主管:中国科学院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

主办:中国优选法统筹法与经济数学研究会

中国科学院科技战略咨询研究院

Chinese Journal of Management Science ›› 2026, Vol. 34 ›› Issue (8): 64-75.doi: 10.16381/j.cnki.issn1003-207x.2024.0800

Previous Articles Next Articles

Gang Li1,2, Boxiong Cao1, Simeng Qin1,2, Jingyi Cheng1, Fang Zhao1,2, Yajing Zhang3( )

)

Received:2024-05-20

Revised:2025-06-14

Online:2026-08-25

Published:2026-07-14

Contact:

Yajing Zhang

E-mail:yajing1990.08@163.com

CLC Number:

Gang Li,Boxiong Cao,Simeng Qin, et al. Research on Personal Default Prediction Methods Based on the AutoGluon Framework[J]. Chinese Journal of Management Science, 2026, 34(8): 64-75.

"

"

| 相关系数 | 关系强度 |

|---|---|

| Corr=0 | 无相关性 |

| 0Corr0.3 | 弱相关性 |

| 0.3≤Corr0.6 | 中相关性 |

| Corr≥0.6 | 强相关性 |

"

"

| 数据集 | 样本 数量 | 非违约样本 | 违约样本 | 分类特征 | 数值特征 | 特征总数 |

|---|---|---|---|---|---|---|

| Lending Club | 31229 | 26455 | 4774 | 7 | 69 | 76 |

| 拍拍贷 | 36055 | 28365 | 7690 | 10 | 9 | 19 |

"

| 预测值0 | 预测值1 | |

|---|---|---|

| 真实值0 | 真阴性(TN) | 假阳性(FP) |

| 真实值1 | 假阴性(FN) | 真阳性(TP) |

"

| 特征选择方法 | 特征集 | 评价指标 | ||

|---|---|---|---|---|

| Type II error | AUC | ACC | ||

| XGBoost | order1PPD | 0.4545 | 0.9310 | 0.9844 |

| XGBoost | order2PPD | 0.5949 | 0.9211 | 0.9821 |

| PI-XGBoost | Order3PPD | 0.2105 | 0.7554 | 0.7869 |

| RF | order1PPD | 0.5677 | 0.9107 | 0.8686 |

| RF | order2PPD | 0.7781 | 0.8705 | 0.8705 |

| PI-RF | Order3PPD | 0.3900 | 0.9232 | 0.9033 |

| GBDT | order1PPD | 0.5245 | 0.9054 | 0.9025 |

| GBDT | order2PPD | 0.6245 | 0.8824 | 0.9245 |

| PI-GBDT | Order3PPD | 0.4066 | 0.7656 | 0.7935 |

| XGBoost | order1LC | 0.2200 | 0.9689 | 0.9562 |

| XGBoost | order2LC | 0.1862 | 0.9678 | 0.9593 |

| PI-XGBoost | order2LC | 0.0987 | 0.9835 | 0.9683 |

| RF | order1LC | 0.1302 | 0.9674 | 0.9639 |

| RF | order2LC | 0.1302 | 0.9700 | 0.9623 |

| PI-RF | Order3LC | 0.1315 | 0.9638 | 0.9646 |

| GBDT | order1LC | 0.1259 | 0.9710 | 0.9650 |

| GBDT | order2LC | 0.1333 | 0.9702 | 0.9634 |

| PI-GBDT | Order3LC | 0.0987 | 0.9815 | 0.9683 |

"

| 数据集 | 样本 数量 | 非违约样本 | 违约样本 | 分类特征 | 数值特征 | 特征总数 |

|---|---|---|---|---|---|---|

| Lending Club | 31229 | 26455 | 4774 | 7 | 36 | 43 |

| 拍拍贷 | 36055 | 28365 | 7690 | 10 | 9 | 19 |

"

| 数据集 | 分类方法 | 样本内 | 样本外 | ||||

|---|---|---|---|---|---|---|---|

| Type II error | AUC | ACC | Type II error | AUC | ACC | ||

| PPD | KNN | 0.1744±0.065 | 0.8918±0.047 | 0.8351±0.047 | 0.1854 | 0.8815 | 0.8350 |

| LGBM | 0.1981±0.048 | 0.9240±0.041 | 0.8677±0.037 | 0.2059 | 0.9265 | 0.8652 | |

| CatBoost | 0.1804±0.039 | 0.9223±0.042 | 0.8714±0.036 | 0.1861 | 0.9213 | 0.8703 | |

