J]. 统计研究, 2023, 40(3): 32-42. |

| Wang S D, Yang Z H, Zhang P M. Geographical agglomeration, path evolution and driving mechanism for credit risk contagion of municipal investment bonds: Analysis based on elastic net shrinkage[J]. Statistical Research, 2023, 40(3): 32-42. | |

| [25] | Joe H. Multivariate Models and Multivariate Dependence Concepts[M]. London:Chapman and Hall/CRC, 1997. |

| [26] | 胡根华. 人民币与国外主要货币的尾部相依和联动[J]. 统计研究, 2015, 32(5): 40-46. |

| Hu G H. Tailed dependence and co-movements of RMB and foreign currencies[J]. Statistical Research, 2015, 32(5): 40-46. | |

| [27] | 邹玉梅, 范敬雅. 基于广义自回归得分模型的时变D-vine的应用[J]. 数理统计与管理, 2018, 37(1): 74-82. |

| Zou Y M, Fan J Y. Time-varying D-vine based on GAS model and application[J]. Jouranl of Applied Statistics and Management, 2018, 37(1): 74-82. | |

| [28] | Wu X, Zhu S, Wang S. Research on information spillover effect of the RMB exchange rate and stock market based on R-vine copula[J]. Complexity, 2020, 2020: 2492181. |

| [29] | 陈粘, 黄迅, 严晓凤. 结构突变下的高维汇率资产时变投资组合预测研究[J]. 中国管理科学, 2021, 29(11): 13-22. |

| Chen Z, Huang X, Yan X F. Dynamic portfolio forecasting of high-dimensions exchange rate assets under structure break[J]. Chinese Journal of Management Science, 2021, 29(11): 13-22. | |

| [30] | Nelsen R B. An Introduction to Copulas[M]. New York, NY: Springer New York, 1999. |

| [31] | Wang G J, Xie C, He K, et al. Extreme risk spillover network: Application to financial institutions[J]. Quantitative Finance, 2017, 17(9): 1417-1433. |

| [32] | 杨子晖, 王姝黛. 突发公共卫生事件下的全球股市系统性金融风险传染——来自新冠疫情的证据[J]. 经济研究, 2021, 56(8): 22-38. |

| Yang Z H, Wang S D. Systemic financial risk contagion of global stock market under public health emergency: Empirical evidence from COVID-19 epidemic[J]. Economic Research Journal, 2021, 56(8): 22-38. | |

| [33] | Yao H, Zhang W, Wu Z. Monetary policy rule under rare events: With implications by digital finance development[J]. Pacific-Basin Finance Journal, 2024, 85: 102376. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||