| ET | 0.9086±0.055 | 0.7772±0.067 | 0.7895±0.069 | 0.9086 | 0.7355 | 0.7870 | |

| RandomForest | 0.1941±0.036 | 0.9394±0.042 | 0.9320±0.057 | 0.1963 | 0.9300 | 0.9315 | |

| DecisionTree | 0.2142±0.022 | 0.7977±0.060 | 0.8823±0.061 | 0.2168 | 0.8758 | 0.8839 | |

| GradientBoosting | 0.2341±0.211 | 0.9332±0.046 | 0.9176±0.054 | 0.2372 | 0.9219 | 0.9132 | |

| XGBoost | 0.1995±0.019 | 0.9334±0.040 | 0.7831±0.050 | 0.2105 | 0.7554 | 0.7869 | |

| DNN | 0.2154±0.045 | 0.5000±0.000 | 0.7835±0.050 | 0.2172 | 0.5000 | 0.7828 | |

| SuperLearner | 0.2123±0.021 | 0.9137±0.009 | 0.9051±0.006 | 0.1957 | 0.9184 | 0.9112 | |

| AGT-multi-layer-Stacking | 0.0963±0.008 | 0.9342±0.005 | 0.9274±0.006 | 0.0745 | 0.9330 | 0.9219 | |

| LC | KNN | 0.9438±0.012 | 0.5659±0.014 | 0.8252±0.005 | 0.9344 | 0.5593 | 0.8308 |

| LGBM | 0.1235±0.013 | 0.9761±0.004 | 0.9643±0.004 | 0.1227 | 0.9721 | 0.9643 | |

| CatBoost | 0.1267±0.012 | 0.9748±0.004 | 0.9629±0.003 | 0.1270 | 0.9718 | 0.9635 | |

| ET | 0.4983±0.219 | 0.8830±0.062 | 0.9040±0.030 | 0.3947 | 0.8782 | 0.9183 | |

| RandomForest | 0.1275±0.013 | 0.9723±0.007 | 0.9637±0.003 | 0.1244 | 0.9684 | 0.9625 | |

| DecisionTree | 0.3722±0.074 | 0.8964±0.013 | 0.9229±0.010 | 0.3646 | 0.8998 | 0.9364 | |

| GradientBoosting | 0.1280±0.011 | 0.9748±0.006 | 0.9636±0.003 | 0.1269 | 0.9710 | 0.9646 | |

| XGBoost | 0.1350±0.010 | 0.9707±0.005 | 0.9611±0.003 | 0.1407 | 0.9703 | 0.9608 | |

| DNN | 0.1440±0.012 | 0.8472±0.005 | 0.8450±0.002 | 0.1420 | 0.8562 | 0.8460 | |

| SuperLearner | 0.1673±0.014 | 0.9742±0.004 | 0.9594±0.002 | 0.1556 | 0.9684 | 0.9603 | |

| AGT-multi-layer-Stacking | 0.0325±0.006 | 0.9738±0.001 | 0.9642±0.001 | 0.0275 | 0.9769 | 0.9640 | |

"

| 数据集 | 分类方法 | 样本内 | 样本外 | ||||

|---|---|---|---|---|---|---|---|

| Type II error | AUC | ACC | Type II error | AUC | ACC | ||

| PPD | SuperLearner | 0.2123±0.0212 | 0.9137±0.0093 | 0.9051±0.0061 | 0.1957 | 0.9184 | 0.9112 |

| AGT-multi-layer-Stacking-AUC | 0.0963±0.0076 | 0.9342±0.0050 | 0.9274±0.0064 | 0.0745 | 0.9330 | 0.9219 | |

| AGT-multi-layer-Stacking-SR | 0.1140±0.0098 | 0.9630±0.0053 | 0.9119±0.0080 | 0.1190 | 0.9579 | 0.9041 | |

| AGT-multi-layer-Stacking-MCE | 0.0770±0.0042 | 0.926±0.0044 | 0.9150±0.0035 | 0.0676 | 0.9351 | 0.9259 | |

| LC | SuperLearner | 0.1673±0.0144 | 0.9742±0.0041 | 0.9594±0.0019 | 0.1556 | 0.9684 | 0.9603 |

| AGT-multi-layer-Stacking-AUC | 0.1257±0.0200 | 0.9765±0.004 | 0.9648±0.0040 | 0.1257 | 0.9769 | 0.964 | |

| AGT-multi-layer-Stacking-SR | 0.0327±0.0060 | 0.9918±0.002 | 0.9660±0.0040 | 0.0317 | 0.9914 | 0.9629 | |

| AGT-multi-layer-Stacking-MCE | 0.0231±0.0030 | 0.9769±0.004 | 0.9642±0.0040 | 0.0226 | 0.9724 | 0.9646 | |

"

| 数据集 | 分类方法 | 样本内 | 样本外 | ||||

|---|---|---|---|---|---|---|---|

| Type II error | AUC | ACC | Type II error | AUC | ACC | ||

| 德国 | KNN | 0.5922±0.072 | 0.6968±0.070 | 0.7450±0.038 | 0.5484 | 0.6982 | 0.7050 |

| LGBM | 0.5299±0.044 | 0.7796±0.034 | 0.7688±0.027 | 0.4839 | 0.7474 | 0.7600 | |

| CatBoost | 0.4714±0.065 | 0.7591±0.035 | 0.7562±0.029 | 0.4516 | 0.7444 | 0.7500 | |

| ET | 0.5964±0.089 | 0.7060±0.056 | 0.7225±0.049 | 0.6935 | 0.6753 | 0.7200 | |

| RandomForest | 0.6141±0.051 | 0.7936±0.034 | 0.7687±0.032 | 0.5484 | 0.7845 | 0.7550 | |

| DecisionTree | 0.6344±0.082 | 0.6389±0.062 | 0.6762±0.040 | 0.5645 | 0.6510 | 0.6600 | |

| GradientBoosting | 0.5344±0.074 | 0.7920±0.032 | 0.7675±0.045 | 0.4516 | 0.7796 | 0.7450 | |

| XGBoost | 0.5091±0.071 | 0.7793±0.029 | 0.7625±0.023 | 0.4677 | 0.7467 | 0.7450 | |

| AutoGluon | 0.2052±0.028 | 0.8086±0.033 | 0.7775±0.035 | 0.2000 | 0.8050 | 0.7760 | |

| 澳大利亚 | KNN | 0.1382±0.048 | 0.9006±0.029 | 0.8461±0.039 | 0.1034 | 0.8651 | 0.8406 |

| LGBM | 0.1279±0.078 | 0.9422±0.034 | 0.8606±0.058 | 0.0805 | 0.9112 | 0.8768 | |

| CatBoost | 0.1180±0.071 | 0.9370±0.035 | 0.8749±0.037 | 0.1264 | 0.8970 | 0.8406 | |

| ET | 0.1752±0.065 | 0.9029±0.037 | 0.8281±0.050 | 0.1149 | 0.8862 | 0.8406 | |

| RandomForest | 0.1214±0.045 | 0.9370±0.032 | 0.8858±0.036 | 0.1149 | 0.9202 | 0.8478 | |

| DecisionTree | 0.1925±0.073 | 0.8366±0.057 | 0.7989±0.064 | 0.2069 | 0.8231 | 0.7826 | |

| GradientBoosting | 0.1347±0.070 | 0.9322±0.031 | 0.8677±0.053 | 0.1149 | 0.9146 | 0.8333 | |

| XGBoost | 0.1449±0.069 | 0.9377±0.025 | 0.8587±0.046 | 0.1264 | 0.9087 | 0.8623 | |

| AutoGluon | 0.0800 ±0.028 | 0.9362±0.023 | 0.9091±0.024 | 0.0720 | 0.9351 | 0.9072 | |

| 日本 | KNN | 0.1334±0.049 | 0.8938±0.040 | 0.8424±0.033 | 0.9344 | 0.8933 | 0.8696 |

| LGBM | 0.1109±0.049 | 0.9398±0.038 | 0.8749±0.050 | 0.1227 | 0.9052 | 0.8188 | |

| CatBoost | 0.1237±0.041 | 0.9307±0.040 | 0.8658±0.039 | 0.1270 | 0.8878 | 0.7826 | |

| ET | 0.2096±0.107 | 0.8670±0.059 | 0.7989±0.062 | 0.3947 | 0.8387 | 0.7681 | |

| RandomForest | 0.1173±0.053 | 0.9328±0.044 | 0.8767±0.044 | 0.1244 | 0.9082 | 0.8261 | |

| DecisionTree | 0.1838±0.075 | 0.8676±0.064 | 0.8224±0.053 | 0.3646 | 0.8755 | 0.7971 | |

| GradientBoosting | 0.1176±0.052 | 0.9344±0.046 | 0.8768±0.045 | 0.1269 | 0.8931 | 0.8188 | |

| XGBoost | 0.1363±0.060 | 0.9334±0.040 | 0.8531±0.050 | 0.1407 | 0.8866 | 0.8043 | |

| AutoGluon | 0.1451±0.071 | 0.9409±0.041 | 0.8802±0.056 | 0.1594 | 0.9144 | 0.8478 | |

"

"

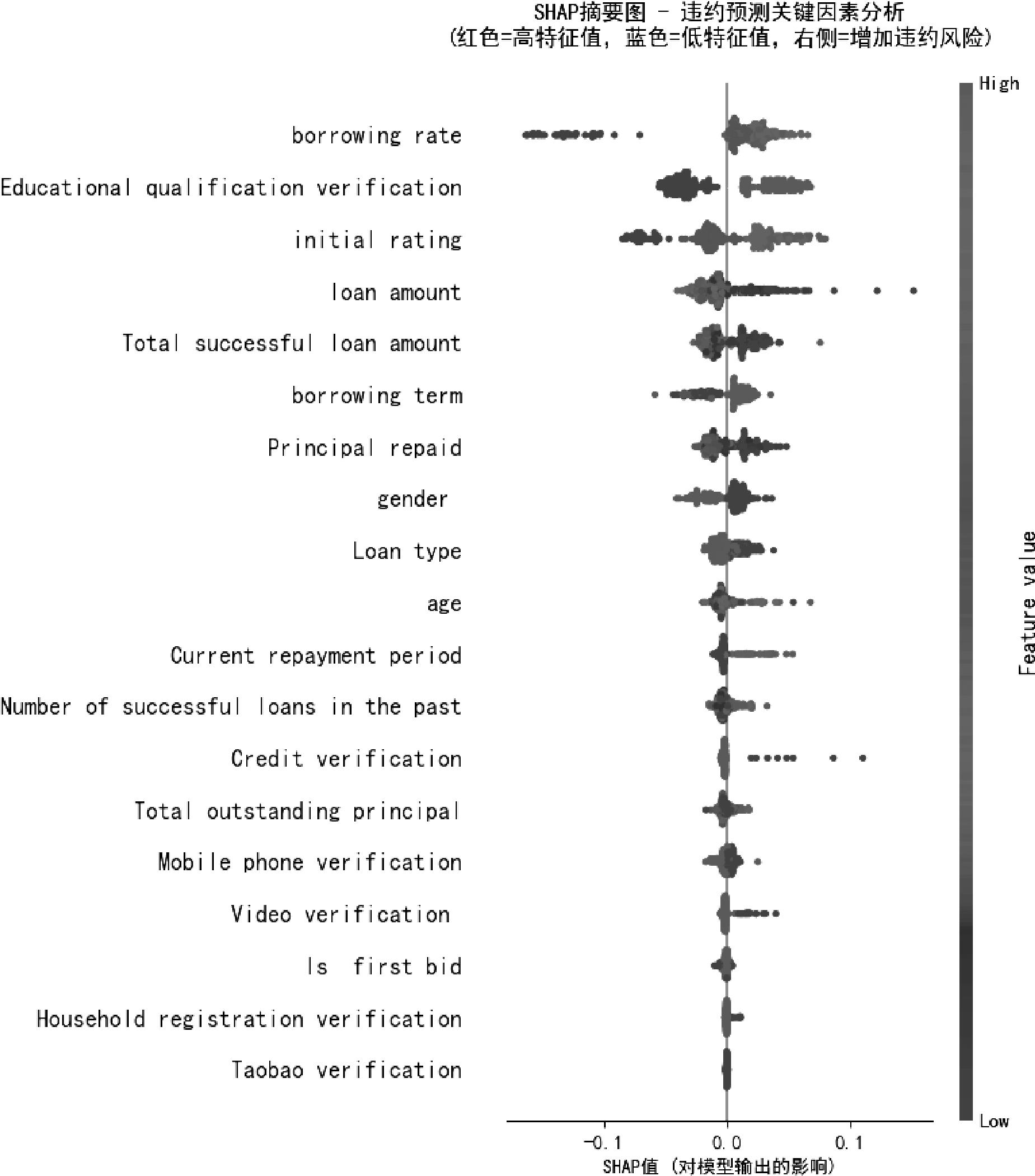

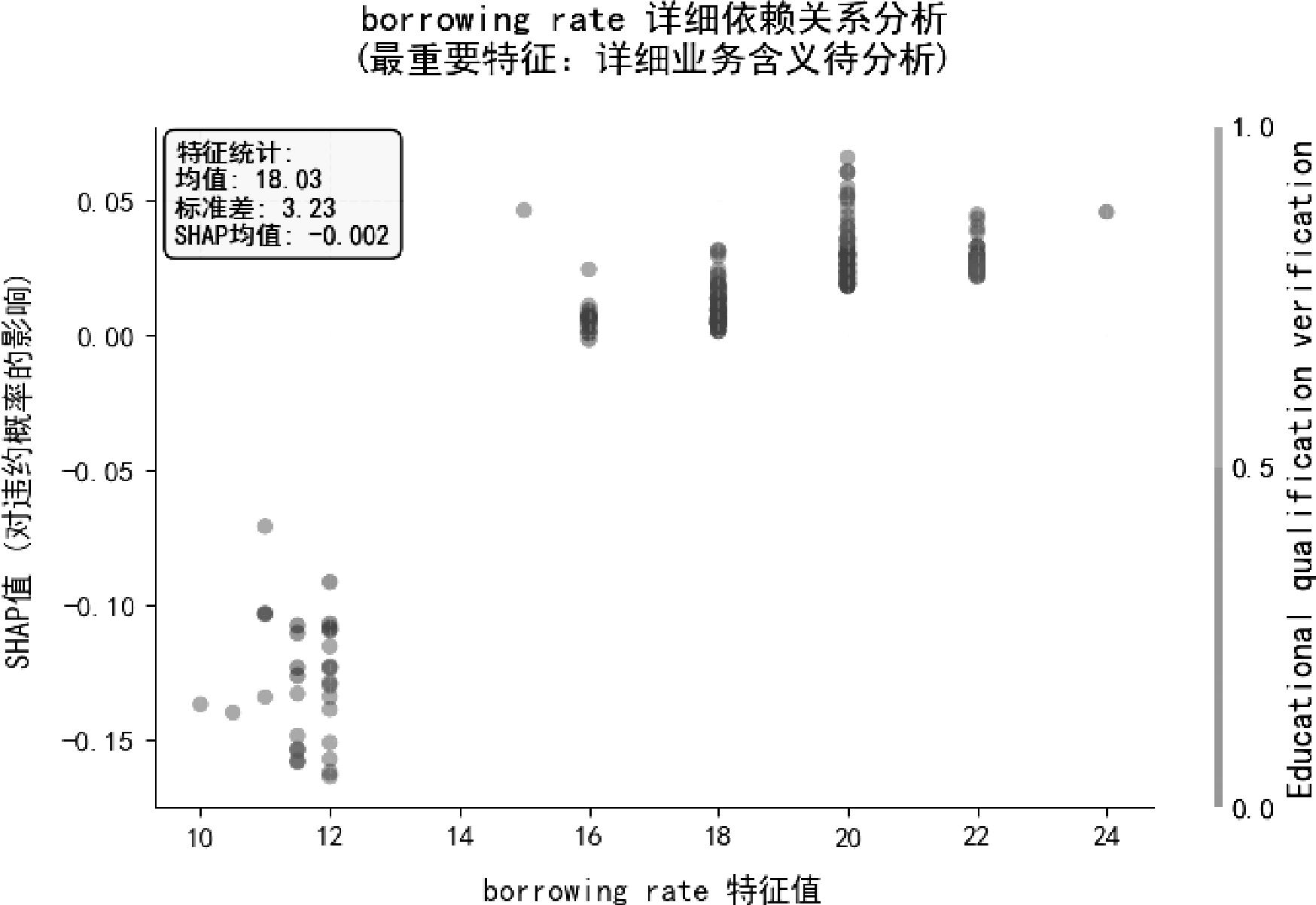

| 特征 | 含义 | SHAP重要性值 |

|---|---|---|

| borrowing rate | 借款利率 | 0.0377 |

| Educational qualification verification | 是否通过教育认证 | 0.0369 |

| initial rating | 初始利率 | 0.0332 |

| loan amount | 借款金额 | 0.0193 |

| Total successful loan amount | 总成功借款金额 | 0.0158 |

| borrowing term | 借款期限 | 0.0151 |

| Principal repaid | 已偿还本金 | 0.0147 |

| gender | 性别 | 0.0127 |

| Loan type | 借款类型 | 0.0091 |

| age | 年龄 | 0.0078 |

"

| [1] | Hand D J, Henley W E. Statistical classification methods in consumer credit scoring: A review[J]. Journal of the Royal Statistical Society Series A: Statistics in Society, 1997, 160(3): 523-541. |

| [2] | Ye X, Dong L A, Ma D. Loan evaluation in P2P lending based on Random Forest optimized by genetic algorithm with profit score[J]. Electronic Commerce Research and Applications, 2018, 32: 23-36. |

| [3] | 沈隆, 周颖. 基于JS散度指标离散化的企业贷款违约预测模型[J]. 中国管理科学, 2024, 32(10): 41-55. |

| Shen L, Zhou Y. Credit scoring model based on JS divergence feature discretization[J]. Chinese Journal of Management Science, 2024, 32(10): 41-55. | |

| [4] | 王小燕, 张中艳, 马双鸽. 基于文本先验信息的贷款信用风险评估模型[J]. 中国管理科学, 2021, 29(5): 34-44. |

| Wang X Y, Zhang Z Y, Ma S G. A loan credit risk model incorporating text prior information[J]. Chinese Journal of Management Science, 2021, 29(5): 34-44. | |

| [5] | Cai S, Zhang J. Exploration of credit risk of P2P platform based on data mining technology[J]. Journal of Computational and Applied Mathematics, 2020, 372: 112718. |

| [6] | 李爱华,刘婉昕,陈思帆,等.面向不平衡数据的SMOTE-BO-XGBoost集成信用评分模型研究[J].中国管理科学,2024,DOI:10.16381/j.cnki.issn1003-207x.2023.0635 . |

| Li A H, Liu W X, Chen S F, et al. Research on SMOTE-BO-XGBoost Ensemble Credit Scoring Model for Imbalanced Data[J]. Chinese Journal of Management Science, 2024,DOI:10.16381/j.cnki.issn1003-207x. 2023.0635 . | |

| [7] | Khandani A E, Kim A J, Lo A W. Consumer credit-risk models via machine-learning algorithms[J]. Journal of Banking Finance, 2010, 34(11): 2767-2787. |

| [8] | Zhang C, Ma Y. Ensemble machine learning: Methods and applications[M]. New York, NY: Springer New York, 2012. |

| [9] | Tsai C F, Hsu Y F, Yen D C. A comparative study of classifier ensembles for bankruptcy prediction[J]. Applied Soft Computing, 2014, 24: 977-984. |

| [10] | Sun J, Lang J, Fujita H, et al. Imbalanced enterprise credit evaluation with DTE-SBD: Decision tree ensemble based on SMOTE and bagging with differentiated sampling rates[J]. Information Sciences, 2018, 425: 76-91. |

| [11] | 彭艳玲, 彭一杰, 周红利, 等. 基于机器学习的农户农地经营权抵押贷款信用风险识别及其损失度量[J]. 系统工程理论与实践, 2025, 45(2): 448-462. |

| Peng Y L, Peng Y J, Zhou H L, et al. Identification and loss measurement of credit risk on rural households' farmland management right mortgages based on the machine learning[J]. Systems Engineering —Theory Practice, 2025, 45(2): 448-462. | |

| [12] | Xia Y, Liu C, Da B, et al. A novel heterogeneous ensemble credit scoring model based on bstacking approach[J]. Expert Systems with Applications, 2018, 93: 182-199. |

| [13] | Yin W, Kirkulak-Uludag B, Zhu D, et al. Stacking ensemble method for personal credit risk assessment in Peer-to-Peer lending[J]. Applied Soft Computing, 2023, 142: 110302. |

| [14] | Chen S, Guo Z, Zhao X. Predicting mortgage early delinquency with machine learning methods[J]. European Journal of Operational Research, 2021, 290(1): 358-372. |

| [15] | Erickson N, Mueller J, Shirkov A,et al. AutoGluon-Tabular:Robust and Accurate AutoML for Structured Data[C]//Proceedings of 7th ICML Workshop on Automated Machine Learning (AutoML 2020), Vienna, Austria, July 17-18 , ICML, 2020: 1-7. |

| [16] | Ge P. Analysis on approaches and structures of automated machine learning frameworks[C]//Proceedings of 2020 International Conference on Communications, Information System and Computer Engineering (CISCE), 2020. Kuala Lumpur, Malaysia, July 3-5, IEEE, 2020: 474-477. |

| [17] | Mangalath Ravindran S, Moorakkal Bhaskaran S K, Ambat S K, et al. An automated machine learning methodology for the improved prediction of reference evapotranspiration using minimal input parameters[J]. Hydrological Processes, 2022, 36(5): e14571. |

| [18] | Chawla N V, Bowyer K W, Hall L O, et al. SMOTE: Synthetic minority over-sampling technique[J]. Journal of Artificial Intelligence Research, 2002, 16: 321-357. |

| [19] | 衣柏衡, 朱建军, 李杰. 基于改进SMOTE的小额贷款公司客户信用风险非均衡SVM分类[J]. 中国管理科学, 2016, 24(3): 24-30. |

| Yi B H, Zhu J J, Li J. Imbalanced data classification on micro-credit company customer credit risk assessment using improved SMOTE support vector machine[J]. Chinese Journal of Management Science, 2016, 24(3): 24-30. | |

| [20] | 迟国泰, 章彤, 张志鹏. 基于非平衡数据处理的上市公司ST预警混合模型[J].管理评论,2020,32(3): 3-20. |

| Chi G T, Zhang T, Zhang Z P. Special treatment warning hybrid model dealing with imbalanced data of Chinese listed companies[J]. Management Review, 2020, 32(3): 3-20. | |

| [21] | 陈妍, 张小威, 金赞, 等. 基于加权GraphSAGE和生成对抗网络的医保欺诈识别方法[J]. 系统工程理论与实践, 2024, 44(2): 732-751. |

| Chen Y, Zhang X W, Jin Z, et al. Medical fraud detection method based on weighted GraphSAGE and generative adversarial network[J]. Systems Engineering-Theory Practice, 2024, 44(2): 732-751. | |

| [22] | 张忠良, 陈愉予, 唐佳怡, 等. 一种基于高斯过采样的集成学习算法[J]. 系统工程理论与实践, 2021, 41(2): 513-523. |

| Zhang Z L, Chen Y Y, Tang J Y, et al. An ensemble learning algorithm with Gaussian-based oversampling[J]. Systems Engineering —Theory Practice, 2021, 41(2): 513-523. | |

| [23] | Tao X, Li Q, Guo W, et al. Self-adaptive cost weights-based support vector machine cost-sensitive ensemble for imbalanced data classification[J]. Information Sciences, 2019, 487: 31-56. |

| [24] | 杨莲, 石宝峰, 董轶哲. 基于Class Balanced Loss修正交叉熵的非均衡样本信用风险评价模型[J]. 系统管理学报, 2022, 31(2): 255-269+289. |

| Yang L, Shi B F, Dong Y Z. A credit risk evaluation model for imbalanced data classification based on class balanced loss modified cross entropy function[J]. Journal of Systems Management, 2022, 31(2): 255-269+289. | |

| [25] | 杨莲, 石宝峰. 基于Focal Loss修正交叉熵损失函数的信用风险评价模型及实证[J]. 中国管理科学, 2022, 30(5): 65-75. |

| Yang L, Shi B F. Credit risk evaluation model and empirical research based on focal loss modified cross—Entropy loss function[J]. Chinese Journal of Management Science, 2022, 30(5): 65-75. | |

| [26] | Zhu B, Qian C, vanden Broucke S, et al. A bagging-based selective ensemble model for churn prediction on imbalanced data[J]. Expert Systems with Applications, 2023, 227: 120223. |

| [27] | Guo Y, Feng J, Jiao B, et al. A dual evolutionary bagging for class imbalance learning[J]. Expert Systems with Applications, 2022, 206: 117843. |

| [28] | 吴红霞, 吴悦, 刘宗田, 等. 基于Relief和SVM-RFE的组合式SNP特征选择[J]. 计算机应用研究, 2012, 29(6): 2074-2077. |

| Wu H X, Wu Y, Liu Z T, et al. Combined SNP feature selection based on relief and SVM-RFE[J]. Application Research of Computers, 2012, 29(6): 2074-2077. | |

| [29] | Altmann A, Toloşi L, Sander O, et al. Permutation importance: A corrected feature importance measure[J]. Bioinformatics, 2010, 26(10): 1340-1347. |

| [30] | Wang B, Ning L, Kong Y. Integration of unsupervised and supervised machine learning algorithms for credit risk assessment[J]. Expert Systems with Applications, 2019, 128: 301-315. |

| [31] | Kuppili V, Tripathi D, Reddy Edla D. Credit score classification using spiking extreme learning machine[J]. Computational Intelligence, 2020, 36(2): 402-426. |

| [32] | Kazemi H R, Khalili-Damghani K, Sadi-Nezhad S. Estimation of optimum thresholds for binary classification using genetic algorithm: An application to solve a credit scoring problem[J]. Expert Systems, 2023, 40(3): e13203. |

| [33] | Han D, Guo W, Chen Y, et al. Personal credit default prediction fusion framework based on self-attention and cross-network algorithms[J]. Engineering Applications of Artificial Intelligence, 2024, 133: 107977. |

| [34] | Lundberg S M, Lee S I. A unified approach to interpreting model predictions[C]//Proceedings of the 31st International Conference on Neural Information Processing Systems, Long Beach, CA, USA, December 4-9, :Curran Associates, 2017: 4768–4777. |

| [1] | Long Shen,Ying Zhou. Credit Scoring Model Based on JS Divergence Feature Discretization [J]. Chinese Journal of Management Science, 2024, 32(10): 41-55. |

| [2] | DONG Bing-jie, CHI Guo-tai. Study on Default Prediction Based on Sentiment Data [J]. Chinese Journal of Management Science, 2023, 31(4): 111-120. |

| [3] | GUO Wei-dong, ZHOU Zach Zhi-zhong, QIAN Chun-tao. Application of Mobile App List in Evaluating Borrowers’ Credit Risk——An Empirical Analysis of an Online Lending Platform [J]. Chinese Journal of Management Science, 2022, 30(12): 96-107. |

| [4] | LIU Wei, XIA Li-qiu. Analysis on the Behavioral Strategy of Participants on Online Lending Market based on Evolutionary Game Theory——A Trilateral Game Perspective [J]. Chinese Journal of Management Science, 2018, 26(5): 169-177. |

| [5] | JIANG Cui-qing, WANG Rui-ya, DIGN Yong. The Default Prediction Combined with Soft Informationin Online Peer-to-Peer Lending [J]. Chinese Journal of Management Science, 2017, 25(11): 12-21. |

| Viewed | ||||||

|

Full text |

|

|||||

|

Abstract |

|

|||||

|

||